Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

* The facts below differentiate between healthcare spending, prices, and costs based upon the following definitions:

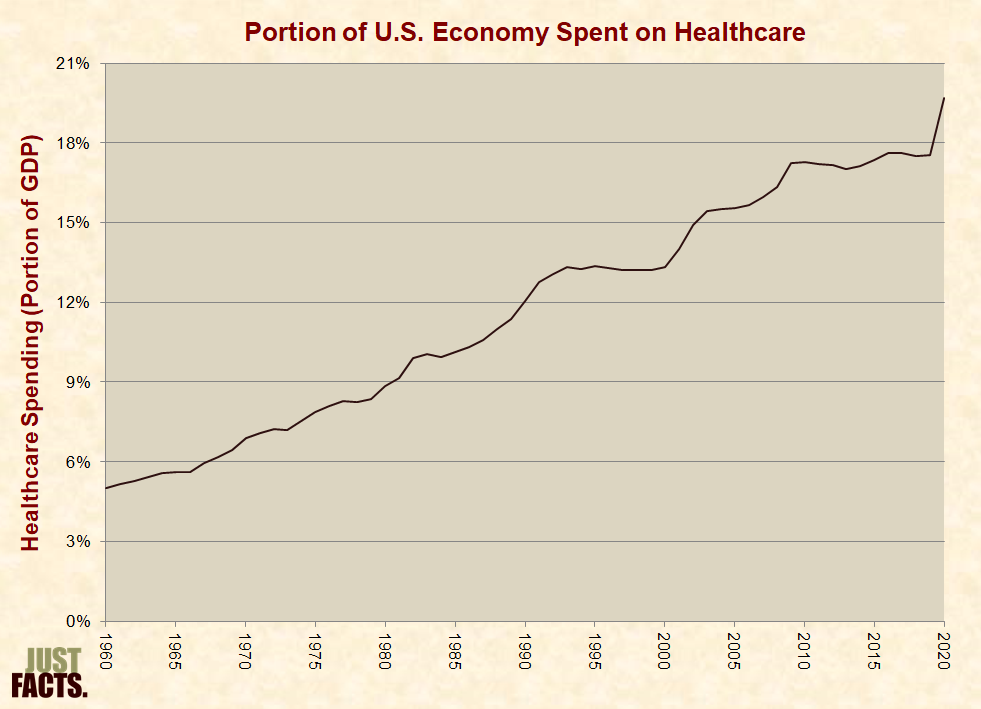

* From 1960 to 2020, healthcare spending in the United States increased:

* In 1942, the price for a maternity room at Christ Hospital in Jersey City, NJ was $7.00 per day.[3] Adjusting for inflation, this amounts to $97.29 in 2011 dollars.[4] In 2011, the price for a maternity room at the same hospital was $1,360 per day.[5]

* A 2022 survey of 15 hospitals in Ohio (where state law requires hospitals to publish their prices[6]) found that the daily price of a typical hospital room ranged from $1,905 to $3,675, with an average of $2,391 and a median of $2,166.[7]

* In 1980, the average price for a typical hospital room in the U.S. was $127 per day.[8] Adjusting for inflation, this amounts to $459 in 2022 dollars.[9]

* In 1988, Mutual of Omaha insurance company paid an average of $270 per day for all types of hospital rooms (such as medical/surgical, intensive care, maternity, etc.).[10] [11] Adjusting for inflation, this amounts to $656 in 2022 dollars.[12]

* In 2002, Mutual of Omaha paid an average of $748 per day for all types of hospital rooms.[13] Adjusting for inflation, this amounts to $1,187 in 2022 dollars.[14]

* Third-party payments are healthcare expenses that are not directly paid by consumers but by other entities such as governments and insurance companies. Such entities are called “third-parties” because they do not deliver or receive healthcare. In other words, they are not patients or caregivers.[15]

* From 1960 to 2020, the portion of U.S. healthcare expenses paid:

* A scientific, nationally representative survey commissioned in 2019 by Just Facts found that 38% of voters believe the government now pays a smaller portion of all U.S. healthcare costs than it did in 1960.[17] [18] [19]

* Per the Encyclopedia of Health Care Management:

* A Rand Corporation study tracked the healthcare spending of 2,756 families over periods of either three or five years during 1974–1982. The families were given insurance plans that covered all healthcare expenses above $1,000 per year or a reduced amount for lower-income families so that healthcare expenses could never exceed certain portions of their income.[23] (Accounting for inflation, $1,000 during the timeframe of this study equates to about $4,507 in 2022 dollars.[24])

* The families in the study were then randomly assigned to plans that covered their healthcare expenses below $1,000 per year, covering either 5%, 50%, 75%, or 100% of this spending. For example, families with 75% coverage paid 25% of their healthcare spending up to $1,000 per year (a maximum of $250 out-of-pocket), and insurance paid for everything else. The results were as follows:

* A 2001 study published in the American Journal of Public Health analyzed insurance coverage levels and health outcomes of “an older, chronically ill population” with conditions such as “diabetes, hypertension, coronary artery disease, congestive heart failure, or depression.” The study grouped “individuals into 3 cost-sharing categories: no copay (insurance pays all), low copay (insurance pays more than half but not all), and high copay (insurance pays half or less).” Per the study:

* U.S. law has incentivized and subsidized third-party healthcare payments by:

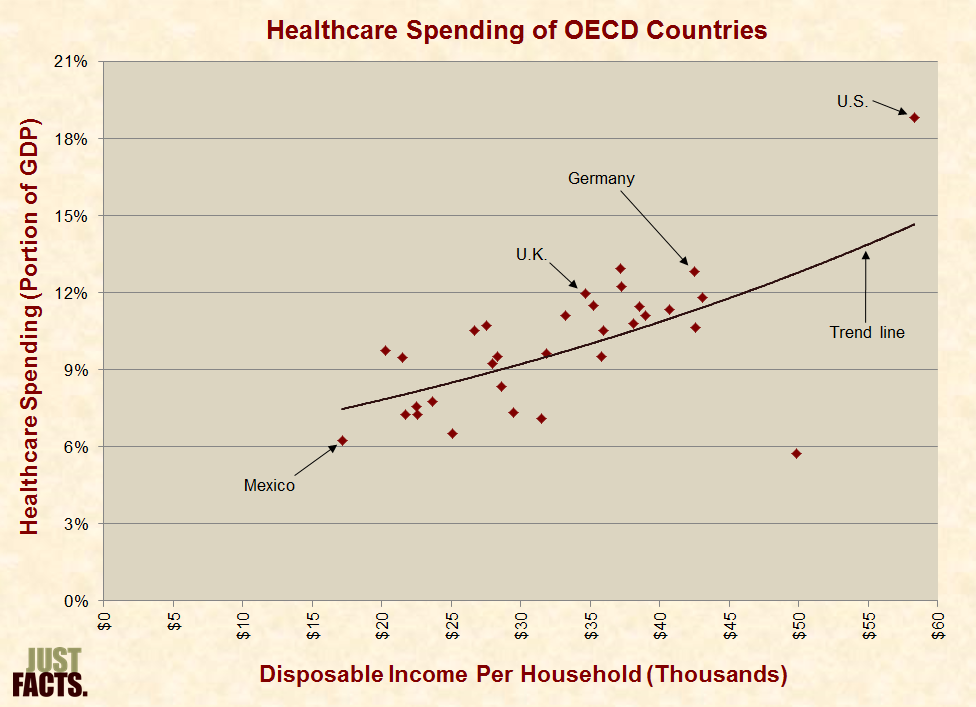

* Two common measures of nations’ wealth are:

* The Organization for Economic Cooperation and Development (OECD) is a group of 38 mostly developed nations such as Australia, Canada, Germany, Japan, and the United States.[52] [53]

* Among OECD nations, higher disposable income is generally associated with a greater portion of GDP spent on healthcare:

* Per the Handbook of Health Economics, “results obtained with international comparisons should be treated with considerable caution,” but a “common and extremely robust result of international comparisons is that the effect of per capita GDP (income) on [healthcare] expenditures is clearly positive and significant….”[58] [59]

* Personal healthcare expenditures consist of monies directly spent to “treat individuals with specific medical conditions.”[60]

* In the U.S. during 2014, the average annual healthcare spending per person for 65–84-year-olds was 3.5 times higher than that of 19–44 year-olds:

|

Age Group (Years) |

Annual Personal Healthcare Spending Per Person |

|

0–18 |

$3,749 |

|

19–44 |

$4,856 |

|

45–64 |

$10,212 |

|

65–84 |

$16,977 |

|

85+ |

$32,903 |

|

All ages |

$8,054 |

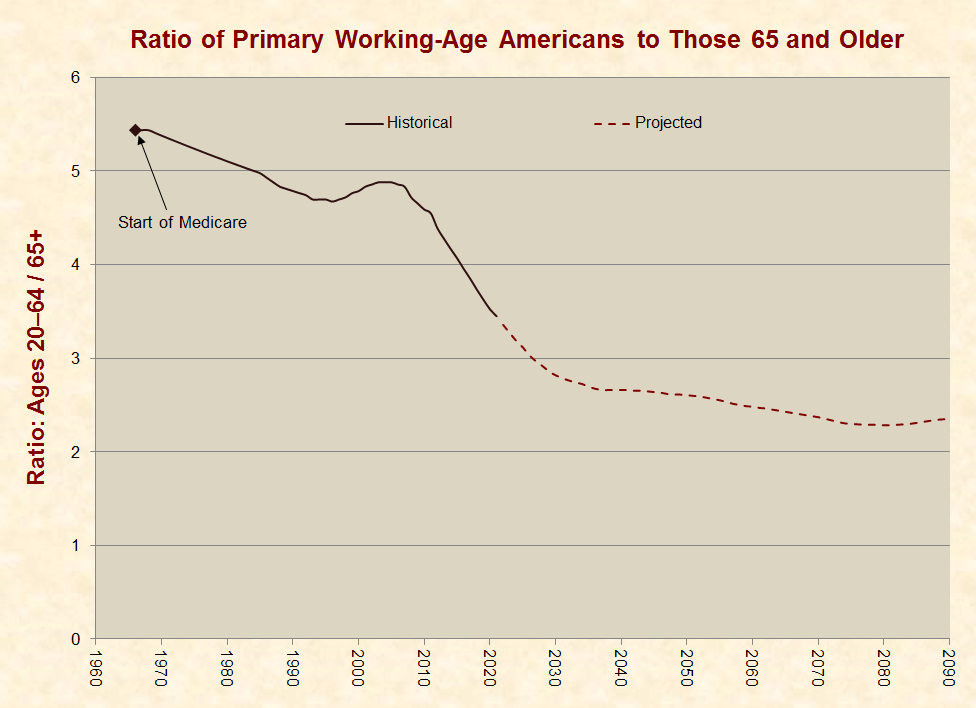

* When the first wave of baby boomers reached the age of 65 in 2011, there were 4.5 Americans aged 20–64 for every American aged 65 or older. As the baby-boom generation ages and projected life expectancy increases, the Social Security Administration projects that this ratio will drop to 2.8 to 1 by 2030 and to 2.7 to 1 by 2040.[62] [63] [64]

* Cancer, cardiovascular disease, and diabetes are responsible for the majority of deaths and healthcare costs in the United States.[65] [66]

* In 2008, the journal of the American Heart Association published a study entitled “The Impact of Prevention on Reducing the Burden of Cardiovascular Disease.” The authors found that:

* Per the Congressional Budget Office:

* In 2008, the journal PLoS Medicine published a study on the healthcare costs of obesity and smoking in the Netherlands. The authors found that:

* The study’s conclusion states:

* In 1998, the British Medical Journal published a study examining the cost effectiveness of preventing fatal diseases in the Netherlands. The study found that:

* The study’s conclusion states:

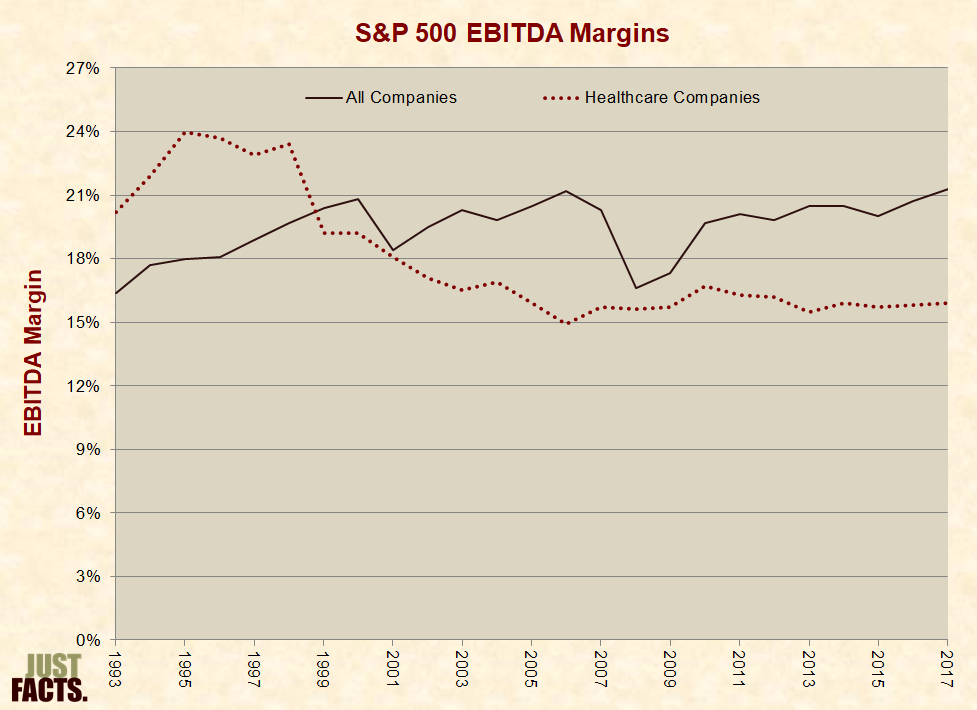

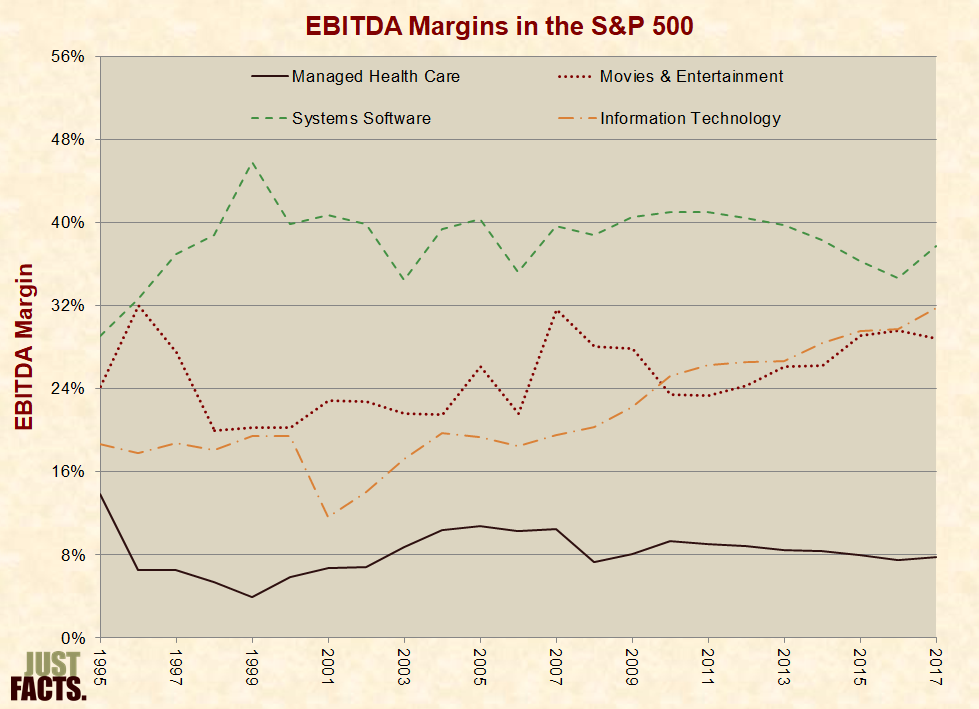

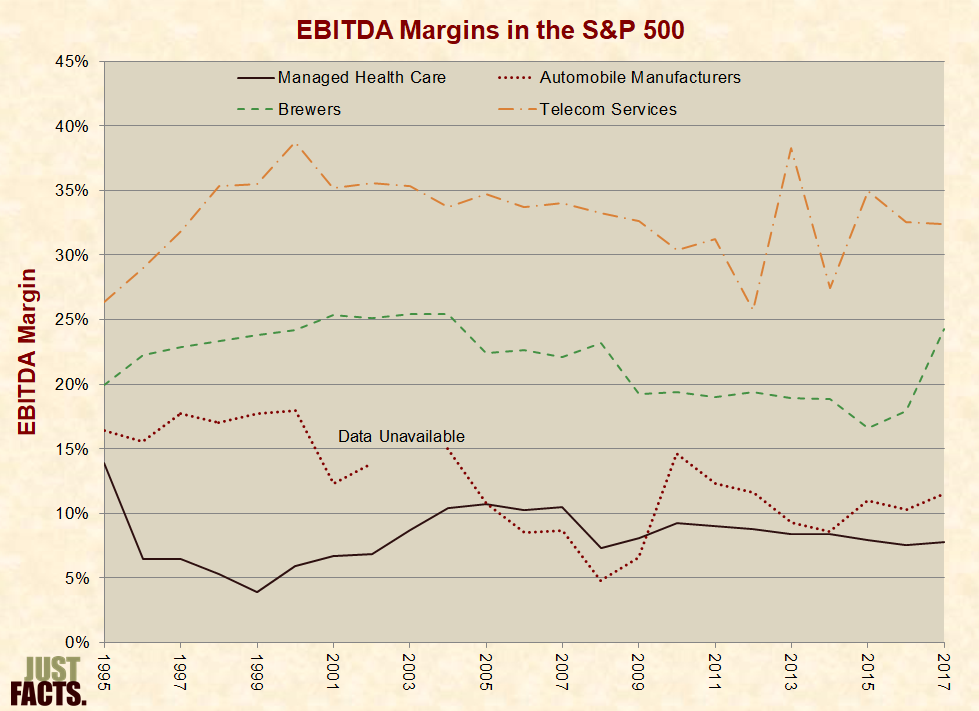

* EBITDA or “earnings before interest, taxes, depreciation and amortization,” is “an important standard measure” of company and industry profitability.[73] [74]

* From 1993 to 2017, the average EBITDA margin for all companies in the S&P 500 was 20%. For healthcare companies in the S&P 500, it was 18%:

* As of August 2015, the net profit margins (after taxes[77]) for various industries within the healthcare sector were as follows:

|

Industry |

Net Profit Margin |

|

Medical Practitioners |

–11.5% |

|

Generic Drugs |

–4.4% |

|

Long-Term Care Facilities |

–2% |

|

Home Healthcare |

–0.5% |

|

Drug-Related Products |

1.7% |

|

Healthcare Plans |

3.2% |

|

Hospitals |

4.1% |

|

Specialized Health Services |

6.2% |

|

Medical Laboratories & Research |

6.4% |

|

Drug Delivery |

8.2% |

|

Medical Appliances & Equipment |

10.2% |

|

Medical Instruments & Supplies |

10.5% |

|

Diagnostic Substances |

11.4% |

|

Non-Major Drug Manufacturers |

17.6% |

|

Biotechnology |

19.5% |

|

Major Drug Manufacturers |

21.6% |

* In May of 2021, the average hourly wage (not including benefits) for nonfarm workers in the U.S. was $28.01, and the average hourly wage for various healthcare occupations was as follows:

|

Occupation Title |

Average Hourly Wage |

|

Pharmacy Technicians |

$18.25 |

|

Paramedics |

$23.80 |

|

Dietitians and Nutritionists |

$31.55 |

|

Chiropractors |

$39.06 |

|

Registered Nurses |

$39.78 |

|

Physical Therapists |

$44.67 |

|

Physician Assistants |

$57.43 |

|

Pharmacists |

$60.43 |

|

Dentists |

$85.47 |

|

Pediatricians |

$95.40 |

|

Family Medicine Physicians |

$113.43 |

|

Psychiatrists |

$120.08 |

|

Surgeons |

$141.60 |

|

Obstetricians and Gynecologists |

$142.41 |

|

Anesthesiologists |

$159.22 |

* In 2021, all of the top-10 highest-paying occupations were in the medical or dental fields.[81]

* Per the Congressional Budget Office:

* Per the U.S. Treasury Department, an “improper payment” is:

* Per the U.S. Government Accountability Office:

* In 2021, the U.S. Department of Health and Human Services and Department of Justice spent $2.2 billion trying to control healthcare fraud and abuse.[88]

* According to federal government estimates, during 2021:

* In New Jersey during 2007, the agency that administers Medicaid and the Children’s Health Insurance Program provided such benefits to at least 873 families with gross incomes above $85,000, including three families with incomes above $700,000.[94] [95]

* In 2008, the Government Accountability Office reported that their investigators were able to “easily set up two fictitious” medical supply companies that were “approved for Medicare billing privileges despite having no clients and no inventory.”[96]

* A 2009 Medicare fraud investigation by CBS News found that:

* A 2010 Medicare fraud investigation by the Wall Street Journal found that:

* Per the FBI’s “2009 Financial Crimes Report”:

* In 2011, the U.S. Government Accountability Office reported the results of an investigation to “determine the extent to which Medicare beneficiaries obtained frequently abused drugs from multiple prescribers.” This is called “doctor shopping,” and it is one of the main ways people “obtain highly addictive” prescription drugs “for illegitimate use.” The investigation found that:

* The Inspector General of the U.S. Department of Health and Human Services investigated opioid use among Medicare beneficiaries during 2021 to determine the extent to which beneficiaries overdosed on or received high amounts of opioids.[101] This study found that:

* In the U.S. during 2020:

* Federal law requires all nonprofit hospitals to treat Medicare and Medicaid patients.[112] During 2020:

* As of 2018, state Medicaid plans limited payments for hospital stays to no more than 45 days in Florida, 24 days in Oklahoma, and 30 days in Texas. Many states require prior approval for hospital stays or certain procedures.[114]

* Federal law requires most hospitals with emergency departments to provide an “examination” and “stabilizing treatment” for anyone who comes to such a facility and requests care for an emergency medical condition or childbirth, regardless of their ability to pay and immigration status. This is mandated under a federal law called the Emergency Medical Treatment and Active Labor Act (EMTALA).[115] [116] [117]

* In 2000, emergency room physicians incurred an average of $138,300 in bad debt by providing treatment mandated under EMTALA. Bad debt does not include charity care or care for which charges were reduced through negotiations. It only includes care for which payment was owed and not received.[118]

* In 2001, emergency room physicians spent about half of their patient-care time providing treatment mandated under EMTALA.[119]

* Since 2014, the Affordable Care Act (a.k.a. Obamacare) has required private health insurers to:

* The added costs of insuring people after they become ill raises the premiums of other customers.[124] [125] [126] [127] Per a 2016 report by Blue Cross Blue Shield (BCBS):

* “Uncompensated care” is defined as the total cost to healthcare providers of both charity care and bad debt.[129]

* In 2021, the Consumer Financial Protection Bureau reported that 58% of all third-party debt collection efforts were associated with medical bills.[130] [131]

* In 2020, hospitals provided $42.7 billion of uncompensated care,[132] amounting to 3.5% of hospitals’ total costs.[133]

* “Defensive medicine” is defined by the American Academy of Orthopaedic Surgeons as “the practice of ordering excessive or unnecessary tests, procedures, visits, or consultations solely for reducing liability risk to the physician, and/or the practice of avoiding high-risk patients or procedures.”[134]

* In 2010, the costs to the U.S. healthcare system of malpractice awards, lawyers’ fees, and lawsuit-related administrative costs were about $30 billion or 1.1% of total healthcare spending.[135] [136] (This does not include the costs of defensive medicine.)

* States and localities have varying legal systems and demographics that drive disparities in medical malpractice costs.[137] As examples:

* A nationwide survey of 462 physicians conducted in 2009/2010 by Gallup and Jackson Healthcare found that 73% of doctors engaged in some form of defensive medicine over the past 12 months. On average, the physicians who practiced defensive medicine estimated that 21% of their practice was defensive in nature.[146]

* As of November 2022, Just Facts has been unable to find a credible estimate for the system-wide costs of defensive medicine in the U.S.[147] [148]

* A widely cited 2010 paper in the journal Health Affairs estimates that the costs of defensive medicine in the U.S. during 2008 were $38.8 billion for hospitals and $6.8 billion for physician and clinical services.[149]

* The authors of this study arrived at the $38.8 billion estimate for hospitals by:

* The authors of this same study:

* Examples of administrative and regulatory dynamics that impact healthcare costs include:

* A 2001 study conducted by PricewaterhouseCoopers for the American Hospital Association chronicled more than 40 layers of paperwork associated with caring for a typical Medicare patient who arrives at an emergency room with a broken hip and receives treatment until recuperation.[183] Some of the findings are:

* In 2022, federal, state, and local governments in the U.S. spent $2,239 billion on health and healthcare programs.[191] This amounts to:

* Relative to other types of government spending in 2022, healthcare spending was:

* From 1959 to 2022, spending on health and healthcare programs rose from:

* “Mandatory” federal programs are those that are permanently funded by law. Hence, they can spend money without Congress and the president passing new laws. In contrast, Congress and the president typically fund “discretionary” programs for one year at a time.[198] [199] The four major federal mandatory healthcare programs are Medicare, Medicaid, the Children’s Health Insurance Program, and the Affordable Care Act (i.e., Obamacare) exchange subsidies.[200] [201]

* The share of federal revenues spent on mandatory healthcare programs increased from 5% in 1970 to 14% in 1990 and 36% in 2010. In 2014, the Congressional Budget Office projected that under current federal policies, this share would rise to 41% in 2030, 55% in 2050, and 75% in 2080. Combining these projections with historical data and actual outcomes since then yields the following results:

* Data from the chart above:

|

Year |

Historical |

Projection |

|

1970 |

5% |

|

|

1980 |

9% |

|

|

1990 |

14% |

|

|

2000 |

16% |

|

|

2010 |

36% |

|

|

2020 |

41% |

|

|

2021 |

35% |

|

|

2030 |

41% |

|

|

2040 |

49% |

|

|

2050 |

55% |

|

|

2060 |

61% |

|

|

2070 |

68% |

|

|

2080 |

75% |

|

|

2089 |

81% |

* The Medicare program was founded in 1965 to provide health insurance for people aged 65 and older. It was later expanded to cover younger people who are permanently disabled.[203]

* In 2021, Medicare provided health insurance for almost all Americans aged 65 and over (roughly 56 million people) and about 8 million permanently disabled individuals under the age of 65.[204] [205] [206] In total, Medicare enrollees are about 19% of the U.S. population.[207]

* Medicare provides coverage for:

* In 2021, Medicare beneficiaries received an average of $13,536 per person in healthcare benefits and paid an average of $1,940 per person in premiums.[212]

* To qualify for premium-free Medicare hospital insurance, individuals or their spouses must work while paying Medicare’s payroll tax for at least ten years.[213]

* In 2019 (latest available data), Medicare covered 66% of healthcare expenses for traditional Medicare beneficiaries not living in institutions such as nursing homes. The remainder of beneficiaries’ healthcare expenses were paid by:

* In 2021, Medicare spent about $840 billion.[216] This amounts to 12% of all federal expenditures and 19% of all federal revenues.[217]

* Medicare expenditures in 2020 were funded by:

|

Portion[218] |

Category |

Source |

|

46% |

General revenues[219] |

Federal income, corporate, excise, and other taxes.[220] In total, these taxes are progressive so that higher-income households pay higher effective tax rates.[221] [222] [223] [224] [225] [226] |

|

34% |

Payroll taxes |

A 2.9% payroll tax on all workers’ wages and another 0.9% payroll tax on wages above $200,000 for singles and $250,000 for couples.[227] [228] [229] |

|

15% |

Insurance premiums |

Premiums paid by Medicare beneficiaries who receive Part B or Part D benefits. These premiums are indexed so that wealthier beneficiaries pay greater amounts.[230] [231] [232] |

|

3% |

Taxes on Social Security benefits |

Taxes paid by Social Security beneficiaries whose incomes exceed certain thresholds.[233] |

|

1% |

Transfers |

State governments.[234] |

|

1% |

Interest[235] |

Interest paid on the Medicare Trust Fund from the general fund of the U.S. Treasury.[236] [237] |

|

1% |

Miscellaneous |

Fees and gifts.[238] |

* In 2017, 81% of primary care physicians accepted new Medicare patients, as compared to 76% who accepted new Medicaid patients and 97% who accepted new privately insured patients.[239]

* All nonprofit hospitals are required by law to treat Medicare patients.[240]

* In 2019, Medicare payment rates for inpatient hospital services were 60% of private health insurance payment rates.[241]

* In 2020, Medicare paid hospitals an average of 16% below their costs of caring for Medicare patients.[242]

* The Affordable Care Act (a.k.a. Obamacare) progressively cuts Medicare payment rates “for hospital, skilled nursing facility, home health, hospice, ambulatory surgical center, diagnostic laboratory, and many other services” over upcoming decades to “less than half of their level under the prior law.” The U.S. Centers for Medicare and Medicaid Services projects that by 2097, Medicare payment rates for inpatient hospital services will be about 40% of private health insurance payment rates. Medicare’s Trustees have stated that these cuts will likely cause “withdrawal of providers from the Medicare market” and “severe problems with beneficiary access to care….”[243] [244]

* From 2013 to 2017, the number of rural hospital closures in the U.S. was more than twice the number of closures during the preceding five-year period. The U.S. Government Accountability Office found that the closures “were generally preceded and caused by financial distress” that was “exacerbated” by a decline in the number of patients receiving inpatient care and “across-the-board Medicare payment reductions.”[245]

* A scientific, nationally representative survey commissioned in 2019 by Just Facts found that 45% of voters believe the price controls in Obamacare won’t worsen Medicare patients’ access to care.[246] [247] [248]

* In 2003, Congress and Republican President George W. Bush passed a law adding a prescription drug benefit to the Medicare program.[249] [250] The bill passed with 88% of Republicans voting for it and 89% of Democrats voting against it.[251] The Congressional Budget Office estimated it would add $395 billion to the deficit over the following 10 years.[252]

* The Democratic Congressional Campaign Committee later described the Republican-passed Medicare prescription drug benefit as “costly.”[253] When this bill was being debated, 85% of House Democrats voted for a competing plan that the Congressional Budget Office estimated would add $969 billion to the deficit over the following 10 years, or 2.4 times more than the Republican plan.[254] [255]

* When Medicare began paying benefits in 1966,[256] there were 5.4 Americans in their primary working years (aged 20–64) for every American aged 65 or older. By 2021, this ratio declined to 3.4 or by 37%.[257] [258]

* As the baby-boom generation matures and projected life expectancy increases,[259] the Social Security Administration projects that the ratio of people in their primary working years to Medicare benefit recipients will decline to 2.8 by 2030, or by 48% from 1966 to 2030:

* From the time that Medicare was established in 1965, the general eligibility age for benefits has stayed at 65 years old.[261] [262] In 1965:

* In 2012, the journal Demography published research that found the Social Security Administration is using an antiquated method to project life expectancies, and as a result, the program “may be in a considerably more precarious position than officially thought.”[275]

* The 2022 Medicare Trustees Report projects the future finances of the Medicare program based upon high, low, and intermediate-cost assumptions.[276] Per the intermediate assumptions, the Medicare program faces a $52 trillion actuarial deficit over the next 75 years (in 2022 dollars). The resources needed to cover this deficit “would be in addition to the payroll taxes, benefit taxes, and premium payments.”[277]

* The above actuarial deficit approximates how much money must be immediately added to the Medicare program to cover the projected shortfall between the program’s dedicated funding sources and its costs for the next 75 years.[278] It is equivalent to 62 times the total spending for Medicare in 2021.[279]

* The Medicare Trustees have stated that measurements such as the actuarial deficit can:

* One way to account for the last of these concerns is to calculate how much money must be immediately added to the Medicare program in order to cover the projected shortfall for all current participants in the program (both taxpayers and beneficiaries).[282] This amounts to $52.7 trillion or an additional $201,572 from every U.S. resident aged 16 or older.[283] [284] [285] This measure approximates the method by which publicly traded companies are required by law to report the finances of their pension and retirement plans.[286] [287] [288] [289]

* The Medicare Trustees Report makes financial projections based primarily on current laws.[290] Per the Trustees, the “actual future costs for Medicare may exceed the projections shown in this report, possibly by substantial amounts.”[291] This is because:

* In 2022, U.S. Centers for Medicare and Medicaid Services published an alternative projection to estimate the potential costs of Medicare given the facts listed above.[294] Per this estimate, actual Medicare costs will exceed the costs shown in the Trustees Report by 3% per year by 2040, 13% per year by 2060, 24% per year by 2080, and 33% per year by 2096.[295]

* In 2022, the U.S. Treasury published a financial analysis of the alternative projection described above. These calculations show that Medicare’s 75-year open group unfunded obligation is 21% higher under the alternative projection than it is under current law.[296]

* When Democratic President Lyndon B. Johnson proposed a “hospital insurance” program for senior citizens in his 1964 State of the Union speech, he said that it would cost “no more than $1 a month” per worker.[297]

* Adjusted for inflation, $1 in 1964 equals $9.68 in 2023.[298] Individuals with the following wages now pay the following Medicare hospital insurance payroll taxes per month:

|

Yearly Wages |

Monthly Hospital Insurance Taxes |

|

$25,000 |

$60 |

|

$50,000 |

$121 |

|

$100,000 |

$242 |

|

$250,000 |

$642 |

|

$1,000,000 |

$3,017 |

* Hospital insurance payroll taxes fund about 34% of Medicare’s total spending. Other Medicare benefits—like physician services, lab tests, and prescription drugs—are paid through other taxes, premiums, and miscellaneous receipts.[300]

* The Medicare payroll tax amounts shown on paychecks generally do not account for the taxes that employers pay.[301] These taxes are mainly borne by employees in the form of reduced wages (for more details, see Just Facts’ research on tax distribution).[302] [303] [304] [305]

* Medicare hospital insurance payroll taxes were previously limited by a wage threshold that generally increased as the national average wage increased. Earnings above this threshold were not subject to the Medicare payroll tax. In 1993, this threshold was $135,000 per year.[306] That year, the 103rd Congress and Democratic President Bill Clinton passed a law that removed the threshold, thus making all earnings subject to Medicare payroll taxes.[307] The bill passed with 85% of Democrats voting for it and 100% of Republicans voting against it.[308]

* The same 1993 bill imposed a new Medicare tax on Social Security beneficiaries with incomes above certain limits. This tax is levied on the Social Security benefits of individuals if the total of one-half of their benefits and all other income is more than $34,000 per year ($44,000 if married and filing jointly).[309] [310] This threshold is not indexed for inflation or wage growth.[311]

* Starting in 2013, the Affordable Care Act (a.k.a. Obamacare) levied an additional 0.9% Medicare hospital insurance payroll tax on wages above $200,00 for singles and $250,000 for couples.[312] [313] This law passed with 89% of Democrats voting for it and 100% of Republicans voting against it.[314]

* The Medicaid program was founded in 1965 to pay for healthcare services for “certain low-income persons in the United States and its Territories.”[315] [316]

* In 2019, an average of 74 million people in the U.S. and its territories were enrolled in Medicaid for the entire year.[317] [318]

* During the Covid-19 pandemic—amid government-mandated business shutdowns that cost millions of jobs[319] [320]—average Medicaid enrollment increased from 75 million people in 2020 to 84 million in 2021.[321]

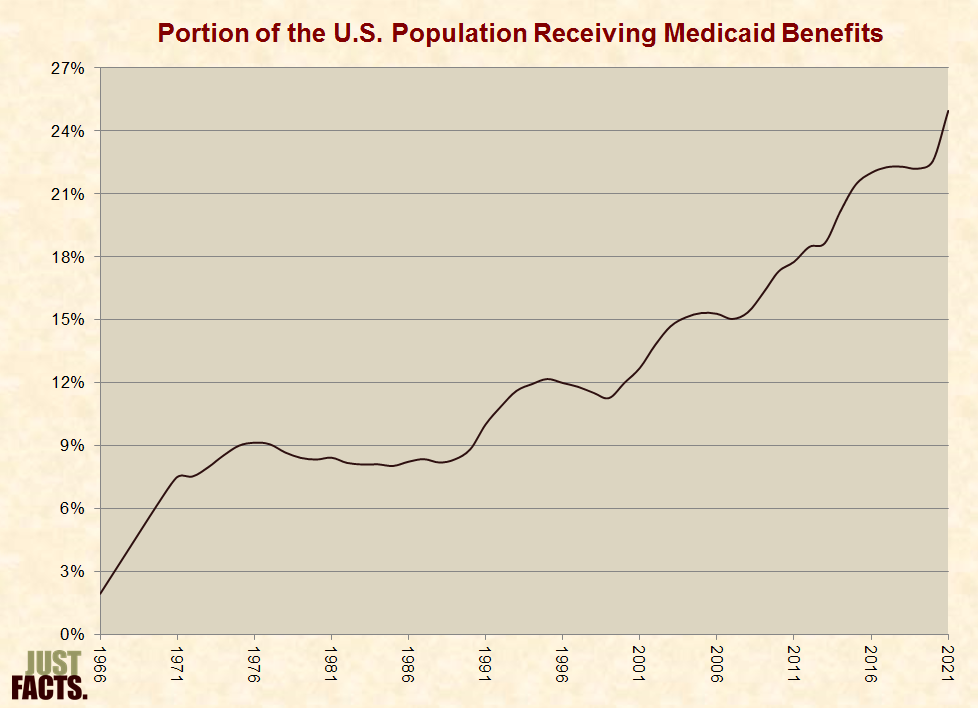

* The average portion of the U.S. population receiving Medicaid benefits for the entire year increased from 2% in 1966 to 25% in 2021:

* In 2019, Medicaid enrollment and spending was divided as follows:

|

Category |

Portion of Beneficiaries[323] |

Cost Per Enrollee[324] |

Portion of Medicaid Spending[325] |

|

Adults |

39% |

$5,808 |

28% |

|

Children |

38% |

$3,336 |

16% |

|

Disabled |

13% |

$21,368 |

34% |

|

Aged |

10% |

$17,885 |

23% |

* States are not required to participate in the Medicaid program, but all choose to do so. Within certain federal guidelines, states have latitude in setting eligibility criteria, deciding which healthcare services to cover, and regulating payments to doctors and other healthcare providers.[326] [327] [328]

* An example of a federal guideline is that all participating states must provide Medicaid coverage for pregnant women and children in families with income below a certain level.[329]

* Per the Congressional Research Service, “compared to both Medicare and employer-sponsored health care plans,” Medicaid “offers the broadest array of medical care and related services available in the United States today.”[330]

* Medicaid-covered services vary by state and include items such as ambulance transportation, chiropractic care, dental care, eyeglasses, physician services, hospital services, substance abuse rehabilitation, nonemergency medical transportation, personal care, prescription drugs, and private duty nursing.[331] [332]

* Medicaid expenditures are funded by federal and state general revenues.[333] Federal general revenues are comprised of income, corporate, excise, and other taxes.[334] [335] In total, these taxes are progressive so that higher-income households pay higher effective tax rates.[336] [337] [338]

* In 2021, Medicaid spent about $736 billion. This amounts to:

* The portion of Medicaid expenditures paid by the federal versus state governments varies by state. The federal government pays a greater share of Medicaid costs for states with lower average income levels.[340]

* There is no dollar limit on the federal funds states may receive for their Medicaid programs. Thus, as states provide more generous Medicaid benefits, they receive more funding from the federal government.[341] [342]

* The average share of Medicaid spending paid by the federal government (versus the states) has risen from 48% in 1966 to 69% in 2020, with a spike in 2009–2010 due to various “stimulus” bills and the Affordable Care Act and another spike beginning in 2020 due to the Covid-19 pandemic:

* In 2020, Medicaid paid for:

* Unauthorized immigrants are not eligible for standard Medicaid coverage but can receive Medicaid for emergency conditions. An emergency condition is defined as “one manifested by acute symptoms of such severity that the absence of immediate medical attention could reasonably be expected to result in”:

* In 2009, 74% of all babies delivered at Parkland Memorial Hospital in Dallas, Texas were born to women who were noncitizens.[352]

* Depending upon the state of residence, as of 2022, Medicaid will pay up to 100% of nursing home costs for individuals who have:

* Per the U.S. Centers for Medicare and Medicaid Services:

* From January 2006 through May 2009, a Medicaid enrollee in Buffalo, NY used an ambulance service 603 times at no cost to him, costing taxpayers at least $118,158.[355]

* All nonprofit hospitals are required by law to treat Medicaid patients.[356]

* In 2019, Medicaid payment rates for inpatient hospital services were 62% of private health insurance payment rates.[357]

* In 2020, Medicaid paid hospitals an average of 12% below their costs of caring for Medicaid patients.[358]

* Under current law, Medicaid payment rates for inpatient hospital services will progressively decline to about 40% of private health insurance payment rates by 2097.[359]

* In 2019, Medicaid payment rates for physician services were about 54% of private health insurance payment rates.[360]

* Per the 2013 Medicare Trustees Report, low Medicaid payment rates for healthcare services “have already led to access problems for Medicaid enrollees.”[361] [362]

* For a study published in the New England Journal of Medicine (2011), researchers posing as mothers called 273 specialty clinics in Cook County, Illinois (an urban area containing Chicago), to schedule appointments for “common health conditions requiring outpatient specialty care.” The researchers called each clinic twice, once while stating that their children were covered by Medicaid or the Children’s Health Insurance Program (CHIP), and the other while stating that their children were covered by private insurance. The study found that:

* A survey conducted by the Center for Studying Health System Change found that “about half of physicians reported accepting all new Medicaid patients in 2004–05, compared with more than 70 percent for Medicare and privately insured patients.”[364]

* In 2017, 76% of primary care physicians accepted new Medicaid patients, as compared to 81% who accepted new Medicare patients and 97% who accepted new privately insured patients.[365]

* Starting in 2014, the Affordable Care Act (a.k.a. Obamacare) required all states to provide Medicaid coverage for all individuals under the age of 65 with family incomes below 138% of federal poverty guidelines, without regard for any assets they have.[366] [367] In 2022, 138% of the federal poverty guideline was $38,295 for a family of four.[368]

* Obamacare stripped all federal Medicaid funds from any state that refused to comply with this expansion of Medicaid.[369]

* In the 2012 Supreme Court case of National Federation of Independent Business v. Sebelius:

* As of January 2022, 39 states and the District of Columbia have expanded Medicaid in accord with Obamacare. In these states, all adults under the age of 65 with family incomes below at least 138% of federal poverty guidelines are eligible for Medicaid. Some of these states also provide Medicaid to people with higher incomes.[371] [372]

* As of 2022, an additional 20 million people have enrolled in Medicaid as a result of the states’ expansions.[373]

* Among the 12 states that have not expanded Medicaid in accord with Obamacare:

* In 2013, Democratic President Barack Obama stated that expanding Medicaid will reduce healthcare costs by reducing emergency room visits:

* In 2008, the state of Oregon began providing Medicaid coverage to thousands of people selected through a lottery from a pool of uninsured, low-income adults. Random selection methods like this allow researchers to directly measure of the effects of public policies.[376] In 2014, the journal Science published a study of about 25,000 people who participated in this lottery and lived in the most-populated area of Oregon. The study followed the new Medicaid recipients for about 18 months after the lottery and found they had:

* In 2016, the New England Journal of Medicine published a follow-up study to the one above. This study analyzed an additional year of data to determine if Medicaid recipients would make less use of emergency rooms over time. It found that their increased levels of emergency room visits did not decline.[379]

* In 1997, the 105th Congress and Democratic President Bill Clinton passed a law that created a Children’s Health Insurance Program (CHIP) to help states provide insurance to low-income children.[380] [381] [382] The bill passed with 84% of Republicans and 78% of Democrats voting for it.[383]

* In 2020, 9.1 million children were enrolled in CHIP during some point in the year.[384]

* The legislation that created CHIP states that the “purpose” of the program is to provide “child health assistance to uninsured, low-income children … under 19 years of age … whose family income is at or below 200 percent” of the federal poverty line.[385] In 2022, 200% of the federal poverty line for a family of four was $55,500.[386]

* In 2022, states had income eligibility limits for CHIP ranging from 185% of the federal poverty line ($51,338 for a family of four) in Idaho to 400% of the federal poverty line ($111,000 for a family of four) in New York.[387] [388]

* In 2022, the median income eligibility limit for CHIP was 255% of the federal poverty line or $70,763 for a family of four.[389] [390]

* Not all sources of household income are considered when determining eligibility for CHIP. For example, the income of the following household members is not counted unless they are legal parents or guardians of the child:

* Since 2014, the Affordable Care Act (a.k.a. Obamacare) has mandated that families can have unlimited financial assets and still be eligible for CHIP.[395] [396]

* From 1998 to 2020, the average annual inflation-adjusted CHIP spending for every person in the U.S. under the age of 18 increased from $9 to $303:

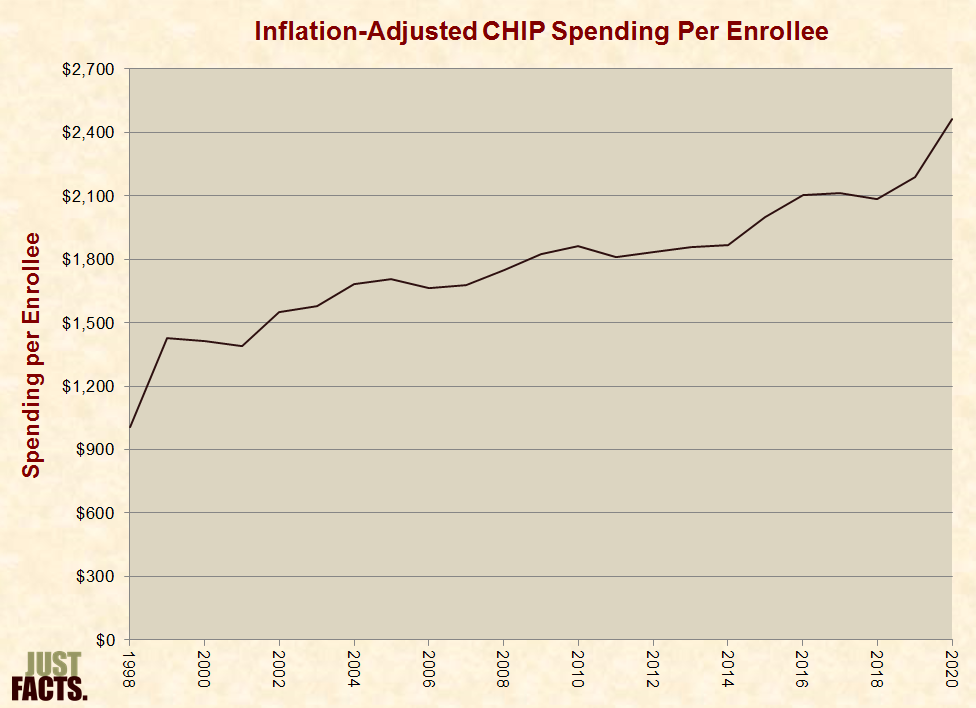

* From 1998 to 2020, the average annual inflation-adjusted CHIP spending per enrollee increased from $1,004 to $2,462:

* Like Medicaid, the federal and state governments share in the cost for CHIP, and states have latitude in setting eligibility criteria and deciding which healthcare services to cover.[399] The federal portion of CHIP funding varies by state, and before 2016, these rates ranged over time in different states from 65% to 81%.[400]

* During 2016–2019, the 2010 Affordable Care Act (a.k.a. Obamacare) raised the share of CHIP paid by the federal government by 23 percentage points per state, up to a maximum of 100%.[401] [402] Depending upon the state, the federal government paid from 88% to 100% of CHIP costs in 2019.[403]

* In 2020, the U.S. Congress and Republican President Donald Trump increased the federal government’s share of CHIP spending for the duration of the Covid-19 pandemic. Depending upon the state, the federal government paid from 69% to 89% of CHIP costs in 2022.[404] [405]

* In 2009, the U.S. Congress and Democratic President Barack Obama made legal immigrants immediately eligible for CHIP, overriding a previous requirement of a five-year waiting period.[406] This bill passed Congress with 99% of Democrats voting for it and 75% of Republicans voting against it.[407]

* In 2010, the 111th Congress and President Obama passed two laws that are collectively known as the “Affordable Care Act.” Formally, these bills were named the “Patient Protection and Affordable Care Act” and the “Health Care and Education Reconciliation Act.” Informally, these bills are known as “Obamacare.” The bills were passed separately for political and procedural reasons detailed in these footnotes.[408] [409]

* The bills passed Congress with 79–89% of Democrats voting for them and 99–100% of Republicans voting against them.[410] [411] Together, the bills contain about 1,000 pages.[412] [413]

* The Affordable Care Act:

* During the debate over the Affordable Care Act, Republicans proposed more than a hundred amendments to the legislation, most of which were rejected by the Democrats, who were in the majority at the time.[511] Examples of rejected amendments include:

* Between 2008 and 2013, Barack Obama promised at least 39 times that everyone who liked their health insurance could keep it under Obamacare. He also pledged at least 11 times that everyone who liked their doctor could keep their doctor under Obamacare.[518] For example, he stated:

* When Obamacare’s health insurance mandates went into effect, all health insurance plans that did not meet criteria specified in the Affordable Care Act were cancelled. By the end of 2013, millions of people (precise number unknown) had received health insurance cancellation notices due to Obamacare.[520] [521] [522]

* Some of the people who lost their health insurance were eligible to purchase federally-subsidized insurance through the Obamacare exchanges.[523]

* A 2015 study by Avalere Health of insurance plans offered by Obamacare exchanges in the five states with the greatest enrollment found that:

* Some of the people who lost their health insurance because of Obamacare were eligible to enroll in Medicaid.[525]

* Per the 2011 Medicare Trustees Report, low Medicaid payment rates for healthcare services cause “access problems for Medicaid enrollees.”[526] [527]

* For a study published in the New England Journal of Medicine (2011), researchers posing as mothers called 273 specialty clinics in Cook County, Illinois (an urban area containing Chicago), to schedule appointments for “common health conditions requiring outpatient specialty care.” The researchers called each clinic twice: once while stating that their children were covered by Medicaid or the Children’s Health Insurance Program (CHIP), and the other while stating that their children were covered by private insurance. The study found that:

* During the 2008 presidential election campaign, Barack Obama promised at least 18 times that his healthcare plan would save families an average of $2,500 per year on insurance premiums.[529] For example, he stated:

* In the years surrounding the passage of the 2010 Affordable Care Act, inflation-adjusted premium increases for employer-provided family health insurance varied as follows:

* In 2010, Congress’s Joint Committee on Taxation and the U.S. Centers for Medicare and Medicaid Services projected that the following changes in federal spending and revenues would occur during 2010–2019 as a result of the Affordable Care Act. Most of this would occur beginning in 2014, when many provisions of the act were scheduled to take effect.[535]

|

Projected Federal Spending Changes From the Affordable Care Act, 2010–2019 |

|

|

Provision |

Increase (billions) |

|

Medicare Cuts |

–$575 |

|

Insurance Subsidies for Individuals |

$507 |

|

Medicaid Expansion |

$410 |

|

Insurance Subsidies for Small Businesses |

$31 |

|

CHIP Increased Funding |

$29 |

|

Other Medicaid and CHIP Provisions |

$28 |

|

Miscellaneous |

$8 |

|

Total |

$438 |

|

Projected Federal Revenue Changes From the Affordable Care Act, 2010–2019 |

|

|

Provision |

Increase |

|

Taxes and Fees |

$421 |

|

Fines on Individuals & Employers |

$120 |

|

CLASS Act (discussed below) |

$38 |

|

Total |

$579 |

* The totals above net to a $141 billion improvement in the federal government’s finances over 2010–2019.[539] [540] This assumed:

* As of November 2022, the Joint Committee on Taxation, U.S. Centers for Medicare & Medicaid Services, and Congressional Budget Office have not studied the Affordable Care Act’s actual impact on federal revenues or spending thus far.[569] Per the:

NOTE: When interpreting the facts in this section, it is important to realize that association does not prove causation, and it is often difficult to determine causation in economics and other social sciences. This is because numerous variables might affect a certain outcome, and there is frequently no objective way to identify all of these factors and determine which is causing the others and to what degree.

* A 2016 study by the U.S. Department of Health & Human Services found that Obamacare “resulted in gains in health insurance coverage for 20.0 million nonelderly adults (ages 18 to 64).”[572]

* The following proponents of Obamacare linked insurance coverage and life expectancy to promote the law and criticize the U.S. healthcare system:

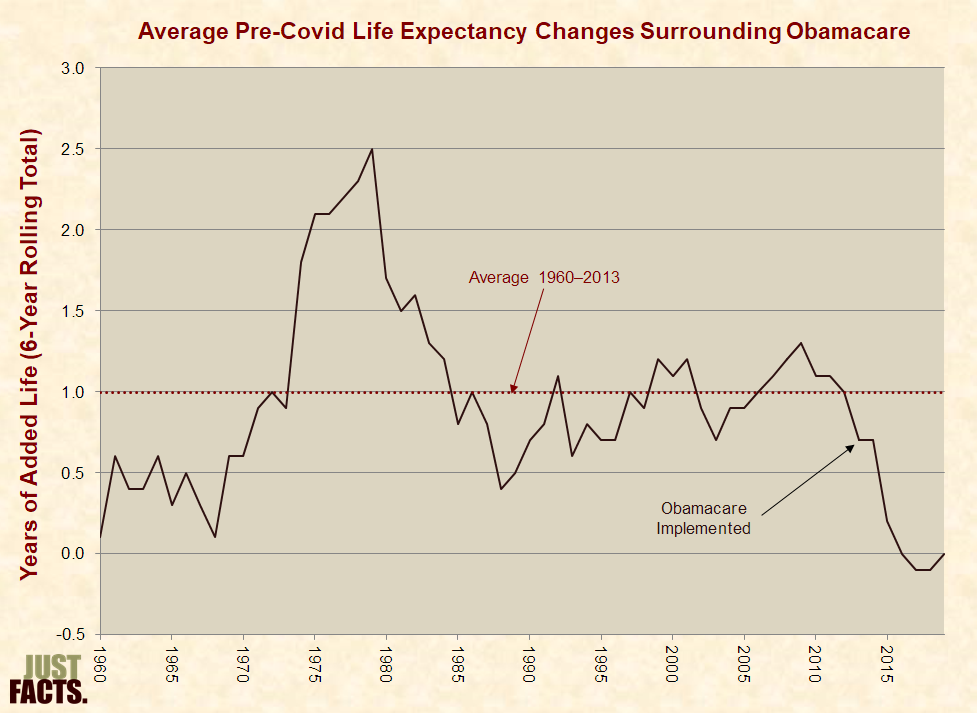

* In the U.S. from 1960 until most provisions of Obamacare were implemented in 2014, the average life expectancy rose by an average of 1.0 years every six years. In the ensuing six years of Obamacare implementation (2014–2019) prior to the Covid-19 pandemic,[577] average life expectancy had a net change of zero:

* Since the outset of 2014, the Affordable Care Act has required all new and renewed health insurance plans to cover treatment for substance abuse.[580] [581] [582] [583] [584] Obamacare supporters claimed that this mandate:

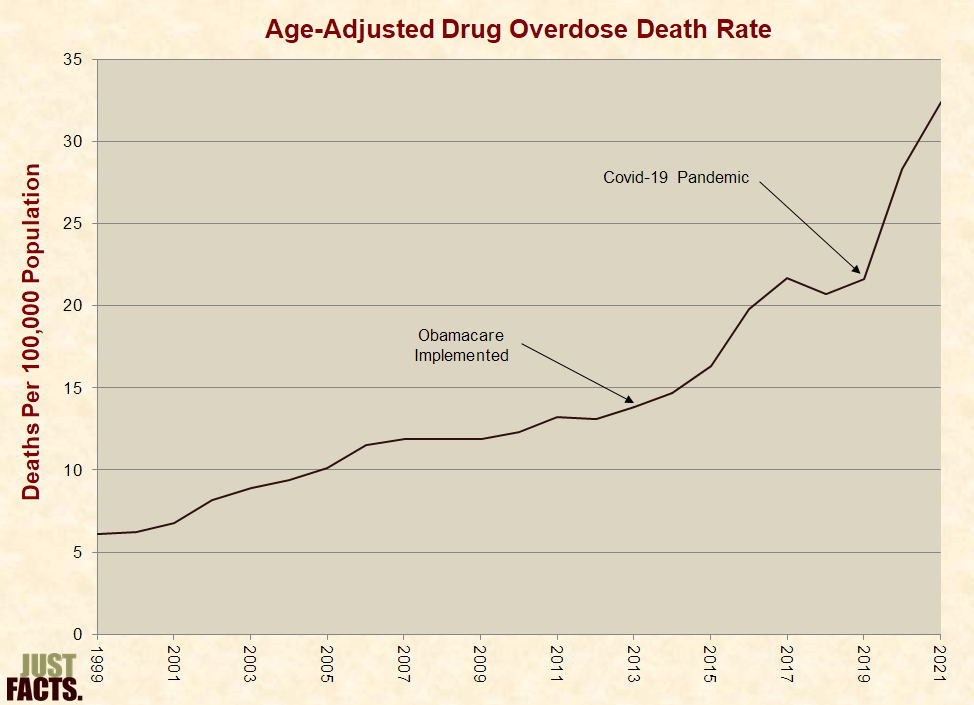

* From the start of Obamacare’s substance abuse coverage mandate in 2014 until just before the Covid-19 pandemic began six years later,[588] [589] the drug overdose death rate rose 4.1 times faster than in the six years prior to the mandate:

* In 2009, the American Journal of Public Health published a study that “analyzed the relationship between uninsurance and death.” Using survey data for 1988–1994 on 9,000 adults, the authors compared mortality rates at the end of the year 2000 between uninsured and privately insured participants. After controlling for 11 factors (such as age, gender, income, education, and body mass index), its authors concluded that “lack of health insurance is associated with as many as 44,789 deaths per year in the United States….”[594] The authors also:

* In 2009, Health Services Research published a study on the relationship between lack of insurance and risk of death. Using survey data for 1986–2000 on 643,000 people collected by the National Center for Health Statistics, the author compared mortality rates as of 2002 between the uninsured and privately insured participants. After controlling for 17 factors (such as age, gender, income, education, and body mass index), the author concluded that “there is little evidence to suggest extending insurance coverage to all adults would have a large effect on the number of deaths in the United States.”[617] [618] The study was similar to the above study from 2009 except that it:

* In a paper published by Annals of Family Medicine in 2019, the authors conducted a meta-analysis of studies that examined associations between healthcare and health outcomes.[626] They found that:

* Other than healthcare, factors that can affect mortality rates and life expectancy include:

* In September 2011:

* None of the above-cited articles or editorials mentioned the following facts, which are contained in the Census Bureau survey they cited:

* A study that cross-checked respondents from the above-referenced survey with data from the Centers for Medicare and Medicaid Services found that in 2005, about 18% of the “uninsured” in the survey actually had insurance through Medicaid.[646] [647]

* From 2007 through 2020, the annual portion of total private health insurance company revenues paid out in healthcare benefits for customers ranged from 86.9% to 89.2%.[648] [649] The remainder went to profits, taxes on premiums, and administrative expenses such as employee salaries and benefits, office space and furniture, computers, utilities, property taxes and insurance, sales commissions, advertising, legal fees, and audit fees.[650] [651] [652]

* From 2007 through 2010 (later data not available), the annual median net profit margin for the ten largest health insurance/managed care companies ranged from 2.1% to 4.4%. Throughout this period, the highest profit made by any of these companies in any year was 7.3%.

|

Net Profit Margins of the Ten Largest Health Insurance/Managed Care Companies |

|||

|

Year |

Median |

High |

Low |

|

2007 |

4.4% |

6.6% |

1.4% |

|

2008 |

2.1% |

4.5% |

–1.1% |

|

2009 |

3.1% |

7.3% |

–0.3% |

|

2010 |

4.2% |

6.3% |

–1.0% |

* In 2009, CNN uncritically reported the following statement from U.S. Senate Majority Leader Harry Reid:

* In 2008 (later data not available), the health insurance/managed care industry had a 2.2% net profit margin, which ranked 35th out of 53 top industries. The industry with the highest profit margin was network/communications equipment, which had a 20.4% profit margin.[657] [658]

* EBITDA or “earnings before interest, taxes, depreciation and amortization,” is “an important standard measure” of company and industry profitability.[659] [660] [661]

* In 2009, the average EBITDA margin for health insurance/managed care companies in the S&P 500 was 8%. For various other industries in the S&P 500, the margins were as follows:

|

Industry |

2009 EBITDA Margin |

|

Auto Parts & Equipment |

5% |

|

Automobile Manufacturers |

7% |

|

Advertising |

12% |

|

Retail Apparel |

14% |

|

Publishing |

18% |

|

Brewers |

19% |

|

Information Technology |

22% |

|

Movies & Entertainment |

28% |

|

Healthcare Equipment |

30% |

|

Telecom Services |

33% |

|

Pharmaceuticals |

33% |

|

Systems Software |

41% |

* From 1995 through 2017, the following industries (and others) in the S&P 500 had continually higher EBITDA margins than the health insurance/managed care industry:

* In 2009, the following exchange occurred on NBC:

Chris Matthews (MSNBC host):

Katty Kay (BBC’s Washington correspondent):

* In the last quarter of 2011 (earlier data not available), health insurance companies had a 4.5% quarterly net profit margin, as compared to 6.9% for electric utilities, 8.2% for gas utilities, and 12.0% for water utilities.[667] EBITDA margins for utilities are not available.[668]

* In 2010 on NPR’s All Things Considered, reporter Julie Rovner stated:

* In 2010, the average EBITDA margin for health insurance/managed care companies in the S&P 500 was 15% higher than automakers, 52% lower than brewers, and 69% lower than telecom companies:

* In 2011, the New York Times published a story by Reid Abelson stating:

* In the last quarter of 2011 (full-year data not available), health insurance companies had a 4.5% quarterly net profit margin, as compared to 2.9% for the New York Times Company,[673] 5.2% for music & video stores, 9.7% for toys & games, 14.0% for wireless communications, and 53.1% for periodical publishers.[674]

* In 2011, the average EBITDA margin for health insurance/managed care companies in the S&P 500 was 7% higher than auto parts & equipment, 59% lower than publishing, and 74% lower than pharmaceuticals:

* The facts in this section pertain to countries that are members of the Organization for Economic Cooperation and Development (OECD). This is a group of 38 mostly developed nations like Australia, Canada, Germany, Japan, and the United States. [677] [678]

* Per the Handbook of Health Economics, “results obtained with international comparisons should be treated with considerable caution.” The significance of such comparisons is limited by:

* A product or service is a luxury good if people spend a larger portion of their budget on it when their income increases.[682]

* Comparisons of developed countries show that healthcare is a luxury good: as national income increases, generally so does the portion of the economy spent on healthcare.[683] [684] [685] [686]

* Two common measures of nations’ wealth are:

* Among OECD nations, higher disposable income is generally associated with a greater portion of GDP spent on healthcare. In 2020, the U.S. had the highest average disposable income in the OECD and spent 19% of its economy on healthcare.[692]

* The relatively high healthcare spending in the U.S. may result from higher prices, but direct price comparisons are limited by a lack of comparable data. A 2018 study published by the Journal of the American Medical Association found that:

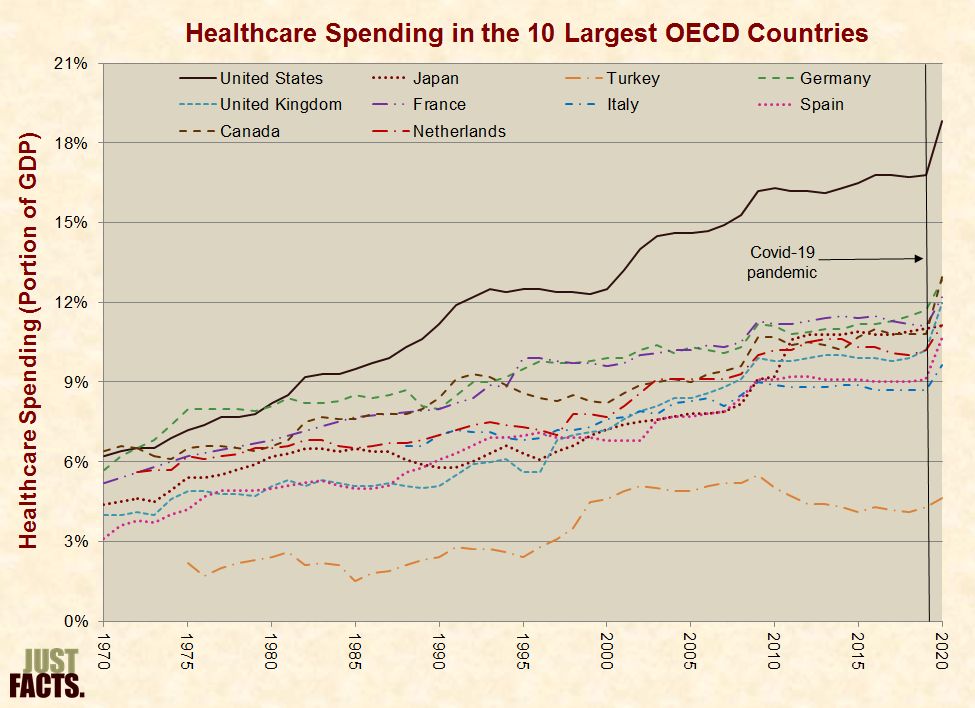

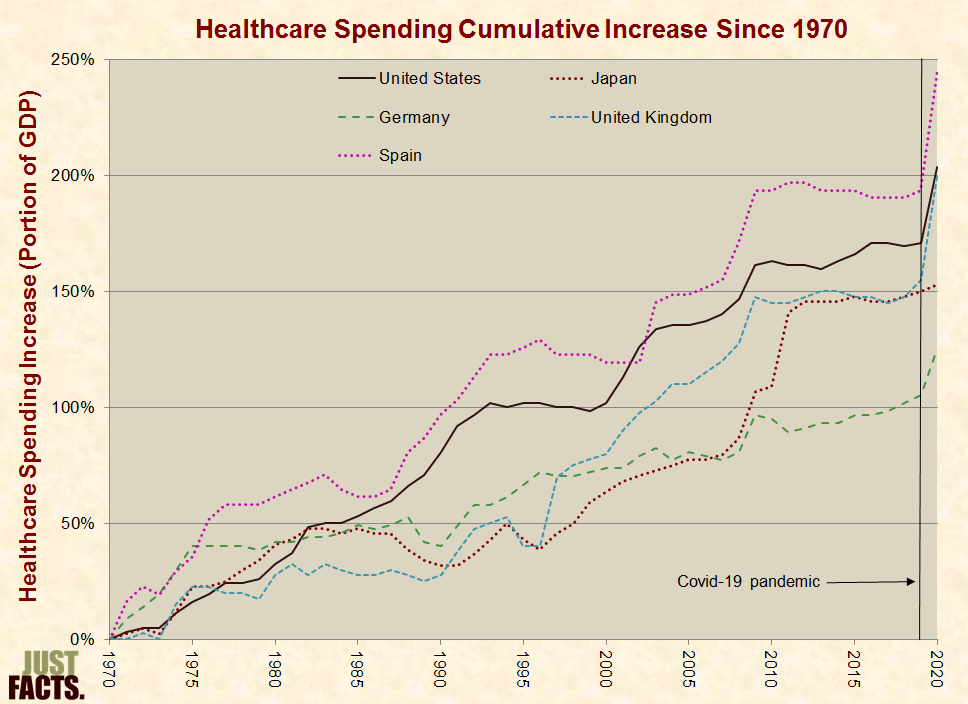

* From 1970 to 2020, healthcare spending as a portion of GDP in the 10 most-populated OECD countries grew as follows:

* From 1970 to 2020, healthcare spending as a portion of GDP rose by 203% in the United States. In the next four most-populated OECD countries with data available during that period, healthcare spending rose by 102% to 246%:

* Several factors can affect the quantity, quality, and appropriateness of the healthcare that people receive, including but not limited to:

* Rationing is a process of deliberately reducing people’s healthcare use to save money or restrict use of limited supplies.[706] [707] [708] [709] Some considerations that lead to rationing include but are not limited to:

* Rationing can include but is not limited to:

* In order to avoid the effects of rationing in their public or private insurance plan, some people purchase additional policies that:

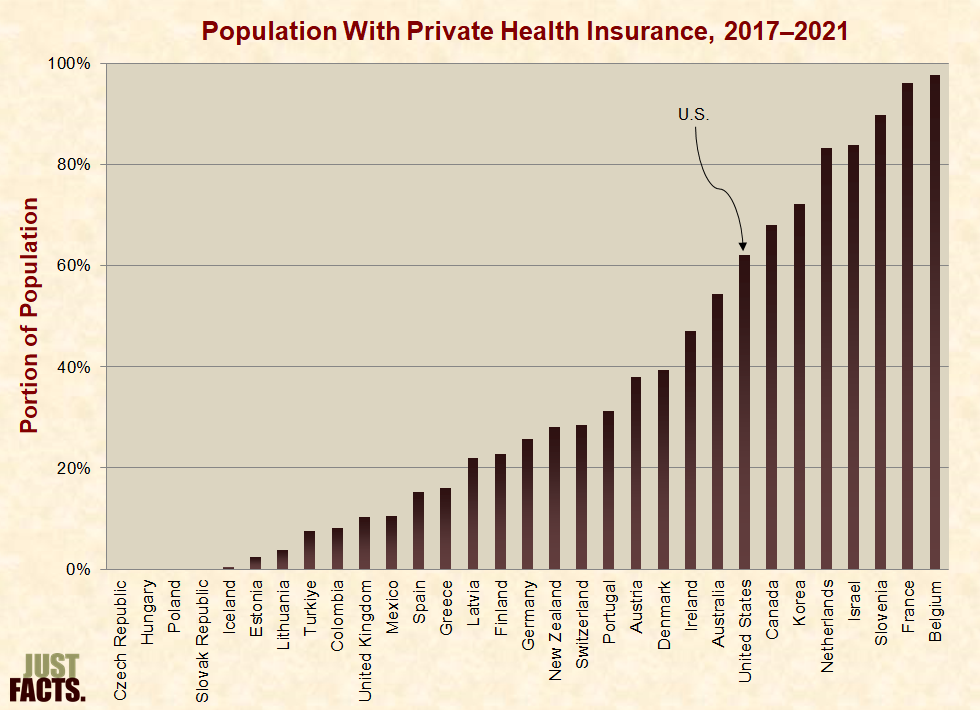

* The portion of people with private health insurance in the OECD ranges from 98% in Belgium to 0% in the Czech Republic, Hungary, Poland, and the Slovak Republic:

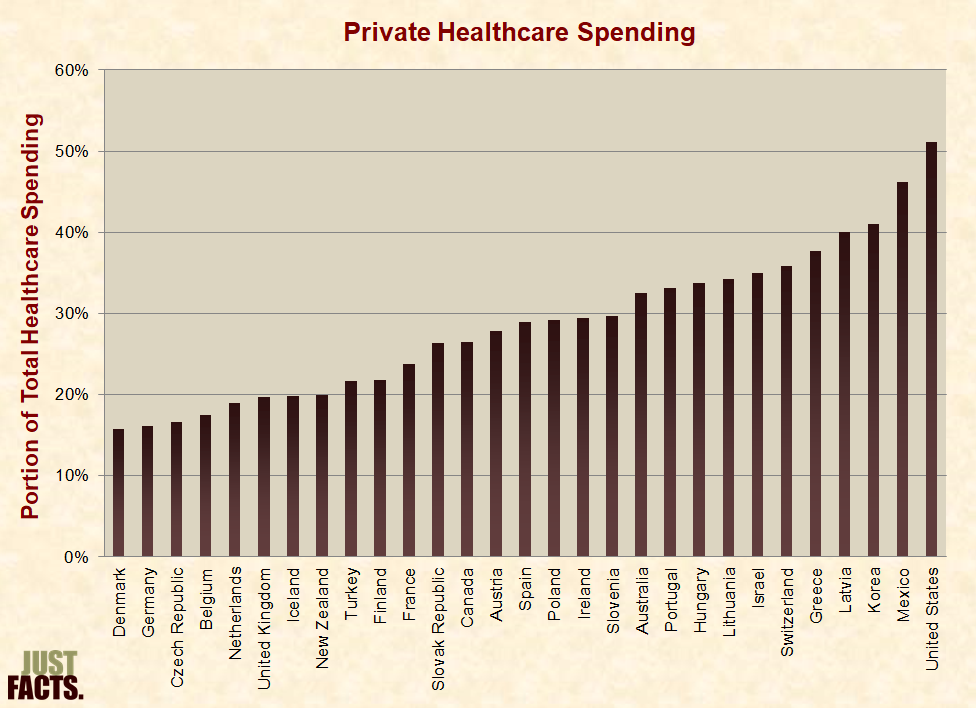

* In 2013, before Obamacare required most Americans to have health insurance or pay a fine, the U.S. led the OECD in the portion of all healthcare spending not provided or mandated by the government:

* Long wait times for health services can cause increased pain and disability, worse medical outcomes, and lost wages.[756] [757]

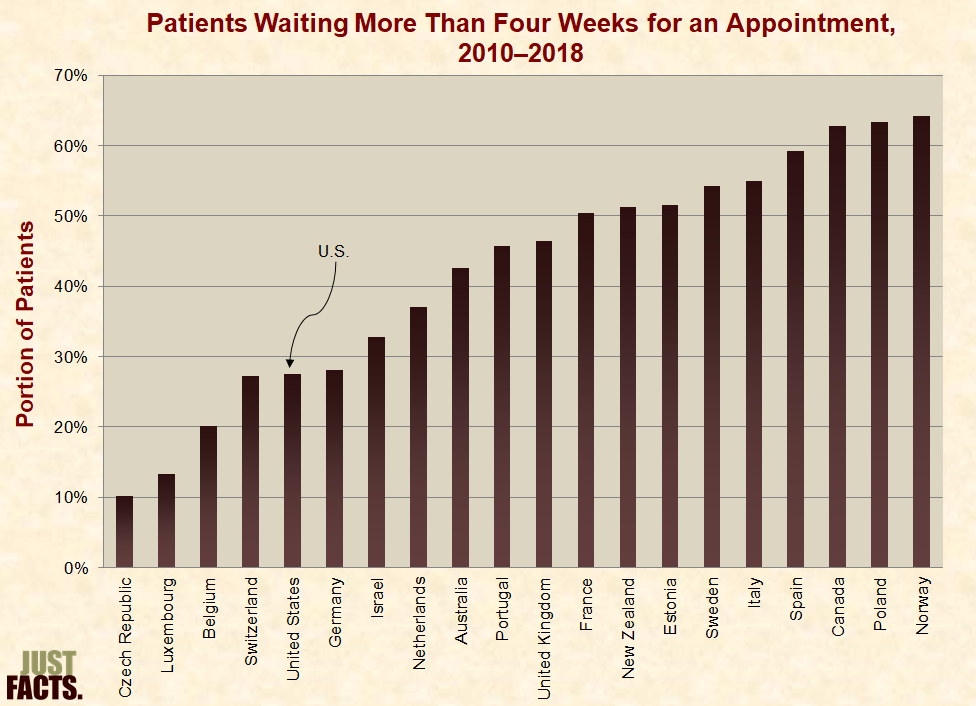

* According to survey data from 2010 to 2018,[758] the portion of patients who wait more than four weeks to get an appointment with a specialist ranges from 10% in the Czech Republic to 64% in Norway:

* Some contributing factors and outcomes of wait times in developed countries include:[761]

* The World Health Organization identifies human resources as the most important—and often the most costly—aspect of healthcare.[774]

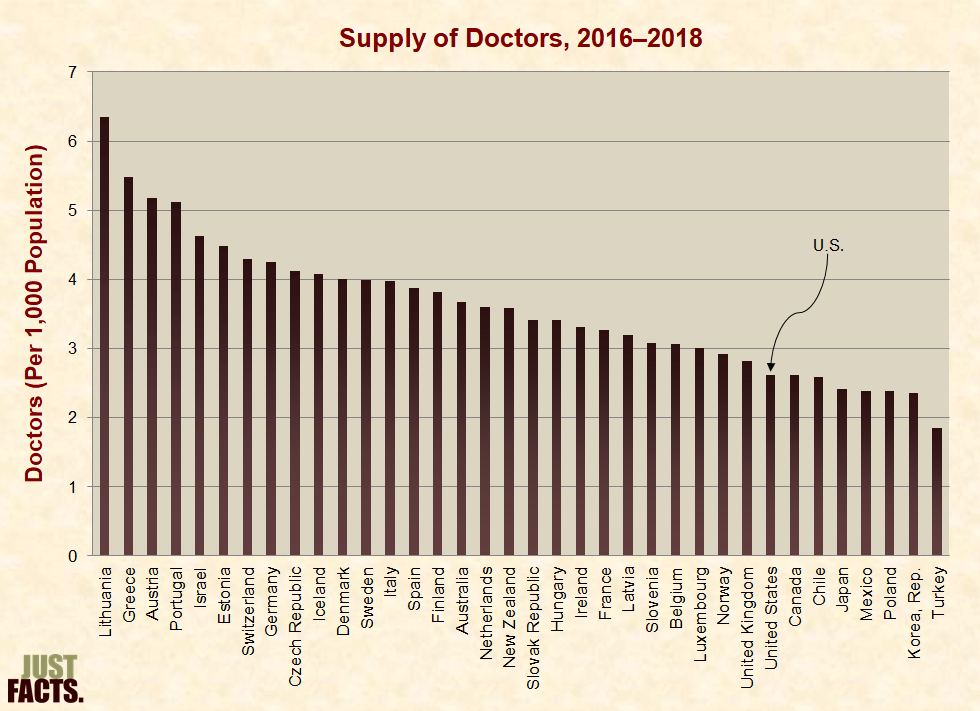

* The staff of medical professionals in OECD nations ranges from 1.8 to 6.4 doctors per 1,000 people. The United States has 2.6 doctors per 1,000 people, which is fewer than the OECD’s median of 3.5 and average of 3.6:

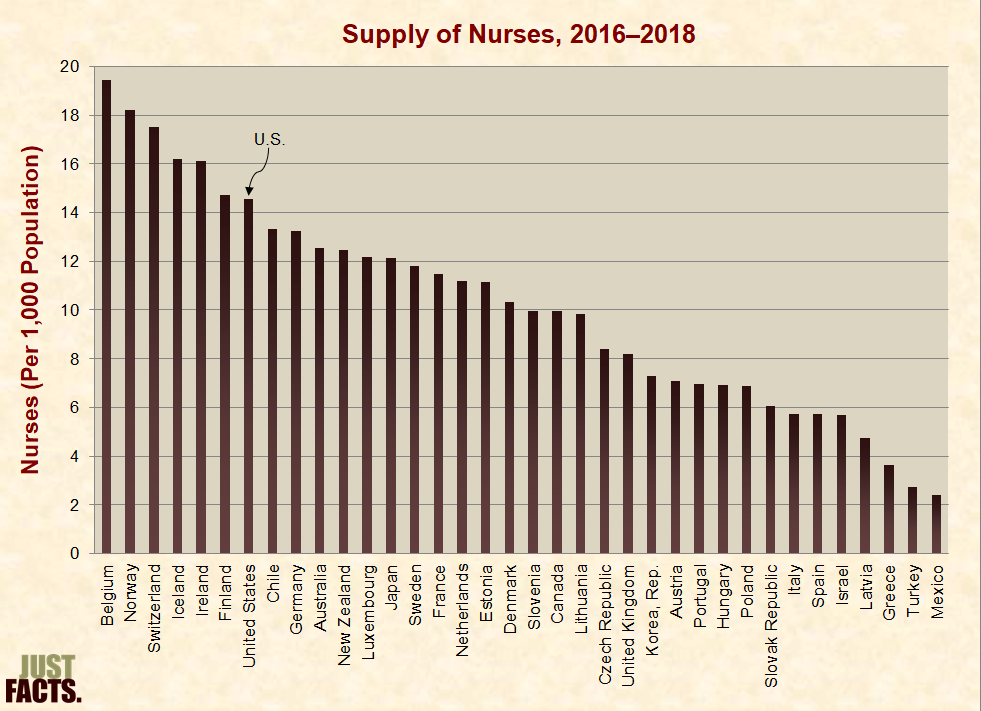

* The staff of medical professionals in OECD countries ranges from 2.4 to 19.5 nurses per 1,000 people. The United States has 14.5 nurses per 1,000 people, which is more than the OECD’s median of 10.1 and average of 10.2:

* The frequency of doctor visits differs between developed nations for various reasons, including but not limited to:

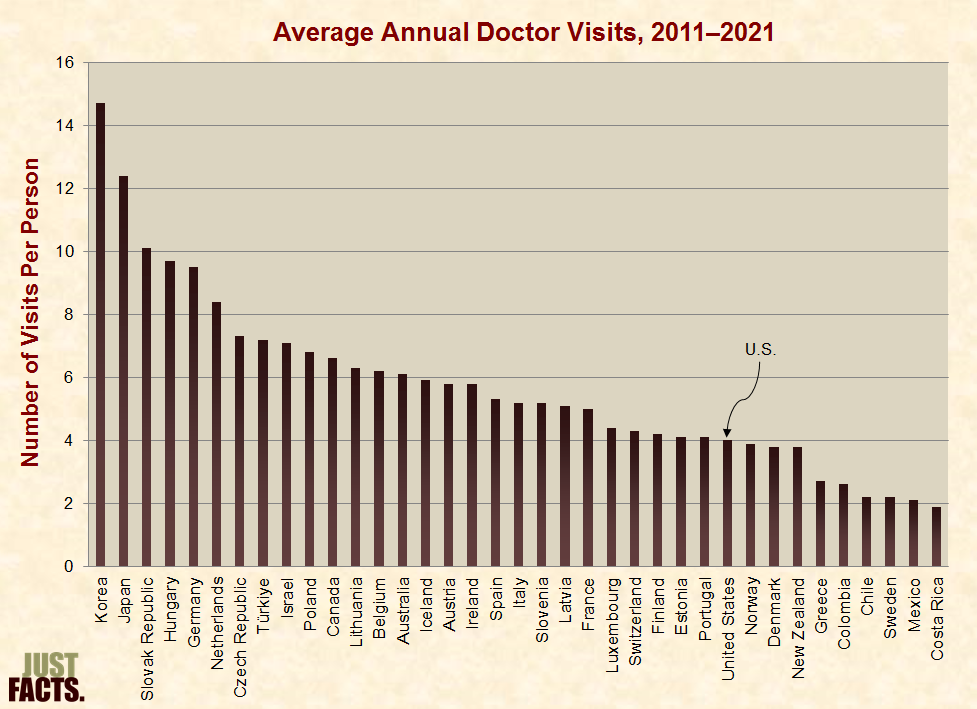

* In OECD nations, people visit a doctor in person an average of 5.8 times per year, with a median of 5.3 times. Americans visit a doctor about 4 times per year:

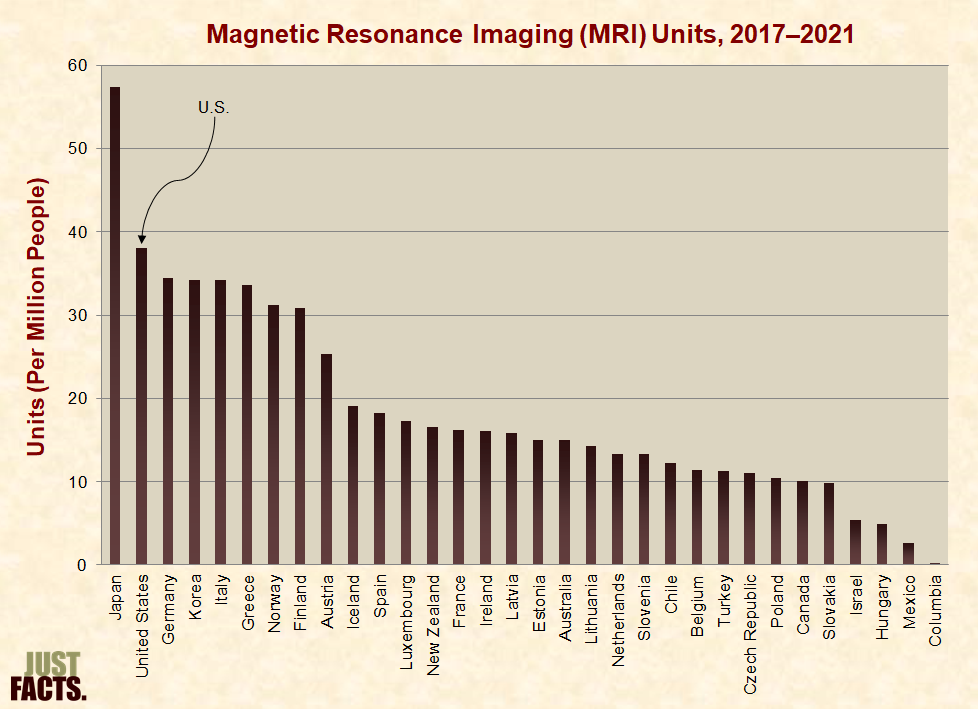

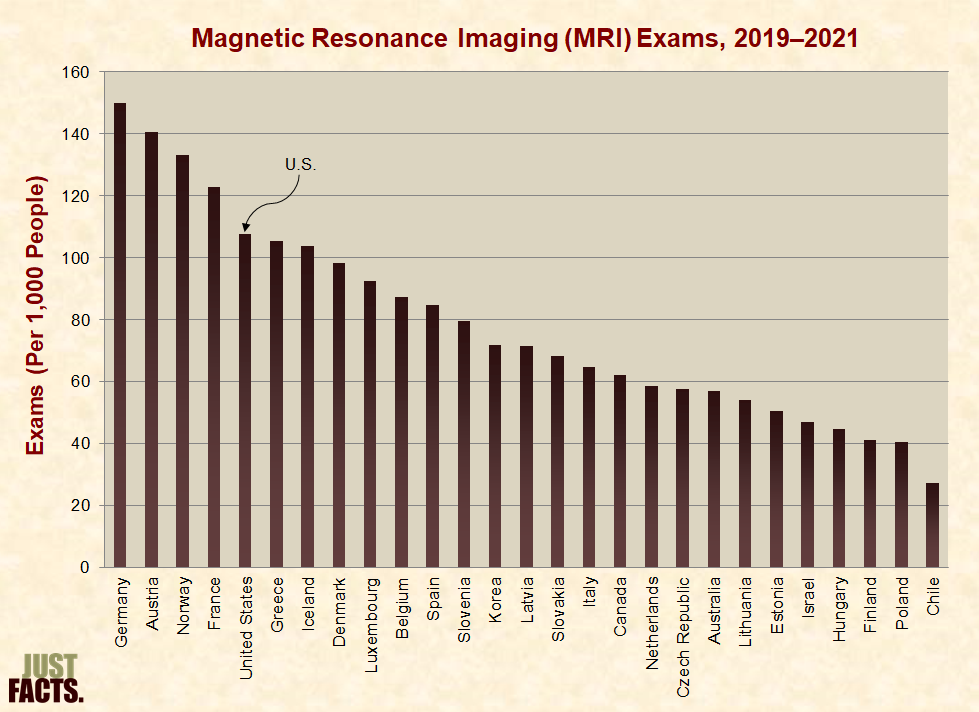

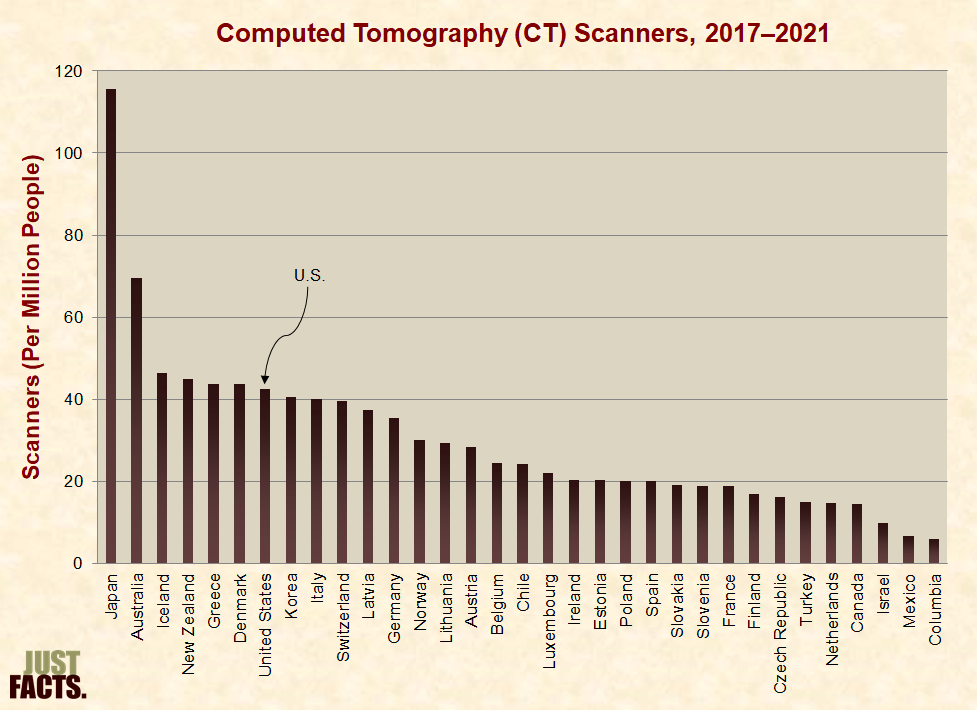

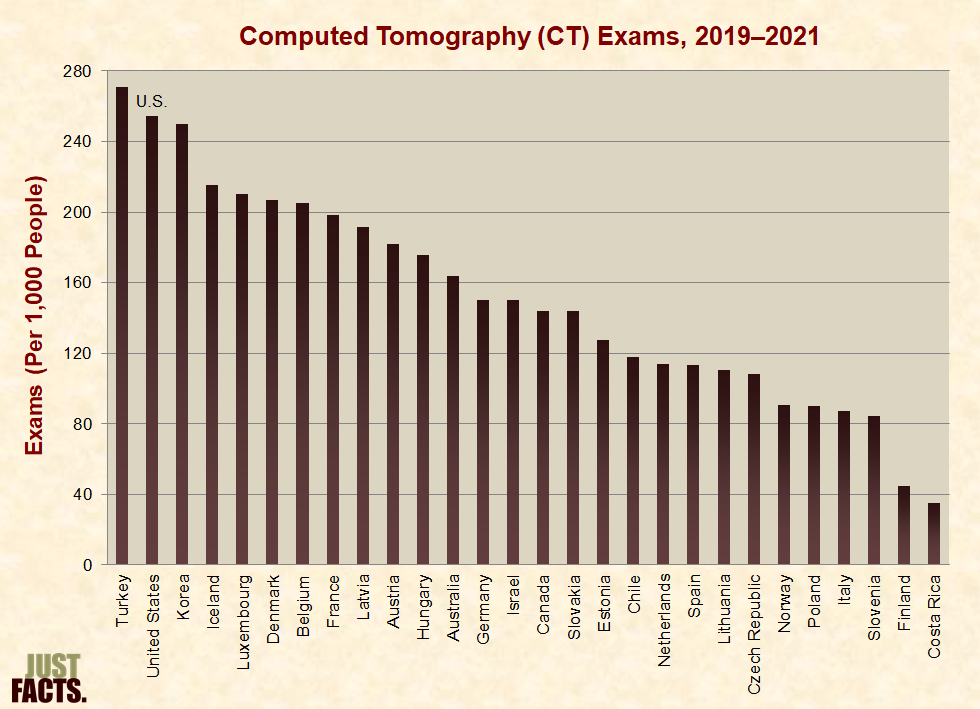

* Medical technologies such as Magnetic Resonance Imaging (MRI) and Computed Tomography (CT) are important for properly diagnosing diseases in order to improve the efficiency of treatments and reduce unnecessary procedures.[791] [792] [793] [794] [795] The OECD does not have guidelines for the ideal number of MRI units or CT scanners. Too few units could lead to long wait times, and too many units could lead to overuse.[796]

* The following four charts show the number and use of MRI units and CT scanners in OECD countries. The United States has more of these units and performs more of these exams than the average and median for the OECD:

* Certain cancer screenings can contribute to earlier diagnoses and more effective treatment. The World Health Organization recommends breast cancer screening for women aged 50–69.[801] [802] [803] In the OECD, screening rates for this target group range from 31% to 90% with a median of 74%:

* Per the textbook Neuropsychopharmacology: The Fifth Generation of Progress:

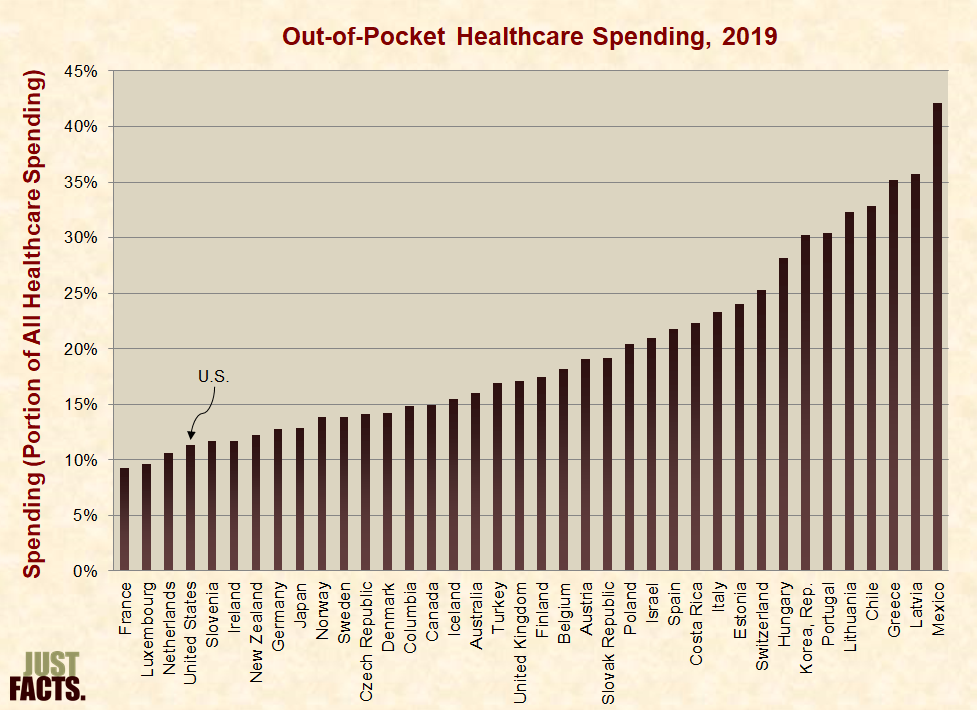

* The portion of medical expenses that patients pay out of pocket affects their use of healthcare services. The OECD states:

* In the majority of OECD countries, 100% of the population has health insurance. In the United States, approximately 90% of the population has health insurance. Mexico has the lowest insured rate with 72%.[809] [810] [811]

* Among OECD countries, the portion of healthcare expenditures that households pay out of pocket ranges from 9% in France to 42% in Mexico, with an average of 20% and a median of 17%. In the United States, households pay 11% of all healthcare expenditures:

* Cost control through rationing can prevent doctors from recommending medical care,[813] [814] and patients may forgo recommended treatment if their share of the cost is too high or if they think a doctor recommended a test or procedure only to protect against a lawsuit.[815] [816] [817]

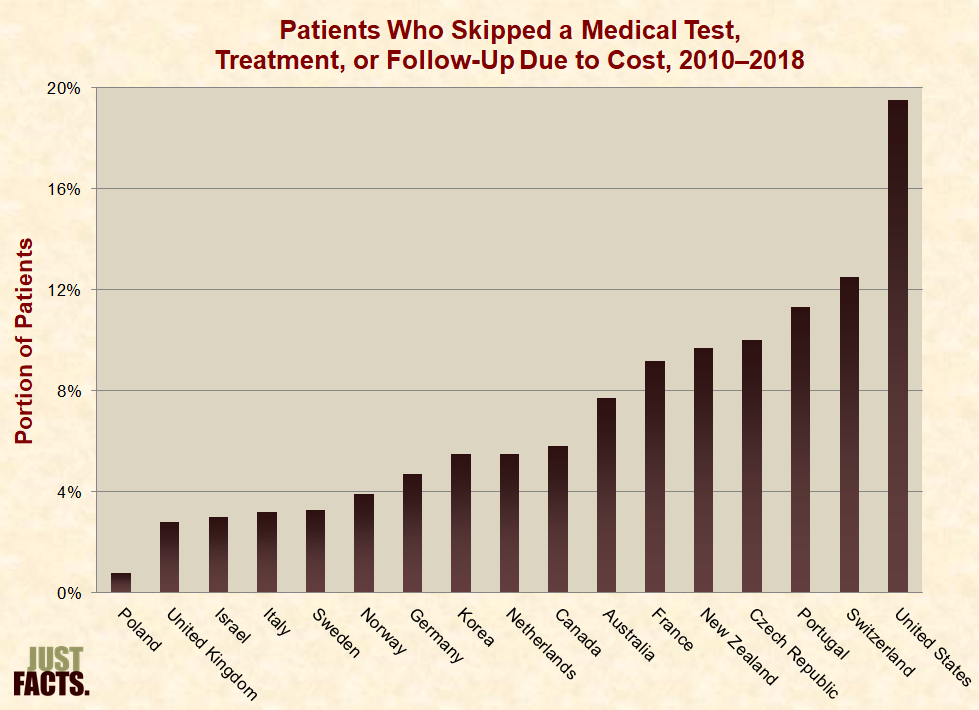

* According to the most recent survey data (collected during 2010–2018),[818] [819] [820] the portion of patients who skip recommended medical care due to cost ranges from about 1% in Poland to about 20% in the U.S.:

* When patients pay a lower (or no) portion of their medical expenses out of pocket, they use more healthcare services. This is called the moral hazard effect, and it was demonstrated in two randomized health insurance experiments:[823] [824]

* Government-run health systems and private insurance companies sometimes use rationing to limit overutilization from the moral hazard effect.[829]

* Healthcare outcomes measure if medical care improves patient health. These are not the same as health outcomes, which also reflect a range of non-medical factors.[830] [831]

* Cancer survival rates reflect how effectively healthcare systems provide early detection and treatment.[832] [833] The United States has higher cancer survival rates than the average and median of OECD countries for three out of four common types of cancer:

|

Five-Year Cancer Survival Rates, 2010–2014 |

|||

|

Cancer |

OECD Average |

OECD Median |

United States |

|

Breast |

85% |

86% |

90% |

|

Cervical |

66% |

66% |

63% |

|

Colon |

62% |

64% |

65% |

|

Rectal |

61% |

63% |

64% |

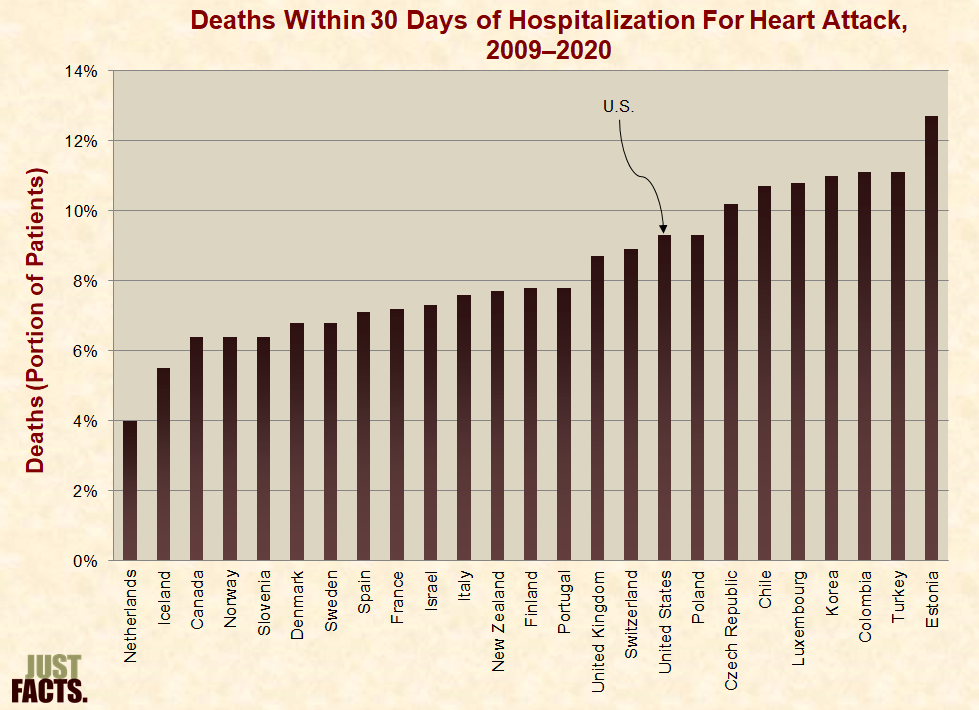

* Per the OECD, measuring the mortality rate of patients hospitalized for a heart attack is a “good indicator of acute care quality” because it “reflects the processes of care, such as timely transport of patients and effective medical interventions.”[836] [837]

* In the United States, about 9% of patients hospitalized for a heart attack die within 30 days, which is also the median for OECD countries:

* Per the OECD, health outcomes, as opposed to healthcare outcomes, are “not only related to health spending and the performance of health systems, but also to a wide range of non-medical determinants of health.”[839] [840]

* Besides healthcare, other factors that can affect life expectancy include but are not limited to:

* When comparing health outcomes in the United States to those of other countries, a 2019 paper in the Journal of the American Medical Association explains that:

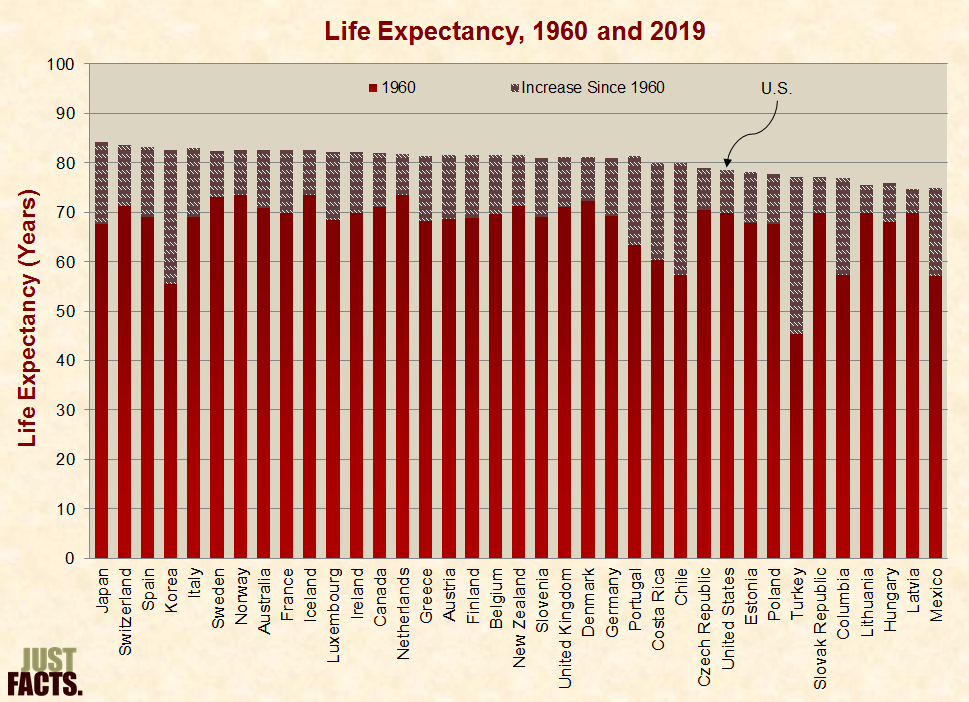

* From 1960 to 2019, OECD nations gained between five and 32 years of life expectancy. In 2019, prior to the outset of the Covid-19 pandemic,[846] life expectancy ranged from 75 to 84 years, with an average of 81 and a median of 82:

* Most non-communicable diseases are linked to tobacco use, physical inactivity, unhealthy diet, or alcohol overuse.[848] [849] Among people in OECD countries:

* In the United States, the death rate from non-health causes (like accidents, suicides, and assaults) is 78% higher than the average for developed countries.[854]

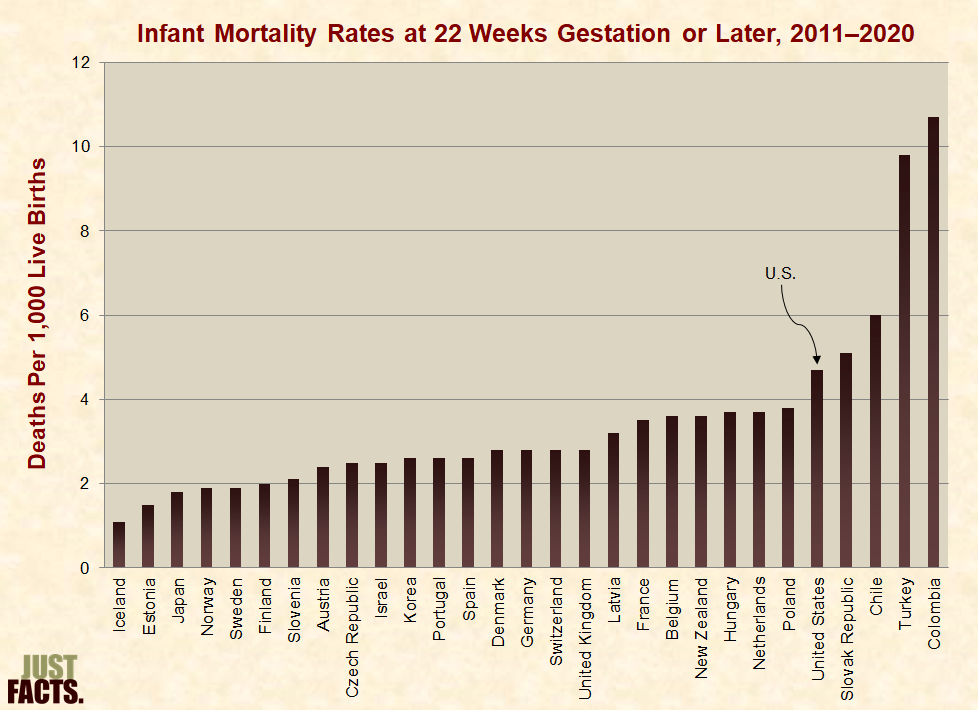

* Infant mortality rates can vary between countries because of differences in birth registration practices. For example, some countries use a minimum weight or gestational age to define a live birth.[855] [856] [857] Based on data that only includes births at or after 22 weeks of gestation or weighing at least 500 grams, the infant mortality rate in the U.S. is the fifth highest in the OECD:

* Besides healthcare, other factors that can affect infant mortality rates include but are not limited to:

[1] Calculated with data from:

a) Dataset: “National Health Expenditures by Type of Service and Source of Funds: Calendar Years 1960 to 2020.” U.S. Department of Health & Human Services, Centers for Medicare and Medicaid Services, December 1, 2021. <www.cms.gov>

b) Dataset: “CPI—All Urban Consumers (Current Series).” U.S. Department of Labor, Bureau of Labor Statistics. Accessed March 5, 2021 at <www.bls.gov>

“Series Id: CUUR0000SA0; Series Title: All Items in U.S. City Average, All Urban Consumers, Not Seasonally Adjusted; Area: U.S. City Average; Item: All Items; Base Period: 1982–84=100”

c) Dataset: “Table 1.1.5: Gross Domestic Product [Billions of Dollars].” United States Department of Commerce, Bureau of Economic Analysis. Last revised February 25, 2021. <www.bea.gov>

Line 1: “Gross Domestic Product”

d) Dataset: “Table 7.1. Selected Per Capita Product and Income Series in Current and Chained Dollars.” U.S. Department of Commerce, Bureau of Economic Analysis. Last revised February 25, 2021. <www.bea.gov>

Line 18: “Population (Midperiod, Thousands)”

NOTE: An Excel file containing the data and calculations is available upon request.

[2] Calculated with data from:

a) Dataset: “National Health Expenditures by Type of Service and Source of Funds: Calendar Years 1960 to 2020.” U.S. Department of Health & Human Services, Centers for Medicare and Medicaid Services, December 1, 2021. <www.cms.gov>

b) Dataset: “Table 1.1.5: Gross Domestic Product (Billions of Dollars).” United States Department of Commerce, Bureau of Economic Analysis. Last revised February 25, 2021. <www.bea.gov>

Line 1: “Gross Domestic Product”

NOTE: An Excel file containing the data and calculations is available upon request.

[3] Receipt: Christ Hospital, 176 Palisade Avenue, Jersey City, NJ, 1942.

|

Service |

Price ($) |

|

Hospital room ($7.00 per day) |

70.00 |

|

Operating Room Fee (Baby circumcision) |

5.00 |

|

Laboratory Fee |

1.00 |

|

Maternity Room |

15.00 |

|

Care of Baby |

7.50 |

|

Total |

98.50 |

|

Special Allowance |

–33.50 |

|

Balance |

65.00 |

NOTE: Just Facts has examined the original receipt and has a scanned copy of it, but we are not publishing this image because it contains personal information.

[4] Webpage: “CPI Inflation Calculator.” Bureau of Labor Statistics. Accessed October 12, 2011 at <www.bls.gov>

“$7.00 in 1942 has the same buying power as $97.29 in 2011”

[5] Email from Christ Hospital, 176 Palisade Avenue, Jersey City, NJ, September 23, 2011.

For a normal vaginal delivery (limit of 2 days) the fee for the hospital service will be $4000.00. Any additional days over the normal 2 day stay will incur a charge of $1360.00 per day.

For a cesarean section delivery (limit of 4 days) the fee for the hospital service will be $5565.00. Any additional days over the normal 4 day stay will incur a charge of $1360.00 per day.

This quoted price is for a standard Vaginal Delivery/Cesarean Section and normal newborn birth barring any unforeseen complications which could add to this billable amount.

* This amount is payable in full prior to discharge.

* A $500.00 deposit is required at time of pre-registration.

* Patient Access staff will flag your account when they obtain your demographic information in order to insure a smooth admission process.

* The above amounts do not include physician fees, anesthesia, or any other professional component.

[6] Ohio Revised Code, Title 37, Chapter 3727, Section 3727.42: “Price Information List.” Ohio General Assembly. Accessed November 7, 2022 at <law.justia.com>

Effective: September 10, 2012 …

(A) Every hospital shall compile and make available for inspection by the public a price information list containing the information specified in division (B) of this section and shall periodically update the list to maintain current information. The price information list shall be compiled and made available in a format that complies with the electronic transaction standards and code sets adopted by the United States secretary of health and human services under 42 U.S.C. 1320d-2.

(B) Each price information list required by division (A) of this section shall contain all of the following information:

(1) The usual and customary room and board charges for each level of care within the hospital, including but not limited to private rooms, semiprivate rooms, other multiple patient rooms, and intensive care and other specialty units;

(2) Rates charged for nursing care, if the hospital charges separately for nursing care;

(3) The usual and customary charges, stated separately for inpatients and outpatients if different charges are imposed, for any of the following services provided by the hospital:

(a) The thirty most common x-ray and radiological procedures;

(b) The thirty most common laboratory procedures;

(c) Emergency room services;

(d) Operating room services;

(e) Delivery room services;

(f) Physical, occupational, and pulmonary therapy services;

(g) Any other services designated as high volume services by a rule which shall be adopted by the director of health.

(4) The hospital’s billing policies, including whether the hospital charges interest on an amount not paid in full by any person or government entity and the interest rate charged;

(5) Whether or not the charges listed include fees for the services of hospital-based anesthesiologists, radiologists, pathologists, and emergency room physicians and, if a charge does not include such fees, how such fee information can be obtained.

(C) Every hospital shall do all of the following with the price information list required by this section:

(1) At the time of admission, or as soon as practical thereafter, inform each patient of the availability of the list and on request provide the patient with a free copy of the list;

(2) On request, provide a paper copy of the list to any person or governmental agency, subject to payment of a reasonable fee for copying and processing;

(3) Make the list available free of charge on the hospital’s internet web site.

[7]

|

Hospital |

Price |

Type of Room |

|

$1,905 |

Semi-private |

|

|

$2,040 |

Routine care |

|

|

$2,828 |

Semi-private |

|

|

$2,166 |

Medical/surgical (no option for routine care or semi-private) |

|

|

$3,675 |

Medical/surgical private (no option for routine care or semi-private) |

|

|

$3,582 |

Medical/surgical (no option for routine care or semi-private) |

|

|

$1,849 |

Semi-private medical/surgical |

|

|

$1,659 |

Medical/surgical |

|

|

$2,246 |

Semi-private |

|

|

$2,460 |

Semi-private |

|

|

$1,894 |

Semi-private medical/surgical |

|

|

$1,155 |

Private |

|

|

$3,108 |

Private or semi-private |

|

|

$3,675 |

Medical/surgical (private or semi-private) |

|

|

$1,622 |

Private |

|

|

Average† |

$2,391 |

|

|

Median† |

$2,166 |

NOTES:

[8] Article: “70% Rise in Hospital Room Costs Since 1980.” Associated Press, November 5, 1986. <www.nytimes.com>

“The average daily cost of hospital rooms jumped nearly 70 percent over the last five years, from $127 in 1980, according to statistics published by the Census Bureau. The figures were drawn from data compiled by the Health Insurance Association of America and the American Hospital Association.”

NOTE: Just Facts searched the websites of the Census Bureau, Health Insurance Association of America [now America’s Health Insurance Plans], and the American Hospital Association for up-to-date data on the average price of hospital rooms, but we were unable to find such information. Just Facts also contacted the American Hospital Association, which was unable to provide any data beyond 2002. This data is cited in footnotes below.

[9] Webpage: “CPI Inflation Calculator.” Bureau of Labor Statistics. Accessed November 7, 2022 at <www.bls.gov>

“$127.00 in January 1980 has the same buying power as $458.94 in January 2022”

[10] Book: Current Trends in Health Care and Dental Costs Utilization. Mutual of Omaha, 2003.

Page 2: “The data in Current Trends represents Mutual of Omaha’s group business, and is not necessarily representative of other population subgroups. The data is based upon the actual experience of our policyholders. The data does not necessarily represent a cross section of all providers. No efforts have been made to adjust for differences in case mix.”

Page 3: “The average room and board charges are for all types of rooms (medical/surgical, intensive care, obstetrical, etc.), and they include charges for nursing care for those facilities with separate room and board charges from nursing charges.”

[11] Book: Current Trends in Health Care Costs and Utilization. Mutual of Omaha, 1990.

Page 5: “Average Daily Charges for Room and Board … 1988 … National Average [=] $270.”

[12] Webpage: “CPI Inflation Calculator.” Bureau of Labor Statistics. Accessed November 7, 2022 at <www.bls.gov>

“$270 in January 1988 has the same buying power as $656.09 in January 2022”

[13] Book: Current Trends in Health Care and Dental Costs Utilization. Mutual of Omaha, 2003.

Page 5: “Average Daily Charges for Room and Board … 2002 … National Average [=] $748.”

[14] Webpage: “CPI Inflation Calculator.” Bureau of Labor Statistics. Accessed November 7, 2022 at <www.bls.gov>

“$748 in January 2002 has the same buying power as $1,187.46 in January 2022”

[15] Book: Practical Decision Making in Health Care Ethics: Cases and Concepts (3rd edition). By Raymond J. Devettere. Georgetown University Press, 2010.

Pages 459–460:

Thanks to Medicare, Medicaid, and the various other insurance programs, by the last third of the twentieth century most people in the United States were not paying for hospitals and doctors with their own money. They were covered by nonprofit insurance plans such as Blue Cross or Blue Shield, commercial (for profit) insurance plans, or the government plans. All these plans became known as third-party payers. The phrase third-party payer means someone other than the patient (first party) or the providers (the second party—doctors, hospitals, pharmacies, etc.) is paying for medical care.

[16] Calculated with the dataset: “National Health Expenditures by Type of Service and Source of Funds: Calendar Years 1960 to 2020.” U.S. Department of Health & Human Services, Centers for Medicare and Medicaid Services, December 1, 2021. <www.cms.gov>

NOTE: An Excel file containing the data and calculations is available upon request.

[17] Article: “Scientific Survey Shows Voters Widely Accept Misinformation Spread By the Media.” By James D. Agresti. Just Facts, January 2, 2020. <www.justfacts.com>

The findings are from a nationally representative annual survey commissioned by Just Facts, a non-profit research and educational institute. The survey was conducted by Triton Polling & Research, an academic research firm that used sound methodologies to assess U.S. residents who regularly vote. …

The survey was conducted by Triton Polling & Research, an academic research firm that serves scholars, corporations, and political campaigns. The responses were obtained through live telephone surveys of 700 likely voters across the U.S. during December 2–11, 2019. This sample size is large enough to accurately represent the U.S. population. Likely voters are people who say they vote “every time there is an opportunity” or in “most” elections.

The margin of sampling error for the total pool of respondents is ±4% with at least 95% confidence. The margins of error for the subsets are 6% for Democrat voters, 6% for Trump voters, 5% for males, 5% for females, 12% for 18 to 34 year olds, 5% for 35 to 64 year olds, and 6% for 65+ year olds.

The survey results presented in this article are slightly weighted to match the ages and genders of likely voters. The political parties and geographic locations of the survey respondents almost precisely match the population of likely voters. Thus, there is no need for weighting based upon these variables.

NOTE: For facts about what constitutes a scientific survey and the factors that impact their accuracy, visit Just Facts’ research on Deconstructing Polls & Surveys.

[18] Dataset: “Just Facts 2019 U.S. Nationwide Survey.” Just Facts, December 2019. <www.justfacts.com>

Page 5:

Q22: In 1960, governments paid for 24% of all healthcare costs in the U.S. Do you think governments now pay a greater portion or a lesser portion of all healthcare costs in the U.S.?

Greater [=] 56.6%

Lesser [=] 38.0%

Unsure [=] 5.1%

[19] For facts about how surveys work and why some are accurate while others are not, click here.

[20] Article: “Nonprice Competition in Hospitals.” By John L. Mariotti. Encyclopedia of Health Care Management. Edited by Michael J. Stahl. Sage Publications, 2004.

Page 391: “In conclusion, because most medical care is delivered with third-party payments, and the purchaser is in dire need of the services, the typical patient has little interest in price. The result is that most medical care is bought on decision criteria other than price. Thus, nonprice competition seems to be the norm, not only in hospitals but also in a wide range of health and medical services.”

[21] Book: Practical Decision Making in Health Care Ethics: Cases and Concepts (3rd edition). By Raymond J. Devettere. Georgetown University Press, 2010.

Pages 459–460:

The shift from patient payment to third-party payment did not immediately disturb the basic FFS [fee-for-service] system. Providers of medical services—hospitals, physicians, pharmacies, and others—continued charging fees for their goods and services. The only major difference was that a party other than the patient or family paid the fees that were billed.

FFS Flaws

Two major structural flaws eventually undermined this combined FFS/third-party payment system. First, the third-party payers had no control over the extent or the cost of the services rendered. Patients decided when to seek treatment, physicians controlled what they would provide and, along with hospitals and pharmacies, what fees they would charge for their services. The third-party payers had no say in the services provided or the fees charged; they simply paid the bills.

The second structural flaw was the incredible built-in incentive for providers to raise their fees rapidly. In the FFS/third-party payer system, the government or the insurance company pays whatever fees are considered customary for the service or medicine. What determines a “customary” fee? Obviously a customary fee is a fee roughly the same as what other physicians, hospitals, and drug companies in the same geographical area are charging. Hence, the faster everyone raises their fees, the faster what is considered “customary” also rises. As long as patients and their families were paying the fees, physicians and hospitals tended to be sensitive to what they charged these people. But when the billing shifted to anonymous government and institutional payers—the third-party payers—it did not take long for everyone reimbursed by these third-party payers to begin to raise their fees rapidly, thereby raising the level of what was considered customary.

[22] Report: “Drug Industry: Profits, Research and Development Spending, and Merger and Acquisition Deals.” U.S. Government Accountability Office, November 17, 2017. <www.gao.gov>

Page 13:

According to economic experts, the usual mechanisms that enforce market discipline may not work in the same way in the health care market as they do in other markets. In most markets—automobiles, for example—consumers are expected to be conscious of the price of goods. If a company raises the price of its goods, consumers would likely purchase fewer goods, causing the company’s revenues to decline. However, in the health care market, the purchase of goods and services is largely influenced by health care providers, who may not be well-informed about, or incentivized to consider, the prices involved. In the case of drugs, some experts argue that marketing and advertising may further distort provider decision making. In addition, if the patients’ medical bills are largely paid by insurance plans (other than copayment or coinsurance costs), then patients’ demand may not be significantly influenced by changes in price to the extent that it might be in other markets where the consumers see and pay the bill themselves.

[23] Paper: “Some Interim Results From a Controlled Trial of Cost Sharing.” By Joseph P. Newhouse and others. Rand Corporation, January 1982. <www.rand.org>

Page iii: “[T]he first regular sample [of study participants] was enrolled in late 1974. Most participants have now completed their period of participation, and all will complete it by January 1982.”

Page v:

A total of 7706 participants in six cities have taken part in a controlled experiment related to cost sharing in health insurance policies. …

The families were assigned in an unbiased manner to insurance plans that covered a broad range of medical services but varied the coinsurance rate, i.e., the fraction of its medical bills that the family must pay. This out-of-pocket expenditure was subject to an upper limit of $1000 per year or 5, 10, or 15% of income, whichever was less.

Page 4: “A total of 2756 families, consisting of 7706 persons, have been enrolled in one of several different health insurance plans, 70 percent of them for 3 years and the rest for 5 years.”

[24] Calculated with data from the webpage: “CPI Inflation Calculator.” Bureau of Labor Statistics. Accessed November 7, 2022 at <www.bls.gov>

“$1,000 in January 1974 has the same buying power as $6,033.22 in January 2022”

“$1,000 in January 1982 has the same buying power as $2,981.42 in January 2022”

CALCULATION (to obtain an average of the figures above): ($6,033.22 + $2,981.42) / 2 = $4,507

[25] Paper: “Some Interim Results From a Controlled Trial of Cost Sharing.” By Joseph P. Newhouse and others. Rand, January 1982. <www.rand.org>

Page iii: “[T]he first regular sample [of study participants] was enrolled in late 1974. Most participants have now completed their period of participation, and all will complete it by January 1982.”

Page v:

A total of 7706 participants in six cities have taken part in a controlled experiment related to cost sharing in health insurance policies. …

The families were assigned in an unbiased manner to insurance plans that covered a broad range of medical services but varied the coinsurance rate, i.e., the fraction of its medical bills that the family must pay. This out-of-pocket expenditure was subject to an upper limit of $1000 per year or 5, 10, or 15% of income, whichever was less. …

Expenditure per person responds to variation in cost sharing. It is about 50 percent greater in the plan with no cost sharing [100% coverage] than in the one with 95-percent coinsurance [5% coverage] up to a maximum of $1000 in any one year. …

As cost sharing declines, the percentage of individuals seeking care rises, as does the number of ambulatory [outpatient] visits per user. The number of adults hospitalized increases, but the number of children hospitalized shows no systematic relationship to plan. Cost per person hospitalized does not appear to be related to plan.

Pages v–vi: “The implications of these findings are that: 1) Cost sharing unambiguously reduces expenditure; it is not ‘penny-wise and pound-foolish’ (with respect to expenditure) as some have argued.”

Page 4: