Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

* A “tax” is defined by the Collins English Dictionary as a “compulsory financial contribution imposed by a government to raise revenue….”[1]

* In 2022, U.S. federal, state and local governments collected a combined total of $7.1 trillion in taxes, or more precisely, $7,146,628,750,000. This amounts to:

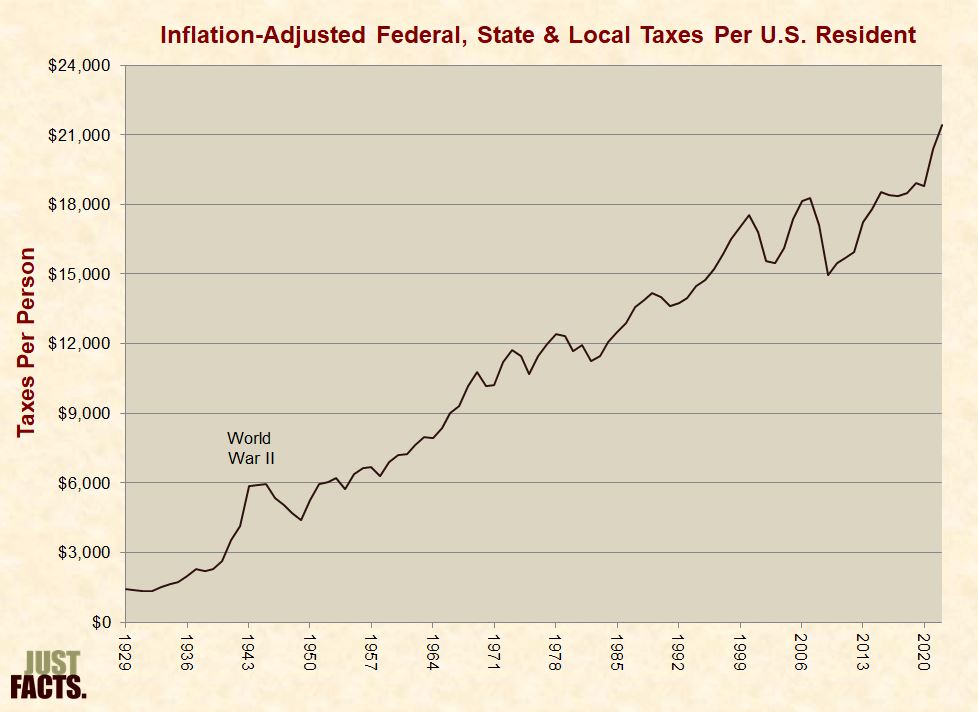

* From 1929 to 2022, inflation-adjusted federal, state and local tax collections per person in the U.S. have ranged from $1,333 to $21,423 per year, with a median of $11,458 and an average of $10,697. In 2022, they were $21,423, or 100% above the average:

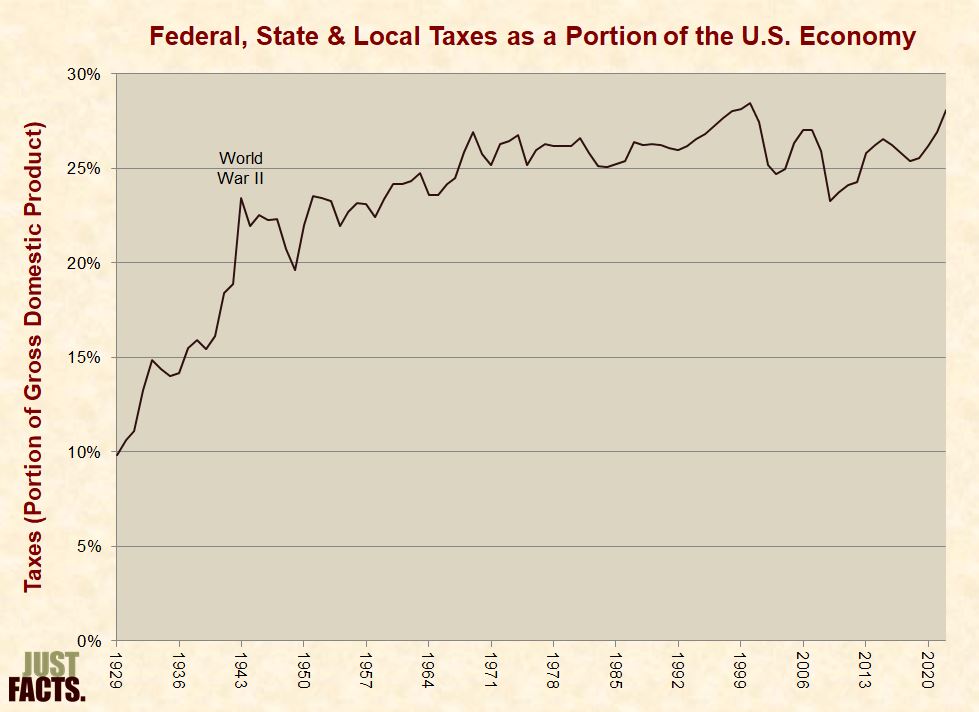

* From 1929 to 2022, the portion of the U.S. economy collected in federal, state and local taxes has ranged from 10% to 28%, with a median of 25% and an average of 24%. In 2022, it was 28%, or 19% above the average:

* Per the U.S. Government Accountability Office, when government spends more than it collects in revenues, the resulting debt is “borne by tomorrow’s workers and taxpayers.” This burden can manifest in the form of higher taxes, lower wages, reduced government benefits, decreased economic growth, inflation, or combinations of such results.[7] [8] [9] [10]

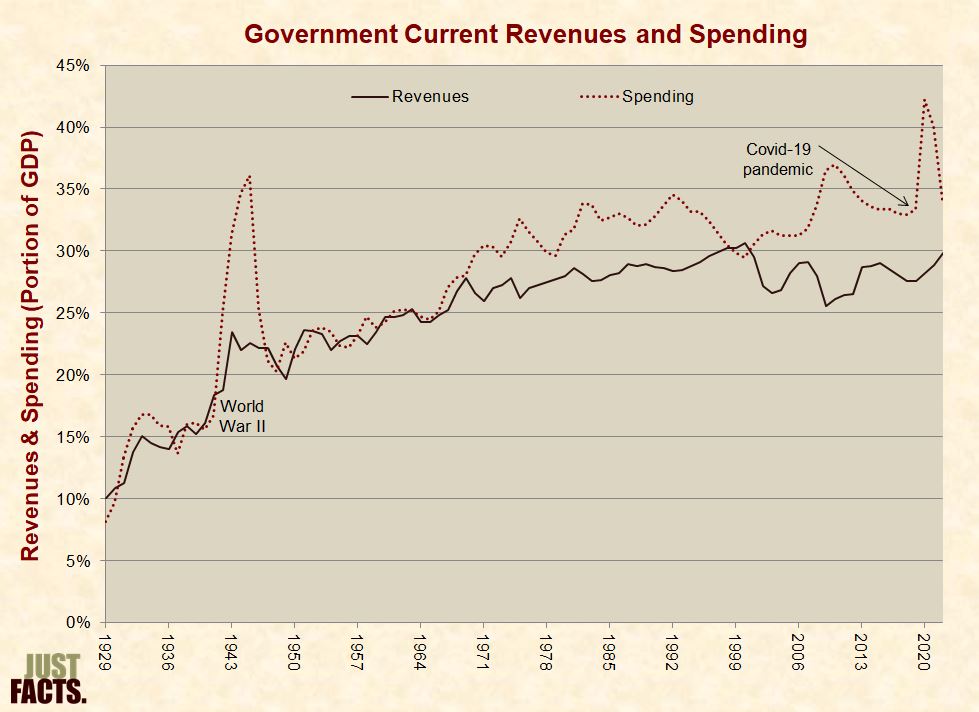

* In 2022, federal, state and local governments spent $8.7 trillion for current programs and received $7.6 trillion in revenues, leaving a gap of $1.1 trillion. This amounts to 4.1% of the U.S. economy and an average of $8,006 for every household in the U.S.:

* In addition to government debts, explicit and implicit government obligations such as public employee pensions and Social Security/Medicare benefits also constitute a burden on future taxpayers.[15]

* At the close of the federal government’s 2023 fiscal year, the federal government had $144.3 trillion in debts, liabilities, and unfunded obligations. This shortfall equates to $430,252 for every person living in the United States, or $1,098,087 per household.[16]

* In 2022, the U.S. federal government collected $4.8 trillion in taxes, or more precisely, $4,834,240,000,000. This amounts to:

* From 1929 to 2022, inflation-adjusted federal tax collections per person in the U.S. have ranged from $275 to $14,491 per year, with a median of $7,604 and an average of $7,113. In 2022, they were $14,491, or 104% above the average:

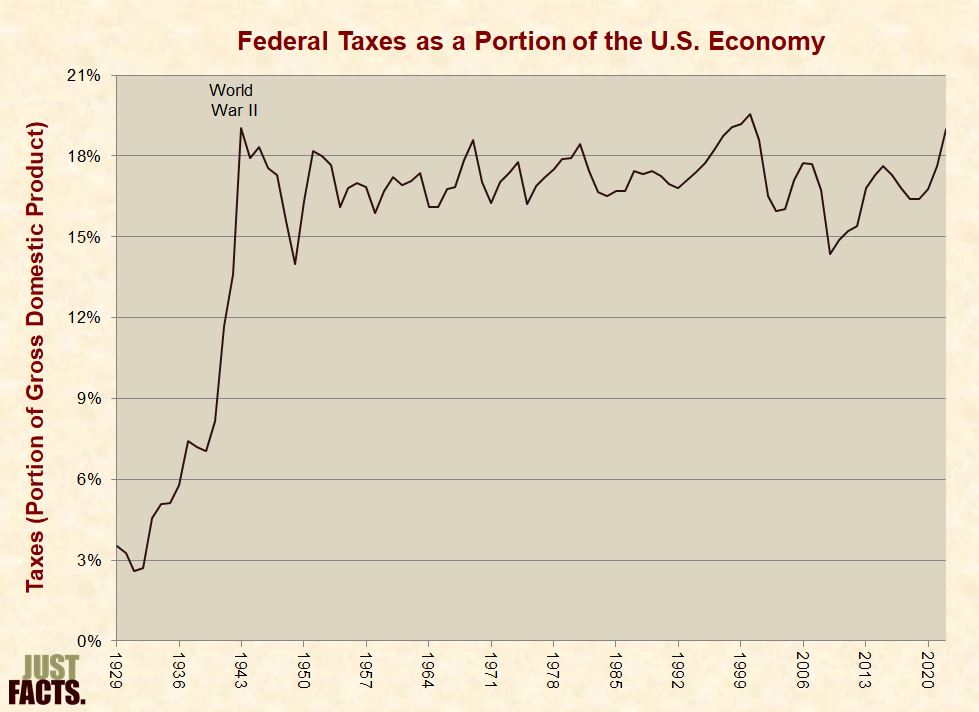

* From 1929 to 2022, the portion of the U.S. economy collected in federal taxes has ranged from 3% to 20%, with a median of 17% and an average of 16%. In 2022, it was 19%, or 22% above the average:

* In 2022, federal taxes came from following sources:

|

Type of Tax |

Portion of Total |

|

Personal Income Taxes |

54% |

|

Social Insurance Taxes |

34% |

|

Corporate Income Taxes |

7% |

|

Excise Taxes |

2% |

|

Custom Duties |

2% |

|

Estate and Gift Taxes |

1% |

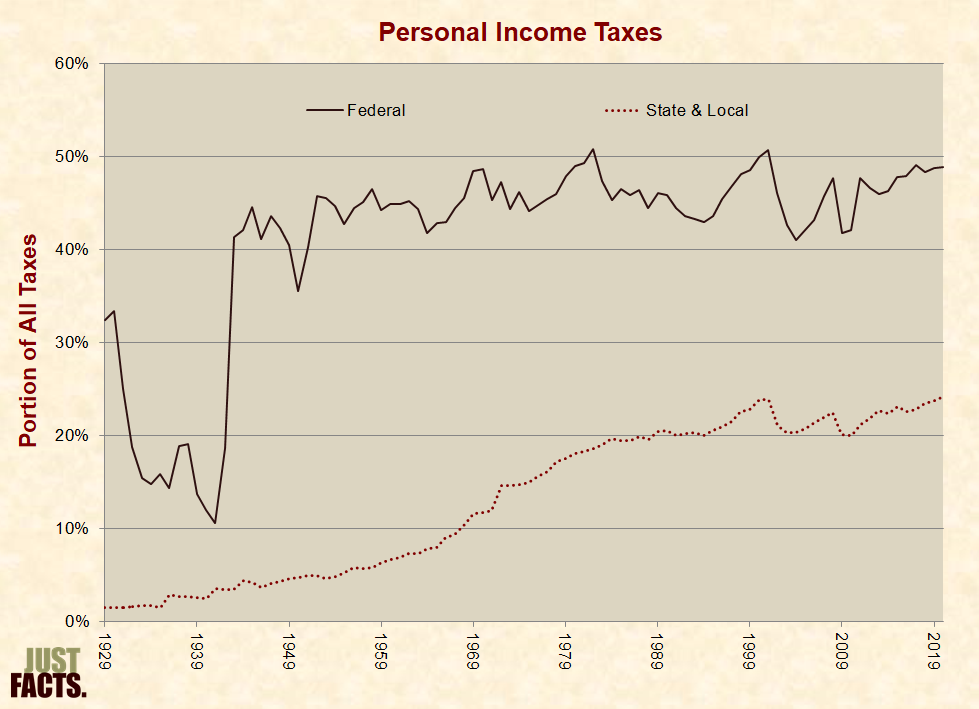

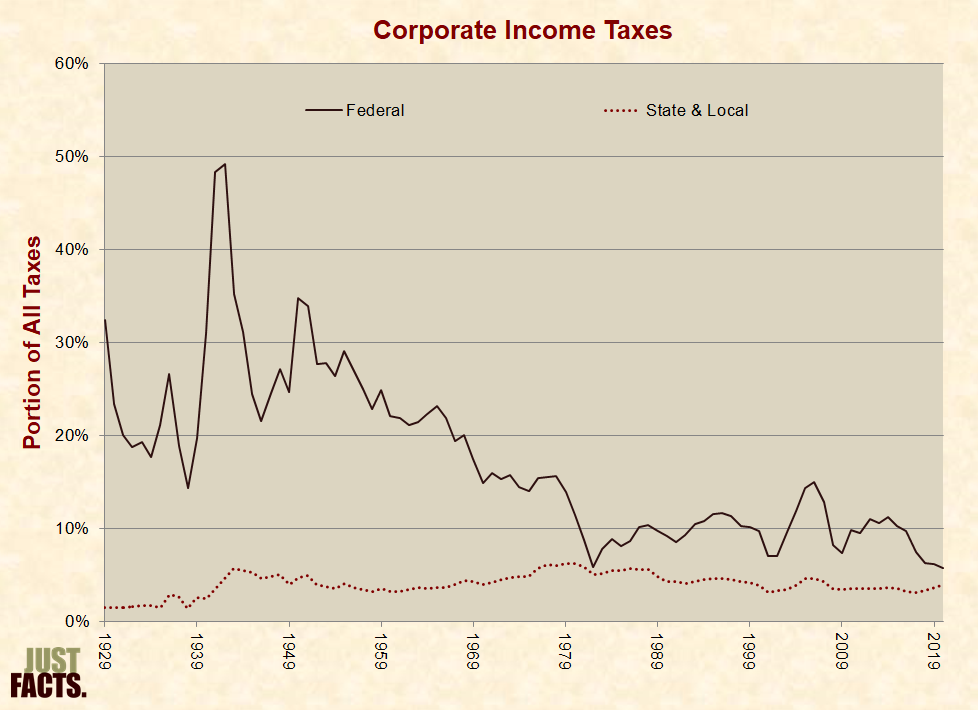

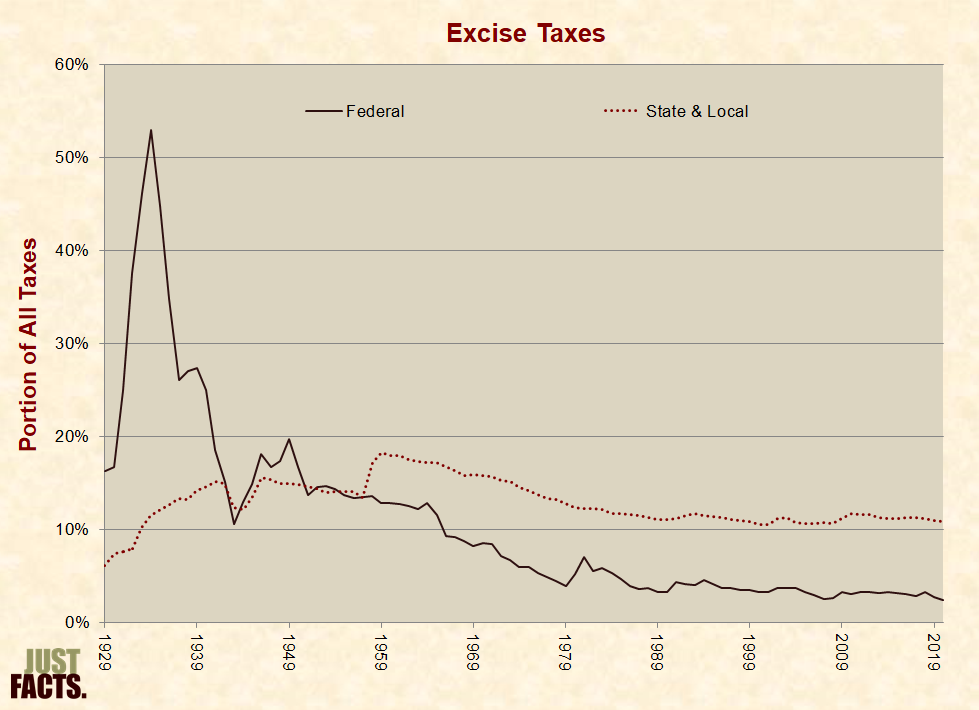

* Since 1929, the components of federal tax collections have varied as follows:

* In 2022, U.S. state and local governments collected a combined total of $2.3 trillion in taxes, or more precisely, $2,188,200,000,000. This amounts to:

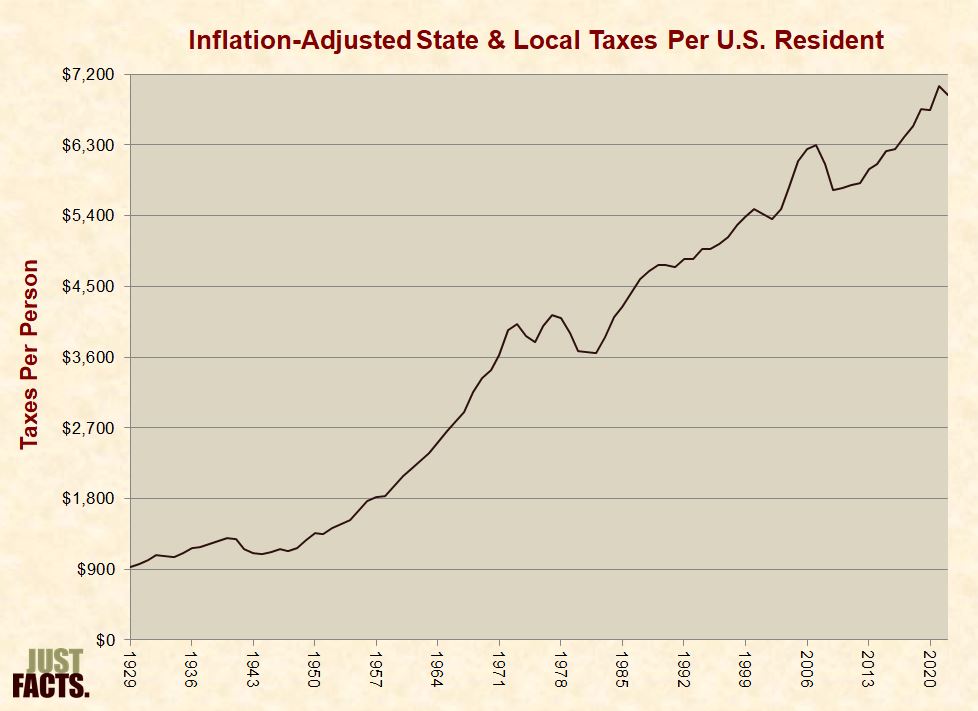

* From 1929 to 2022, inflation-adjusted state and local tax collections per person in the U.S. have ranged from $924 to $7,047 per year, with a median of $3,826 and an average of $3,584. In 2022, they were $6,932, or 93% above the average:

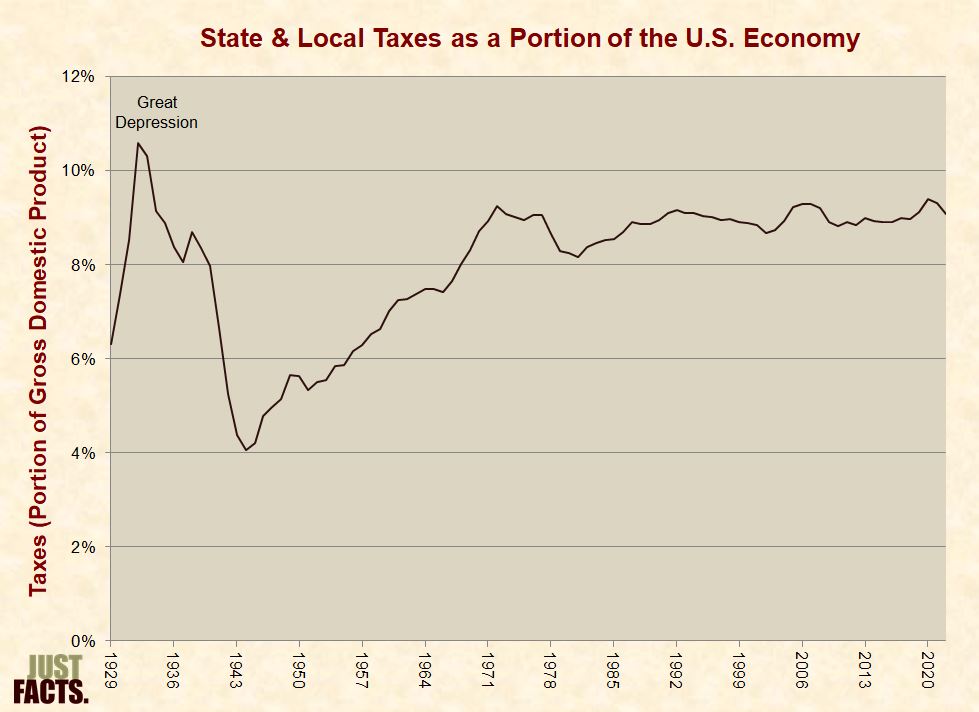

* From 1929 to 2022, the portion of the U.S. economy collected in state and local taxes has ranged from 4% to 11%, with a median of 9% and an average of 8%. In 2022, it was 9%, or 13% above the average:

* In 2022, state and local taxes came from following sources:

|

Type of Tax |

Portion of Total |

|

Sales & Excise Taxes |

33% |

|

Property Taxes |

29% |

|

Personal Income Taxes |

24% |

|

Corporate Income Taxes |

5% |

|

Social Insurance Taxes |

1% |

|

Other |

8% |

* Since 1929, the components of state and local tax collections have varied as follows:

* Tax burdens are shaped by a combination of public laws and market forces. Lawmakers dictate who must remit taxes, but the final burden is determined by how people alter their actions in response to these taxes.[33] [34] [35] Per the textbook Public Finance:

* Per the director of the Congressional Budget Office (CBO):

[T]he ultimate cost of a tax or fee is not necessarily borne by the entity that writes the check to the government.[37]

* To calculate tax burdens, CBO uses the following assumptions/simplifications:

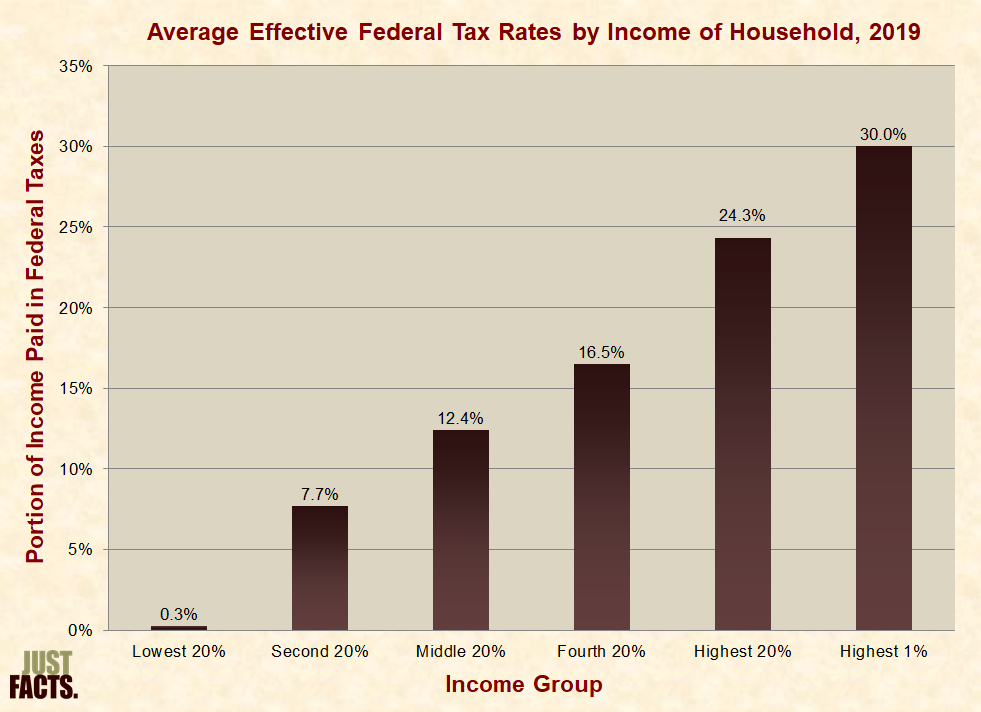

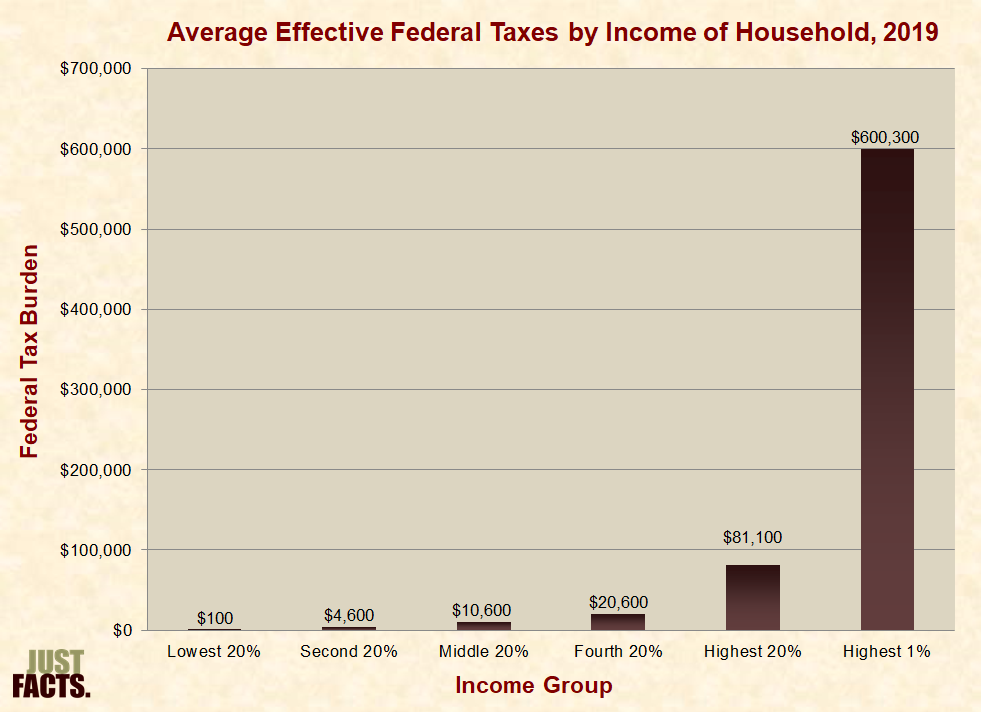

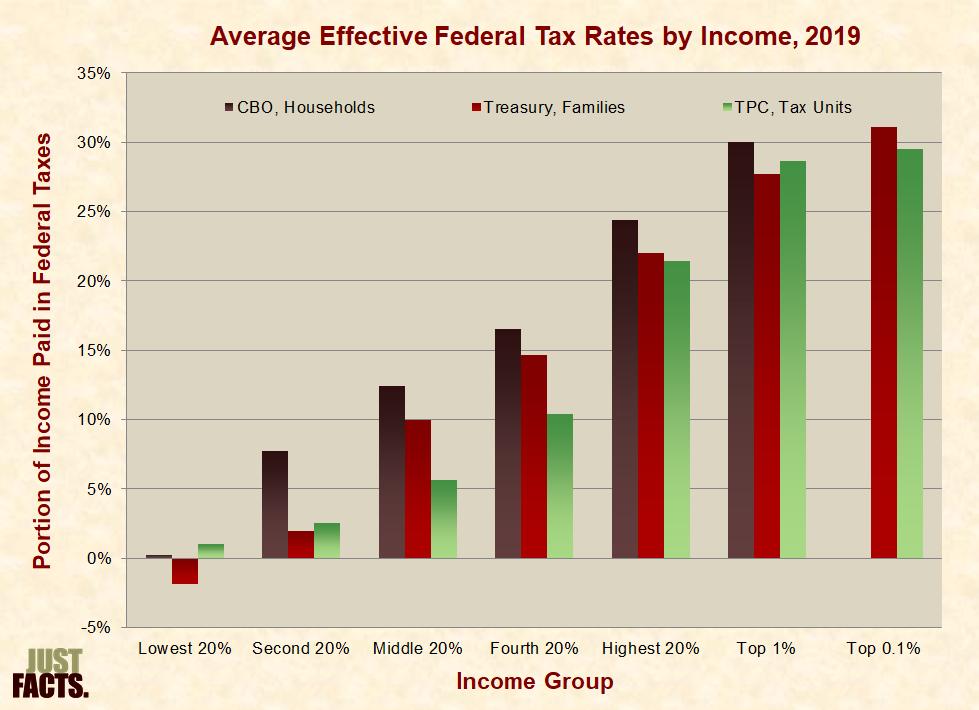

* Per the latest pre-pandemic data from CBO,[52] the effective federal tax burdens for various income groups were as follows in 2019:

* Data from the charts above:

|

Average Effective Federal Tax Rates (2019) |

|||

|

Income Group |

Household Income |

Tax Rate |

Taxes Paid |

|

Lowest 20% |

$39,100 |

0.3% |

$100 |

|

Second 20% |

$59,600 |

7.7% |

$4,600 |

|

Middle 20% |

$85,500 |

12.4% |

$10,600 |

|

Fourth 20% |

$124,900 |

16.5% |

$20,600 |

|

Highest 20% |

$333,100 |

24.3% |

$81,100 |

|

Highest 1% |

$1,998,700 |

30.0% |

$600,300 |

* Per the latest available data from CBO, the effective federal tax burdens for various income groups were as follows in 2020 amid Covid-19 government lockdowns and intensified social spending:[59] [60] [61]

* Data from the charts above:

|

Average Effective Federal Tax Rates (2020) |

|||

|

Income Group |

Household Income |

Tax Rate |

Taxes Paid |

|

Lowest 20% |

$42,200 |

–8.8% |

–$3,700 |

|

Second 20% |

$63,600 |

0.6% |

$400 |

|

Middle 20% |

$90,500 |

7.0% |

$6,300 |

|

Fourth 20% |

$131,800 |

12.7% |

$16,800 |

|

Highest 20% |

$360,900 |

23.6% |

$85,200 |

|

Highest 1% |

$2,291,800 |

29.9% |

$686,300 |

* Per CBO, the effective federal tax rates for various income groups have varied over time as follows:

* CBO does not include state and local taxes in its analysis of effective tax rates “because of the complexity” of estimating them for individual households.[71] Just Facts has not found a reliable analysis of the distribution of state and local taxes.[72]

* Using rough approximations and methods that vary from CBO’s,[73] the U.S. Treasury Department and the Tax Policy Center estimated the following effective federal tax burdens for various income groups in 2019, prior to the Covid-19 pandemic[74]:

* A scientific, nationally representative survey commissioned in 2019 by Just Facts found that 79% of voters believe that middle-income households pay a greater portion of their income in federal taxes than the top 1%.[78] [79]

* Using rough approximations and methods that vary from CBO’s,[80] the U.S. Treasury Department and the Tax Policy Center estimated the following effective federal tax burdens for various income groups in 2023:

* The overall federal tax burden is progressive, which means that overall tax rates generally rise with income,[82] but this is not the case for all types of federal taxes. Excise taxes, for example, fall more heavily on lower-income households.[83] [84] In 2019, prior to the Covid-19 pandemic,[85] effective federal tax rates varied by income and tax type as follows:

|

Average Effective Federal Tax Rates (2019) |

||||||

|

Type of Tax |

Household Income Group |

|||||

|

Lowest |

Second |

Middle |

Fourth |

Top |

Top |

|

|

Individual Income † |

–6.6% |

–1.5% |

2.3% |

5.9% |

15.3% |

23.3% |

|

Social Insurance |

5.6% |

7.9% |

8.7% |

9.1% |

6.5% |

2.3% |

|

Corporate Income |

0.3% |

0.5% |

0.7% |

0.8% |

2.2% |

4.2% |

|

Excise |

1.0% |

0.8% |

0.8% |

0.6% |

0.4% |

0.2% |

|

Overall |

0.3% |

7.7% |

12.4% |

16.5% |

24.3% |

30.0% |

|

† Negative income tax burdens result from refundable tax credits, which often exceed the income tax liabilities of low-income households.[86] In such cases, individuals receive cash payments from the government through the IRS (for more detail, see Tax Preferences).[87] |

||||||

* In a 2005 New York Times article, reporter David Cay Johnston claimed that “the 400 taxpayers with the highest incomes … now pay income, Medicare and Social Security taxes amounting to virtually the same percentage of their incomes as people making $50,000 to $75,000.”[91] That statement fails to account for the burden of corporate income taxes, which fall more heavily on upper-income households.[92]

* In a 2012 Fox News article entitled “Republicans Dispute Obama’s ‘Fair Share’ Claims, Say Top Earners Already Pay Enough,” reporter Jim Angle wrote that “the top 1 percent of earners take home 16.9 percent of the nation’s total income, but pay 36.7 percent of the nation’s income taxes.”[93] That statement fails to account for the burden of social insurance taxes, which fall more heavily on lower-income households.[94]

* In two columns published by the New York Times in 2012, James B. Stewart, a Pulitzer Prize-winning professor of journalism at Columbia University,[95] claimed:

* Both of the claims above fail to account for the burden of corporate income taxes, which fall more heavily on upper-income households.[98]

* Based upon Mitt Romney’s 2010 federal tax return, the following organizations published articles claiming that Romney pays a lower federal tax rate than most Americans: PolitiFact, FactCheck.org, CBS News, and Agence France-Presse.[99] [100] [101] [102] All of these articles fail to account for the burden of corporate income taxes, which fall more heavily on upper-income households.[103] Both PolitiFact and FactCheck.org also:

* Just Facts and two Certified Public Accountants from Ceterus (a nationwide accounting firm) conducted a comprehensive analyses of Romney’s 2010 federal tax return that accounted for all measurable sources of income and federal taxes. It found:

* An Excel spreadsheet detailing the calculations of Romney’s tax burden is available here.

* In August 2011, the New York Times published an op-ed by billionaire investor Warren Buffett, who wrote:

* Buffett’s tax rate comparison fails to account for the burden of corporate income taxes, which fall more heavily on upper-income households.[118]

* Buffett’s tax rate comparison uses “taxable income” as the denominator for his tax burden calculations. Per the book Federal Taxation, using “taxable income” to calculate tax burdens is a “bit misleading” and says “little about the true impact of a tax on the taxpayer.”[119] Per a Congressional Research Service report on the Buffett Rule:

* In September 2011 (the month after the Times published Buffett’s op-ed), the Obama administration released a budget plan calling for tax reform that would:

* In 2011, households in the middle 20% of the U.S. income distribution paid an average effective federal tax rate of 11.7%, as compared to 29.0% for the top 1% of income earners. In 2019, prior to the Covid-19 pandemic,[122] households in the middle 20% paid a tax rate of 12.4%, as compared to 30.0% for the top 1%.[123] [124] [125]

* CBO’s latest data shows that in 2020—amid Covid-19 government lockdowns and intensified social spending,[126] [127] [128] households in the middle 20% paid a tax rate of 7.0%, as compared to 29.9% for the top 1%.[129] [130] [131]

* In 2011, 15,000 individuals with incomes over $200,000 paid no federal individual income taxes (this does not include corporate income taxes). In 58% of these cases, the primary reason was because they had earned interest from tax-exempt bonds issued by state and local governments.[132] These bonds are called “municipal bonds” or “munis,” and they are a principal means by which wealthy investors limit their federal income taxes.[133] [134]

* Per CBO:

* Per the IRS:

* “General revenues” are taxes that are collected to fund the general operations of government. These taxes are not legally restricted to funding a specific program.[138] [139] [140]

* The national debt and interest on it are paid with general revenues.[141]

* Overall, general revenue taxes are progressive so that higher-income households pay higher effective tax rates. In 2019, prior to the Covid-19 pandemic,[142] the average federal general revenue taxes paid by various income groups varied as follows:

|

Average Federal General Revenue Taxes (2019) |

|||

|

Income Group |

Household Income |

Effective Tax Rate † |

Taxes Per Household |

|

Lowest 20% |

$39,100 |

–6.0% |

–$2,359 |

|

Second 20% |

$59,600 |

–0.7% |

–$424 |

|

Middle 20% |

$85,500 |

3.9% |

$3,300 |

|

Fourth 20% |

$124,900 |

7.0% |

$8,682 |

|

Highest 20% |

$333,100 |

17.6% |

$58,658 |

|

81st–90th% |

$181,300 |

10.2% |

$18,552 |

|

91st–95th% |

$250,400 |

13.0% |

$32,523 |

|

96th–99th% |

$417,400 |

17.6% |

$73,428 |

|

Top 1% |

$1,998,700 |

27.6% |

$551,879 |

|

† Negative tax burdens result from refundable tax credits, which often exceed the general revenue taxes of low-income households.[143] In such cases, individuals receive cash payments from the government through the IRS (for more detail, see Tax Preferences).[144] |

|||

* In 2020—amid Covid-19 government lockdowns and intensified social spending,[148] [149] [150] the average federal general revenue taxes paid by various income groups varied as follows:

|

Average Federal General Revenue Taxes (2020) |

|||

|

Income Group |

Household Income |

Effective Tax Rate † |

Taxes Per Household |

|

Lowest 20% |

$42,200 |

–13.7% |

–$5,798 |

|

Second 20% |

$63,600 |

–6.7% |

–$4,230 |

|

Middle 20% |

$90,500 |

–1.4% |

–$1,295 |

|

Fourth 20% |

$131,800 |

3.6% |

$4,739 |

|

Highest 20% |

$360,900 |

17.1% |

$61,609 |

|

81st–90th% |

$191,500 |

8.2% |

$15,707 |

|

91st–95th% |

$265,100 |

12.0% |

$31,775 |

|

96th–99th% |

$440,000 |

17.3% |

$76,077 |

|

Top 1% |

$2,291,800 |

27.6% |

$633,629 |

|

† Negative tax burdens result from refundable tax credits, which often exceed the general revenue taxes of low-income households.[151] In such cases, individuals receive cash payments from the government through the IRS (for more detail, see Tax Preferences).[152] |

|||

* The general revenues of the U.S. Treasury are comprised of:

* In 2020, income taxes paid by individuals (as opposed to corporations) comprised 49% of the taxes collected by the federal government and 24% of the taxes collected by state and local governments:

* Federal individual income taxes are typically allocated to the general fund of the U.S. Treasury, which means that these taxes are not earmarked for specific programs and can be used for any legitimate purpose of government.[159] [160]

* Federal individual income tax liabilities are calculated in the following manner:

* Federal individual income taxes also include taxes on capital gains and dividends,[177] which are addressed below.

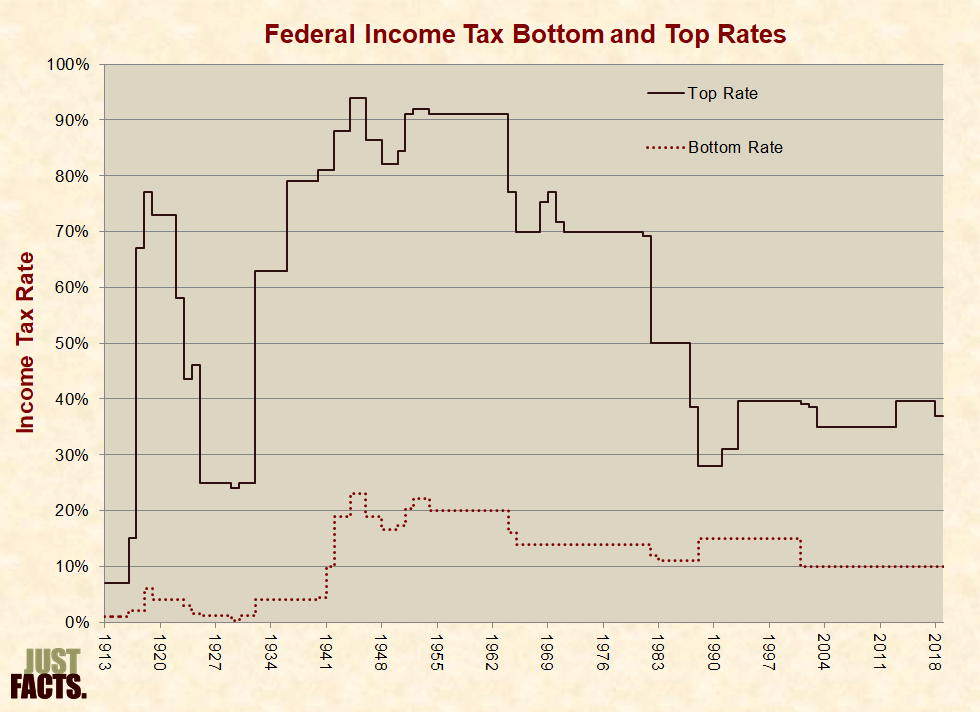

* When the modern federal individual income tax was instituted in 1913,[178] the bottom tax rate was 1%, and the top rate was 7%. Since then, the bottom rate has been as high as 23% (in 1944–1945), and the top rate has been as high as 94% (in 1944–1945).[179] [180] In 2020, the bottom rate was 10%, and the top rate was 37%.[181]

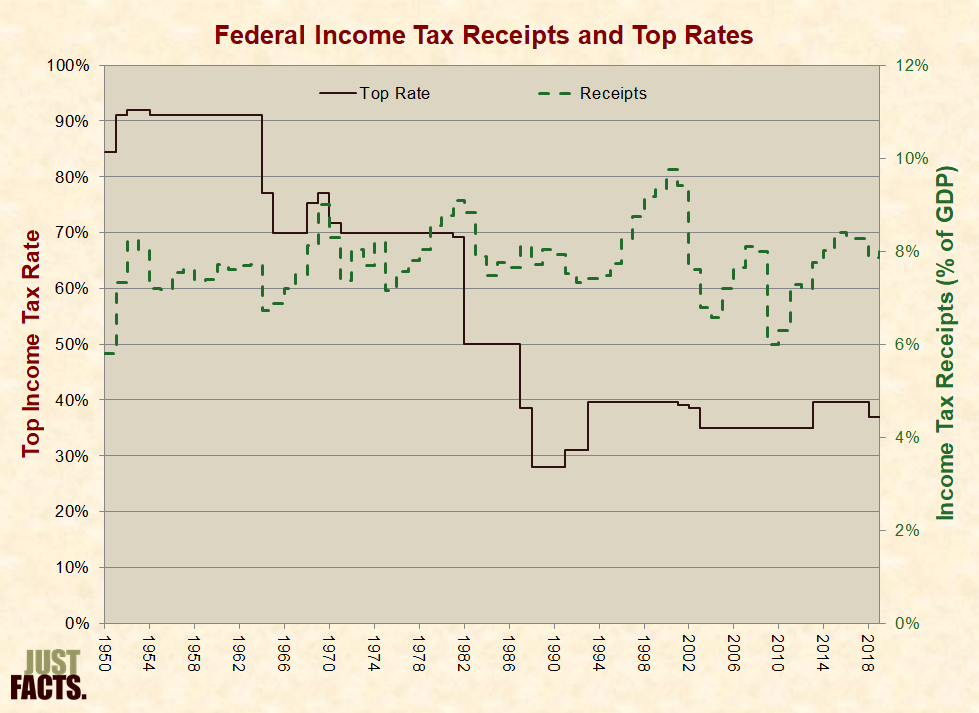

* From 1950 to 2019, the top federal individual income tax rate varied from 92% (in 1952–1953) to 28% (in 1988–1990), and income tax receipts (as a portion of gross domestic product) varied from 5.8% (in 1950) to 9.8% (in 2000). Over this period, these lower and higher income tax rates often do not correspond with lower and higher income tax collections:

* As of January 1, 2021, the 50 U.S. states have individual income tax rates that vary from a top rate of 13.3% in California to 0% in seven states that don’t have such a tax (Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming).[184]

* In 2019, 4,964 counties, cities, townships, and school districts in 17 states levied individual income taxes.[185]

* In 2018, the portion of state and local tax collections that were comprised of individual income taxes varied from a high of 43% in Oregon, to a median of 24% in South Carolina to a low of 0% in Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming.[186]

* Current government “social insurance” programs in the U.S. include Social Security, Medicare hospital insurance, unemployment insurance, and several smaller healthcare and income security programs. “Social insurance taxes,” which are also known as “payroll taxes” or “employment taxes,” are taxes that are levied specifically for these programs.[187] [188] [189] [190]

* In 2020, social insurance taxes comprised 41% of the taxes collected by the federal government and 1% of the taxes collected by state and local governments:

* Employees and employers both pay social insurance taxes, but payroll taxes levied on employers are predominately borne by employees in the form of reduced wages.”[192] [193] [194] [195] [196] (For more detail, see Distribution of the Tax Burden).

* Federal taxpayers in all income groups except for the top 20% pay more in social insurance taxes than individual income taxes.[197]

* In 2020, 99% of federal social insurance taxes were levied for three programs: Social Security, Medicare hospital insurance, and unemployment insurance.[198] [199]

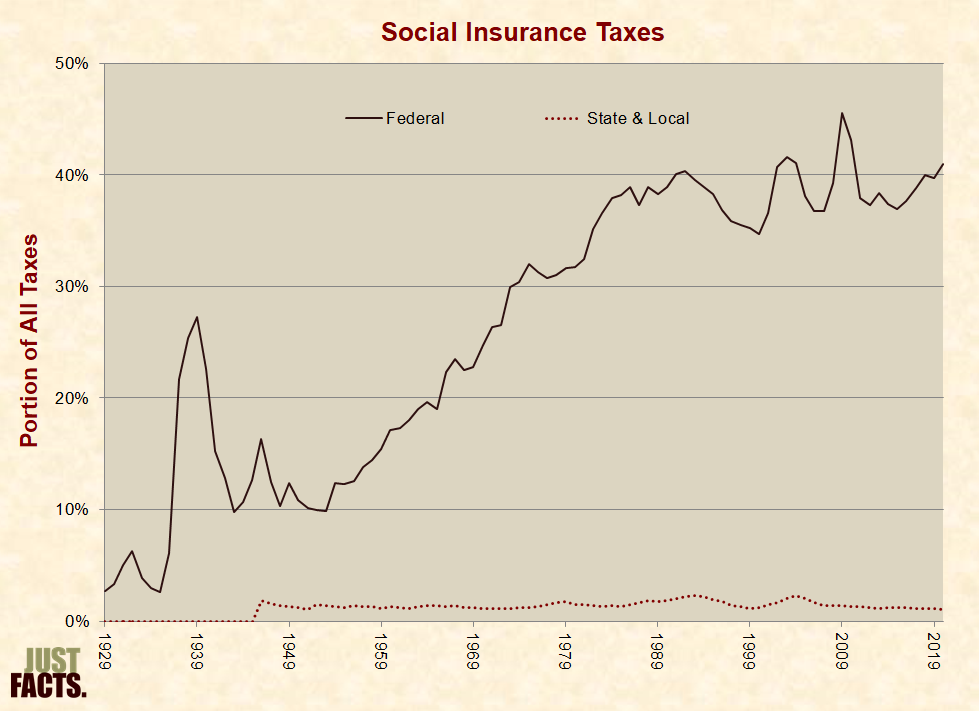

* Government began collecting social insurance taxes for unemployment insurance in 1936, Social Security in 1937, and Medicare hospital insurance in 1966. Combined payroll taxes for these programs have ranged from 0.2% of the nation’s gross domestic product (GDP) in 1936 to 6.5% in 1991 and 1998–2001:

* In 2019, Social Security payroll taxes accounted for 74% of federal social insurance taxes.[201]

* For 2021, Social Security’s baseline payroll tax rate (employee and employer combined) is 12.4%.[202]

* Social Security payroll taxes are restricted to a “taxable maximum” or “wage threshold.” Earnings above the threshold are not subject to this tax. For 2021, the threshold is $142,800.[203] Since 1982, the taxable maximum has been annually indexed roughly based upon average worker compensation levels.[204] [205]

* At the outset of the Social Security program, the federal government published an informational pamphlet that stated the following about the program’s taxes:

* Accounting for inflation, the figures above equate to a maximum tax collection of $1,935 per person in 2020 dollars.[207] In 2020, the maximum payroll tax collection per person was $17,075 or 8.8 times the promised maximum.[208] This figure does not include other taxes that are now levied to fund Social Security, such as the tax on Social Security benefits.

* For comprehensive facts about Social Security’s taxes, benefits, and financial status, visit Just Facts’ research on Social Security.

* Medicare hospital insurance, which is also known as Medicare “Part A,” provides coverage for hospital inpatient services, skilled nursing facility care (not custodial care[209]), and hospice care.[210]

* In 2019, Medicare hospital insurance payroll taxes accounted for 22% of federal social insurance taxes.[211]

* Medicare’s baseline payroll tax rate is 2.9% of workers’ wages (employer and employee combined).[212] [213]

* Medicare’s payroll tax was previously limited by a wage threshold that generally increased as the national average wage increased. Earnings above this threshold were not subject to the tax. In 1993, this threshold was $135,000 per year.[214] That year, Congress and Democratic President Bill Clinton passed a law that removed the threshold, thus making all earnings subject to Medicare payroll taxes.[215] The bill passed with 85% of Democrats voting for it and 100% of Republicans voting against it.[216]

* The Affordable Care Act (a.k.a. Obamacare) levies an additional 0.9% Medicare payroll tax on earnings above $200,000 for singles and $250,000 for couples.[217] [218]

* For comprehensive facts about Medicare’s taxes, benefits, and financial status, visit Just Facts’ research on Medicare.

* In 2019, unemployment insurance payroll taxes accounted for 3% of federal social insurance taxes.[219] [220]

* Corporate income taxes are typically levied on “C corporations,” which are business entities that are fully separated by law from their owners’ personal finances. Most major and public corporations are structured in this manner.[221] [222]

* Per the IRS and the Congressional Research Service, U.S. tax law imposes a “double tax” on corporate profits. This is because the “profit of a corporation is taxed to the corporation when earned,” but shareholders cannot receive these profits without also paying dividend or capital gain taxes on them.[223] [224] [225] (For more detail, see Capital Gains, Dividends, and Interest).

* Business entities can be structured in other ways, such as “S corporations,” partnerships, and sole proprietorships. In these cases, tax law combines business incomes with owners’ personal incomes. These types of businesses are called “passthrough entities.” They are subject to personal income taxes instead of corporate income taxes and dividend taxes.[226] [227] [228]

* The combination of taxes on corporate income and dividends is typically higher than personal income taxes. Thus, people who have the option to structure business as pass-through entities often do so. The law does not allow businesses with more than 100 shareholders—like most major public corporations—to be structured as pass-through entities.[229] [230] [231] [232]

* In 2020, corporate income taxes comprised 6% of the taxes collected by the federal government and 4% of the taxes collected by state and local governments:

* The burden of corporate income taxes falls on:

* The Congressional Budget Office (CBO) estimates that 75% of corporate income taxes are borne by owners/stockholders and 25% are borne by workers.[236] [237] [238] Other creditable sources estimate that owners/stockholders bear anywhere from 33% to 100% of this tax burden.[239] (For more detail, see Distribution of Tax Burdens.)

* In basic terms, federal corporate income taxes are levied on profits, which are calculated by adding income from business operations and the sale of company stock minus:

* Higher marginal tax rates—which are the rates that taxpayers pay on the next dollar of income they earn—typically weaken incentives to save and invest.[244] [245] [246] [247] For more detail, see Economic Effects.)

* Starting in 2018, the Trump Tax Cuts reduced the top marginal federal corporate income tax to a flat rate of 21%.[248] [249] [250]

* In 2017 (latest IRS data), the marginal federal corporate income tax rate for active corporations averaged 36% before tax credits. After tax credits were applied, the average effective rate was 26%.[251] [252] (For more detail, see Tax Preferences).

* Out of 20 major business sectors, the effective federal corporate income tax rates in 2017 averaged as low as 15% for mining and 19% for utilities to as high as 32% for educational services and retail trade and 33% for healthcare and social assistance.[253] [254]

* In 2018, the portion of state and local tax collections that were comprised of corporate income taxes varied from a high of 11% in New Hampshire to a median of 3% in Iowa to a low of 0% in Nevada, Texas, Washington and Wyoming.[255]

* A “capital gain” is an increase in the price of a financial asset between when it is purchased and when it is sold.[256] [257] Financial assets that are subject to capital gain taxes include items such as company stocks, real estate, collectibles, and precious metals.[258]

* A “dividend” is a company profit that is distributed to shareholders.[259] [260]

* “Interest income” is money earned from “certain bank accounts or from lending money to someone else.”[261]

* Per the Encyclopedia of Taxation and Tax Policy (as confirmed by the IRS, Congressional Research Service, and U.S. Joint Committee on Taxation):

* Taxes on dividends and capital gains are classified by the federal government as individual income taxes, but the tax rates are generally lower, which mitigates some of the double taxation. The lower tax rates on capital gains only apply to assets that are owned for a year or longer. Assets that are owned for less than a year are considered “short-term capital gains” and are taxed at ordinary income tax rates.[268] [269] [270] [271]

* In 2020, the tax rates on most dividends and capital gains ranged from 0% to 20%. For couples filing jointly, the typical rates are:

* Interest income, such as that from bank accounts and personal loans, is not considered a capital gain or a dividend, and it is generally subject to regular income tax rates.[274] [275]

* Starting in 2013, the Affordable Care Act (a.k.a. Obamacare) began subjecting income earned from interest, dividends, and capital gains to an additional 3.8% tax for singles with incomes above $200,000 and couples with incomes above $250,000. This tax is called the “net investment income tax.”[276] [277] [278]

* Taxes on interest income, dividends, and capital gains are not offset for inflation, and investors must pay taxes on gains that are due to inflation (a.k.a. “phantom gains”).[279] [280] For example, if a $1,000 investment yields a 4% return over the course of a year while inflation is at 3% and the tax rate is at 25%, the effective tax rate is 100%:

* With capital gains (but not dividends or interest income), some effects of inflation are alleviated because taxes on capital gains don’t need to be paid until an asset is sold. This allows an asset to grow in value without losing some gains to taxes each year.[283] [284] [285]

* In 2019, 11.2% of federal individual income tax receipts came from capital gain taxes.[286]

* For 2020, the Congressional Budget Office estimated that 6.5% of gross income earned by individuals will come from capital gains, and 3.5% from dividends or interest income.[287]

* In 2020, state taxes on capital gains ranged from as low as 0%—in Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington and Wyoming—to as high as 13% in California and 11% in Hawaii and New Jersey.[288] [289]

* “Tax preferences,” which are also called “tax expenditures,” are defined by federal law as “revenue losses attributable to provisions of the federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability.”[290] [291]

* Tax preferences fall into five broad categories:

* Per Donald B. Marron, director of the Tax Policy Center and former acting director of the Congressional Budget Office:

* Examples of unambiguous tax preferences/expenditures include:

* Per the U.S. Joint Committee on Taxation, tax preferences/expenditures are commonly:

* Many tax preferences have the same purpose and effects as government spending. For example, if the government were to repeal the child tax credit and instead send checks to certain households with children, the result would be the same.[308] [309] [310] [311] [312]

* With regard to tax preferences:

* Per the federal government’s Energy Information Administration:

* The primary beneficiaries of tax preferences are sometimes not the individuals who claim them. For example, the exemption for interest earned on state and local government bonds mainly benefits the governments that issue the bonds instead of the investors who buy them. This is because governments can sell tax-exempt bonds with lower interest rates than comparable taxable bonds, and investors will still buy these bonds as long as their after-tax profits are equivalent or greater. Hence, the tax exemption allows governments to issue bonds at lower interest rates, which lowers their costs of financing.[318] [319] Per the Internal Revenue Service:

* During the U.S. Constitutional Convention, James Madison, who would later become known as the Father of the Constitution for his central role in its formation, stated that all civilized societies are “divided into different sects, factions, and interests,” and “where a majority are united by a common interest or passion, the rights of the minority are in danger.” He then listed some “unjust laws” that were due to majorities taking advantage of minorities, such as those that sanctioned slavery and those that imposed “a disproportion of taxes” on certain types of properties.[321] [322] [323]

* Out of 20 major business sectors, the effective federal corporate income tax rates in 2017 averaged as low as 15% for mining and 19% for utilities to as high as 32% for educational services and retail trade and 33% for healthcare and social assistance.[324]

* Some tax credits are refundable, and low-income households with tax credits that exceed their income tax liabilities receive the difference as cash payments from the federal government.[325] [326] [327] [328]

* The first major refundable tax credit was implemented by the federal government in 1976. Since then, six others have been enacted, and a total of five such programs are still in effect.[329] [330]

* In 2014, the Affordable Care Act (a.k.a. Obamacare) began providing refundable tax credits for people who purchase health insurance through the program. Under this law:

* Due to refundable tax credits, the lowest-income 20% of U.S. households paid an average effective federal income tax rate of –6.6% in 2019 prior to the Covid-19 pandemic.[334] This amounted to an average payment from the federal government of $2,600 per household.[335] [336] [337] [338]

* Due to refundable tax credits, the lowest-income 20% of U.S. households paid an average effective federal income tax rate of –14.2% in 2020—amid Covid-19 government lockdowns and intensified social spending.[339] [340] [341] This amounted to an average payment from the federal government of $6,000 per household.[342] [343] [344] [345]

* In 1986, the 99th Congress passed and Republican President Ronald Reagan signed a tax reform law that eliminated many tax preferences while reducing the top personal income tax bracket from 50% to 28% and reducing the top corporate income tax bracket from 46% to 34%.[346]

* In the year after the 1986 reform, the average effective federal tax rate for the top 20% of income earners increased by 2.1 percentage points, while the rates for all other income groups dropped by less than one percentage point. In the next five years, the tax rate for the top 20% stayed higher than before the law was enacted, while the rates for all other income groups stayed about the same or lower:

* The 1986 reform kept in place some of the more widely used tax preferences, such as the deduction for home-mortgage interest.[350]

* In the 25 years after the 1986 reform was passed, various congresses and presidents enacted at least 150 provisions into law that the Joint Committee on Taxation classifies as tax preferences. Examples of such include:

* The alternative minimum tax (AMT) is a form of federal income tax that is imposed on top of the standard income tax. The AMT disallows certain tax preferences and thereby increases the income taxes that some individuals must pay.[352] [353] [354] [355]

* Per the Congressional Budget Office (CBO):

* The AMT has a greater impact on taxpayers with large families, high medical bills, and high state and local taxes.[358]

* Between 2001 and 2011, various Congresses and presidents partially alleviated the inflationary impact of the AMT by enacting temporary changes in the law.[359] [360]

* In 2012, President Obama and Congress passed permanent legislation to adjust the AMT for inflation on an annual basis. This reduced but did not eliminate the impact of bracket creep.[361] [362]

* In 2017, President Trump and Congress passed legislation that temporarily decreases the portion of taxpayers subject to the AMT until 2025. This law:

* From 1983 to 1998, the portion of taxpayers liable for the AMT stayed below 1%. By 2017, 4.9% of taxpayers were required to pay the AMT. In 2018 the portion dropped to 0.2%:

* The origins of the AMT can be traced to a January 1969 speech given by Treasury Secretary Joseph Barr, in which he stated that “there is going to be a taxpayer revolt over the income taxes in this country unless we move in this area.” Barr criticized the use of “loopholes and gimmicks” by the wealthy and pointed out that “in the year 1967, there were 155 tax returns in this country with incomes of over $200,000 a year and 21 returns with incomes over a million dollars for the year on which the ‘taxpayers’ paid the U.S. Government not 1 cent of income taxes….”[367] [368]

* Barr’s speech spurred a public uproar, and in August of 1969, Life magazine published a house editorial noting that Congress was considering a “minimum tax” to address “the scandal under which 155 individuals with incomes over $200,000 were in 1967 able to pay no income tax at all.”[369] [370]

* In December of 1969, Congress passed and the president signed the first minimum tax law. The legislative report echoed Barr’s speech and stated, “It should not have been possible for 154 individuals with adjusted gross incomes of $200,000 or more to pay no Federal income tax on 1966 income.”[371] [372]

* Over the ensuing three decades, various U.S. Congresses and presidents made at least 18 changes to this tax.[373] The legislative report for the changes passed in 1982 echoed Barr’s speech again, stating that the changes have “one overriding objective: no taxpayer with substantial economic income should be able to avoid all tax liability by using exclusions, deductions, and credits.”[374]

* The 155 tax returns cited by Barr amounted to 0.0002% of taxable returns in 1967.[375] Adjusted for inflation, $200,000 in 1967 is equivalent to $1.5 million in 2018.[376] In 2018, the AMT levied additional taxes on 0.2% of taxable returns,[377] including:

* In 2017, 10,988 individuals with incomes over $200,000 paid no federal individual income taxes (this does not include corporate income taxes). In 42% of these cases, their primary tax preference was interest earned from tax-exempt bonds issued by state and local governments.[379] These bonds are called “municipal bonds” or “munis,” and they are a principal means by which wealthy individuals limit their federal income taxes.[380] [381]

* When Congress was considering the first minimum tax in 1969, the editors of Life wrote that the proposed law has “some dubious side effects” because “among the tax shelters this reform goes after is the interest on tax-exempt bonds, on the sale of which our hard-pressed state and local governments depend for financing their public works.”[382]

* Currently, under federal tax law, the definition of “gross income” excludes interest from tax-exempt munis, and hence, income from these bonds is not subject to the alternative minimum tax.[383] [384] [385]

* Per the CBO:

* Per the IRS:

* Per the Congressional Budget Office (CBO), “Most parameters of the tax code are not indexed for real income growth, and some are not indexed for inflation.” Thus, if tax laws remain unchanged, “average federal tax rates would increase in the long run.” This is referred to as “bracket creep.”[389]

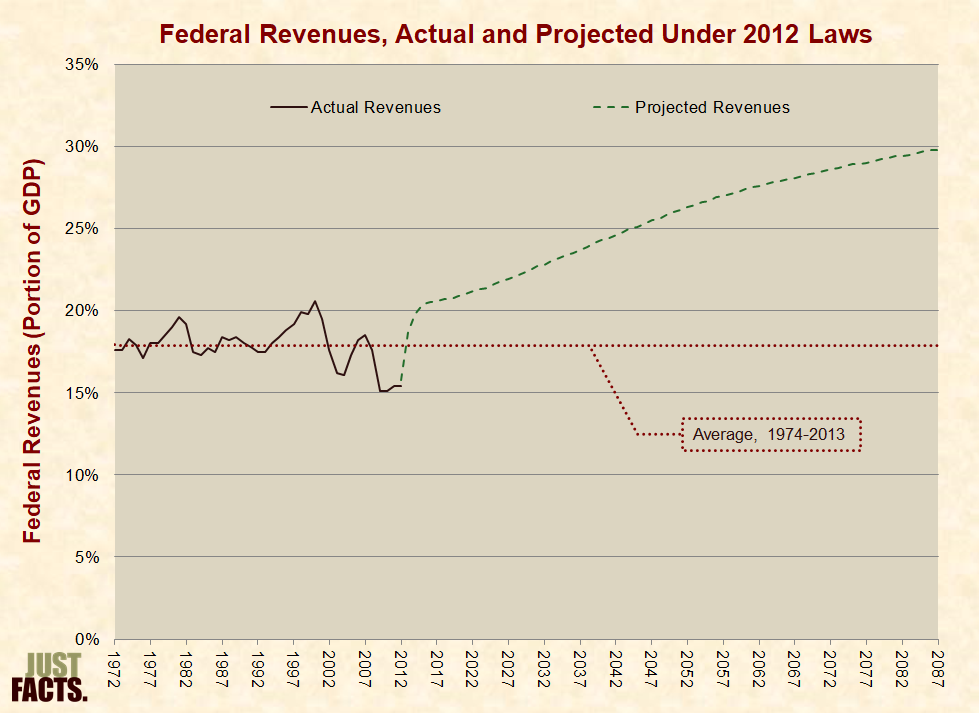

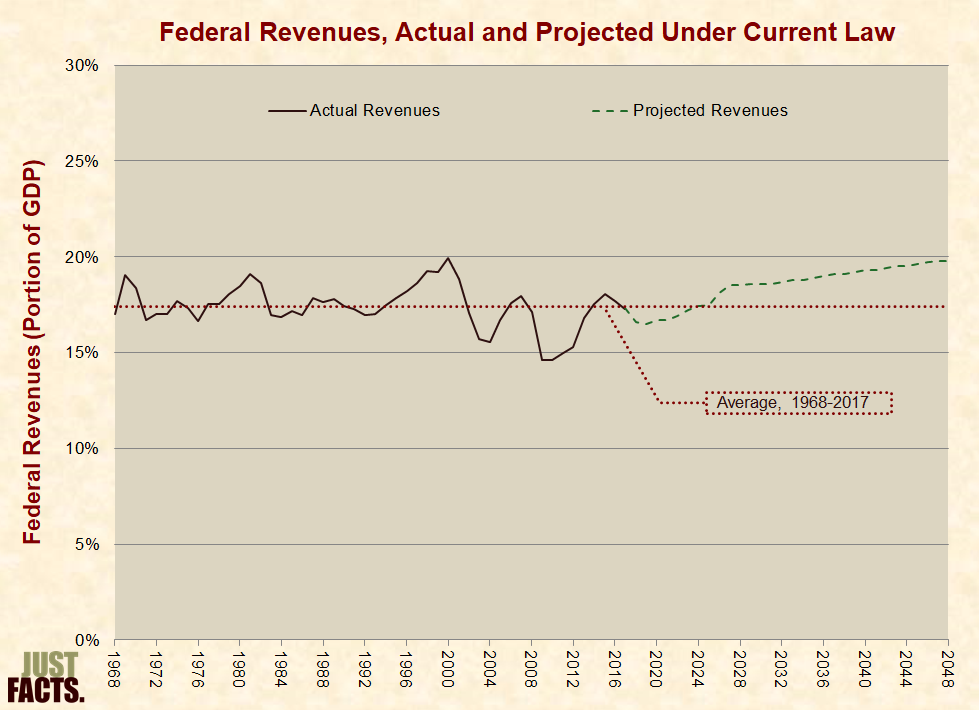

* In 2012, before Congress and President Obama passed a law to index the alternative minimum tax for inflation and make most of the Bush tax cuts permanent for everyone but high-income earners,[390] [391] CBO projected that if tax laws remained unchanged, federal revenues would grow to 46% above the average of the previous 40 years by 2051:

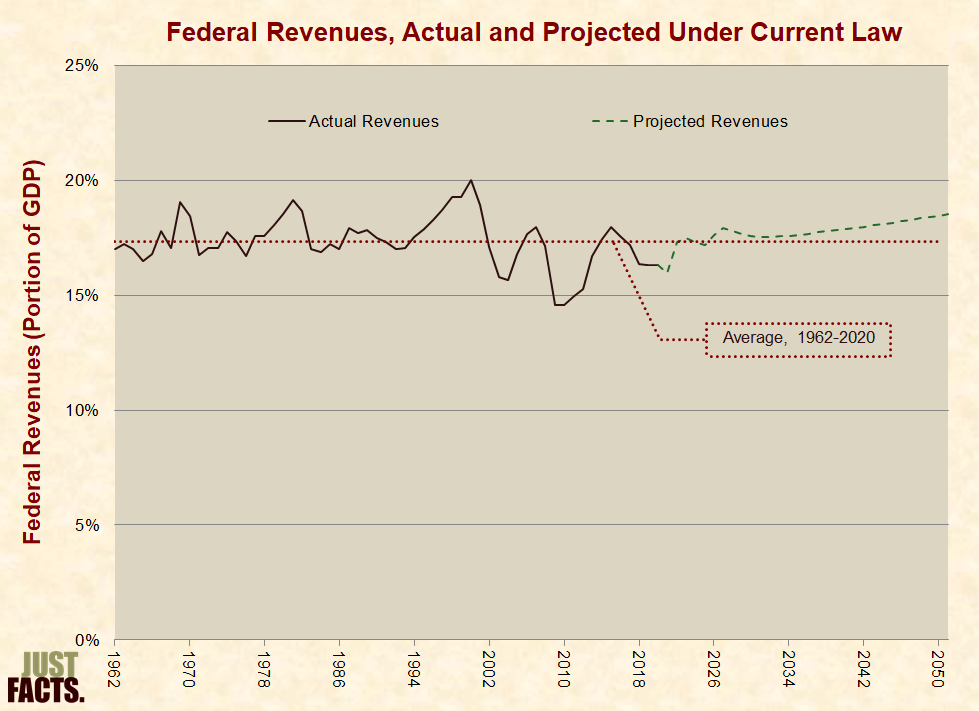

* From 1962 to 2020, federal revenues averaged 17.3% of the nation’s gross domestic product (GDP). In 2021, CBO projected that if current tax laws remain unchanged, federal revenues will grow to 7% above this long-term average by 2051, mainly due to bracket creep:

* With regard to middle-income families, CBO projected:

* Examples of tax laws that are not indexed for inflation or wage growth include:

* Examples of tax laws that are indexed for inflation (but not for wage growth) include:

* In a 2011 budget analysis published by the Washington Post, Ezra Klein posted a chart of federal spending and revenue projections based on the Congressional Budget Office’s “current law” scenario and wrote that it:

* Klein called this is a “pretty good plan” without revealing that under it:

* In a 2012 commentary published by Rolling Stone, Jared Bernstein—a former economic advisor to President Obama and a senior fellow with the Center on Budget and Policy Priorities—wrote that “it is well within our means” to reduce the national debt by following the “broad outlines” of “current law.” He then pushed for this without revealing that under the law at that time, federal taxes would progressively consume a greater share of the U.S. economy, rising to:

* Per the Congressional Budget Office:

* The federal tax code is about 6,000 pages when printed on 8.5×11 inch paper in size 11 font. This includes supplementary materials that do not have the force of law (such as indexes and records of some repealed provisions), but these materials are often needed to understand the law.[432] [433] [434]

* Per the IRS, “Federal tax regulations … pick up where the Internal Revenue Code (IRC) leaves off by providing the official interpretation of the IRC by the U.S. Department of the Treasury.”[435] When printed on 8.5×11 inch paper in size 8 font, current federal tax regulations are about 15,000 pages. This does not include obsolete provisions or indexes.[436] [437]

* U.S. taxpayers (including businesses) spend roughly six billion hours per year complying with the requirements of federal tax law. This amounts to 48 hours per household, or the labor equivalent of more than three million full-time workers. Per the IRS’s Taxpayer Advocate, these figures do not include “millions of additional hours that taxpayers must spend when they are required to respond to IRS notices or audits.”[438] [439]

* The IRS’s Taxpayer Advocate estimates that the cost of complying with federal income tax laws was $195 billion in 2015, or 10% of income tax receipts.[440]

* In 2006, General Electric filed the nation’s longest federal tax return, which was about 24,000 pages long.[441] In 2011, its federal tax return was about 57,000 pages long.[442]

* In 2019, the IRS spent $11.8 billion and employed 78,004 people, including seasonal and part-time workers.[443]

* Per the IRS’s Taxpayer Advocate:

* A 2019 IRS study found that from 2011 to 2013, the difference between what was legally due in federal taxes and what was actually paid amounted to an average annual “tax gap” of $381 billion. This equates to a noncompliance rate of 14.2%.[445] [446]

* Per the IRS’s Taxpayer Advocate, the tax gap represents an effective tax on most taxpayers “to subsidize noncompliance by others.”[447] Adjusted for inflation into 2020 dollars, the 2013 tax gap was an average of $3,519 for every household in the U.S.[448]

* Per the IRS’s Taxpayer Advocate:

* In instances where income was reported to the IRS and withheld by third parties (such as employers), the noncompliance rate was about 1% from 2011 to 2013. In instances where income was not subject to reporting or withholding, the noncompliance rate was 55%.[450] [451]

* Willfully evading federal taxes is a felony crime punishable by up to five years in prison and fines of up to $250,000 for individuals and $500,000 for corporations.[452] [453] [454]

* Some tax credits are refundable, and low-income households with tax credits that exceed their income tax liabilities receive the difference as cash payments from the federal government.[455] [456] [457] Per the Treasury Department’s Inspector General for Tax Administration, “the risk of fraud for these types of claims is significant.”[458] [459]

* Two of the costliest and most frequently claimed refundable tax credits are the earned income tax credit and the child tax credit.[460] [461] [462]

* In 2019, the IRS improperly paid $17.4 billion in earned income tax credits, amounting to an improper payment rate of 25%.[463] [464] These improper payments were greater than the budget of the IRS.[465]

* In 2019, the IRS improperly paid about $7.2 billion in refundable child tax credits, amounting to an improper payment rate of 15%.[466]

* In 2020, the maximum refundable child tax credit is $1,400 per child.[467]

* Federal law generally prohibits illegal immigrants from earning income in the U.S., but the law also requires them to file tax returns if they do earn income. Federal law also prohibits illegal immigrants from receiving most federal benefits, but the IRS has concluded that this restriction does not apply to refundable child tax credits. In 2010, the IRS paid out $4.2 billion in refundable child tax credits to 2.3 million tax filers who were not legally authorized to work in the United States.[468] [469]

* In 2010, 72% of the tax returns filed by illegal immigrants and foreign investors received cash payments from the IRS for child tax credits. Among the U.S. citizens and foreigners legally working the U.S., 14% of tax filers received cash payments from the IRS for child tax credits.[470]

* In April 2012, WTHR, an NBC News affiliate in Indiana, aired a report by investigative journalist Bob Segall about illegal immigrants who were fraudulently obtaining child tax credits by claiming credit for children who live in Mexico. The IRS responded to the report by stating that the agency “has procedures in place specifically for the evaluation of questionable credit claims early in the processing stream and prior to issuance of a refund.”[471]

* In the wake of the WTHR news report, 11 current and former IRS employees contacted WHTR and made statements such as the following:

* Two months later, the Treasury Department’s Inspector General for Tax Administration published an audit of the IRS department that handles tax returns for illegal immigrants and foreign investors. Since these individuals are ineligible to receive Social Security Numbers, the IRS issues them ITINs (Individual Taxpayer Identification Numbers).[473] The audit found that the:

* With regard to fraudulent tax refunds obtained through identity theft, IRS Inspector General J. Russell George stated: “Once the money is out the door, it is almost impossible to get it back.”[480]

* Various members of Congress have sponsored bills to prevent the IRS from awarding refundable child tax credits to illegal immigrants, none of which have become law. For example:

* In 2017, Congress passed and Republican President Donald Trump signed a law that:

* President Trump’s 2018, 2019, 2020 and 2021 budget proposals called for restricting illegal immigrants from obtaining refundable child tax credits.[503] [504] [505] [506]

* Examples of the types of decisions that are affected by taxes include:

* Among different measures of taxes, marginal tax rates—which are the rates that taxpayers pay on the next dollar of income they earn—typically have the greatest impact on people’s financial decisions. This is because when people are deciding whether or not to take effort or risk to earn more income, they typically consider how much money they will take home after taxes. The marginal tax rate informs such decisions because it determines how much of this added income will be taken in taxes.[514] [515]

* Per the U.S. Joint Committee on Taxation, the negative economic effects of taxes can be minimized while collecting the same amount of tax revenue when there is “a broad base of taxation in order to keep marginal tax rates as low as possible….”[516]

* Marginal tax rates are generally higher than average tax rates because much income is not subject to taxation (due to tax preferences) and because income tax brackets rise with income.[517] [518] For example, households with $85,500 in income during 2019 paid an average of $10,600 in federal taxes, which amounts to an effective tax rate of 12%.[519] [520] [521] However, if the household earned another $10,000, they would have paid a marginal tax rate of about 39% on this added income.[522]

* Marginal tax rates can have differing effects on people depending upon their circumstances and mindsets.[523] Per the Congressional Budget Office (CBO):

* There is disagreement among economists about the quantitative effects of marginal tax rates, but there is broad agreement that:

* With regard to the effects of marginal tax rate on investments and savings, the Congressional Budget Office and Joint Committee on Taxation have stated:

* In addition to marginal tax rates, other aspects of tax laws with economic effects include provisions such as the following:

* Excise taxes are imposed on specific goods and services, whereas sales taxes are imposed on wide arrays of goods and services.[538] [539]

* In addition to raising revenue, excise taxes are sometimes imposed to discourage or penalize certain activities.[540] [541] Per the U.S. Joint Committee on Taxation:

* In 2020, excise taxes comprised 2% of the taxes collected by the federal government and 11% of the taxes collected by state and local governments:

* In 2018, state and local excise taxes ranged from a low of $328 per person in Arizona to a high of $1,134 per person in Vermont. The nationwide average was $613 per person.[544]

* Excise taxes are remitted by businesses that manufacture, import, or sell the goods and services that are taxed.[545] [546]

* The economic burden of excise taxes primarily falls on retail customers in the form of higher prices. Per the Congressional Budget Office:

* In 2010, the 111th Congress and President Obama passed the Affordable Care Act (a.k.a. Obamacare), which enacted several new types of excise taxes on items such as medical devices, indoor tanning services, and high-cost health plans. Some of these taxes took effect during 2010–2014, and others were delayed by Congress.[551] [552] [553] In 2019, the 116th Congress and President Trump repealed the taxes on medical devices and high-cost health plans.[554]

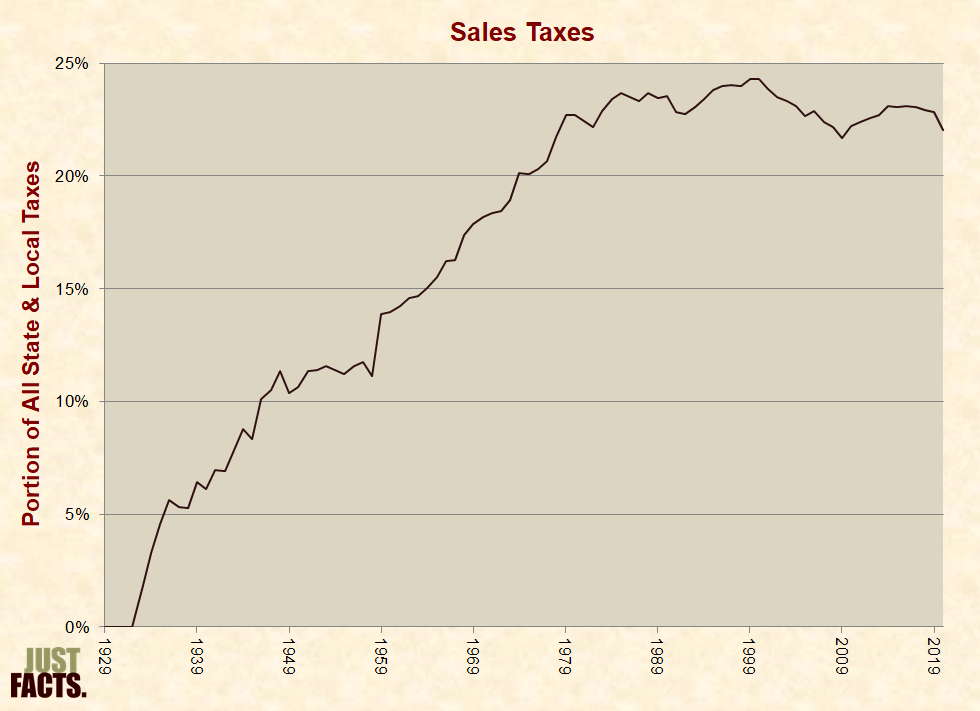

* Sales taxes are typically remitted by retailers and shown on purchase receipts, but the burden of these taxes falls on both consumers and retailers to varying degrees, depending upon the product or service.[555] [556] [557]

* Most states don’t impose a sales tax on prescription drugs or food.[558]

* In 2020, sales taxes comprised 22% of the taxes collected by state and local governments:

* In 2018, the portion of state and local tax collections that were comprised of sales taxes varied from a high of 42% in Louisiana, to a median of 22% in Michigan, to a low of 0% in Delaware, Montana, New Hampshire and Oregon.[560]

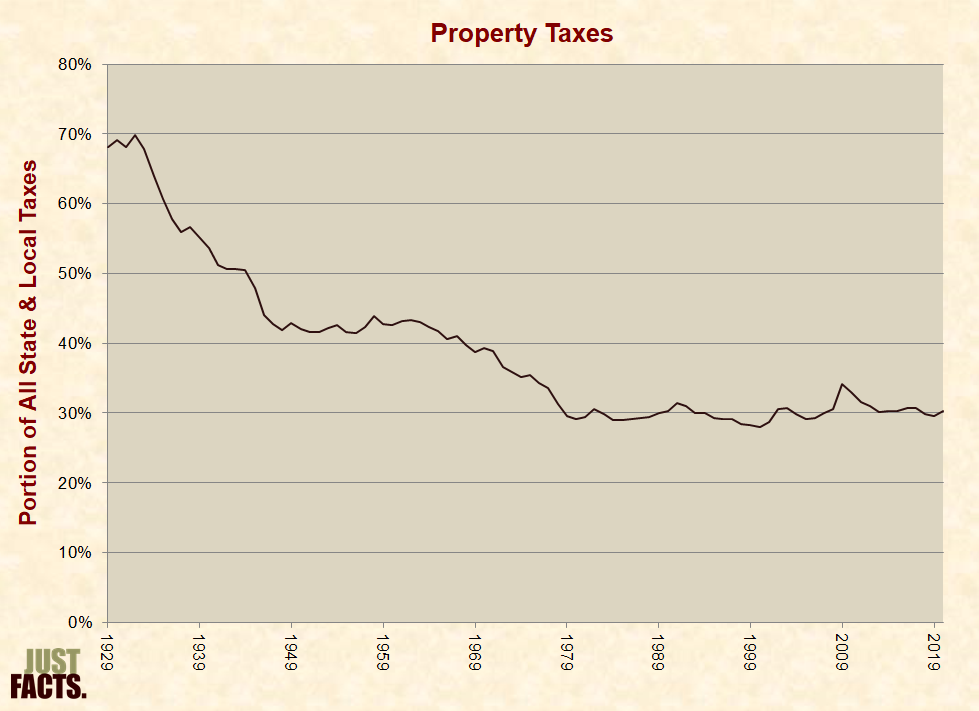

* Property taxes are annual levies on properties based upon their appraised value. Per The Oxford Companion to American Law, property taxes were levied:

* Local governments generally do not levy property taxes on colleges, hospitals, and other nonprofit organizations, but these organizations sometimes make “payments in lieu of taxes” or “PILOTs” to local governments. Such payments are generally lower than property taxes.[562]

* In addition to property taxes on real estate, some states levy taxes on personal property such as automobiles, boats, and aircraft.[563]

* In 2020, property taxes comprised 30% of the taxes collected by state and local governments:

* In 2018, the portion of state and local tax collections that were comprised of property taxes varied from a high of 64% in New Hampshire, to a median of 30% in Arizona, to a low of 17% in Delaware.[565]

* In 2018, state and local property taxes ranged from a low of $598 per person (not per household) in Alabama to a high of $3,378 per person in New Jersey. The nationwide average was $1,675 per person.[566]

* Economists generally fall into three different camps regarding who bears the burden of property taxes. All three groups agree that property taxes on owner-occupied housing are mostly borne by homeowners, and property taxes on land (but not necessarily housing located on the land) are mostly borne by landowners. There is much disagreement over commercial and industrial properties.[567]

* Per the Congressional Research Service, the federal:

* The modern federal estate tax was first enacted in 1916, and per the IRS, it “was to serve the dual purposes of producing revenue and redistributing wealth.”[569]

* In 2020, estate and gift taxes comprised 0.5% of total federal taxes and 0.3% of total state and local taxes:

* Hidden taxes are those that are not apparent to the individuals who ultimately pay them. Per the director of the Congressional Budget Office (CBO):

[T]he ultimate cost of a tax or fee is not necessarily borne by the entity that writes the check to the government.[571]

* Examples of hidden taxes include:

* In 2020, U.S. households paid an average of $7,000 in hidden federal taxes. For different income groups, the amounts and rates varied as follows:

|

2020 Average Hidden Federal Taxes Per Household |

|||

|

Income Group |

Full Income |

Hidden Taxes |

Hidden Tax Rate |

|

Lowest 20% |

$42,200 |

$1,400 |

3.3% |

|

Second 20% |

$63,600 |

$3,000 |

4.7% |

|

Middle 20% |

$90,500 |

$4,700 |

5.2% |

|

Fourth 20% |

$131,800 |

$7,350 |

5.6% |

|

Highest 20% |

$360,900 |

$19,500 |

5.4% |

|

81–90% |

$191,500 |

$11,300 |

5.9% |

|

91–95% |

$265,100 |

$15,700 |

5.9% |

|

96–99% |

$440,000 |

$22,900 |

5.2% |

|

Highest 1% |

$2,291,800 |

$111,300 |

4.9% |

* Governments also enact laws and regulations that do not collect tax revenue but impose the costs of government policies on the private sector. These are functional hidden taxes, and examples of such include:

* The U.S. Constitution vests Congress with the powers to tax, spend, and pay the debts of the federal government. Legislation to carry out these functions must be enacted in one of the following ways:

* Per the Congressional Budget Office (CBO), “Most parameters of the tax code are not indexed for real income growth, and some are not indexed for inflation.” Thus, if tax laws remain unchanged, “average federal tax rates would increase in the long run” (for more detail, see Bracket Creep).[595]

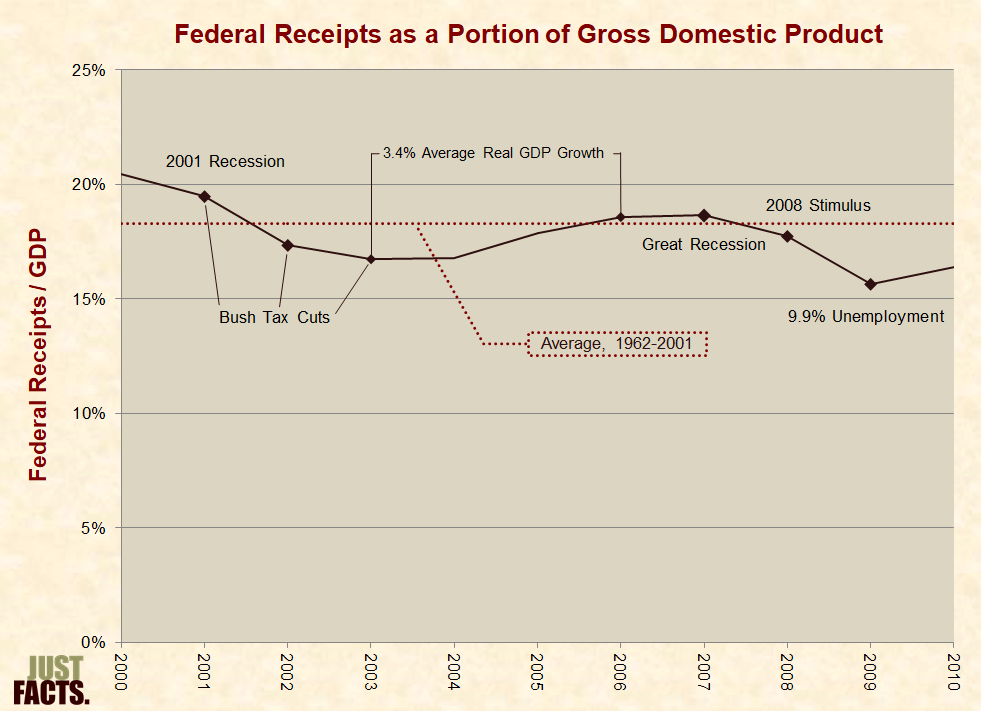

* In 2000, the federal government collected revenues equal to 20.4% of the nation’s gross domestic product (GDP). This was the highest level in the history of the United States.[596]

* In 2000, the stock market “dotcom” bubble burst,[597] [598] [599] the NASDAQ lost 39% of its value,[600] and profits for nonfinancial corporations fell by 18%.[601] In the first quarter of 2001, the nation’s GDP contracted and a recession began.[602] [603]

* Republican President George W. Bush entered office in January of 2001 and signed his first major economic bill in June of that year.[604] [605] Among other provisions, this law enacted various tax reforms that Congress and Bush accelerated and expanded upon in 2002 and 2003. Collectively, these statues:

* Collectively, the tax provisions in these laws are known as the “Bush tax cuts.” Congress passed these bills with Democratic and Republican support varying as follows:

|

Congressional Bush Tax Cut Votes |

||||

|

Bill Year |

Democrats |

Republicans |

||

|

For |

Against |

For |

Against |

|

|

2001 |

15% |

71% |

95% |

1% |

|

2002 |

90% |

4% |

98% |

0% |

|

2003 |

4% |

96% |

97% |

1% |

* In order to avert Democratic filibusters in the Senate, Republicans used a procedural rule that required them to sunset many of the tax cuts at the end of 2010.[611] [612] [613] [614] [615]

* In addition to the Bush tax cuts, federal revenues during 2000–2010 were impacted by factors such as:

* From 2000 to 2010, federal revenues (as a portion of GDP) varied as follows:

* For facts related to the economic implications of the Bush tax cuts, see the sections of this research on economic effects and government debt.

* In 2007, the housing bubble burst, and “banks began reporting large losses resulting from declines in the market value of mortgages and other assets.”[629] The nation entered a recession in the last quarter of 2007,[630] and unemployment increased from 5.0% at the outset of 2008 to 9.9% at the end of 2009.[631]

* Democratic President Barack Obama entered office in January of 2009 and signed his first major economic bill one month later in February.[632] [633] Among other provisions, this law:

* Congress passed this bill with 97% of Democrats voting for it and 98% of Republicans voting against it.[635]

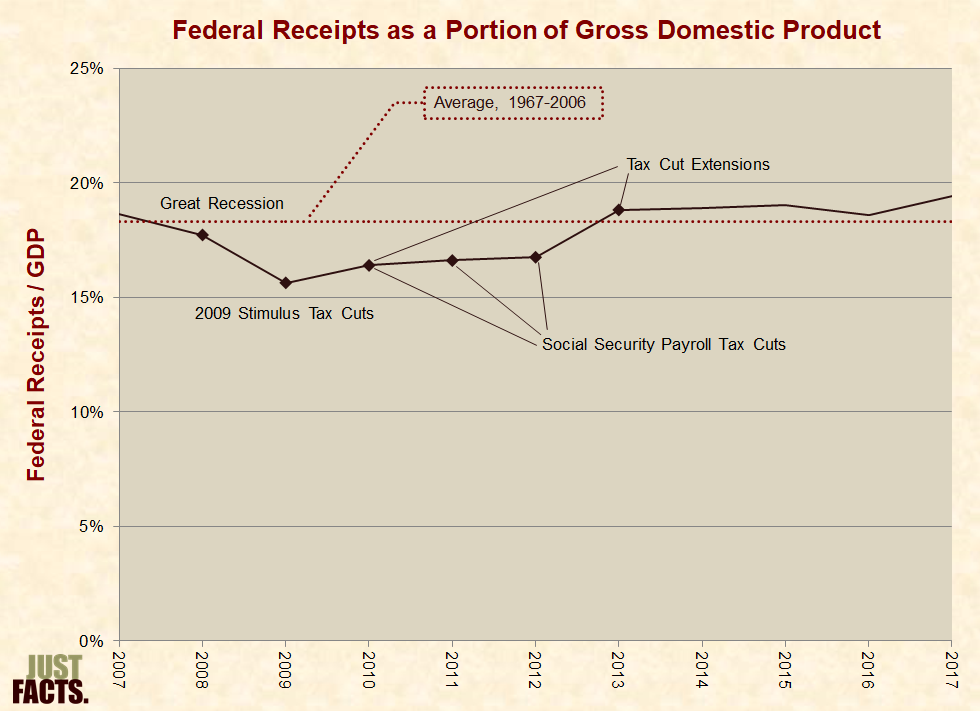

* In December of 2010, Congress passed and Obama signed a bill that extended most of the Bush tax cuts and some of the tax cuts from Obama’s 2009 law through 2012. This law also decreased the Social Security payroll tax by two percentage points until the end of 2011.[636] [637] In 2011 and 2012, Congress and Obama extended the Social Security tax cut through the end of 2012.[638] [639]

* In January of 2013, Congress passed and Obama signed a bill to make the most of the previous tax cuts permanent for everyone but high-income earners (except for adjustments to the estate, gift, and alternative minimum taxes). Also, the law did not renew the Social Security payroll tax cut.[640] [641]

* In addition to the Obama tax cuts, federal revenues during 2007–2017 were impacted by factors such as:

* From 2007 to 2017, federal revenues (as a portion of GDP) varied as follows:

[650] [651] [652] [653] [654] [655]

* For facts related to the economic implications of the Obama tax cuts, see the sections of this research on economic effects and government debt.

* In a campaign speech during September of 2008, Barack Obama stated:

I can make a firm pledge: under my plan, no family making less than $250,000 a year will see any form of tax increase. Not your income tax, not your payroll tax, not your capital gains taxes, not any of your taxes.[656]

* About two weeks after taking office, Obama signed a law that more than doubled federal excise taxes on cigarettes, cigars, and other tobacco products.[657] [658] [659] The bill passed with 98% of Democrats voting for it and 75% of Republicans voting against it.[660] Per the Congressional Budget Office, “The effect of excise taxes, relative to income, is greatest for lower-income households, which tend to spend a greater proportion of their income on such goods as gasoline, alcohol, and tobacco, which are subject to excise taxes.”[661]

* In 2010, the 111th Congress and President Obama passed two laws that are collectively known as the Affordable Care Act or “Obamacare.” These bills passed with 88% to 89% of Democrats voting for them and 99% of Republicans voting against them.[662] [663] These laws impose or increase 10 types of taxes, fees, and penalties (in addition to fines for not having health insurance).[664] The largest of these are:

* Regarding tax preferences (which are also a form of spending), the Affordable Care Act provided refundable tax credits for individuals who purchase health insurance with incomes up to 400% of federal poverty guidelines (for example, $106,000 for a family of four).[676] [677] [678] The law also eliminated or reduced six other preferences while adding three others.[679] [680]

* The Affordable Care Act also imposed fines on large employers that don’t provide full time-employees with health insurance that meets certain requirements,[681] and the law requires most Americans to carry some form of health insurance starting in 2014 or pay a fine.[682] [683] [684] [685] (In 2017, Congress passed and President Trump signed a law that repealed this fine starting in 2019.[686] [687] [688])

* During a September 2009 interview on ABC News, Obama was asked if such a fine constitutes a tax increase, and he replied, “I absolutely reject that notion.”[689] In March of 2012, an Obama administration lawyer argued before the Supreme Court that the Affordable Care Act’s fine for not buying health insurance is constitutional because:

* The Supreme Court ruled (5 to 4) that Obamacare’s fine is constitutional on the grounds that it is a tax.[691]

* Obama’s budget proposal for 2017 contained 45 pages of tax-related provisions.[692] Some of his proposals were to:

* Per the Joint Committee on Taxation and Congressional Budget Office:

* For more facts related to the economic implications of the Obama tax increases, see the sections of this research on economic effects and government debt.

* Republican President Donald Trump entered office in January of 2017 and signed his first major economic bill in December of that year.[705] [706] Among other provisions, this law permanently lowered the corporate tax rate beginning in 2018 and temporarily (during 2018–2025):

* The bill passed Congress with 95% of Republicans voting for it and 98% of Democrats voting against it.[708]

* In order to avert a Democratic filibuster in the Senate, Republicans used a procedural rule that required them to sunset many of the tax reforms at the end of 2025.[709] [710] [711]

* In April of 2018, the Congressional Budget Office (CBO) projected that federal revenues will vary as follows under current law:

* Per the Congressional Budget Office, the corporate income tax “reduces capital investment in the United States,” and hence:

* By August 2020, businesses had enacted at least 1,200 general pay raises, bonuses, benefit increases, consumer price reductions, charitable donations, and business expansions that they credited to the Trump tax cuts.[715]

* For more facts related to the economic implications of the Trump tax cuts, see the sections of this research on economic effects and government debt.

* When President Bush proposed tax cuts at the outset of his presidency, Newsweek published a cover story that showed pictures of objects that people with various incomes could buy with money from the tax cuts. On the low end, Newsweek showed a bowl of pasta to signify “three weeks’ worth of groceries” or $168 that a family of four with a gross income of $20,000 would save on an annual basis. On the high end, Newsweek showed a Lexus GS 430 to signify $47,114 that a married couple with an income of $1,000,000 would save on an annual basis.[716]

* Newsweek did not reveal what these families were currently paying in federal taxes or what they were receiving in cash and other benefits from the federal government. The family with a gross income of $20,000 was paying about $1,600 per year in taxes while receiving $16,000 from the government. In comparison, the family with an income of $1,000,000 was paying $325,000 in taxes and receiving $7,000 from the government.[717] [718]

* Per the U.S. Government Accountability Office, when government spends more than it collects in revenues, the resultant debt is “borne by tomorrow’s workers and taxpayers.” This burden can manifest in the form of higher taxes, reduced government benefits, decreased economic growth, inflation, or combinations of such results.[719] [720] [721] [722]

* Other factors impacting the debt/GDP ratio include but aren’t limited to high inflation (which lowers the ratio in the short term and raises it in the long term),[723] [724] [725] legislation passed by previous Congresses and presidents,[726] economic cycles, terrorist attacks, pandemics, government-mandated lockdowns, natural disasters, demographics, and the actions of U.S. citizens and foreign governments.[727] [728] [729]

* During the first session of the 113th Congress (January–December 2013), U.S. Representatives and Senators introduced 168 bills that would have reduced spending and 828 bills that would have raised spending.[730]

* The table below quantifies the costs and savings of these bills by political party. This data is provided by the National Taxpayers Union Foundation:

|

Costs/Savings of Bills Sponsored or Cosponsored in 2013 by Typical Congressman (in Billions) |

||||

|

Legislative Body & Party |

Proposed Increases |

Proposed Decreases |

Net Agendas |

Change in 2013 Budget Outlays (%) |

|

House Democrats |

$407 |

$10 |

$397 |

11.5 |

|

Senate Democrats |

$22 |

$3 |

$18 |

0.5 |

|

House Republicans |

$9 |

$91 |

–$83 |

–2.4 |

|

Senate Republicans |

$6 |

$165 |

–$159 |

–4.6 |

* The table below quantifies the net agendas of the political parties in previous Congresses:

|

Costs/Savings of Bills Sponsored or Cosponsored in the First Sessions of Congress by Typical Congressman (in Billions) |

|||||||

|

2011 |

2009 |

2007 |

2005 |

2003 |

2001 |

1999 |

|

|

House Democrats |

$497 |

$500 |

$547 |

$547 |

$402 |

$262 |

$34 |

|

Senate Democrats |

$24 |

$134 |

$59 |

$52 |

$174 |

$88 |

$15 |

|

House Republicans |

–130 |

–$45 |

$7 |

$12 |

$31 |

$20 |

–$5 |

|

Senate Republicans |

–$239 |

$51 |

$7 |

$11 |

$26 |

$19 |

–$324 |

|

NOTE: Data not adjusted for inflation. |

|||||||

* In February 2001, Republican President George W. Bush stated:

* From the time that Congress enacted Bush’s first major economic proposal (June 7, 2001[735]) until the time that he left office (January 20, 2009), the national debt rose from 54% of GDP to 74%, or an average of 2.7 percentage points per year.[736]

* During eight years in office, President Bush vetoed 12 bills, four of which were overridden by Congress and thus enacted without his approval.[737] These bills were projected by the Congressional Budget Office to increase the deficit by $26 billion during 2008–2022.[738]

* In February 2009, Democratic President Barack Obama stated:

* From the time that Congress enacted Obama’s first major economic proposal (February 17, 2009[740]) until the time that he left office (January 20, 2017), the national debt rose from 75% of GDP to 104%, or an average of 3.6 percentage points per year.[741]

* During eight years in office, President Obama vetoed twelve bills, one of which was overridden by Congress and thus enacted without his approval.[742] The Congressional Budget Office estimated that this bill “would have no significant effect on the federal budget.”[743]

Donald Trump

* In March 2016, Republican presidential candidate Donald Trump had the following exchange in an interview with Bob Woodward of the Washington Post:

* From the time that Congress enacted Trump’s first major economic proposal (December 20, 2017[745]) until the outset of the Covid-19 pandemic (March 11, 2020[746]), the national debt rose from 102.9% of GDP to 108.9%, or an average of 2.7 percentage points per year.[747]

* Before the Covid-19 pandemic, President Trump vetoed six bills, none of which were overridden by Congress.[748]

* From the outset of the Covid-19 pandemic (March 11, 2020[749]) until the end of 2020, the national debt rose from 108.9% of GDP to 129.1%, or at a rate of 24.9 percentage points per year.[750]

* During the Covid-19 pandemic, President Trump vetoed four bills, one of which was overridden by Congress and thus enacted without his approval.[751] The Congressional Budget Office estimated that this bill would increase the deficit by $21 million during 2021–2030.[752]

* In May 2022, President Biden claimed:

* From the time that Congress enacted Biden’s first major economic proposal (March 10, 2021[754]) until June 28, 2024, the national debt:

* From the beginning of his presidency until December 31, 2022, Biden vetoed one bill, and it was not overridden by Congress.[759]

* The lifting of Covid-19 lockdowns allowed GDP to recover in the first year of Biden’s term, thereby decreasing the debt/GDP ratio.[760] [761] [762] [763]

* As documented in an article published by the Federal Reserve Bank of St. Louis, inflation:

* Without mentioning the role of Congress in taxes, spending, or the national debt,[767] [768] PolitiFact reported in 2009 that the national debt increased by $5 trillion “under” George W. Bush, while “there were several years of budget surpluses” at “the end of the Clinton administration.”[769]

* Measured in consistent terms, the average annual changes in national debt varied as follows during the tenures of recent presidents and congressional majorities:

|

Political Power |

Dates |

Annual Change in National Debt |

|

|

Raw Debt (Trillions) |

Percentage Points of GDP |

||

|

Bill Clinton with Democratic House and Senate |

1/20/93 – 1/4/95 |

$0.3 |

0.8 |

|

Bill Clinton with Republican House and Senate |

1/4/95 – 1/19/01 |

$0.2 |

-1.5 |

|

George W. Bush with Republican House and Senate |

1/20/01 – 6/6/01, 11/12/02 – 1/4/07 |

$0.5 |

0.7 |

|

George W. Bush with Republican House and Democratic Senate |

6/6/01 – 11/12/02 |

$0.4 |

2.2 |

|

George W. Bush with Democratic House and Senate |

1/4/07 – 1/20/09 |

$1.0 |

6.2 |

|

Barack Obama with Democratic House and Senate |

1/20/09 – 1/5/11 |

$1.7 |

9.0 |

|

Barack Obama with Republican House and Democratic Senate |

1/5/11 – 1/6/15 |

$1.0 |

2.2 |

|

Barack Obama with Republican House and Senate |

1/6/15 – 1/20/17 |

$0.9 |

1.6 |

|

Donald Trump with Republican House and Senate |

1/20/17 – 1/3/19 |

$1.0 |

0.2 |

|

Donald Trump with Democratic House and Republican Senate |

1/3/19 – 1/20/21 |

$2.8 |

9.2 |

|

Joseph Biden with Democratic House and Democratic Senate |

1/20/21 – 1/3/23 |

$1.8 |

-3.0 |

* Other factors impacting the debt/GDP ratio include but aren’t limited to high inflation (which lowers the ratio in the short term and raises it in the long term),[771] [772] [773] legislation passed by previous Congresses and presidents,[774] economic cycles, terrorist attacks, pandemics, government-mandated lockdowns, natural disasters, demographics, and the actions of U.S. citizens and foreign governments.[775] [776] [777]

[1] Entry: “tax.” Collins English Dictionary—Complete & Unabridged. HarperCollins, 1991, 1994, 1998, 2000, 2003. <www.thefreedictionary.com>

“1. (Government, Politics & Diplomacy) a compulsory financial contribution imposed by a government to raise revenue, levied on the income or property of persons or organizations, on the production costs or sales prices of goods and services, etc.”

[2] Calculated with data from:

a) Dataset: “Table 3.1. Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

b) Dataset: “Table 3.2. Federal Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

c) Dataset: “Table 3.3. State and Local Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

d) Dataset: “Table 5.11U. Capital Transfers Paid and Received, by Sector and by Type [Millions of Dollars; Quarters Seasonally Adjusted at Annual Rates].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

e) Dataset: “CPI—All Urban Consumers (Current Series).” U.S. Department of Labor, Bureau of Labor Statistics. Accessed January 27, 2023 at <www.bls.gov>

“Series Id: CUUR0000SA0; Series Title: All Items in U.S. City Average, All Urban Consumers, Not Seasonally Adjusted; Area: U.S. City Average; Item: All Items; Base Period: 1982–84=100”

f) Dataset: “Table 7.1. Selected Per Capita Product and Income Series in Current and Chained Dollars.” U.S. Bureau of Economic Analysis. Last revised January 26, 2023. <apps.bea.gov>

Line 18: “Population (Midperiod, Thousands)”

g) Dataset: “HH-1. Households by Type: 1940 to Present.” U.S. Census Bureau, Current Population Survey, November 2022. <www.census.gov>

h) Dataset: “Table 1.1.5. Gross Domestic Product.” United States Department of Commerce, Bureau of Economic Analysis. Last revised January 26, 2023. <apps.bea.gov>

Line 1: “Gross Domestic Product”

NOTES:

[3] Calculated with data from:

a) Dataset: “Table 3.1. Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023 <apps.bea.gov>

b) Dataset: “Table 3.2. Federal Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023 <apps.bea.gov>

c) Dataset: “Table 3.3. State and Local Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023 <apps.bea.gov>

d) Dataset: “Table 5.11 Capital Transfers Paid and Received, by Sector and by Type [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised September 30, 2022. <apps.bea.gov>

e) Dataset: “Table 5.11U. Capital Transfers Paid and Received, by Sector and by Type [Millions of Dollars; Quarters Seasonally Adjusted at Annual Rates].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023 <apps.bea.gov>

f) Dataset: “CPI—All Urban Consumers (Current Series).” U.S. Department of Labor, Bureau of Labor Statistics. Accessed January 27, 2023 at <www.bls.gov>

“Series Id: CUUR0000SA0; Series Title: All Items in U.S. City Average, All Urban Consumers, Not Seasonally Adjusted; Area: U.S. City Average; Item: All Items; Base Period: 1982–84=100”

g) Dataset: “Table 7.1. Selected Per Capita Product and Income Series in Current and Chained Dollars.” U.S. Bureau of Economic Analysis. Last revised January 26, 2023. <apps.bea.gov>

Line 18: “Population (Midperiod, Thousands)”

NOTES:

[4] Article: “Federal Reserve’s Role During WWII.” By Gary Richardson. Federal Reserve Bank of Richmond, Federal Reserve History, November 22, 2013. <www.federalreservehistory.org>

In September 1939, Germany’s invasion of Poland triggered war among the principal European powers. In December 1941, Japan attacked Pearl Harbor. Germany and Italy declared war on the United States. The American “arsenal of democracy” joined the Allied nations, including Britain, France, China, the Soviet Union, and numerous others, in the fight against the Axis alliance. The Allied counteroffensive began in 1942. The Axis surrendered in 1945.

[5] Calculated with data from:

a) Dataset: “Table 3.1. Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

b) Dataset: “Table 3.2. Federal Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

c) Dataset: “Table 3.3. State and Local Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

d) Dataset: “Table 5.11 Capital Transfers Paid and Received, by Sector and by Type [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised September 30, 2022. <apps.bea.gov>

e) Dataset: “Table 5.11U. Capital Transfers Paid and Received, by Sector and by Type [Millions of Dollars; Quarters Seasonally Adjusted at Annual Rates].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

f) Dataset: “Table 1.1.5. Gross Domestic Product.” United States Department of Commerce, Bureau of Economic Analysis. Last revised January 26, 2023. <apps.bea.gov>

Line 1: “Gross Domestic Product”

NOTES:

[6] Article: “Federal Reserve’s Role During WWII.” By Gary Richardson. Federal Reserve Bank of Richmond, Federal Reserve History, November 22, 2013. <www.federalreservehistory.org>

In September 1939, Germany’s invasion of Poland triggered war among the principal European powers. In December 1941, Japan attacked Pearl Harbor. Germany and Italy declared war on the United States. The American “arsenal of democracy” joined the Allied nations, including Britain, France, China, the Soviet Union, and numerous others, in the fight against the Axis alliance. The Allied counteroffensive began in 1942. The Axis surrendered in 1945.

[7] Report: “United States Federal Debt: Answers To Frequently Asked Questions, An Update.” U.S. Government Accountability Office, August 12, 2004. <www.gao.gov>

Page 39:

Over the long term, the costs of federal borrowing will be borne by tomorrow’s workers and taxpayers. Higher saving and investment in the nation’s capital stock—factories, equipment, and technology—increase the nation’s capacity to produce goods and services and generate higher income in the future. Increased economic capacity and rising incomes would allow future generations to more easily bear the burden of the federal government’s debt. Persistent deficits and rising levels of debt, however, reduce funds available for private investment in the United States and abroad. Over time, lower productivity and GDP [gross domestic product] growth ultimately may reduce or slow the growth of the living standards of future generations.

Page 41:

GAO’s [Government Accountability Office’s] long-term simulations show that absent policy actions aimed at deficit reduction, debt burdens of such magnitudes imply a substantial decline in national saving available to finance private investment in the nation’s capital stock. The fiscal paths simulated are ultimately unsustainable and would inevitably result in declining GDP and future living standards. Even before such effects, these debt paths would likely result in rising inflation, higher interest rates, and the unwillingness of foreign investors to invest in a weakening American economy.

[8] Brief: “Federal Debt and the Risk of a Fiscal Crisis.” Congressional Budget Office, July 27, 2010. <www.cbo.gov>

Page 1: “[I]f the payment of interest on the extra debt was financed by imposing higher marginal tax rates, those rates would discourage work and saving and further reduce output.”

[9] Book: This Time is Different: Eight Centuries of Financial Folly. By Carmen M. Reinhart (University of Maryland) and Kenneth S. Rogoff (Harvard University). Princeton University Press, 2009.

Page 175: “[I]nflation has long been the weapon of choice in sovereign defaults on domestic debt and, where possible, on international debt.”

[10] The consequences of unchecked government debt are addressed in greater detail in Just Facts’ research on the national debt.

[11] Calculated with data from:

a) Dataset: “Table 3.1. Government Current Receipts and Expenditures [Billions of dollars].” U.S. Bureau of Economic Analysis. Last revised March 30, 2023. <apps.bea.gov>

b) Dataset: “Table 1.1.5. Gross Domestic Product.” United States Department of Commerce, Bureau of Economic Analysis. Last revised January 26, 2023. <apps.bea.gov>

Line 1: “Gross Domestic Product”

c) Dataset: “HH-1. Households by Type: 1940 to Present.” U.S. Census Bureau, Current Population Survey, November 2022. <www.census.gov>

NOTES:

[12] Article: “Federal Reserve’s Role During WWII.” By Gary Richardson. Federal Reserve Bank of Richmond, Federal Reserve History, November 22, 2013. <www.federalreservehistory.org>

In September 1939, Germany’s invasion of Poland triggered war among the principal European powers. In December 1941, Japan attacked Pearl Harbor. Germany and Italy declared war on the United States. The American “arsenal of democracy” joined the Allied nations, including Britain, France, China, the Soviet Union, and numerous others, in the fight against the Axis alliance. The Allied counteroffensive began in 1942. The Axis surrendered in 1945.

[13] “WHO Director-General’s Opening Remarks at the Media Briefing on Covid-19.” World Health Organization, March 11, 2020. <www.who.int>

[Dr. Tedros Adhanom Ghebreyesus:] …

WHO [World Health Organization] has been assessing this outbreak around the clock and we are deeply concerned both by the alarming levels of spread and severity, and by the alarming levels of inaction.

We have therefore made the assessment that COVID-19 can be characterized as a pandemic.