Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

* Money is any standardized financial medium for making payments and settling debts.[1]

* Money serves as a:

* Before humans invented money, they traded with barter—the direct exchange of goods and services.[3] [4]

* People used common goods such as cattle, tea, and raw metals for barter.[5] Other barter items included tools, jewelry, and weapons.[6]

* Barter was inefficient because it required the “double coincidence of wants”—the condition of “two people each having a good that the other wants at the right time and place to make an exchange.”[7]

* As far back as the 13th century BC, societies in Asia, Africa, and Europe began using seashells known as cowries for money.[8]

Cowries

Photo credit: Fotolia/jamocki

* At the end of the Stone Age, China developed a currency system using metals. Copper and bronze were cast to depict cowrie shells, tools, and knives.[9]

* The “stater” coin of the Lydian Empire (modern Turkey) is the earliest known currency issued by a government. It was first minted around the second half of the seventh century BC. The value of the coin was based on a strict weight standard.[10] [11]

* War and trade spread coins from Lydia across the Persian Empire, Greece, Sicily, Macedonia, and India.[12]

* The gold solidus, first minted by the Roman Emperor Constantine in the early fourth century AD, is one of history’s most famous coins. It was produced at a constant weight for 700 years.[13]

* England standardized the silver penny around 765 AD, and it was widely used in Northern Europe.[14]

* English money was known as “sterling,” and 240 silver pennies made up one “pound sterling.” The silver used for the coins had to meet strict purity standards. From 1078 until 1914, the term “pound sterling” meant high-quality and stability.[15]

* In mainland Europe, gold coins—such as florins from Florence and Ghent, and ducats from Venice—were the primary coins used in international trade.[16]

* Paper money was invented and developed in China several centuries before Europe:

* During the 1500s, silver mined at St. Joachimsthal in Bohemia was used to mint the thaler, which circulated in Germany for more than 300 years.[18] The Spanish version of the thaler—the peso—was used in the Americas during the colonial era and became the basis for the American dollar.[19] [20]

* In 1717, the United Kingdom’s Master of the Mint, Sir Isaac Newton, defined the pound sterling’s value in terms of gold rather than silver for the first time.[21]

* Starting with the Coinage Act of 1792, the United States used a bimetallic currency standard. This means the dollar was defined by its value in both silver and gold.[22]

* In the early 1800s, Britain officially adopted the gold standard.[23] During the 1870s, Germany, Holland, Austro-Hungary, Russia, Scandinavia, and France also switched to the gold standard.[24]

* The United States effectively adopted the gold standard in the 1870s, formalizing this with the Specie Payment Resumption Act of 1875 and the Gold Standard Act of 1900.[25] [26] [27]

* In 1913, in response to a series of banking crises, the U.S. Congress established the Federal Reserve.[28]

* During World War I, many countries suspended the gold standard and began printing money to finance the war effort, which led to high inflation.[29] By 1919, the United States was the only world power that still followed the gold standard.[30]

* After World War I, Britain and other European countries briefly returned to the gold standard.[31]

* Britain left the gold standard in 1931 amidst the Great Depression, and the value of British money dropped significantly.[32] [33] Other nations that relied heavily on Britain for trade then dropped the gold standard to prevent Britain’s weak currency from pricing their “goods out of the large market which Britain provided.”[34]

* In 1934, the United States reduced the dollar’s value by raising the price of gold from $20.67 to $35 per ounce. The federal government also stopped allowing Americans to exchange their dollars for gold and confiscated privately-held gold.[35] [36] [37]

* In 1944, delegates from 44 nations met in Bretton Woods, New Hampshire to establish a new international monetary system. These countries agreed to value their currencies according to the U.S. dollar for international trade. In turn, the U.S. dollar would keep a fixed value of $35 per ounce of gold.[38]

* The Bretton Woods delegates also created the International Monetary Fund and the International Bank for Reconstruction and Development (now called World Bank Group) to help run the new system.[39]

* In 1971, Republican President Richard Nixon stopped allowing the exchange of dollars into gold, thus ending the Bretton Woods system. Most of the world’s currencies therefore had no link to a metal standard. Per the Federal Reserve Bank of Richmond:

* From 1965 to 1982, inflation in the United States increased multiplicatively during an era known as the Great Inflation. The annual inflation rate ranged from just over 1% in 1964 to over 14% in 1980.[41] [42] [43]

* In the early 1980s, the Federal Reserve enacted policies to raise private-sector interest rates. These high interest rates reduced inflation amid the recession of 1981–82.[44] [45] [46]

* The period from the mid-1980s to 2007 is known as the Great Moderation, when inflation stabilized and the economy expanded.[47] Part of this expansion took place in housing-related industries such as construction and mortgage borrowing.[48]

* From 1998 to 2006, home prices rose at unprecedented rates, and in 2007, they began to sharply decline.[49] As housing prices fell, financial institutions lost money because of borrowers defaulting on mortgages. These losses had “large spillover effects” on other parts of the economy. This led to the Great Recession that began in December 2007 and ended in 2009.[50] [51] [52]

* In response to the Great Recession, the Federal Reserve:

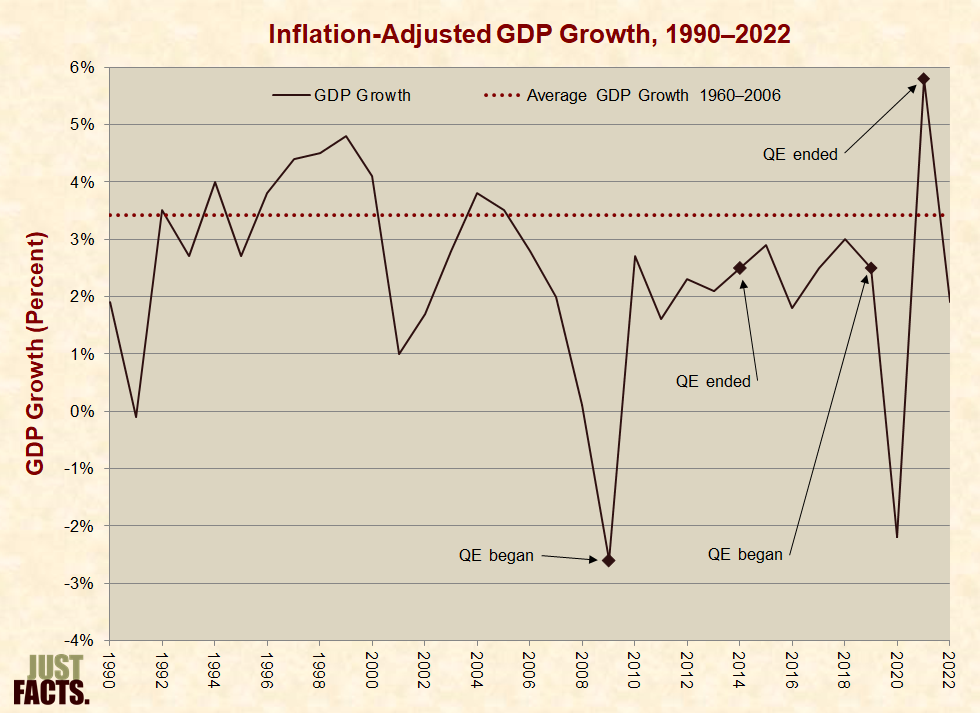

* Recovery from the Great Recession was a period of slow growth.[61] From 2010 to 2016, real (inflation-adjusted) gross domestic product (GDP) growth averaged 2.2% annually. From 1946 to 2007, the average annual growth rate was 3.2%.[62]

* During the Covid-19 outbreak of 2020—amid government-mandated shutdowns of businesses in nearly every state that cost millions of jobs[63] [64]—the Federal Reserve:

* A digital currency, virtual currency, or digital asset is a computerized representation of money. This includes traditional currencies that are transferred electronically and currencies that exist mainly in digital form.[74] [75]

* A virtual currency is stored and/or traded digitally but is not legally recognized by a government. Some, such as the gold that players earn in the online game World of Warcraft, cannot be converted into other currencies. Others, such as the now-defunct e-Gold, can be exchanged into traditional currencies. Most virtual currencies are centralized, meaning they have an administrator that controls its supply and makes rules for its use.[76] [77]

* Cryptocurrencies are a subset of virtual currencies that do not have central administrators. They use automated computer networks, instead of banks, to verify and process payments. Cryptocurrencies can be exchanged for traditional currencies.[78] [79] [80] [81] [82]

* In 2009, an anonymous computer programmer invented Bitcoin—the first cryptocurrency.[83] [84]

* Another cryptocurrency, XRP, was introduced by the company Ripple in 2012. It is primarily used as a currency to facilitate cross-border payments between banks.[85] [86]

* The computer network groups together a set of transactions, called a block. Computers across the network confirm the transactions contained in the block. Each block then becomes part of a shared public record—a block chain.[87] [88] [89]

* Because payment verifications are automated and recorded across an entire network, cryptocurrency trade is neutral and transparent.[90] [91] [92] [93]

* Cryptocurrency payments can be made at any time, since they do not rely on a third party bank for confirmation. They are also settled more quickly than traditional transactions. The process for a merchant to receive payment from a credit card transaction takes 24 to 72 hours. An average Bitcoin transaction takes 10 minutes, and an average XRP transaction takes four seconds.[94] [95] [96]

* Transactions using cryptocurrencies may have lower fees than traditional credit card transactions because they do not involve multiple intermediaries. In some cases, they have no transaction fee, whereas businesses typically pay 2% to 3% in fees to credit card companies.[97] [98] [99]

* The blockchain technology used in cryptocurrency transactions makes it nearly impossible to reverse payments. Businesses may see this as a benefit because they are not at risk for chargebacks by customers.[100] [101]

* The value of a virtual currency is not tied to a commodity such as gold and is not declared to be legal tender by the U.S. government.[102] [103] [104] [105] [106] Instead, it has value because people agree to use and accept it as payment.[107] [108]

* The value of a cryptocurrency can change quickly.[109] [110] [111] According to Lael Brainard, a member of the Federal Reserve’s Board of Governors:[112]

* Inflation is a general rise in prices for goods and services due to a decline in a currency’s value or purchasing power.[114] [115] [116]

* Inflation often occurs when governments create and circulate more money than needed by their nations’ economies. This causes the purchasing power of money to shrink and prices to increase.[117] [118] [119] [120] [121]

* Governments engage in inflationary policies to effectively tax citizens at higher rates and/or to default on their national debts.[122] [123] [124] [125]

* Per a 2002 speech by Ben Bernanke of the Federal Reserve:

* When governments create more money than needed by their economies, this doesn’t always raise the prices of consumer products and services. Instead, the additional money can inflate the prices of assets like stocks, real estate, and commodities. This is called “asset inflation,” and it increases the wealth of those who already own assets while making those assets less affordable for everyone else.[127] [128] [129] [130] [131]

* Government actions can have inflationary effects. For example:

* Market forces can have inflationary effects. For example:

* Deflation is the opposite of inflation—prices generally fall as the purchasing power of money increases.[138]

* Major causes of deflation or deflationary effects include the following:

* For facts about the “Inflation Reduction Act of 2022,” read this article from Just Facts.

* The Federal Reserve has recorded several measures of money in the U.S. economy:

* From 1959 to 2022, M2 and M3 relative to the size of the nation’s gross domestic product varied as follows:

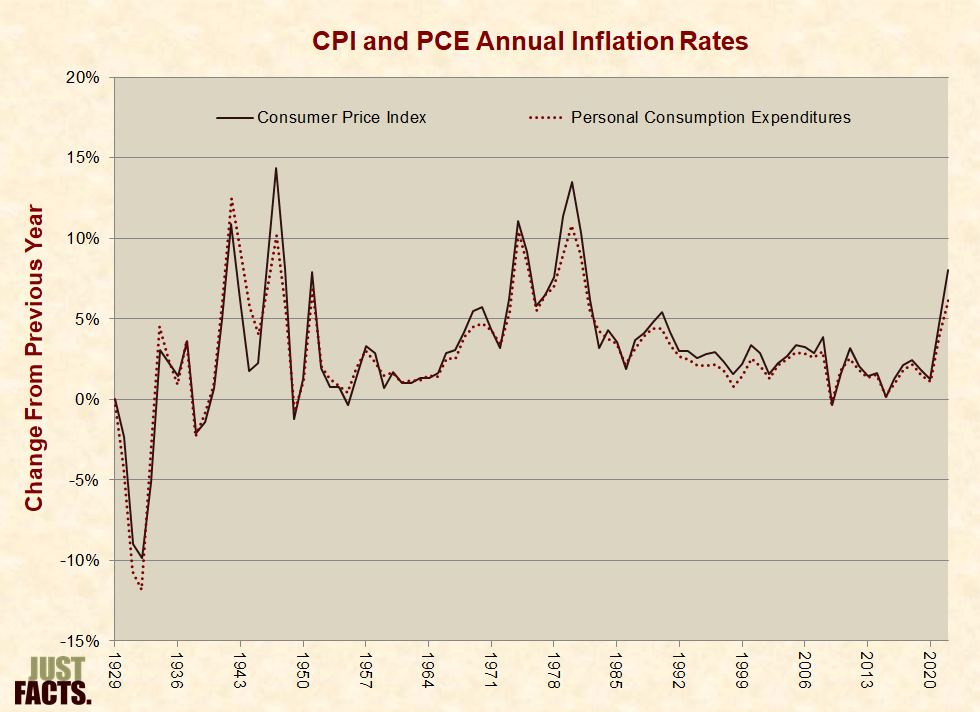

* Inflation is typically measured by comparing prices for a wide range of goods and services over time.[151]

* The Federal Reserve mainly uses the Personal Consumption Expenditures (PCE) index—which is calculated by the U.S. Department of Commerce—to guide its policy decisions.[152]

* The Bureau of Labor Statistics calculates the Consumer Price Index (CPI), which is the most widely used measure of inflation. It affects the income of about 80 million people because it is used to adjust Social Security, food stamp, military retirement, and federal civil service retirement benefits. It is also used to determine school lunch prices and adjust the federal income tax code.[153]

* Although PCE and CPI follow the same general trends, there are differences between them:

* From 1929 to 2022, the annual inflation rate as measured by CPI ranged from –9.9% to 14.4%, with a median of 2.8% and an average of 3.2%. During the same time period, the annual inflation rate as measured by PCE ranged from –11.8% to 12.5%, with a median of 2.5% and an average of 2.9%:

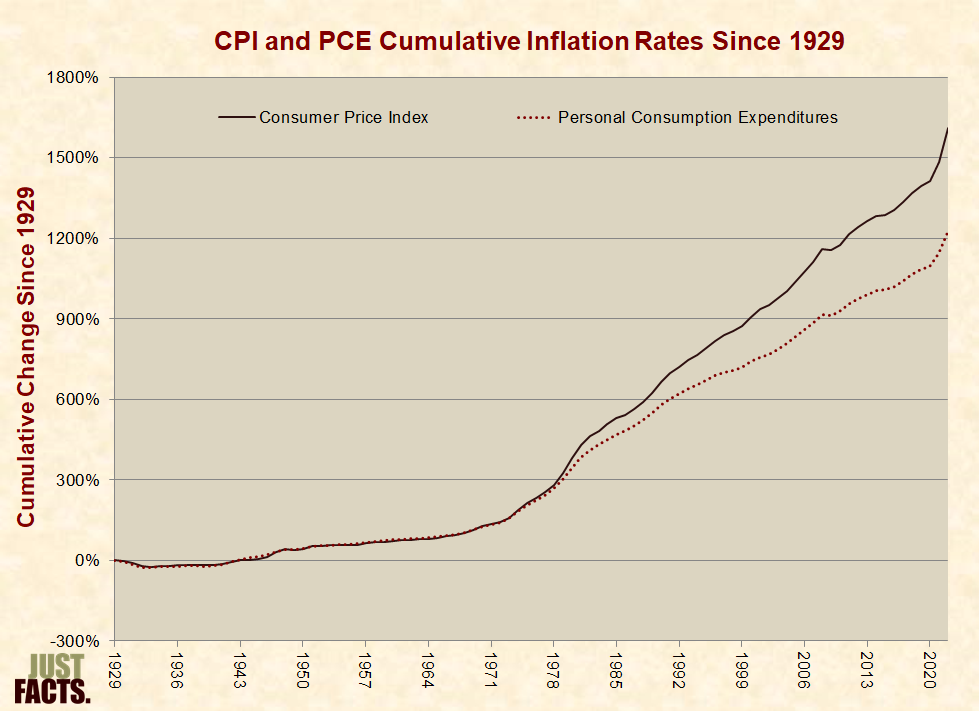

* From 1929 to 2022, the cumulative inflation rate was 1,611% as measured by CPI and 1,221% as measured by PCE:

* The Producer Price Index is a rough approximation of the wholesale prices paid by retailers for the products they sell to consumers.[162]

* From 1947 to 2022, the annual changes in consumer prices (CPI) and wholesale prices (PPI) varied as follows:

* From 1947 to 2022, the cumulative inflation rate was 1,212% as measured by CPI, 883% as measured by PCE, and 851% as measured by PPI:

* Wide variations in inflation can inflict serious damage on an economy.[165] [166] [167] [168] Per the U.S. Federal Reserve:

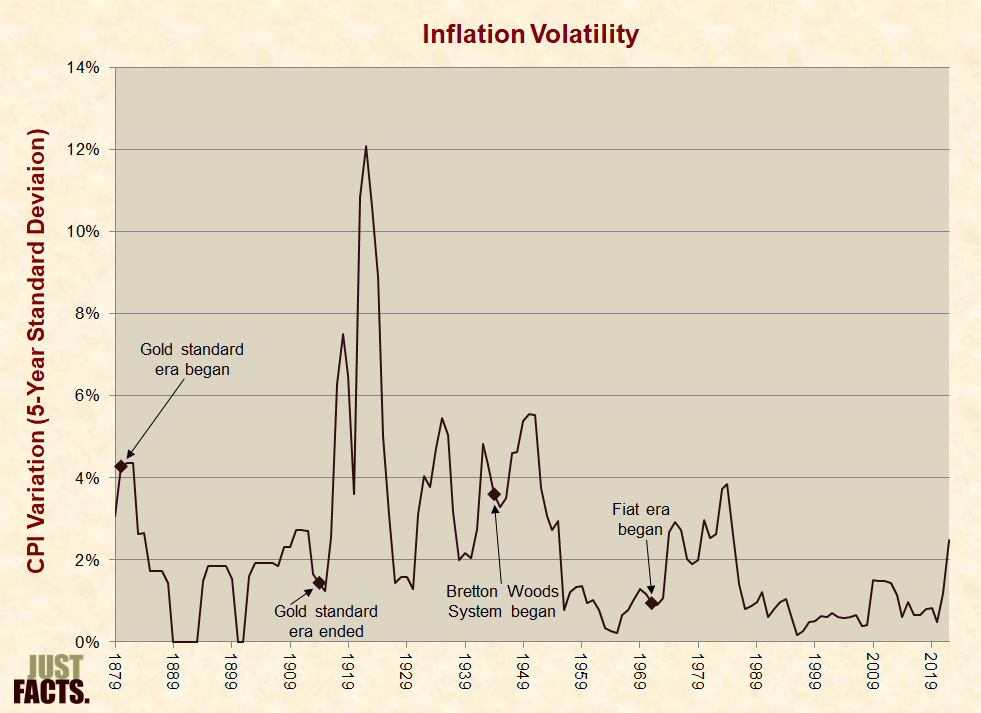

* Generally, periods of high inflation are associated with high volatility.[170] [171] [172]

* A key measure of inflation volatility is its standard deviation—or how widely inflation varies from its average over a specified time.[173] [174] [175]

* Since 1879, the 5-year standard deviation of the Consumer Price Index has varied as follows:

* Some individuals have claimed that the government’s indexes undercount inflation. These critics object to the following aspects of the government’s methodology:

* John Williams, founder of Shadow Government Statistics,[184] has claimed that the government undercounts inflation by 7% each year.[185]

* In 2008, the Bureau of Labor Statistics (BLS) published an article to address such criticisms. It presented the following facts:

* The Billion Prices Project is a non-government academic program that tracks price trends.[193] Its data—collected daily from thousands of online sources—shows a close correlation with government inflation data.[194]

* Inflation or deflation is most damaging if it changes rapidly and unexpectedly, which can inflict serious damage on an economy.[195] [196] [197]

* Unexpected inflation may hurt consumers because prices on goods can change daily, but wages do not always adjust immediately.[198]

* Unexpected inflation can hurt lenders, who are repaid with money worth less than when the terms of the loan were negotiated. This benefits borrowers because they repay their debts with less valuable money.[199]

* Since unexpected inflation can hurt lenders, it may make financial institutions less willing to make loans, particularly long-term loans.[200]

* Inflation also causes:

* When governments create more money than required by their economies, this doesn’t always raise the prices of consumer products and services. Instead, the additional money can inflate the prices of assets like stocks, real estate, and commodities. This is called “asset inflation.”[205] [206] [207] [208] [209] [210]

* Asset inflation can manifest in economic measures like:

* Asset inflation increases the wealth of those who already own assets, while making assets less affordable for people with little wealth.[220] [221] [222] [223] [224]

* Per the journal Environment and Planning, asset inflation:

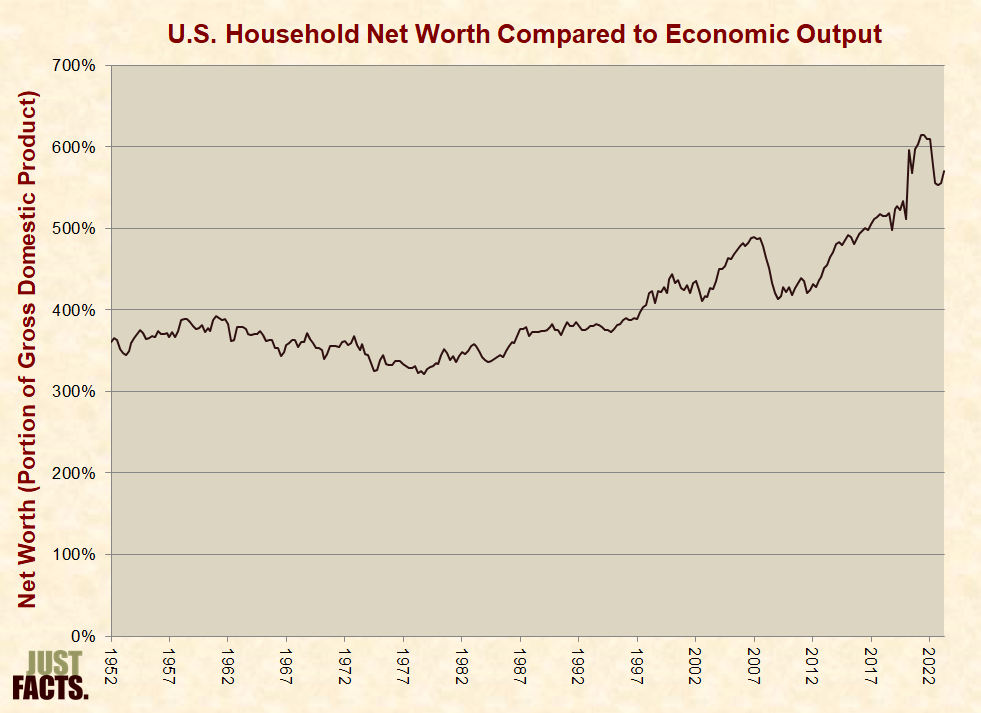

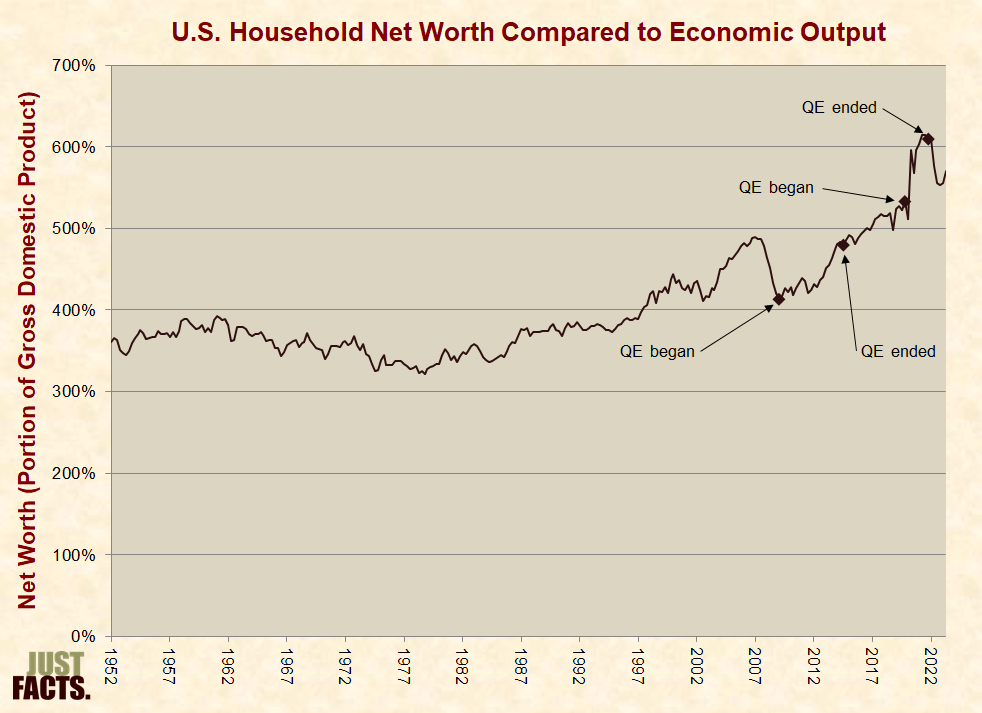

* One way to measure asset inflation is to compare a country’s net wealth to the size of its economy.[226] [227] From 2009 (when the Federal Reserve began a policy called quantitative easing) through the second quarter of 2023, this measure increased by 38%, or by 158 percentage points:

* During deflation, borrowers are less willing to take out loans because they will repay the lender with more valuable money.[230]

* Spending goes down during periods of deflation, because consumers wait for prices to drop even lower before making purchases or investments.[231] [232]

* Reduced spending and falling prices cause lower sales and profits. Lower demand for workers, and workers being unwilling to take pay cuts, can cause higher levels of unemployment.[233] [234]

* In periods of falling prices, the Federal Reserve takes action to reduce private-sector interest rates by reducing the federal funds rate—the interest rate banks charge each other for short-term loans. Lower interest rates encourage more borrowing and spending. This increases demand for products, which then leads to increased prices and wages.[235] [236]

* If the federal funds rate is near zero and there is still deflation, the Federal Reserve may employ quantitative easing. This means the Federal Reserve creates new money to purchase large quantities of assets, such as mortgage-related investments and federal bonds.[237] [238] In 2010, Federal Reserve Chairman Ben Bernanke said these purchases were made to “improve market functioning and to push longer-term interest rates lower.”[239] [240]

* The Federal Reserve used quantitative easing during the Great Depression of the 1930s, the Great Recession that began in 2007, and the Covid-19 pandemic of 2020.[241] [242] [243] [244] [245] [246] [247]

* A gold standard is a monetary system that defines a country’s currency as a fixed amount of gold. The government promises to exchange its currency into gold at a fixed rate.[248]

* If a country’s currency is not convertible into a commodity like gold, it is fiat money. Fiat money has value because a government declares that it is legal tender. The dollar’s status as legal tender is further supported by laws that requires tax debts to be paid in dollars. Its value is not tied to a commodity such as gold or silver.[249] [250]

* Historically, English money was known as “sterling,” and starting in the 10th century, 240 silver pennies made up one “pound sterling.”[251] In 1717, the United Kingdom’s Master of the Mint, Sir Isaac Newton, defined the pound sterling’s value in terms of gold rather than silver for the first time.[252]

* During the American Revolution, the Continental Congress issued paper money known as the “Continental.” It was not defined in terms of any precious metal and was easily counterfeited. Thus, it quickly lost its purchasing power, giving rise to the expression “not worth a Continental.”[253] [254]

* Starting with the Coinage Act of 1792, the United States used a bimetallic currency standard. This means the dollar was defined by its value in both silver and gold.[255]

* In December 1861, the United States suspended its link to a metal standard due to the costs of the Civil War.[256] Its currency was therefore fiat during this period.[257] In 1879, the U.S. government resumed converting paper currency into gold.[258] [259]

* In the early 19th century, Britain officially adopted the gold standard.[260] During the 1870s, Germany, Holland, Austro-Hungary, Russia, Scandinavia, and France also switched to the gold standard.[261]

* In 1900, the United States officially adopted the gold standard with the Gold Standard Act.[262]

* The period from 1880 to the outbreak of World War I in 1914 is known as the “classical gold standard” era.[263] During that time:

* During World War I, many countries suspended the gold standard and began printing money to finance the war effort, which led to high inflation.[269] By 1919, the United States was the only world power that still followed the gold standard.[270]

* After World War I, Britain and other European countries briefly returned to the gold standard.[271] During the Gold Exchange Era of 1925–1931, countries agreed to keep a supply of gold, U.S. dollars, or British pounds. The United States and United Kingdom agreed to hold gold.[272] [273]

* Britain left the gold standard in 1931 amidst the Great Depression, and the value of British money dropped significantly.[274] [275] Other nations that relied heavily on Britain for trade then dropped the gold standard to prevent Britain’s weak currency from pricing “their goods out of the large market which Britain provided.”[276]

* In 1944, delegates from 44 nations met in Bretton Woods, New Hampshire, to establish a new international monetary system. These countries agreed to value their currencies according to the U.S. dollar for international trade. In turn, the U.S. dollar would keep a fixed value of $35 per ounce of gold.[277]

* The Bretton Woods system required the United States to maintain a large supply of gold. In 1971, Republican President Richard Nixon ended the dollar’s link to gold.[278] Per the Federal Reserve Bank of Richmond:

* When the final gold link was severed in August 1971, the U.S. dollar and all other world currencies became fiat. Thus, their values began to rise and fall against one another based on supply and demand, financial speculation, and government currency manipulation.[280] [281]

NOTE: When interpreting the facts in this section, it is important to realize that association does not prove causation, and it is often difficult to determine causation in economics and other social sciences. This is because numerous variables might affect a certain outcome, and there is frequently no objective way to identify all of these factors and determine which is causing the others and to what degree.

* Under a strict gold standard, the amount of money in a country’s economy was determined by the amount of gold the government had in its possession. Prices were expected to remain stable if gold production kept up with the economy’s demand for money.[282] [283]

* Unexpected changes in the supply of gold were associated with short-term price instability.[284] [285] However, annual inflation rates in economies on a gold standard had long-term price stability.[286]

* When a country’s currency is fiat, the monetary policies of its central bank affect inflation. The Federal Reserve is responsible for deciding the amount of money in circulation and “maintaining confidence” in the currency’s value.[287] [288] [289] [290]

* During the classical gold standard era (1880–1914), the annual inflation rate in the U.S. averaged about 0.2% per year. From 1972 (after the end of the Bretton Woods System) to 2022, the average annual inflation rate was 4.0%:

* Wide variations in inflation can inflict serious damage on an economy.[292] [293] [294] [295] Per the U.S. Federal Reserve:

* A key measure of inflation volatility is its standard deviation—or how widely inflation varies from its average over a specified time.[297] [298] [299]

* During the classical gold standard era (1880–1914), the annual inflation rate in the U.S. had a standard deviation of 2.1%. From 1972 (after the end of the Bretton Woods System) to 2022, its standard deviation was 2.9%.[300]

* Since 1879, the 5-year standard deviation of the Consumer Price Index has varied as follows:

* Exchange rates—the prices of one currency in relation to others—play an important role in a country’s trade performance. They have large impacts on international trade and overall financial performance.[302] [303] For example:

* A country can influence exchange rates and its ratio of imports to exports by changing the value of its currency. In 1934, the U.S. reduced the dollar’s value in terms of gold by 69%. In 1949, the U.K. devalued the pound by 30%. In each of these cases, devaluing the currency encouraged exports by making the country’s goods cheaper for other countries to buy.[310] [311] [312] [313]

* When two countries’ currencies are defined in terms of the same material, such as gold, their exchange rate is fixed.[314] [315] For example, when the United States dollar and British pound were both valued in gold during the classical gold standard era (1880–1914), the exchange rate for £1 stayed steady at $4.86.[316]

* When countries do not have a common standard of value for their currencies, their exchange rates float. This means they fluctuate based on supply and demand, financial speculation, interest rates, and government currency manipulation.[317] [318]

* Since 1792, the U.S. dollar and British pound have alternated nine times between fixed exchange rates under the gold standard and floating exchange rates. During these periods, the British pound’s value against the dollar fluctuated as follows:

* In the centuries before 1971, the major economies generally used gold and silver coins for currency, and later, paper money backed by stockpiles of the precious metals.[322]

* In 1944, the Bretton Woods system was established with the U.S. dollar defined at $35 per ounce of gold. All other member countries set fixed exchange rates to the dollar.[323]

* In the 1960s, the U.S. struggled to maintain its role in the Bretton Woods system due to rising spending and inflation. In 1971, Republican President Richard Nixon suspended the government’s policy of exchanging dollars for gold in international markets, to stop the outflow of its gold supply. Within two years, exchange rates began to fluctuate.[324]

* Since 1973, member countries of the International Monetary Fund have chosen their own exchange rate systems. None of these countries are tied to a gold standard.[325]

* The International Monetary Fund (IMF) defines these exchange rate systems as:

* According to a 2023 report, the IMF has 190 member nations plus three territories, and Hong Kong and Macao. It classifies their exchange rate systems as follows:[330]

* The Federal Reserve was established in 1913 and serves as the central bank of the United States.[332]

* In 1775 during the Revolutionary War, the Continental Congress began printing paper money to finance the war. This currency was not backed by precious metals and was easily counterfeited. It quickly lost value, leading to the saying “not worth a Continental.”[333] [334]

* In 1788, the U.S. Constitution gave Congress the power to coin money, regulate its value, and punish those who counterfeit it.[335] [336]

* After the Constitution was ratified, Alexander Hamilton, the nation’s first treasury secretary, proposed the creation of a national bank. In 1791, the First Bank of the United States opened in Philadelphia.[337]

* The First Bank of the United States was authorized by Congress to hold $10 million in capital. It was mostly owned by private interests but was directed to serve a public purpose.[338] It made loans, accepted deposits, sold U.S. government bonds, and issued paper money backed by gold and silver.[339]

* In 1811, Congress did not renew the bank’s charter. Opponents of the national bank considered it unconstitutional and felt it infringed on states’ rights.[340] [341]

* From 1811 to 1816, state banks expanded and issued a wide variety of currencies.[342] These banks stopped backing their paper currencies with silver and gold, and the large volume of money that entered the economy caused the currencies to lose value. In order to fund the War of 1812, the federal government incurred large debts because the money it had lost its purchasing power.[343] [344]

* In 1816, Congress chartered the Second Bank of the United States. This bank redeemed state-issued paper money for gold and silver, which helped stem inflation.[345] [346] President Andrew Jackson considered the bank unconstitutional, and in 1836 he vetoed its re-charter.[347]

* The years from 1837 to 1863 are called the Free Banking Era. Private, state-chartered banks issued their own paper money without federal regulation. Although banks needed to follow state laws, government permission was not needed to open a bank.[348] [349] [350]

* The National Banking Act of 1863 established nationally chartered banks and required that they back their paper money with federal government bonds. The act was later amended to tax currencies issued by state banks. This reduced the amount of state-issued paper money and left the country with a uniform currency.[351] [352]

* From the end of the Civil War in 1865 to 1907, a series of bank panics caused many banks to fail. These panics occurred when a large number of customers withdrew their money out of fear that banks would run out of money.[353] [354] [355]

* In the same era, Canadian banks remained stable and again during the series of bank failures and panics that struck the United States in the 1920s and 1930s. Canadian banks were able to create multiple branches nationwide, which allowed them to spread risk across different markets. State-chartered banks in the United States were not allowed to cross state lines, and in some states, they were not allowed to create any branches.[356] [357] [358]

* Attempts in the United States to mirror the Canadian banking model failed until the 1980s, and full nationwide branch banking was not allowed until 1994. Groups such as farmers and small banks feared that branch banking would negatively affect their interests, and they argued that interstate banking violates states’ constitutional rights.[359] [360]

* In response to a bank panic in 1907, Congress established a Monetary Commission in 1908.[361] [362] The commission, led by Republican Senator Nelson Aldrich, made a plan to create a new central bank.[363] The plan, popularized in a book titled The Creature From Jekyll Island,[364] was criticized by progressives for giving control to bankers rather than the government.[365] [366]

* The Aldrich plan was abandoned when Democrat Woodrow Wilson, a founder of modern liberalism, became president of the United States.[367] In 1913, Wilson signed the Federal Reserve Act into law, creating a central banking system with a balance of power between government and private banks but giving the bulk of this power to government.[368] [369] [370] [371] [372]

* One provision of the Federal Reserve Act gave member banks a way to retire their paper currencies. This moved the country to a centrally controlled currency under the Federal Reserve (the Fed).[373] [374] [375]

* In 1927, Congress re-chartered the Federal Reserve ahead of schedule for an unlimited term. The Great Depression, which began in the United States in 1929, soon followed.[376] [377]

* Congress updated the Federal Reserve System with laws in:

* The Federal Reserve System is comprised of:

* The Board of Governors of the Federal Reserve:

* There are 12 regional Federal Reserve Banks,[390] and each:

* The Federal Open Market Committee:

* The Federal Reserve System is controlled by:

* The Board of Governors of the Federal Reserve:

* The Federal Reserve’s 12 regional Reserve Banks are separately incorporated,[412] and each has a:

* Congress established the Federal Reserve’s authority in 1913.[420] The Fed is governed by federal laws, including those that require:

* In 2023, U.S. Congressman Thomas Massie (R–KY) introduced the Federal Reserve Transparency Act. It would allow audits on areas of the Fed that are currently restricted, including policy decisions and international transactions.[446]

* The Federal Reserve System has five main responsibilities:

* “Monetary policy” refers to the Fed’s actions to achieve three goals set by Congress: maximum employment, stable prices, and moderate long-term interest rates. The Fed’s monetary policies directly affect interest rates, which in turn, affect credit flows, stock prices, exchange rates, business investments, employment, inflation, and other aspects of the economy.[449]

* One of the main ways in which the Federal Reserve implements monetary policy is by influencing the federal funds rate, which is the interest rate that banks charge each other for short-term loans. This rate has wide-ranging ripple effects on the economy.[450] [451]

* Prior the Great Recession of 2007–2009,[452] [453] the Federal Reserve influenced the federal funds rate primarily by ordering the New York Federal Reserve Bank to buy or sell government bonds on the open market.[454] [455] [456] When the Federal Reserve sought to:

* During the Great Recession and the Covid-19 pandemic, the Federal Reserve took actions that caused banks to have excessive amounts of money to lend. This made the previous methods of influencing the federal funds rate ineffective.[459] [460] [461] [462]

* Since the Great Recession, the Federal Reserve has mainly influenced the federal funds rate by paying interest to banks and other financial institutions to store money at regional Federal Reserve Banks.[463] [464]

* From 1954 to 2023, the federal funds rate ranged from 0% to 19%, with an average of 5% and median of 4%:

* Until 2020,[466] the Federal Reserve also implemented monetary policy by requiring member banks to keep a specific portion of the money their customers deposited in cash (either in their own vaults or at regional Federal Reserve Banks). When the Board of Governors allowed banks to decrease this portion, banks could loan more money to the public, which caused more money to circulate through the economy.[467] [468]

* The Federal Reserve stopped requiring banks to keep a specific portion of their assets in cash during 2020 after the following events:

* Since the start of the Federal Reserve policy of paying interest to banks on cash they store at regional Federal Reserve Banks, rates have varied as follows:

* From 1973 to 2023, the total cash assets of commercial banks relative to their liabilities ranged from 3% to 22%, with a median and average of 10% .

* The Federal Reserve also implements monetary policy through the following mechanisms:

* In addition to conducting monetary policy, Federal Reserve Banks provide services to:

NOTE: When interpreting the facts in this section, it is important to realize that association does not prove causation, and it is often difficult to determine causation in economics and other social sciences. This is because numerous variables might affect a certain outcome, and there is frequently no objective way to identify all of these factors and determine which is causing the others and to what degree.

* The Federal Reserve has three priorities set by Congress in 1977: (1) maximum employment, (2) stable prices, and (3) moderate long-term interest rates.[500] [501]

* World War I began in 1914, less than one year after the Federal Reserve System was created. The war created tremendous upheaval in the international financial system, including the suspension of the international gold standard, major increases in government debt, and soaring inflation.[502] [503] [504]

* The interwar years from 1919 to 1939 were a time of financial chaos. After World War I, European nations tried to restore the pre-war gold standard but abandoned it amidst the Great Depression.[505]

* The Great Depression was more severe and longer-lasting in the United States than in many other countries. Some economists believe the Fed’s policies from 1929 to 1937 contributed to the country’s economic problems.[506] [507]

* During World War II, the Federal Reserve focused on financing the United States’ war efforts. This focus diverted the Federal Reserve from its primary mission.[508]

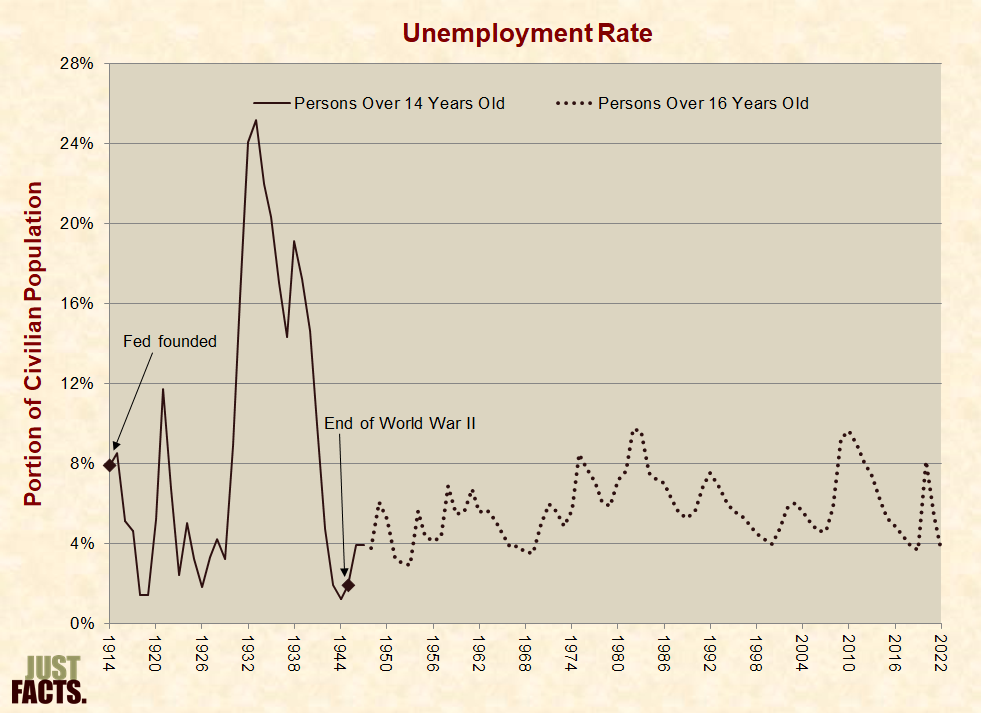

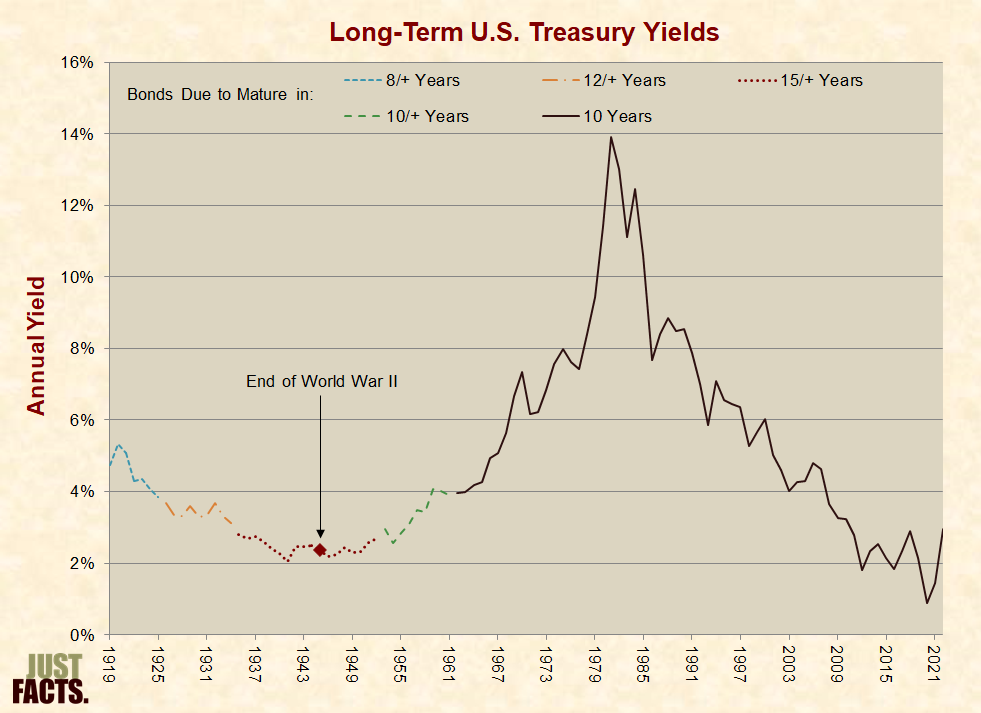

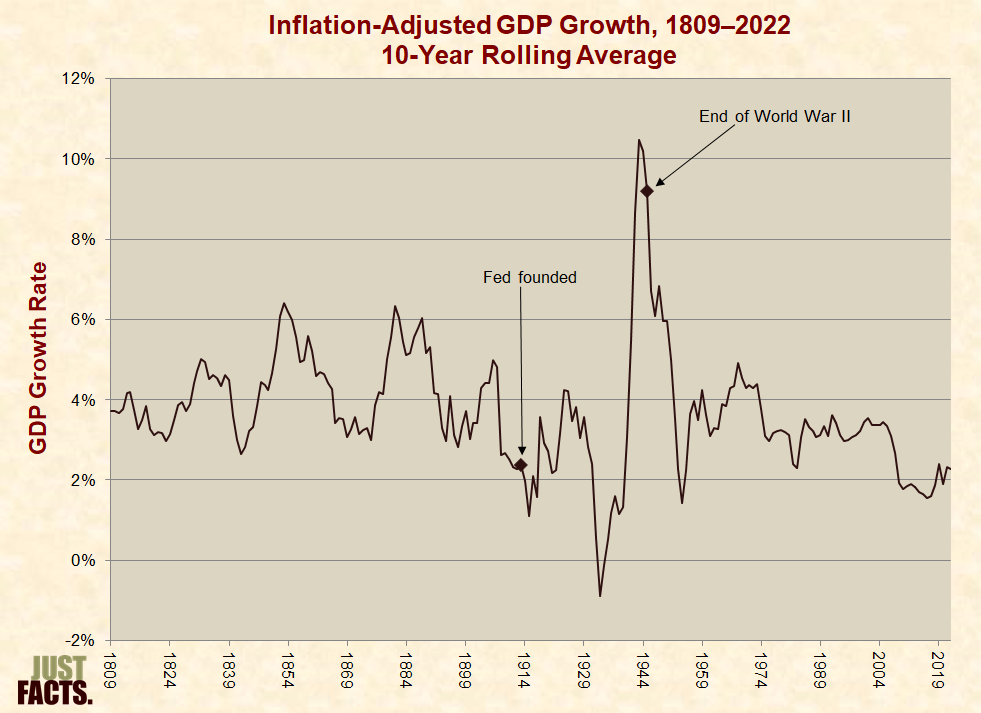

* The forthcoming facts about unemployment, inflation, interest rates, and economic growth cover the Federal Reserve’s tenure from 1914 (when available) to the latest available data. They also isolate the post-World War II period (1946–present) to remove the impact of the two world wars and the Great Depression. When available, data from the period prior to the Fed’s creation in 1913 is also provided.

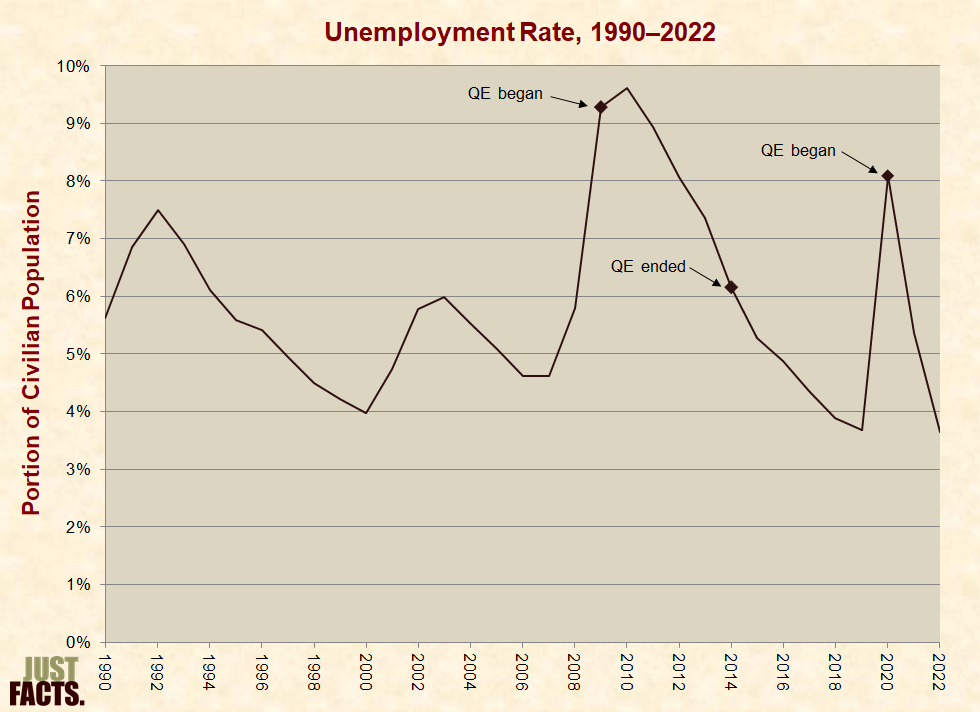

* During the Fed’s tenure, the average annual unemployment rate has ranged from 1% to 25%, with a median of 6% and an average of 7%. Post-World War II, the average annual unemployment rate has ranged from 3% to 10%, with a median and an average of 6%:

* Stable prices occur when the economy is not experiencing high or unexpected rates of inflation or deflation.[512] [513] [514]

* The average inflation rate:

* Wide variations in inflation can inflict serious damage on an economy.[521] [522] [523] [524] Per the U.S. Federal Reserve:

* A key measure of inflation volatility is its standard deviation—or how widely inflation varies from its average over a specified time.[526] [527] [528]

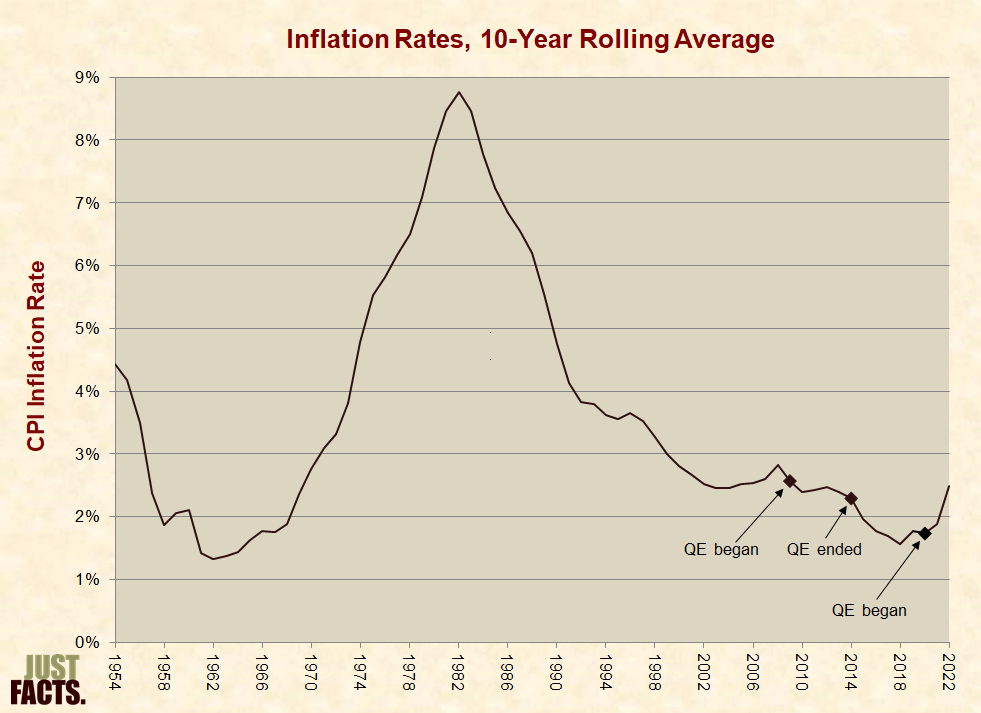

* Inflation’s standard deviation:

* Since 1879, the 5-year standard deviation of the Consumer Price Index has varied as follows:

* Low interest rates help encourage spending in the economy by making it cheaper to borrow money.[533] [534]

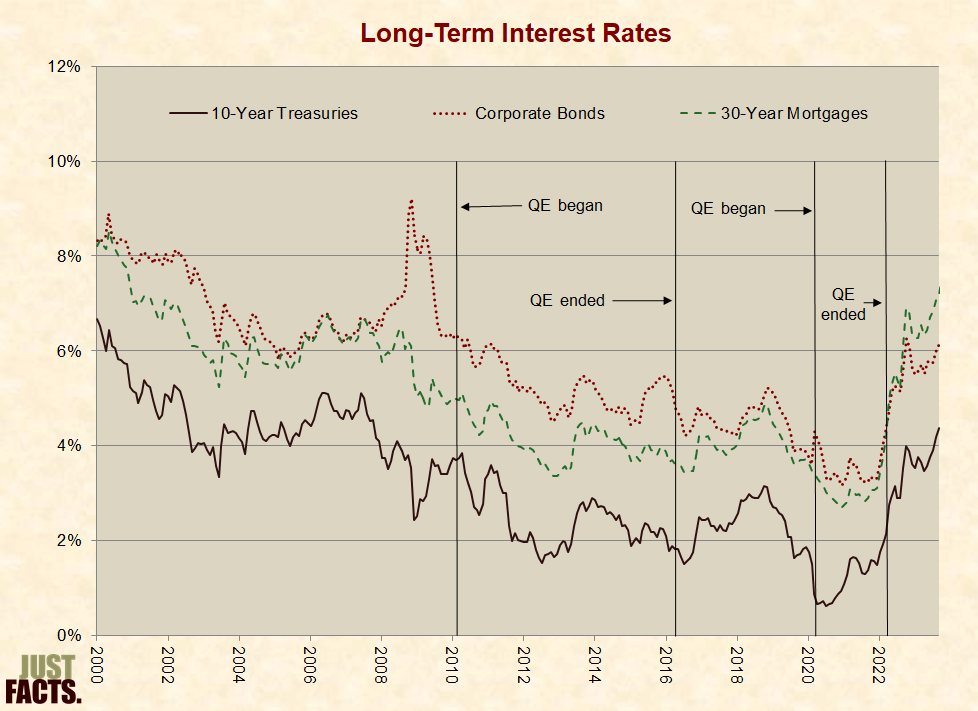

* For the Fed’s tenure starting in 1919, annual interest rates on long-term federal bonds have ranged from 1% to 14%, with an average of 5% and a median of 4%. Post-World War II, they have ranged from 1% to 14%, with an average and a median of 5%:[535]

* Gross domestic product (GDP) measures the value of the goods and services produced by an economy during a specific time period. GDP is defined by the equation: Hours worked × Labor productivity.[538] [539]

* The growth rate of inflation-adjusted GDP is a key indicator of the health of an economy. A strong growth rate is often associated with higher rates of employment, while low or negative rates may accompany employment declines.[540]

* Average annual inflation-adjusted GDP growth was 4.0% prior to the Fed’s creation, 3.3% during the Fed’s full tenure, and 2.9% post-World War II:

* Quantitative easing is an unconventional Federal Reserve policy implemented during the Great Depression of the 1930s, the Great Recession that began in 2007, and the Covid-19 pandemic of 2020.[542] [543] [544] [545] [546] [547] [548] [549]

* During recessions, the Federal Reserve seeks to encourage economic activity by enacting policies to reduce the federal funds rate, which is the interest rate that banks charge each other for short-term loans. This rate has wide-ranging ripple effects on the economy.[550] [551] [552]

* From 1998 to 2006, home prices rose at unprecedented rates, and in 2007, they began to sharply decline.[553] As housing prices fell, financial institutions lost money because of borrowers defaulting on mortgages. These losses had “large spillover effects” on other parts of the economy. This led to the Great Recession that began in December 2007 and ended in 2009.[554] [555] [556]

* In a financial crisis like the Great Recession, the Federal Reserve may push the federal funds rate close to zero, as it did in December of 2008. Since the rate could not be reduced any further, and economic conditions did not improve, the Federal Reserve implemented quantitative easing.[557]

* During the quantitative easing of the Covid-19 pandemic, the Fed created trillions of dollars of new money to purchase financial assets, such as:[563] [564] [565]

* The stated purpose of quantitative easing (QE) during the Great Recession was to help the economy by reducing interest rates.[568]

* In January 2009, as the Fed initiated QE, then-Federal Reserve Chairman Ben Bernanke said the program’s main purpose was to make it easier and less costly for households and businesses to borrow money. “If the program works as planned,” he said, “it should lead to lower rates and greater availability of consumer and small business credit.”[569] [570] [571]

* With easier and cheaper access to credit, businesses are able to make investments, such as buying new equipment. Per an article published by the Federal Reserve Bank of St. Louis in 2011, “over time, new business investments should bolster economic activity, create new jobs, and reduce the unemployment rate.”[572]

* By making large-scale purchases of long-term federal debt, the Fed reduced the amount of debt available for sale to the public, which placed downward pressure on interest rates.[573] [574]

* The Fed also purchased mortgage-related investments and debt from government-sponsored enterprises like Fannie Mae, Freddie Mac, and the Federal Home Loan Banks. The purpose of these purchases was to reduce mortgage rates in order to support the housing sector.[575] [576] Chairman Bernanke said that “bringing down mortgage rates” stimulates “home-buying, construction, and related industries.”[577]

* Bernanke also stated that the Fed was “compelled” to implement QE because “many financial institutions” had incurred “substantial losses” in the housing market crash, and these firms still owned a “large quantity” of “troubled” and “illiquid assets of uncertain value.” These were called “toxic assets” and consisted largely of subprime and other high-risk mortgages that had fueled the housing boom and subsequent crash.[578] [579] [580] [581]

* Since financial institutions had suffered large losses and still owned stockpiles of bad investments that they could not sell without taking further losses, these firms could not effectively loan, borrow, or trade. Bernanke said this was problematic because “our economic system is critically dependent on the free flow of credit.”[582]

* In order to open the flow of credit, the Fed began purchasing toxic assets from financial institutions and providing large loans to these firms. This provided the firms with additional cash and “reduced the total amount of risky assets investors held.”[583] [584] [585]

* As the Fed began implementing QE, Chairman Bernanke stated that:

* When the Fed implemented QE during the Covid-19 pandemic of 2020, Federal Reserve Chairman Jerome Powell said the program’s main purpose was to “safeguard financial markets” and:

* At the beginning of the Great Recession, the Federal Reserve set up an emergency lending program to stimulate the flow of money in the economy. From December 2007 to September 2008, the Fed funded loans to banks and financial firms by selling off $315 billion of its federal bonds.[590] [591] [592]

* In September 2008, the Fed ran out of federal bonds to sell but continued to make loans by creating new money. These new loans increased the Fed’s assets from less than $1 trillion to over $2 trillion in approximately 3 months. Fed Chairman Ben Bernanke referred to this policy as “credit easing.”[593] [594]

* In November 2008, the Federal Reserve announced its plan to begin a quantitative easing (QE) program. The original plan was to purchase large amounts of mortgage-related investments and debt belonging to housing-related government-sponsored enterprises like Fannie Mae, Freddie Mac, and the Federal Home Loan Banks. The stated goal was to make mortgages cheaper and more available to the public.[595]

* In March of 2009, the Fed announced its plan to expand the size and scope of its purchases to include long-term government debt. The stated goal was to help improve credit conditions outside of the housing industry.[596]

* From March 2009 to March 2010, during what is now called QE1, the Fed purchased:

* Due to continued low inflation and economic weakness, the Federal Reserve initiated a second round of large-scale asset purchases called QE2. From November 2010 to June 2011, it purchased $600 billion of long-term federal debt.[599]

* From September 2011 to December 2012, the Fed implemented a Maturity Extension Program, which is also known as “Operation Twist.” The Fed sold short-term bonds and purchased an equal amount of long-term federal bonds. The goal was to reduce long-term interest rates without further expanding the Fed’s balance sheet.[600] [601]

* In September 2012, the Fed began QE3—a phase of large-scale asset purchases without a set end date or total cost estimate. It began purchasing $40 billion of mortgage-related investments each month, then in January 2013 added $45 billion of long-term federal bonds per month. Monthly purchases were tapered down until QE3 ended in October 2014 with a total cost of approximately $1.6 trillion.[602] [603] [604]

* In March 2020, the Fed responded to the Covid-19 pandemic and state government shutdowns of “nonessential businesses” with an effective QE.[605] [606] [607] Per Fed Chairman Jerome Powell: [608]

* From the inception of the Federal Reserve in 1913 through 2007,[610] the Fed accumulated $1.3 trillion of inflation-adjusted net assets. Due to QE and related policies that the Fed has implemented since then, its assets grew:

* From the inception of the Federal Reserve in 1913 through 2007,[616] the Fed accumulated net assets equal to 6% of the nation’s annual economic output, or gross domestic product (GDP). Due to QE and related policies that the Fed has implemented since then, its assets grew:

[617] [618] [619] [620] [621] [622]

* Since 1933, the portion of the national debt borrowed from the Federal Reserve has varied as follows:

NOTE: When interpreting the facts in this section, it is important to realize that association does not prove causation, and it is often difficult to determine causation in economics and other social sciences. This is because numerous variables might affect a certain outcome, and there is frequently no objective way to identify all of these factors and determine which is causing the others and to what degree.

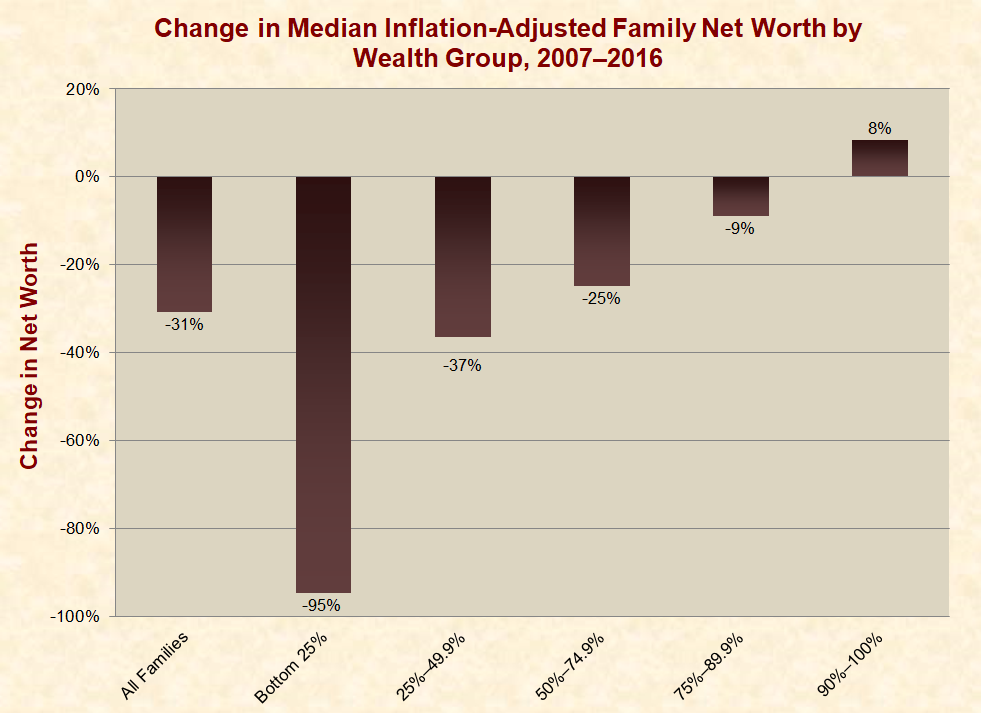

* Net worth is the difference between people’s assets and liabilities.[627]

* From 2007 to 2016, during and after the Great Recession and implementation of quantitative easing, the inflation-adjusted median net worth of U.S. families declined for all wealth groups except the top 10%:

* Market income consists of non-government income, such as labor income, business income, and capital gains.[629]

* From 2007 to 2016, during and after the Great Recession and implementation of quantitative easing, inflation-adjusted market income for the:

* From 2007 to 2016, during and after the Great Recession and implementation of quantitative easing, the annual unemployment rate fell from about 5% to about 4%:

* The labor force participation rate is the portion of people aged 16 and older who are “either working or actively seeking work.”[640] [641] [642]

* From 2007 to 2016, during and after the Great Recession and implementation of quantitative easing, the annual labor force participation rate fell from 66% to 63%:

* Mortgage rates began declining when the Federal Reserve announced its plan to purchase mortgage-related investments in November of 2008, even though it had not made any purchases yet.[646] [647]

* From 2007 to 2016, during and after the Great Recession and implementation of quantitative easing, interest rates on:

* Inflation is a general rise in prices for goods and services due to a decline in a currency’s value or purchasing power.[652] [653] [654] The most widely used measure of inflation is the Consumer Price Index (CPI).[655]

* In 2009, the annual change in CPI dropped below zero to –0.4%. Inflation since 2010 has been positive, which offset fears of a deflationary crisis.[656] [657]

* Some economists worried that the money created during QE would cause high inflation.[658] [659] However, from 2007 to 2016, the average inflation rate was lower than the 10-year rolling average over the preceding 4 decades:

* Inflation likely remained low because the newly created money stayed in banks’ reserves and was not circulated into the economy. If banks begin loaning out these funds, the money supply will expand, and inflation may increase.[663] [664] [665] [666]

* When governments create more money than required by their economies, this doesn’t always raise the prices of consumer products and services. Instead, the additional money can inflate the prices of assets like stocks, real estate, and commodities. This is called “asset inflation.”[667] [668] [669] [670] [671]

* Since quantitative easing’s purpose is to reduce interest rates,[672] its implementation may cause asset inflation. For instance, lower interest rates result in:

* Asset inflation can manifest in economic measures like:

* Asset inflation increases the wealth of those who already own assets, which makes those assets less affordable for others.[688] [689] [690] [691] [692]

* Per the journal Environment and Planning, asset inflation:

* One way to measure asset inflation is to compare a country’s net wealth to the size of its economy.[694] [695] Since 2007, the total net worth of U.S. households has increased from 488% of the nation’s annual economic output to 571%:

* Gross domestic product (GDP) measures the value of the goods and services produced by an economy during a specific time period. GDP is defined by the equation: Hours worked × Labor productivity.[701] [702]

* From 2007 to 2016, during and after the Great Recession and implementation of quantitative easing, inflation-adjusted economic growth did not reach its average of 3.4% over the prior half century:

* The Dow Jones Industrial Average is an indicator that measures the value of a group of large, fiscally sound U.S. companies from various industries.[706] [707]

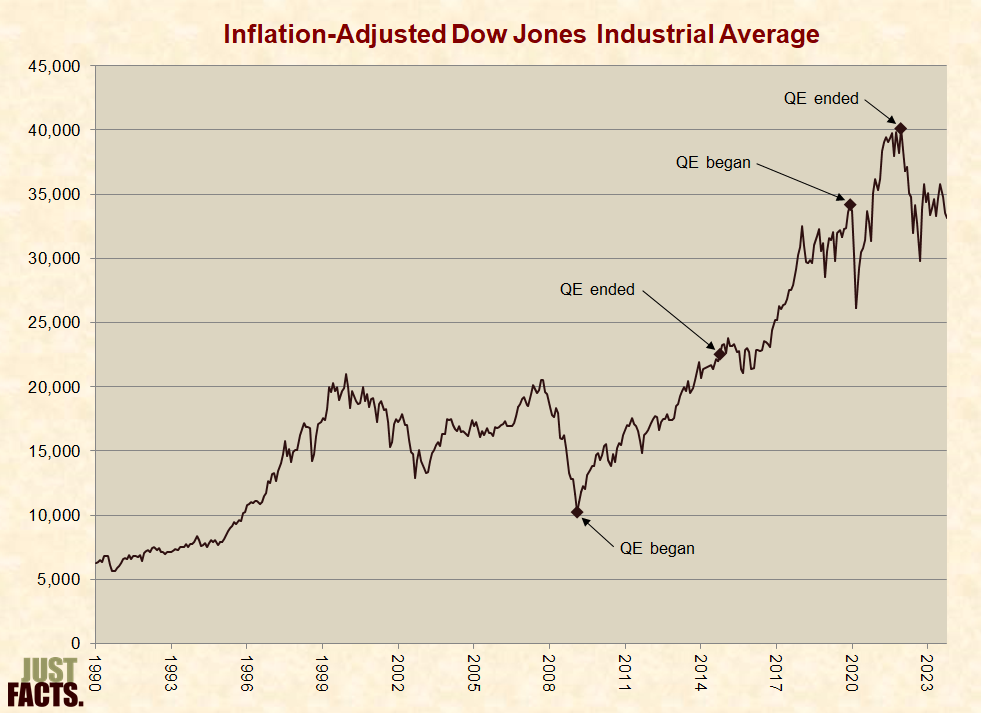

* From 2007 to 2016, during and after the Great Recession and implementation of quantitative easing, the Dow Jones inflation-adjusted average rose about 18%:[708]

* In 2021, Democratic President Joe Biden asserted he was “very fastidious about not talking to” the Federal Reserve in order to maintain the Fed’s independence.[713]

* In 2021, Biden nominated Jerome Powell to a second term as chair of the Federal Reserve in order to ensure “stability and independence” at the Fed.[714] [715]

* In 2022, amid rapidly rising inflation,[716] Biden reiterated the Fed’s “primary responsibility to control inflation” and that he “won’t meddle with the Fed, but” he “will tackle high prices.”[717] [718]

* As a 2016 presidential candidate, Republican Donald Trump criticized the Federal Reserve, saying that it had created “a big, fat, ugly bubble,” and was supporting “a very false economy” with its policies.[719]

* In a 2015 interview, Trump stated that the United States used to be solid “because it was based on a gold standard.” He also stated that it would be difficult to implement the gold standard “at this point” because “we do not have the gold.”[720]

* After taking office, Trump repeatedly said he doesn’t like a “strong” dollar, meaning he doesn’t want the exchange rate to rise excessively.[721] [722]

* In 2017, Trump named Jerome Powell to chair the Federal Reserve. Powell expected to continue the policies put in place by his predecessors.[723] [724]

* In 2019, prior to the Covid-19 pandemic and economic recession,[725] [726] Trump urged the Fed to lower interest rates and resume quantitative easing to boost the economy.[727] [728] [729]

* Senator Rand Paul (R-KY) has criticized the Federal Reserve’s actions during the financial crisis. In 2016, he wrote that the Fed’s power has been “unchecked” and “arguably unconstitutional.”[730]

* Paul proposed legislation in 2011, 2013, 2015, 2017, 2019, 2021, and 2023 entitled the Federal Reserve Transparency Act and commonly known as “Audit the Fed.” Each version of the bill would require the Government Accountability Office to complete an audit of the Federal Reserve Board and Federal Reserve banks.[731] [732] [733] [734] [735] [736] [737]

* In 2020, then Senate Minority Leader Charles “Chuck” Schumer (D-NY) stated that the Fed “must make decisions on an objective economic analysis and judgement.”[738] [739]

* In 2017, Schumer was disappointed when Fed Chairwoman Janet Yellen was not nominated for a second term. He previously advocated for her original nomination in 2013.[740] [741]

* In 2014, Schumer stated that the Federal Reserve should “be careful” about raising interest rates because of the “overwhelming problem” of slow job growth.[742]

* Schumer supported Ben Bernanke’s nomination as chairman in 2005 and later applauded Bernanke’s “steady hand” during the financial crisis.[743] [744]

* Schumer has voted against the “Audit the Fed” bill.[745]

* Senator Ted Cruz (R-TX) cosponsored the 2013 and 2015 “Audit the Fed” bills.[746] [747]

* During a November 2015 Republican presidential debate, Cruz referred to the Federal Reserve as “philosopher kings” and called for “sound money and monetary stability, ideally tied to gold.”[748]

* In a December 2015 hearing with Chairwoman Janet Yellen, Cruz blamed the Federal Reserve’s policies for the 2008 financial crisis.[749]

* Senator Bernie Sanders (I-VT) has criticized the Federal Reserve, calling it a “rigged economic system.” In 2015—when he was a candidate for the Democratic presidential nomination—he wrote that the Fed should undergo a “full and independent audit” every year. He further wrote that “banking industry executives” serving on the Fed’s boards have “conflicts of interest” and should be replaced with “representatives from all walks of life.”[750]

* Sanders has also criticized actions of the Fed. For example, he disagreed with the Fed’s decision to begin raising interest rates in 2015 while unemployment was still over 4%. Rather than paying interest to banks, he proposed that the Fed should charge the banks “a fee that would be used to provide direct loans to small businesses.”[751]

* In 2009, Democratic President Barack Obama nominated Ben Bernanke for a second term as Chairman of the Federal Reserve Board. Bernanke was first appointed by Republican President George W. Bush.[752]

* At the end of Bernanke’s term, Obama nominated Janet Yellen as Chairwoman of the Federal Reserve Board.[753]

* During his tenure, Obama defended the Fed’s quantitative easing program.[754] His administration opposed the 2015 “Audit the Fed” legislation.[755] [756]

* In 2015, U.S. Rep. Kevin Brady (R-TX) introduced a bill that would establish a Centennial Monetary Commission. The Commission would assess the Federal Reserve’s historical impact on the U.S. economy and recommend policies for the future.[757]

* In 2012, Brady proposed the Sound Dollar Act, which would have limited the Fed’s priorities to promoting long-term price stability and establishing a way to measure whether that goal is achieved.[758]

* U.S. Rep. Bill Huizenga (R-MI) proposed the Fed Oversight Reform and Modernization (FORM) Act of 2015. It would require the Federal Reserve to adopt a rules-based monetary policy of its choosing. The Fed could stop following the rule, provided it explains its decision to Congress.[759]

* In 2013, U.S. Rep. Nancy Pelosi (D-CA) supported Janet Yellen’s nomination as Chairwoman of the Federal Reserve, and in 2017 praised Yellen’s tenure. Pelosi called on Yellen’s successor, Jerome Powell, to continue Yellen’s policies.[760] [761]

* Pelosi opposes “Audit the Fed” bills, saying in a 2012 press conference that Congress should not monitor the Federal Reserve “in terms of monetary policy.”[762]

* As a candidate for the Republican presidential nomination in 2011, former Speaker of the House Newt Gingrich heavily criticized the Federal Reserve. He partially blamed the Federal Reserve Board for the Great Recession and weak recovery. He also promised to fire its leadership, demand a full audit, and limit their mandate.[763] [764] [765]

* Gingrich advocated creating a gold commission—similar to the one convened under President Reagan—to consider reinstating a gold standard.[766]

* In a February 2018 commentary, Gingrich warned that the Fed’s attitude and policies will obstruct economic growth.[767]

* In 2008, U.S. Rep. Paul Ryan (R-WI) proposed legislation to set price stability as the Fed’s sole long-term goal, which would eliminate full employment from the Fed’s dual mandate.[768]

* In 2009, Ryan wrote that the Federal Reserve should base monetary policy on a set of “commodities” or should “explicitly embrace inflation” goals.[769]

* Democratic President Bill Clinton nominated Reagan appointee Alan Greenspan to a third term as Federal Reserve chairman in 1996.[770] In 2000, he nominated Greenspan again.[771]

* In 1993, the Clinton administration made a policy not to comment on or interfere with the Federal Reserve’s policies and actions.[772] [773]

* In 1994, Clinton signed the Riegle–Neal Interstate Banking and Branching Efficiency Act into law. This law made it easier for banks to open branches and acquire other banks across state lines. He praised the act for helping banks “better meet the needs of our people.”[774]

* Steve Forbes, the editor of Forbes magazine, ran for president as a Republican in 1996 and 2000, advocating for using the gold price to guide U.S. monetary policy.[775] [776] [777]

* Forbes critiques monetary and exchange rates policy in his column, and in 2014 released the book Money: How the Destruction of the Dollar Threatens the Global Economy—and What We Can Do About It.[778] [779]

* During his campaign for the 1980 presidential election, Republican Ronald Reagan called for a return to the gold standard.[780] He was quoted as believing that “no great nation in history that went off the gold standard remained great.”[781]

* As president, Reagan supported the creation of the U.S. Gold Commission, which in 1982 recommended against restoring the gold standard.[782]

* Reagan publicly supported the Federal Reserve’s unpopular policy decisions during the recession of 1981–82. These policies effectively ended The Great Inflation.[783] [784] [785] [786]

* In 1980, Congress voted to create the U.S. Gold Commission to study whether to reinstate a gold standard in the United States. Senator Jesse Helms (R-NC) and U.S. Rep. Ron Paul (R-TX) sponsored the measure.[787]

* The commission majority report rejected restoring a monetary link between the dollar and gold.[788] Paul co-authored the commission’s minority report, which argued for restoring a gold link. The report was released as a book, The Case for Gold.[789] [790]

* In 2011, Paul sponsored a bill to repeal the Federal Reserve Act and abolish the Federal Reserve Board and banks.[791]

* Paul highlighted his critique of the Federal Reserve during his runs for president and authored the book End the Fed.[792] [793]

* U.S. Rep. Jack Kemp (R-NY), also U.S. Housing Secretary and 1996 vice presidential candidate, advocated for using the price of gold to guide monetary policy.[794] [795]

* In 1984, Kemp introduced legislation to define the dollar relative to gold and require the Treasury to exchange gold for dollars.[796]

[1] Article: “Money.” Encyclopedia Britannica, 1998. <www.britannica.com>

“A commodity accepted by general consent as a medium of economic exchange. It is the medium in which prices and values are expressed; as currency, it circulates anonymously from person to person and country to country, thus facilitating trade, and it is the principal measure of wealth.”

[2] Textbook: Macroeconomics (6th edition). By N. Gregory Mankiw. Worth Publishers, 2006.

Pages 77–78:

Money has three purposes. It is a store of value, a unit of account, and a medium of exchange.

As a store of value, money is a way to transfer purchasing power from the present to the future. If I work today and earn $100, I can hold the money and spend it tomorrow, next week, or next month. Of course, money is an imperfect store of value: if prices are rising, the amount you can buy with any given quantity of money is falling. Even so, people hold money because they can trade the money for goods and services for some time in the future.

As a unit of account, money provides the terms in which prices are quoted and debts are recorded. Microeconomics teaches us that resources are allocated according to relative prices—the prices of good relative to other goods—yet stores post their prices in dollars and cents. A car dealer tells you that a car costs $20,000, not 400 shirts (even though it may amount to the same thing). Similarly, most debts require the debtor to deliver a specified number of dollars in the future, not a specified amount of some commodity. Money is the yardstick with which we measure economic transactions.

As a medium of exchange, money is what we use to buy goods and services. “This note is legal tender for all debts, public and private” is printed on the U.S. dollar. When we walk into stores, we are confident that the shopkeepers will accept our money in exchange for the items they are selling.

[3] Webpage: “All About Money.” European Commission. Accessed June 3, 2018 at <ec.europa.eu>

“Many thousands of years ago, our European ancestors lived as hunters and farmers. They did not have the banknotes and coins that we use today. Instead, they would exchange goods with each other: for example, a hunter could exchange animal skins with a farmer for grain, or a fisherman could exchange decorative seashells for a polished stone axe with a hunter. This exchange is known as barter.”

Pages 9–10:

Throughout by far the greater part of man’s development, barter necessarily constituted the sole means of exchanging goods and services. …

Commodities were chosen as preferred barter items for a number of reasons—some because they were conveniently and easily stored, some because they had high value densities and were easily portable, some because they were more durable (or less perishable).

[5] Webpage: “The Story of Money: 02—Common Products as Money.” Federal Reserve Bank of Atlanta. Accessed August 8, 2017 at <www.frbatlanta.org>

“Trading everyday items made barter easier. It reconciled the wants of buyer and seller, simplified payments, and introduced standard measures. Common goods used in trade are known as commodity money. Cows as a form of money … Tea as a form of money … Raw metals as a form of money.”

[6] Webpage: “The Story of Money: 03—Value in Use, Value in Exchange.” Federal Reserve Bank of Atlanta. Accessed August 8, 2017 at <www.frbatlanta.org>

In some forms, money has value in use: you can eat or wear it, chop wood with it, or use it to make something else. In other forms, money has value in exchange: it works because we agree that the money represents a certain value. The silver in this “tiger tongue” made it intrinsically valuable. This Luristan bronze arm ring is a 7,000-year-old form of money. Dried grain was useful as money and food. Arrowheads were popular in trade. Throwing knives were used in the Congo as tools and money. Cowrie shell necklaces were used for jewelry and exchange. Kissi pennies are still used in parts of West Africa.

[7] Textbook: Macroeconomics (6th edition). By N. Gregory Mankiw. Worth Publishers, 2006.

Page 78: “To better understand the functions of money, try to imagine an economy without it: a barter economy. In such a world, trade requires the double coincidence of wants—the unlikely happenstance of two people each having a good that the other wants at the right time and place to make an exchange. A barter economy permits only simple transactions.”

[8] Webpage: “Cowry Shells, a Trade Currency.” By Ingrid Van Damme. Museum of the National Bank of Belgium, January 11, 2007. <www.nbbmuseum.be>

Long before our era the cowry shell was known as an instrument of payment and a symbol of wealth and power. This monetary usage continued until the 20th century. …

The cowry which is indigenous in the warm waters of the Indian and Pacific Oceans travelled by land and by sea and gradually spread out its realm. It became the most commonly used means of payment of the trading nations of the Old World. The cowry was accepted in large parts of Asia, Africa, Oceania and in some scattered places in Europe. Chinese bronze objects, the oldest dating back to the 13th century B.C., inform us about this monetary usage. This tradition has also left its traces in the written Chinese language.

[9] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 46: “The Chinese at the end of the Stone Age began for instance to manufacture both bronze and copper ‘cowries’; and these dumpy imitations, which must have represented very high values at least when they were first introduced, are considered by some numismatists to be among the earliest examples of quasi-coinage, although this depends on how strictly one defines the term.”

Page 56:

We have already noted how metal cowries, of bronze or copper, were cast in China as symbols of objects already long accepted as money. A similar process took place with regard to spades, hoes and adzes (variants of the most common tools) and also of knives. The common characteristic of all these metallic moneys was not only that they were cast but that they were almost invariably composed of base metals.

[10] Article: “The Importance of the Lydian Stater as the World’s First Coin.” By Everett Millman. World History Encyclopedia, March 27, 2015. <www.worldhistory.org>

The Lydian Stater was the official coin of the Lydian Empire, introduced before the kingdom fell to the Persian Empire. The earliest staters are believed to date to around the second half of the 7th century BCE, during the reign of King Alyattes (r. 619–560 BCE). According to a consensus of numismatic historians, the Lydian stater was the first coin officially issued by a government in world history and was the model for virtually all subsequent coinage.

[11] Webpage: “The Origins of Coinage.” British Museum. Accessed August 8, 2017 at <www.britishmuseum.org>

The earliest coins are found mainly in the parts of modern Turkey that formed the ancient kingdom of Lydia, but are made from a naturally occurring mixture of gold and silver called electrum. …

Although irregular in size and shape, these early electrum coins were minted according to a strict weight-standard. The denominations ranged from one stater (weighing about 14.1 grams) down through half-staters, thirds, sixths, twelfths, 1/24ths and 1/48ths to 1/96th stater (about 0.15gm).

[12] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 66:

From its birthplace in Lydia and Ionia the knowledge and use of coins spread rapidly east into the Persian empire and west through the rest of the Ionian and Aegean islands to mainland Greece, and then to its western colonies, especially Sicily. It also spread northward to Macedonia, Thrace and the Black Sea, but it was only partially, reluctantly and belatedly accepted in Egypt. Mainland Italy also was at first rather slow in accepting the Greek financial innovations, in contrast to the speed with which they were adopted by Sicily. Apart from these two limited exceptions of mainland Italy and Lower Egypt, the use of coinage spread rapidly around the countries bordering the central and eastern Mediterranean and over the widespread and growing Persian empire through Mesopotamia into India. …

The rapid eastward spread of coins from Lydia was not so much because of Lydian traders going east but rather a case of the spoils of war through the Persians moving quickly west.

[13] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Pages 106–107:

Shortly following Diocletian’s abdication in 305 Constantine took over an initially disputed control of much of the western empire in 306, and eventually established his authority throughout the empire…. Early in Constantine’s reign he issued a coin that is in some ways the most famous single coin in history—the gold solidus, which was to be produced, at a rate of 72 to the pound weight, for some seven hundred years. No other coin has remained pure and unchanged in weight for anything like so long a period, for when Rome fell it continued to be issued from the Byzantine capital….

[14] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 125: “The first true English penny … thus dates from 765. However, it was Offa’s conquest of Kent … that enabled Offa so to increase the production of these magnificent coins that their fame soon spread all over northern Europe….”

[15] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Pages 143–144:

Henry [II]’s reform restored the prestige of English money, the quality of which was jealously safeguarded from any further major decline until the mid-sixteenth century. This was so unlike the situation on the Continent that the term “the pound sterling” emerged into common usage with its well-known praiseworthy connotations. …

… Hence “sterling” would be the natural description for English money, which from the tenth century onward tended generally to be of higher quality than that of its continental neighbours, and therefore referred specifically to the penny coins weighing 22 1/2 grains troy of silver at least pure to 925 parts in a thousand, 240 of which made the Tower pound weight or the pound sterling in value. It is also significant to note that the term “pound sterling” was in common use throughout Europe in the Middle Ages, with all its connotations of solidity, stability and quality—long before the issue of a pound coin—when silver was almost the only metal used in British coinage and the penny was almost the only, and certainly the main, coin. … So long as full-bodied gold and silver coins were issued in Britain, that is right up to the First World War, so long did the term “the pound sterling” maintain its prestigious significance, that is for a period spanning well over 800 years, from 1078 to 1914.

[16] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 174: “Sterling was therefore much more widely used than simply within the domestic economy, being a preferred silver currency over much of northern Europe, though playing very much a secondary role in international trade when compared with the gold florins of Florence or Ghent, or the ducats of Venice.”

[17] Article: “The Banknote, a Chinese Invention?” By Coralie Boeykens. Museum of the National Bank of Belgium, November 30, 2021. <www.nbbmuseum.be>

Since the 7th century AD, paper has been used as currency in China. It was probably money lenders who first started the system by giving a certain value to the paper being exchanged in transactions taking place in their stalls. At the same time, merchants were developing the habit of depositing their metallic coins with their corporation in exchange for bearer notes called Hequan. …

Under the Tang Dynasty (618—907), there was a growing need for metallic currency. The notion of credit was already familiar with the Chinese, who were ready to accept a piece of paper giving a measure of value. The origin of this transition to paper money seems to be linked with money lenders. From their stalls, they effectively used the medium of paper for their transactions, as these documents were worth a certain sum of money.

We also know that, around the 6th century, the copper that was needed to make Chinese coins (copper cash coins) became increasingly scarce. So, coins given as an offering or burial money for the dead to pay their passage to the other world were replaced by a note. But can we consider this as an exchange currency in this specific case? Of course not, but it is remarkable that also here paper replaces metal very smoothly.

At the end of the Tang period, traders got used to depositing their values with their corporations. In exchange, they received bearer notes or the so-called Hequan. These Hequan were a real success, and the idea was taken up by the authorities, who called on merchants to deposit their metallic money in the Government Treasury in exchange for official “compensation notes”, called Fey-thsian or flying money.

Under the Song Dynasty (960-1276), booming business in the region of Tchetchuan likewise resulted in a shortage of copper money. Some merchants issued private currency called “Zhu Quan” in mulberry paper. These notes were covered by a monetary reserve which initially consisted of coins and salt, later of gold and silver. This was the first legal tender currency. In 1024, the government itself gave the issuing monopoly and under the Yuan Dynasty (1279-1367), paper money became the only legal tender. …

The most interesting description of this paper money comes from Marco Polo (1254-1324), the famous Venetian traveller who set off to discover the Far East. The banknote that he describes dates from the Yuan period, during which the Mongol chief Kublai Khan reigned (1214–1294). Thanks to his report, we now know about the fascinating world of paper money production. “It is in the city of Khanbalik that the Great Khan possesses his Mint. … This paper currency is circulated in every part of the Great Khan’s dominions, nor dares any person, at the peril of his life, refuse to accept it in payment.”

Marco Polo was amused at the thought that, whereas in Europe alchemists had struggled in vain for centuries to turn base metals into gold, in China, the emperors had very simply turned paper into money. Once back home, Marco Polo amply reported about his experiences and adventures in the Chinese Empire but when he talked about paper money, nobody believed him. …

… In fact, if we keep to the concept of paper money as notes issued with a monetary reserve as a warranty, the first documents date from the 10th century. That means the Chinese had a headstart of no less than seven centuries on the Western world!

[18] Article: “Dollar.” Encyclopedia Britannica, 1998. <www.britannica.com>

The word itself is a modified form of the Germanic word thaler, a shortened form of Joachimst(h)aler, the name of a silver coin first struck in 1519 under the direction of the count of Schlick, who had appropriated a rich silver mine discovered in St. Joachimsthal (Joachim’s dale), Bohemia. These coins were current in Germany from the 16th century onward, with the various spelling modifications such as daler, dalar, daalder, and tallero. Only in 1873 was the thaler replaced by the mark as the German monetary unit.

[19] Article: “Peso.” Encyclopedia Britannica, July 20, 1998. <www.britannica.com>

“Originally divided into eight reales, the peso subsequently became the basis of the silver coinage of the Spanish empire after the monetary reform of 1772–86. In the Americas it was called ‘piece of eight,’ or ‘Spanish milled dollar,’ and was, in fact, equivalent to the U.S. silver dollar.”

[20] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 461:

[T]he colonies continued … with a marked and growing preference for the Spanish peso minted in Mexico City and Lima and the Portuguese eight-real piece. Both these large silver coins were practically identical in weight and fineness, being based on imitation of the famous “thalers” which had been produced from the silver mines in Joachimsthal in Bohemia for centuries—hence the designations “pieces of eight” and “dollars.”

[21] Article: “A Short History of the British Pound.” By Chris Parker. World Economic Forum, June 27, 2016. <www.weforum.org>

1717

The United Kingdom defined sterling’s value in terms of gold rather than silver for the first time.

Sir Isaac Newton, as Master of the Mint, set the gold price of £4.25 per fine ounce that lasted two hundred years, except during the Napoleonic wars when gold cash payments were suspended.

[22] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 469: “That Act [the Coinage Act of 1792] officially adopted the dollar as the American unit of account (so confirming Confederate legislation). … Thirdly, the dollar was officially to be bimetallist, being defined as equivalent to 371.25 grains of silver or 24.75 grains of gold. The mint ratio was thus 15:1—a rate that in practice was found slightly to overvalue silver.”

[23] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 356:

In 1816 gold became at last legally recognized as the official standard of value for the pound, though it was not until the restoration of convertibility in 1821 that the domestic gold standard was in full operation. We have also traced how the Bank of England came to be the monopolistic issuer of bank notes with a fixed fiduciary issue of £14 million and also came to hold the main gold reserves of the centralizing banking system.

[24] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 357:

[T]he major trading countries had become so favourably impressed [with Britain’s management of the gold standard] that they too gave up their flirtations with silver and bimetallism and adopted full gold standards with internal circulation of full-bodied gold coinage and more or less freely allowed imports and exports of gold, as the rules of the international gold standard system demanded. Following the new German Empire’s decision in 1871 to base its mark on gold, Holland, Austro–Hungary, Russia and the Scandinavian countries soon did likewise, while in 1878 France abandoned its bimetallic experiments in favour of gold. Thus by the end of the 1870s, without being consciously planned, the international gold standard system had fallen fittingly into place (though internally the USA still flirted with bimetallism).

[25] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Page 496:

Around the same time [1878] two further aspects of the money question were being resolved, namely the demonetization of silver and the resumption of convertibility into specie, the specie concerned being gold. By the Coinage Act of 1873 … the USA was now virtually on the gold standard. The gold premium carried by notes was clearly falling during the early 1870s, so that the government felt it safe, by the [Specie Payment] Resumption Act of January 1875, to promise full redemption by 1 January 1879.

[26] Article: “Resumption Act of 1875.” Encyclopedia Britannica, 1998. <www.britannica.com>

On Jan. 14, 1875, Congress passed the Resumption Act, which called for the secretary of the Treasury to redeem legal-tender notes in specie beginning Jan. 1, 1879. … Specie resumption proceeded on schedule, however, and Treasury Secretary John Sherman accumulated enough gold to meet the expected demand. When the public realized that the paper money was “good as gold,” there was no rush to redeem, and greenbacks continued as the accepted currency.

[27] Book: A History of Money: From Ancient Times to the Present Day (3rd edition). By Glyn Davies. University of Wales Press, 2002.

Pages 498–499: