Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

A major source of information for this research is the 2023 Social Security Trustees Report.[1] This report was published in March 2023 and uses data from 2022 as a baseline. Unless otherwise stated, all dollar figures in this research are indexed for inflation to keep the data consistent with 2022/2023 dollars.[2] [3]

Whenever the word “projections” is used, this refers to projections made by the United States Social Security Administration. The process of making projections is not an exact science, and actual outcomes often differ from those predicted (see Accuracy of Projections). The Social Security Trustees Report contains high, low, and intermediate projections. Unless otherwise stated, this research cites the intermediate figures, because these “reflect the Trustees’ best estimates of future experience.”[4]

* In 1935, Congress passed and Democratic President Franklin D. Roosevelt signed into law the “Social Security Act.” This law created “a system of Federal old-age benefits” for workers and their families. In 1956, the law was amended to also provide disability benefits.[5] [6]

* Social Security is composed of two separate entities: the “Old-Age and Survivors Insurance” program and the “Disability Insurance” program. Each program has separate finances handled through two separate trust funds. For the purpose of simplicity, the figures shown below reflect the combination of both programs unless otherwise stated.[7] [8]

* The Supplemental Security Income (SSI) program provides benefits for aged, blind, and disabled people without regard to prior workforce participation. It is administered by the Social Security Administration, but it is not funded by Social Security taxes. Unless otherwise stated, this program is not covered in this research.[9]

* As of June 30, 2022, 65.6 million people or 20% of the U.S. population were receiving monthly Social Security benefits.[10]

* Certain groups of workers were originally exempt from Social Security, including government employees, railroad workers, the self-employed, farm workers, domestic help, and employees of nonprofit organizations. In 1950 and 1983, the law was changed to require most of these individuals to participate in the program, although about 25% of state and local government workers are still exempted.[11] [12] [13] [14] [15]

* Under certain conditions, some members of the clergy and religious groups are not required to participate in Social Security.[16]

* Social Security is the largest government program in the world.[17] Relative to other U.S. federal programs, Social Security outlays in 2022 were:

* Payroll taxes are taxes that are levied on the wages of workers.[19] [20]

* From the inception of the Social Security program through 2022, payroll taxes have supplied 97% of the program’s direct tax revenues.[21]

* Social Security and Medicare payroll taxes are sometimes called FICA taxes or SECA taxes. The acronym FICA stands for the “Federal Insurance Contributions Act,” and SECA stands for the “Self-Employment Contributions Act.”[22]

* The typical SECA tax rates for people who are self-employed are as follows:

|

Social Security Tax |

12.4% |

|

Medicare Tax |

2.9% |

|

Total |

15.3% |

* The typical FICA tax rates for people who are employees are as follows:

|

Social Security Tax |

Medicare Tax |

FICA Tax (Total) |

|

|

Employee tax |

6.2% |

1.45% |

7.65% |

|

Employer tax |

6.2% |

1.45% |

7.65% |

|

Totals |

12.4% |

2.9% |

15.3% |

* For both employees and the self-employed, the Affordable Care Act (a.k.a. Obamacare) levies an additional 0.9% Medicare payroll tax on earnings above $200,000 for singles and $250,000 for couples.[25] [26]

* The payroll tax amounts shown on paychecks generally do not account for the taxes that employers pay.[27] Payroll taxes levied on employers are mainly borne by employees in the form of reduced wages (for more detail, see Just Facts’ research on the Distribution of Tax Burdens).[28] [29] [30] [31] [32] [33]

* Social Security payroll taxes are restricted to a “taxable maximum.” Annual earnings above the maximum are not subject to these taxes. For 2023, the taxable maximum is $160,200.[34]

* Previously, Medicare payroll taxes were restricted to the same taxable maximum as Social Security. In 1993, the 103rd Congress and Democratic President Bill Clinton passed a law removing the taxable maximum for Medicare, thus making all earnings subject to these Medicare taxes.[35] [36] [37]

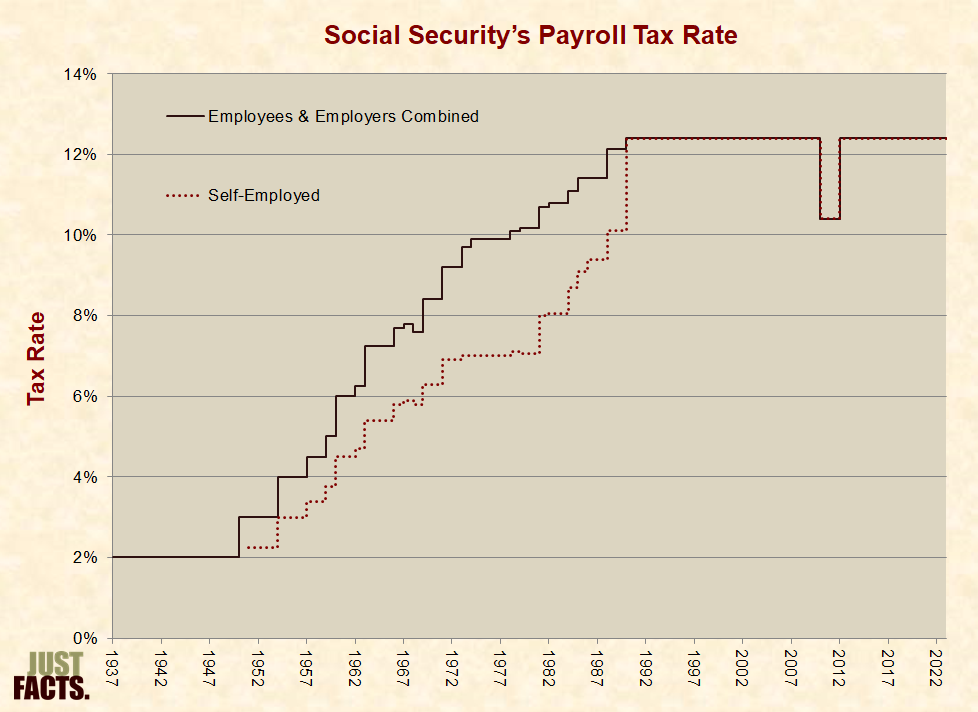

* The Social Security Act of 1935 set the initial payroll tax rate at 2% (employee and employer combined) and specified increases that would bring this rate to 6% by 1949.[38]

* Various Congresses and presidents postponed the tax rate increases scheduled in the original Social Security Act so that the 6% rate planned for 1949 did not take effect until 1960.[39] [40]

* Between 1950 and 1977, various Congresses and presidents passed ten laws increasing the Social Security payroll tax rate above the 6% level specified in the original Social Security Act.[41]

* In 1983, the 98th Congress and Republican President Ronald Reagan accelerated the timeframe for previously enacted payroll tax rate hikes and increased the rate for “the self-employed to equal the combined employee/employer rate but with partially offsetting credits and deductions.”[42]

* In 2010 and 2011, the 111th and 112th Congresses and Democratic President Barack Obama passed three laws that temporarily decreased the Social Security payroll tax during 2011 and 2012 by two percentage points (from 12.4% to 10.4%). These laws also required that monies equivalent to the decreased payroll taxes be transferred to the Social Security program from the general fund of the U.S. Treasury—which is funded by personal income taxes, corporate income taxes, excise taxes, estate and gift taxes, and other miscellaneous receipts.[43] [44] [45] [46] [47] [48]

* Social Security’s payroll tax rate has risen by 6.2 times since the outset of the program:

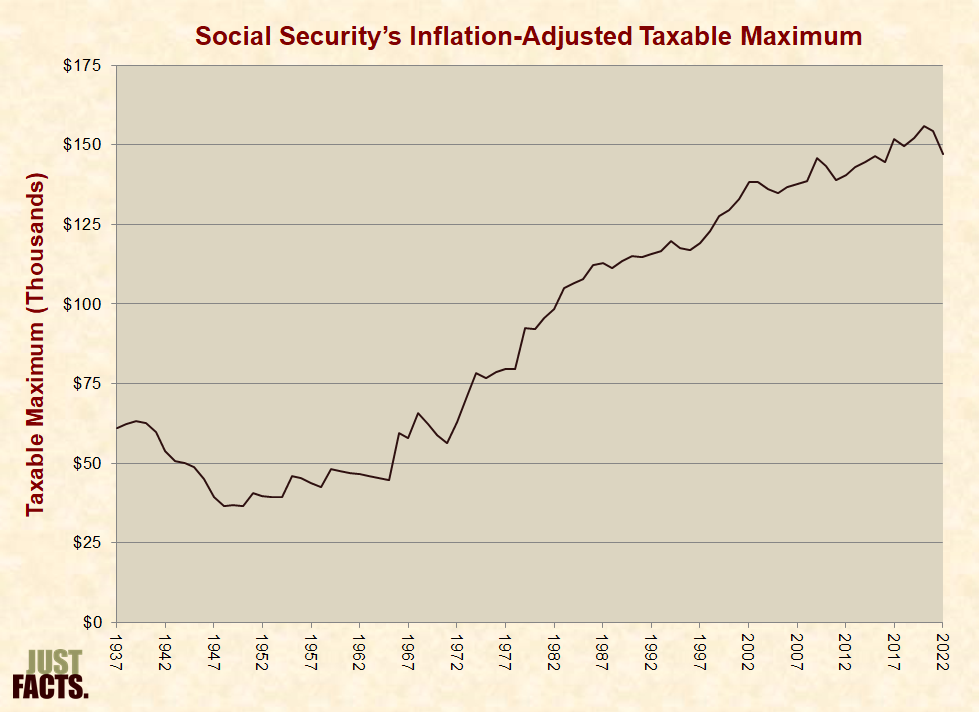

* The Social Security Act of 1935 initially set the annual taxable maximum at $3,000. Income earned above this amount was not subject to Social Security taxes. This threshold was a fixed amount that was not indexed for inflation or wage levels.[50] [51]

* From 1950 to 1971, various Congresses and presidents passed six laws increasing the taxable maximum by a total of 200%—or by 77% above the rate of inflation during this period.[52]

* In 1972 and 1973, the 92nd and 93rd Congresses and Republican President Richard Nixon passed laws:

* In 1977, the 95th Congress and Democratic President Jimmy Carter passed a law increasing the taxable maximum faster than average wage levels in 1979, 1980, and 1981 by a total of 68%.[54] [55]

* Since 1982, the taxable maximum has been annually indexed based roughly upon average worker compensation levels.[56] [57]

* From 1990 to 2021, the inflation-adjusted:

* Adjusted for inflation, Social Security’s taxable maximum has increased by 2.6 times since the outset of the program:

* Since the start of Social Security in 1937, the portion of all covered earnings subject to Social Security payroll taxes has ranged from 71% to 92%, with an average of 84% and a median of 84%. In 2021, this figure was 81%:

* At the outset of the Social Security program, the federal government published an informational pamphlet that stated the following about Social Security taxes:

* Accounting for inflation, the figures above equate to a maximum tax collection of $2,244 per person in 2023 dollars.[64]

* In 2023, the maximum payroll tax collection per person is $19,865 or 8.6 times the promised maximum.[65]

* Some politicians have called for raising the maximum payroll tax to infinity. This includes but is not limited to:

* The taxes above don’t include other taxes that politicians have used to fund Social Security. This includes but is not limited to:

* At the outset of the Social Security program, the federal government published an informational pamphlet that stated the following with regard to old-age benefits:

* Recipients of old-age benefits with incomes of more than $25,000/year and couples with incomes of more than $32,000/year must now pay income taxes on up to 50% of their old-age benefits. Half of an individual’s or couple’s old-age benefits are counted as income when determining if they meet these $25,000 and $32,000 thresholds.[69] [70] These income taxes on Social Security benefits are used to fund Social Security.[71]

* Recipients of old-age benefits with incomes of more than $34,000/year and couples with incomes of more than $44,000/year must also pay income taxes on up to 85% of their old-age benefits. Half of an individual’s or couple’s old-age benefits are counted as income when determining if they meet these $34,000 and $44,000 thresholds.[72]

* The thresholds at which people are required to pay income taxes on their old-age benefits are not automatically indexed to account for inflation or wage growth.[73]

The following projections are based upon what the current law specifies. This does not imply that the Social Security program will have enough money to pay for these benefits. Information concerning the financial stability of the Social Security program is contained in the section below on Financial Status.

* In general, to qualify for old-age benefits, a person must work for ten years while earning at least $6,560 per year.[74]

* Old-age benefit amounts are generally related to the amount of Social Security payroll taxes paid by workers over the course their lifetimes.[75] The Social Security Administration has an Online Calculator that provides an estimate of monthly old-age benefits based upon your earnings, birth date, and expected retirement age. The results can be delivered in either today’s dollars or in future (inflated) dollars.[76]

* People with lower incomes receive higher ratios of annual benefits to taxes.[77] The graph below compares annual old-age benefits to lifetime payroll taxes for 23-year-olds who will work until the age of 67 while earning constant incomes:

* Examples from the graph above:

* Low-income workers receive an effective refund of most of their Social Security taxes through the “earned income tax credit.” This program was established in 1975 to “offset the Social Security taxes of low-income workers with children and to provide those taxpayers with an increased incentive to work.”[80] [81] [82] In 2022, this program spent $64 billion.[83]

* Accounting for interest, people born in 1900 received about seven times more in Social Security benefits than they paid in payroll taxes.[84]

* For workers who earned average wages and retired at the age of 65 in 1980, it took 2.8 years of receiving old-age benefits to recover the value of their payroll taxes (including interest). For workers who retired in 2003, it took 17.4 years. For workers who retired in 2020, it will take 21.6 years.[85] This assumes Social Security will have enough money to pay scheduled benefits for this entire period, which it is not projected to have.[86]

* The federal government adjusts old-age benefits each December based upon the rate of inflation in the previous year. This is called a “cost-of-living adjustment” or “COLA.” The COLAs for recent years were as follows:

|

Year |

COLA |

Year |

COLA |

|

|

2005 |

4.1% |

2014 |

1.7% |

|

|

2006 |

3.3% |

2015 |

0.0% |

|

|

2007 |

2.3% |

2016 |

0.3% |

|

|

2008 |

5.8% |

2017 |

2.0% |

|

|

2009 |

0.0% |

2018 |

2.8% |

|

|

2010 |

0.0% |

2019 |

1.6% |

|

|

2011 |

3.6% |

2020 |

1.3% |

|

|

2012 |

1.7% |

2021 |

5.9% |

|

|

2013 |

1.5% |

2022 |

8.7% |

* The age at which a worker receives full Social Security old-age benefits is referred to as the “full retirement age.” A person’s full retirement age can range from 65 to 67 years old, depending upon his or her year of birth. For those born after 1959, the full retirement age is 67 (more details in footnote).[88]

* Workers have the option to start receiving Social Security benefits at the age of 62, but the benefits are reduced (more details in footnote).[89] Workers also have the option to start receiving benefits later than their full retirement age, and the benefits are increased (more details in footnote).[90]

* Family members of workers who are receiving old-age benefits may also be eligible for benefits, even if they have not worked (more details in footnote).[91]

* When Social Security first began, beneficiaries could take their benefits as a lump sum.[92] The earliest reported applicant for a lump sum Social Security benefit was Ernest Ackerman of Cleveland, OH. Mr. Ackerman retired one day after the program began and paid $0.05 in Social Security taxes. He received a lump sum payment of $0.17, a 240% return.[93]

* Per the Social Security Administration:

* According to the Social Security Administration:

* As of 2023, Social Security pays an average of $21,924/year to retired individuals.[96] In 2022, the U.S. Census Bureau’s poverty threshold for individuals over 65 years of age was $14,036.[97]

* As of 2023, Social Security pays an average of $35,664/year to retired couples.[98] In 2022, the U.S. Census Bureau’s poverty threshold for couples over 65 years of age was $17,689.[99]

* In 2019, the Congressional Budget Office analyzed “whether Social Security benefits enable retired workers to meet their basic needs and the extent to which benefits replace preretirement earnings.” The study focused on “workers with long careers, who generally have higher average earnings than all workers….” Among these people:[100]

* Among elderly Social Security beneficiaries:

* Family members of workers who are receiving old-age benefits may also be eligible for benefits, even if they have not worked (more details in footnote).[108]

* Social Security pays benefits to the families of workers who die and leave behind spouses, children under the age of 20, and sometimes other relations such as parents and ex-spouses (more details in footnote).[109]

* Each dependent receives about 75% to 100% of the deceased worker’s basic Social Security benefit. However, per the Social Security Administration, “there is a limit to the amount of money that can be paid each month to a family. The limit varies, but is generally equal to about 150 to 180 percent of your benefit rate.”[110]

* To qualify for disability benefits, workers generally must first meet two basic tests:

* The federal law that governs Social Security defines “disability” as:

* In general, recipients begin to receive disability benefits after they have been disabled for five full months.[113]

* Disability benefits are calculated based upon a formula that takes into account the Social Security payroll taxes paid over the course of workers’ lifetimes.[114]

* Disability benefits are generally increased once per year based upon the rate of inflation.[115]

* Family members of workers who are receiving disability benefits may also be eligible for benefits, even if they have not worked.[116]

* In December 2021:

* People who received disability payments in December 2021 were awarded benefits for the following primary reasons:

* Distribution of benefits in 2022 were as follows:

|

Category |

Amount (billions) |

Portion of Total Social Security Benefits |

|

Retired workers and their families |

$947 |

77% |

|

Disabled workers and their families |

$143 |

12% |

|

Survivors of deceased workers |

$141 |

11% |

* The Social Security Administration’s website enables individuals to set up an account that provides them with estimates of their benefits and a list of their lifetime earnings according to Social Security’s records. This web-based utility replaces the paper statements that Social Security used to send to individuals each year.

* The Social Security Administration still sends paper statements only to people age 60 and over who are not receiving benefits and don’t have an online Social Security account.[124]

* All financial operations of the Social Security program are legally separated from other operations of the U.S. Treasury.[125] [126]

* Social Security’s expenses include its benefit payments and administrative overhead.[127] [128]

* Social Security’s sources of income include:

* In 2022, Social Security had $1,222 billion in income and $1,244 billion in expenses.[133]

* When Social Security’s sources of income exceed its expenses, federal law requires that the resultant surpluses be loaned to the general fund of the U.S. Treasury. Federal law also requires that the Treasury pay this money back to the Social Security program with interest.[134] [135] [136] [137]

* The money owed by the Treasury to the Social Security program is called the “Social Security Trust Fund,” and at the close of 2022, it had a balance of $2.8 trillion.[138]

* The $2.8 trillion debt that the Treasury owes to Social Security amounts to $8,470 for every person living in the U.S. or $21,569 for every household in the U.S.[139] (Facts about the ability of the Treasury to pay this debt are detailed below in the section below entitled Impact on National Debt.)

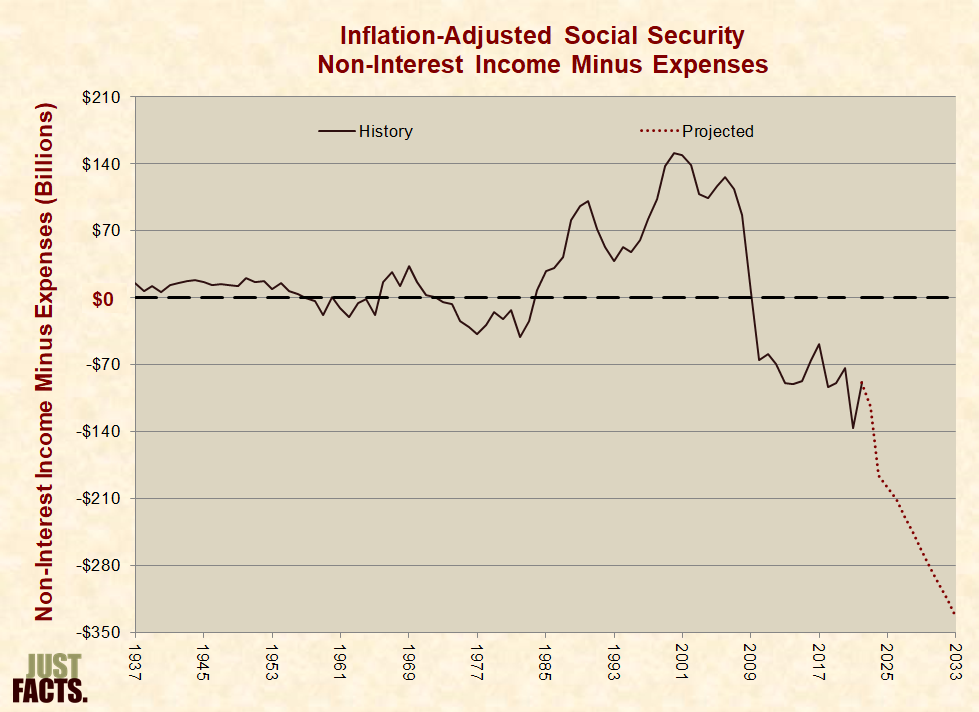

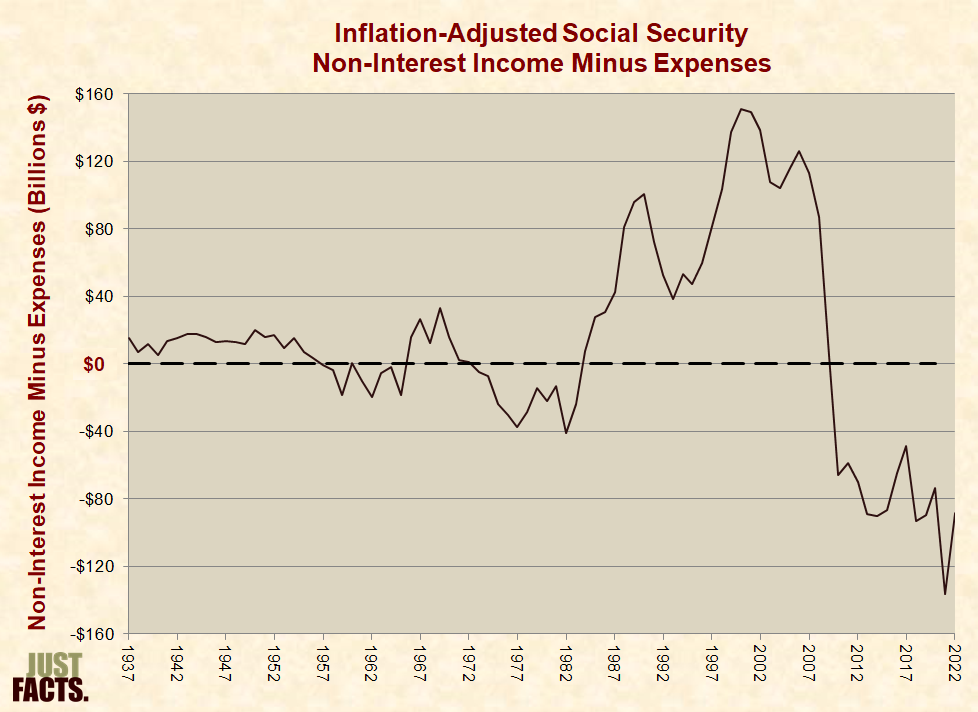

* From 1984 through 2009, Social Security’s non-interest income exceeded its expenses. In 2010, this situation reversed, and the program’s expenses began exceeding its non-interest income. This state of affairs continued through 2022 and is projected to continue every year into the foreseeable future:[140] [141]

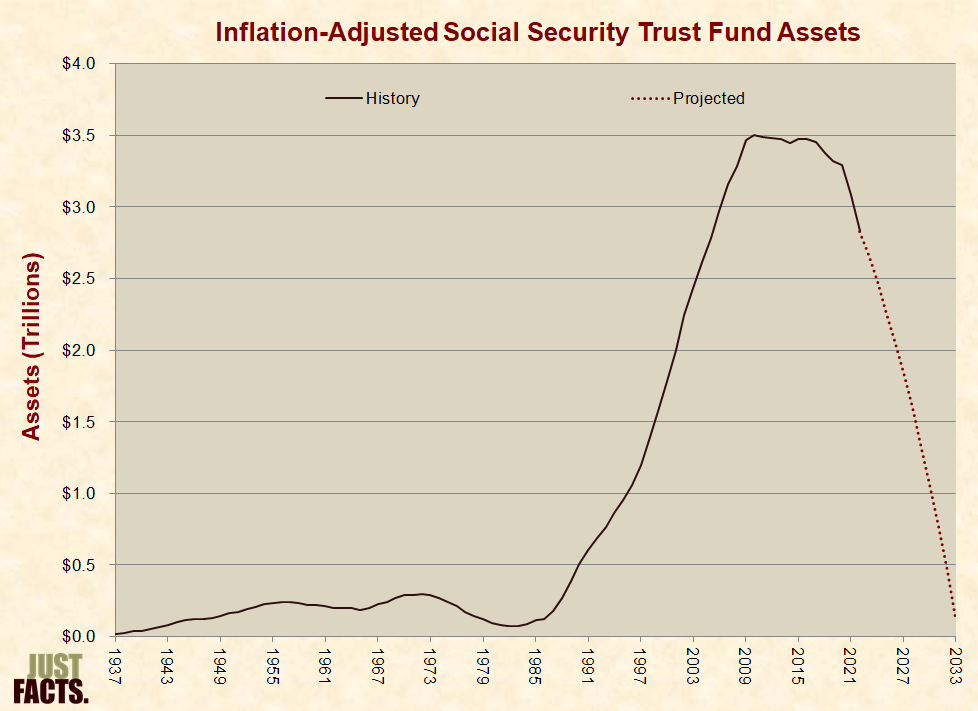

* Despite the interest payments that Social Security receives on the Trust Fund, the Trust Fund began declining in inflation-adjusted value in 2011.[143] [144] [145] [146] This decline began 10 years earlier than the Social Security Administration projected in 2010.[147]

* The Social Security Trust Fund continued to decline in 2012–2014, rose in 2015, and resumed declining in 2016.[148] This state of affairs is projected to continue until the Trust Fund is exhausted in 2034:[149]

* After 2033, Social Security is projected to run deficits every year into the foreseeable future.[151] To cover these deficits, payroll taxes would need to be increased by 25% starting in 2034, rising to a 35% increase by 2097.[152] These shortfalls could also be covered by reducing benefits by 19% starting in 2034, rising to a 25% reduction by 2097.[153]

* There are several other ways to quantify Social Security’s projected deficits. The measure commonly cited by the Social Security Administration and the press involves calculating how much money must be immediately added to the Trust Fund so that the principle and interest would cover projected shortfalls for the next 75 years.[154] [155] This is referred to as the “75-year open group unfunded obligation.” As of January 1, 2023, this amounts to:

* The U.S. Treasury’s “Financial Report of the United States Government” explains that Social Security’s 75-year open group unfunded obligation “understates the total financial needs by capturing relatively more of the revenues from current and future workers and not capturing all the benefits that are scheduled to be paid to them.”[160] A measure that accounts for these financial needs is called the “closed group unfunded obligation.” This measure:

* As of January 1, 2023, Social Security’s closed group unfunded obligation amounts to:

* Another way to quantify Social Security’s projected deficits is to calculate the total debt the program will accumulate if corrective action is not taken and money is borrowed to cover the shortfalls of the next 75 years. This debt (including interest) would amount to $103.6 trillion or an additional $434,842 (in 2023 dollars) for every person expected to be paying Social Security taxes in 2097.[173] [174]

* According to the Social Security Trustees report, relying too heavily on a 75-year projection “can lead to incorrect perceptions and to policy prescriptions that do not achieve sustainable solvency.” To address this shortcoming, the Trustees Report calculates how much money must be placed in the Social Security Trust Fund right now in order to finance projected deficits for the infinite horizon. This amounts to $65.9 trillion, which is comprised of $22.4 trillion to cover the shortfalls during 2022–2097 and another $43.4 trillion to cover the shortfalls for 2097 and beyond.[175]

* The Social Security Administration’s intermediate projections yield the following results:

|

Time Period |

Financial Status |

|

2023–2033 |

The Trust Fund declines in value every year. The federal government pays back the money that the Social Security program has loaned to it with interest, and the Trust Fund is depleted. |

|

2034–2097 |

The Social Security program runs deficits that accumulate to $103.6 trillion, which could be covered by (a) adding $22.4 trillion to the Trust Fund today, or (b) increasing payroll taxes by 25% starting in 2034, rising to a 35% increase by 2097, or (c) reducing benefits by 19% starting in 2034, rising to a 25% reduction by 2097. |

|

2098 and beyond |

The Social Security Program runs deficits that could be covered by adding $43.4 trillion to the Trust Fund today. |

* The primary cause of Social Security’s financial problems is a falling ratio of taxpayers to benefit recipients:[176]

* Three major factors contributing to the falling ratio of taxpayers to benefit recipients are:

1) increases in life expectancy without comparable increases in the retirement age:

2) the higher birth rate of the baby boom generation compared to other generations:

3) the increasing number of people receiving disability benefits:

|

Year |

Population in U.S. |

Number of People Receiving Disability Benefits |

|

1965 |

204,018,000 |

1,739,000 |

|

2023 |

335,997,000 |

8,842,000 |

* The Social Security Trustees Report states that the finances of the program depend upon:

* The report also states that “significant uncertainty” surrounds the “best estimates” of future circumstances.[194]

* The chart below compares Social Security’s yearly incomes to costs. The starting point of each curve is an actual outcome. The rest of each curve shows projections using data from various Trustees Reports.

* Examples from the chart above:

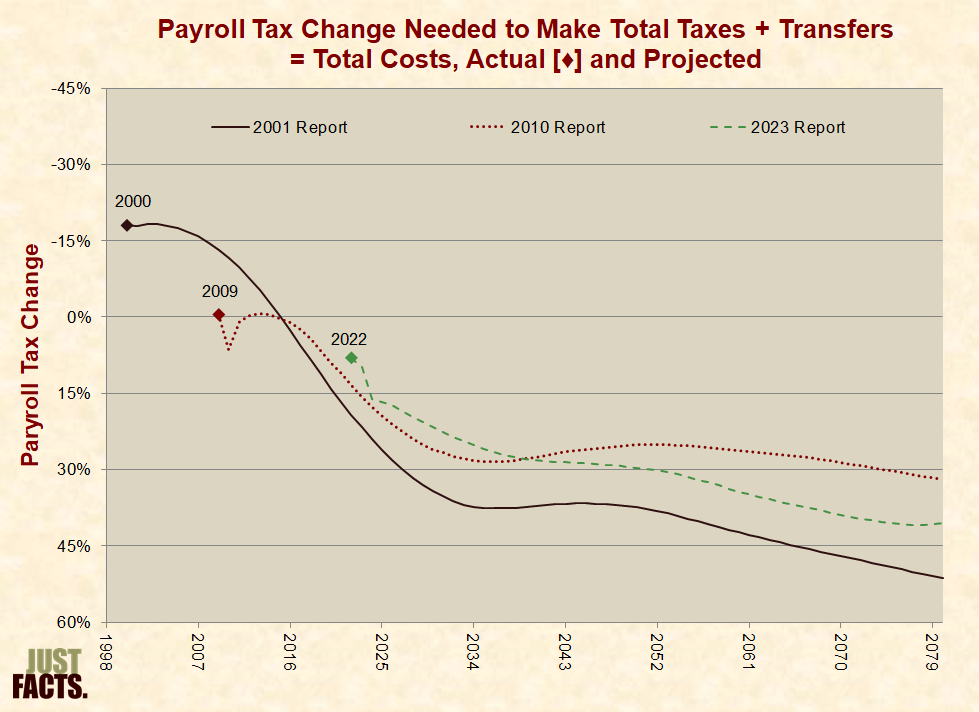

* The chart below shows how much Social Security payroll taxes would need to be decreased or increased to make total taxes plus transfers from the Treasury equal to the costs of the program. The starting point of each curve is an actual outcome, and the rest are based on projections. Note that the values on the vertical axis are inverted so that upward signifies improving finances, and downward signifies declining finances.

* Examples from the chart above:

* In 2012, the journal Demography published research that found the Social Security Administration is using an antiquated method to project life expectancies, and as a result, the program “may be in a considerably more precarious position than officially thought.”[197]

* From 1972 to 1976, the Social Security Trust Fund declined in value every year.[198] In 1977, the 95th U.S. Congress and Democratic President Jimmy Carter passed a bill that increased Social Security taxes and changed the formula governing benefit increases.[199] At the signing ceremony, Carter stated that this law was “the most important Social Security legislation since the program was established” and:

* The bill became law on December 20, 1977,[201] and the Trust Fund continued to decline every year for the next six years.[202] In 1983, the 98th U.S. Congress and Republican President Ronald Reagan increased Social Security taxes, raised the retirement age, and made other changes to help keep the program solvent.[203]

* Six days after the 2010 Social Security Trustees Report was published,[204] Nobel Prize-winning economist Paul Krugman wrote in his New York Times column that Social Security:

* In addition to “intermediate” projections predicting that the Trust Fund will be depleted in 2037, the 2010 Trustees Report included “high-cost” projections predicting that the Trust Fund will be depleted in 2029 and “low-cost” projections predicting that the program will “be able to cover cost for the foreseeable future.”[206]

* Regarding these projections, the report states:

* The report also states that:

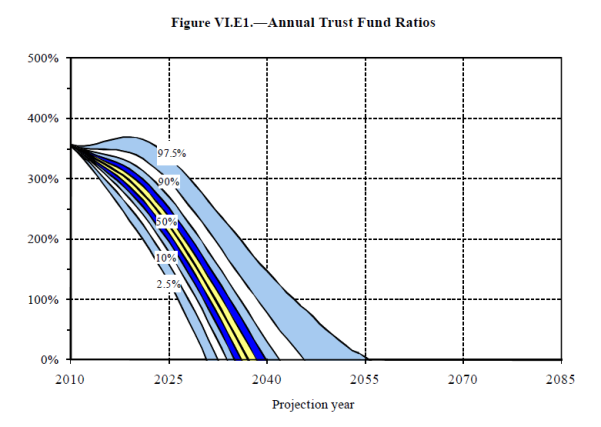

* In an appendix to this report, there is an analysis that “estimates a probability distribution of future outcomes” that “should be interpreted with caution and with an understanding of the inherent limitations.” According to this analysis, there is a 97.5% chance that the Trust Fund will be depleted no later than 2055 and the same chance that the Trust Fund won’t be depleted any earlier than 2030.[209]

* In 2022, the administrative costs of the Social Security program were $6.7 billion. This was equal to 0.54% of all Social Security outlays for the year, or enough to pay 307,699 retired workers the average annual old-age benefit of $21,924 for 2023.[210] [211]

* The figures above do not include the administrative costs borne by employers, which, according to Congressional Budget Office, are “probably substantial” but “difficult to assess.” The same report states that employers “bear the burden of the collection costs” of Social Security taxes and “are also responsible for transmitting substantial amounts of information to the SSA [Social Security Administration] and the IRS.”[212]

* From January 2004 to April 2007, the Social Security Administration made 44,000 corrections for instances in which it had falsely listed individuals as deceased. This required face-to-face interviews with each person and the processing of “resurrection transactions” to remove individuals from the “death master file.”[213]

* Under the 2009 American Recovery and Reinvestment Act (a.k.a., Obama “stimulus”), the Social Security Administration was required to administer the payment of $250 checks to Social Security and Supplemental Security Income beneficiaries. The Administration identified and certified about 52 million people as eligible for the checks, to whom the U.S. Treasury sent a total of $13 billion.[214]

* A 2010 report by the Inspector General of the Social Security Administration found that 71,688 of these checks (totaling $18 million) were sent to people who were deceased and thus ineligible to receive the payments. This included:

* A random audit of 50 such cases found that 26 of the payments had been returned. The stimulus act did not provide authority to reclaim payments issued to the deceased, and thus, the Social Security Administration or Treasury did not pursue collection of unreturned payments.[220]

* In 2022, Social Security made roughly $2.0 billion in improper overpayments. This was equal to 0.17% of all Social Security benefit payments for the year, or enough to pay 89,947 retired workers the average annual old-age benefit of $21,924 for 2023.[221] [222] [223]

* In 2009, President Obama issued Executive Order 13520 “to reduce improper payments by intensifying efforts to eliminate payment error.”[224] In 2010, Congress passed and Obama signed the Improper Payments Elimination and Recovery Act. This law requires federal agencies to report on their actions to reduce and recover improper payments and meet targeted payment accuracy rates.[225] [226]

* Per a 2016 report by the Social Security Administration’s Office of the Inspector General [OIG]:

* Once the Social Security Administration mistakenly overpays a beneficiary for more than four years, it does not recover past overpayments and deliberately continues to make future overpayments, except in cases of fraud.[228] [229] This policy is called “administrative finality,” and it is governed by regulations issued by the Commissioner of Social Security,[230] who is appointed by the U.S. President once every six years.[231]

* In 2007, the Inspector General of the Social Security Administration released the results of an audit that found 77,969 Social Security beneficiaries “whose benefit records indicated that administrative finality was involved.”[232]

* In a random sample of 275 of these beneficiaries,[233] the investigators found that:

* Based on the overpayment amounts of this survey group, the Office of the Inspector General estimated that as of June 2005, 44,230 active beneficiaries had their benefits:

* In the “Conclusion and Recommendation” section of its report, the Inspector General wrote that Social Security:

* The Commissioner of Social Security rejected this suggestion and responded in part:

* In 2012, an audit by the Inspector General of the Social Security Administration recommended that the Social Security Administration “evaluate its administrative finality policies and regulations and consider revising the rules to allow for the collection of more debt.” The Social Security Administration responded, “We agree.”[238]

* As of September 2023, the Social Security Administration’s regulations on administrative finality continue to require overpayments if an error is not corrected within four years.[239] [240]

* In 2010, the Government Accountability Office released the results of an investigation of federal employees and commercial drivers who were receiving disability benefits administered by the Social Security Administration [SSA].[241] The investigators reported that:

* Out of the cases identified above, the Government Accountability Office selected and investigated a nonrandom sample of 20 individuals based upon factors such as “higher overpayment amounts, the types of employment, and the locations of employment.”[246] The investigators found that:

* A common perception about Social Security benefits is:

* Social Security is mainly a “pay-as-you-go” program, which means that it pays most of its benefits by taxing people who are currently working.[256] [257] [258] Per the Social Security Administration:

* From the start of the Social Security program in 1937 through the end of 2022:

* Per the Social Security Administration:

* After the federal government pays back with interest all of the money it has borrowed from Social Security, the program’s current claim against the earnings of future generations is $48.4 trillion.[262] [263] This is larger than the national debt and amounts to an average of $196,731 for every person now receiving Social Security benefits or paying Social Security payroll taxes.[264] [265]

* Per the Social Security Administration:

* In 1960, the U.S. Supreme Court ruled (5 to 4) that entitlement to Social Security benefits is not a contractual right.[267]

* A common perception about Social Security finances is:

* No money has been taken from the Social Security program.[272] [273] [274] By law, Social Security surpluses must be loaned to the federal government.[275] [276] [277] This requirement was established in the original Social Security Act of 1935.[278] [279] [280] [281]

* The federal government is legally required to pay back with interest all money it has borrowed from Social Security, and it has never failed to do so throughout the program’s history.[282] [283] [284]

* Since 2010, Social Security has been using interest received from the federal government to cover the shortfalls between its expenses and non-interest income:

* The assets of the Social Security program include all of the money it has loaned to the federal government.[287] [288] After this money is fully repaid with interest, the program’s trustees project that the:

* If congresses and presidents had not added extra money to the Social Security program by increasing its payroll tax rates above the levels specified in the original Social Security Act, the program would have become insolvent before 1980.[291]

* All finances of the Social Security program are conducted through two dedicated trust funds in the U.S. Treasury: one for the old-age program and another for the disability program.[292]

* When Social Security collects more in taxes than it spends, it generates surplus money. By law, the only thing the program can do with its surplus money is loan it to the federal government.[293] [294] This has been the law since the original Social Security Act of 1935 and has not changed since then.[295] [296] [297] (For facts about the common claim that Social Security has been looted, click here.)

* Federal law requires the government to pay back any money it borrows from Social Security with interest. This money becomes a part of the national debt.[298] [299] [300] [301]

* Increases in the national debt are mainly borne by future workers and taxpayers.[302] [303]

* The national debt and interest on it are paid back with taxes from the general fund of the U.S. Treasury—not taxes that are restricted by law to fund specific programs like Social Security.[304] [305]

* Overall, general fund taxes are progressive so that higher-income households pay higher effective tax rates.[306] [307] [308] [309] [310] [311] These taxes are comprised of:

* The U.S. Treasury Department publishes a “Monthly Statement of the Public Debt” that details the components of the national debt, including the amounts owed to the Social Security program.[313]

* At the end of 2022, the U.S. government owed $2.8 trillion to the Social Security Trust Fund.[314] This equates to $8,470 for every man, woman, and child living in the United States, or $21,569 per household.[315]

* The Social Security program began drawing money from the Trust Fund in 2010 and is projected to keep drawing this money every year until the Fund is exhausted in 2034.[316] [317] [318]

* The U.S. Government Accountability Office explains that the Social Security Trust Fund represents “a claim on future resources” that must be funded “either through increased taxes, spending cuts, increased borrowing from the public, retiring less debt (if the unified budget is in surplus), or some combination thereof.”[319]

* The Clinton administration’s 2000 budget proposal explains that the Social Security Trust Fund does:

* A Congressional Budget Office report on “Debt and Interest Costs” explains that the money needed to pay back the Social Security Trust Fund:

* At the close of the federal government’s 2022 fiscal year, the federal government had $135.5 trillion in debts, liabilities, and unfunded obligations. This shortfall equates to $405,882 for every person living in the United States, or $1,032,660 per household.[322]

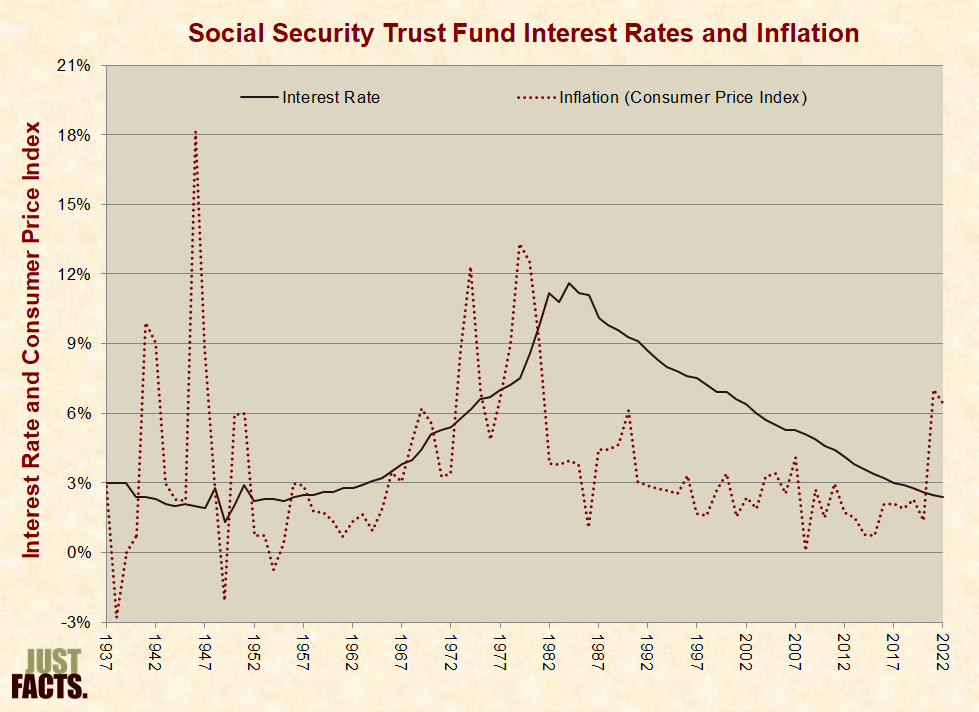

* From the outset of Social Security in 1937 through 2022, the U.S. government paid an annual average interest rate of 5.1% on the debt that it owed to Social Security. During this period, annual inflation as measured by the Consumer Price Index averaged 3.7%:

* The interest rates on the Social Security Trust Fund are driven by the same factors that affect the interest rates on other government debt.[325] These include but are not limited to inflation, economic growth, Federal Reserve policies, and investors’ assessments of risks and rewards.[326]

* The interest rates on the Social Security Trust Fund are determined by the average interest rates on long-term government debt. This applies regardless of whether Social Security holds short-term or long-term debt.[327]

* Because long-term debts generally have higher interest rates than short-term debts, the interest rates received by Social Security tend to be higher than interest rates on other government debt.[328] [329] [330] [331]

* The Social Security Trust Fund starts all new investments as short-term debt scheduled to mature on the upcoming June 30th. On June 30th, the matured debt and its interest are rolled into new debts of different maturities ranging from 1 to 15 years.[332] [333]

* Regardless of the maturity of a debt, Social Security can demand repayment with interest at any time if it needs money to cover expenses. This feature makes the Social Security Trust Fund similar to cash from a liquidity perspective.[334] [335] [336]

* The money that the federal government owes to Social Security is held in the form of securities issued by the United States Treasury. These securities are analogous to U.S. savings bonds, except that they can be redeemed before maturity without suffering a loss or enjoying a gain due to market forces. These securities cannot be purchased by the general public.[337]

* Bonds that represent the debt that the U.S. government owes to Social Security are located in a file cabinet at the Bureau of the Fiscal Service in Parkersburg, West Virginia. Below is a photo of President George W. Bush inspecting the documents along with Susan Chapman of the Office of Public Debt Accounting.[338] [339]

* The federal government divides the national debt into two main categories:[340]

* At the close of the federal government’s 2022 fiscal year,[345] the $30.9 trillion national debt was comprised of:

* The federal law that governs the repayment of the national debt draws no distinction between publicly held debt and intergovernmental debt. Both must be repaid with interest.[347]

* When the Social Security program loans money to the U.S. government, the government can use this money to pay down the debt that it owes to other entities. This leaves the national debt unchanged because the government must still pay back this money to the Social Security program. Some politicians have referred to this action as, “putting Social Security into a lockbox.”[348] [349]

* When the Social Security program loans money to the U.S. government, the government can also spend this money on other government programs. This increases the national debt because the government has spent the money it has borrowed from Social Security. Some politicians have referred to this action as, “raiding the Social Security Trust Fund.”[350] [351]

* When the U.S. government takes either of the above actions, the finances of the Social Security program are not affected. In both cases, the law requires the government to pay back the money to the Social Security program with interest.[352] [353]

* The impact of one action as opposed to the other is whether or not the national debt increases.[354] [355] [356] The national debt is not paid for with Social Security taxes but with money from the general fund of the U.S. Treasury.[357] [358] [359]

* In 1999, Republican Congressman Wally Herger sponsored a “lockbox” bill in the House of Representatives. This legislation would have restricted Congress from using money borrowed from the Social Security program to spend on other government programs.[360] It passed the House by a vote of 416 to 12.[361]

* In the Senate, Republicans attempted to bring this bill up for a vote, and Democrats blocked it with a filibuster. All 55 Republicans voted to allow the bill to move forward, 44 Democrats voted to block the bill, and one Democrat did not vote.[362] [363] [364]

* During his 2000 presidential campaign, Democratic nominee Al Gore stated:

* Regarding this statement:

* In 2001, while addressing Congress, Republican President George W. Bush stated:

* The $2 trillion in debt that President Bush referred to in this statement excluded the debt that is owed to federal entities such as Social Security.[377]

* Bush did not include the following information in his speech to Congress that appeared on page 201 of his budget proposal:

* The Social Security Administration states:

* At the outset of the Social Security program, the federal government published an informational pamphlet that stated the following with regard to Social Security benefits:

* Three years later in 1939, Congress and Democratic President Franklin D. Roosevelt eliminated a lump-sum benefit payment for the survivors of workers who died before the age of 65.[382]

* The original Social Security Act of 1935 states:

* The Social Security Administration’s website states:

* For those planning to collect Social Security after 2034, the program’s trustees project that the Trust Fund will be depleted and all benefits will be paid solely by workers who pay Social Security taxes at that time.[385] [386] It is also projected that Social Security taxes will be sufficient to pay 81% of scheduled benefits at that time.[387]

* Proposals have been made to give workers the option to change part of their Social Security involvement from a benefit program to a savings plan. These savings would be the personal property of each person who chose to participate. In turn, their Social Security benefits would be reduced to correspond with the amount of taxes they paid to the program.[388]

* Proposals to give Social Security an element of personal ownership are generally structured to improve the program’s finances. Typically, there are transition costs to cover the lowered taxes of those who opt to have personal accounts, but these costs are more than offset by the savings of not paying these individuals full benefits. For example, a proposal made in 2008 would eliminate $4.3 trillion in deficits but add $4.1 trillion in transition costs, thus equating to about $200 billion in savings.[389] [390]

* A scientific, nationally representative survey commissioned in 2019 by Just Facts found that 70% of voters believe personal ownership plans generally harm the finances of the Social Security program.[391] [392]

* To restrict speculation, personal ownership plans typically regulate the types of investments that can be made. Examples include restricting investments to broad-based funds or requiring that assets be moved to lower-risk investments as individuals approach retirement age. For instance, a personal ownership bill introduced by Republican Senator Jim DeMint restricts investments to federal bonds and private investment funds similar to those in the federal Thrift Savings Plan (described next).[393] [394] [395]

* Federal employees have access to a program called the Thrift Savings Plan in which the federal government and its employees invest part of their compensation in funds with varying mixes of investments.[396] At the end of 2022, approximately 6.8 million federal employees were enrolled,[397] and the plan had $737 billion in net assets.[398] This program has the following attributes:

* From 1926 through 2022, large company stocks (i.e., the S&P 500) appreciated by an average of 7.0% per year above the rate of inflation.[404] This figure is called the total annual real geometric mean return (hereafter referred to as “annual real return”).[405] From 1926 through 2022, the lowest annual real return for any 45-year period in the S&P 500 was 4.6%, and the highest was 8.7%.[406]

* For other classes of investments, the annual real returns from 1926 through 2022 were as follows:

|

Investment |

Average |

Lowest of Any 45-Year Period |

Highest of Any 45-Year Period |

|

Small Company Stocks |

8.6% |

6.8% |

12.8% |

|

Long-Term Corporate Bonds |

2.7% |

–1.5% |

5.2% |

|

Long-Term Government Bonds |

2.1% |

–1.8% |

4.9% |

|

Intermediate-Term Government Bonds |

1.9% |

–0.7% |

3.3% |

|

U.S. Treasury Bills |

0.3% |

–1.1% |

1.4% |

* The administrative costs associated with pension plans include “collecting funds, keeping records, managing assets, calculating and paying benefits, overseeing and enforcing rules, and (in some cases) marketing and selling the plans.”[409] [410]

* Factors affecting administrative costs include the number of individual accounts, the variety of services provided, the range of investments from which individuals are able to choose, the degree to which the system is centralized, and the amount of competition involved.[411] [412]

* Administrative overhead in pension systems is often expressed in terms of annual administrative costs divided by total assets.[413] [414] Hence, for a personal ownership system with annual administrative costs of $5 billion and total assets of $1 trillion, the annual administrative overhead would be $5/$1,000 or 0.50%.[415]

* In the context of Social Security personal ownership proposals, total administrative costs are typically unaffected by account balances. This is because the administrative cost per account is about the same, regardless of its value. Thus, proposals that allow individuals to save more of their payroll taxes generally have lower administrative costs as a percentage of assets.[416] [417] [418]

* In 2003, the chief actuary of the Social Security Administration estimated that the annual administrative costs of a personal ownership proposal that would allow individuals to save half of their payroll taxes would be about 0.25% of assets.[419]

* In 2004, Democratic Congressman Charles Stenholm and Republican Congressman Jim Kolbe introduced a personal ownership bill that would require individuals to save 19% of their payroll taxes. This bill duplicates features of the personal accounts in the federal Thrift Savings Plan,[420] [421] which in 2022 had total administrative costs ranging from 0.057% to 0.090% of assets.[422] [423] [424]

* Under the current system, a 22-year-old who works for the next 45 years earning $50,000/year will pay $279,000 in taxes to Social Security.[425] The program’s trustees project that all of this money will be spent before she turns 67 years old. Hence, any old-age benefits she receives will be derived from taxpayers who contribute to Social Security at that time.[426] [427]

* If this same person were allowed to save and invest 25% of her payroll taxes in the S&P 500, and the rates of return and administrative costs varied based upon the facts above, she would accumulate the following assets:

|

Scenario |

Annual Real Return (%) |

Administrative Costs (%) |

Assets by Age 67 |

|

“Bad” |

4.6% |

0.50% |

$198,957 |

|

“Average” |

7.0% |

0.25% |

$435,028 |

|

“Good” |

8.7% |

0.12% |

$764,314 |

* If this same person were allowed to save and invest 50% of her payroll taxes in the S&P 500, and the rates of return and administrative costs varied based upon the facts above, she would accumulate the following assets:

|

Scenario |

Annual Real Return (%) |

Administrative Costs (%) |

Assets by Age 67 |

|

“Bad” |

4.6% |

0.25% |

$428,049 |

|

“Average” |

7.0% |

0.12% |

$907,667 |

|

“Good” |

8.7% |

0.06% |

$1,560,468 |

* If this same person were allowed to save and invest 75% of her payroll taxes in the S&P 500 for the first 30 years and then progressively move all of these assets into intermediate-term government bonds over the last 15 years, and the rates of return and administrative costs varied based upon the facts above, she would accumulate the following assets:

|

Scenario |

S&P 500 Annual Real Return (%) |

Bonds Annual Real Return (%) |

Administrative Costs (%) |

Assets by Age 67 |

|

“Bad” |

4.6% |

–0.7% |

0.12% |

$451,836 |

|

“Average” |

7.0% |

1.9% |

0.08% |

$946,105 |

|

“Good” |

8.7% |

3.3% |

0.03% |

$1,596,842 |

* In general, for Social Security participants who are single and have no children under the age of 20, their benefits (or projected benefits) terminate when they die regardless of how much they have paid in Social Security taxes. There is no heritability in these cases except for a one-time death payment of $255 under certain circumstances.[431] [432] [433] [434]

* For workers who are currently 40 years old, their full retirement age is 67.[435] Their life expectancies beyond this age vary from 15.5 for Hispanic females to 5.0 for black males:

|

Race/Sex |

Years of Expected Life Beyond the Age of 67 |

|

Hispanic females |

15.5 |

|

White females |

13.8 |

|

Black females |

10.7 |

|

Hispanic males |

10.3 |

|

White males |

9.5 |

|

Black males |

5.0 |

* Personal ownership allows individuals to pass their Social Security savings to their heirs upon death.[437]

* During 2007–2010, various members of Congress introduced at least three bills that would have given workers the option to save and invest a portion of their Social Security payroll taxes. They also introduced a bill that would have made this mandatory for all workers below 66 years of age and another bill that would have made this optional for workers aged 22–54 and mandatory for younger workers. All of these bills were sponsored by Republicans. No Congressional action was taken on any of them.[438] [439]

* The 2008 and 2012 Republican Party Platforms supported giving workers “control over, and a sound return on” their Social Security contributions.[440] [441] The Republican Party 2016 Platform states that “we oppose tax increases and believe in the power of markets to create wealth and to help secure the future of our Social Security system.”[442] The Republican Party didn’t adopt a new platform in 2020.[443]

* The 2008, 2012, and 2016 Democratic Party Platforms opposed “privatization” of Social Security.[444] [445] [446] The 2020 Democratic Party Platform states that “Democrats will reject every effort to cut, privatize, or weaken Social Security, including attempts to raise the retirement age, diminish benefits by cutting cost-of-living adjustments, or reduce earned benefits.”[447]

* Since 1980, at least 27 countries have added an element of personal ownership to their Social Security systems.[448] The image below shows these nations and years when they adopted these reforms. This interactive website provides an overview of the system in each of these countries:

* At a news conference on March 16, 2005, NBC reporter David Gregory said to President George W. Bush:

* On the day before this news conference, the Washington Post released the results of a poll that included the following question:

* The poll found that 56% of Americans supported this plan, 41% opposed it, and 3% had no opinion.[452] In eight previous Washington Post polls in which this question was asked, the range of support varied from 52% to 64%.[453]

* The Washington Post summarized the results of its latest poll in a front-page article entitled “Skepticism of Bush’s Social Security Plan Is Growing.” The article, written by Jonathan Weisman, did not report the results of the question above.[454]

* In February 2001, the New York Times published an article written by Robert Pear entitled:

* The article stated:

* This study compared the disability benefits produced by several personal ownership proposals to the disability benefits specified by current law. To pay the disability benefits specified by current law, the Social Security tax rate needed to be increased over time by 49%.[457]

* This information appeared on page 44 of the General Accounting Office study and nowhere in the New York Times article.[458] [459]

* When this study compared the personal ownership proposals to the current Social Security system using the same tax rate for both plans, in the majority of cases, the personal ownership systems produced higher disability benefits than the current Social Security system.[460]

* This information appeared on page 36 of the General Accounting Office study and nowhere in the New York Times article.[461] [462]

* The New York Times article also stated that George W. Bush “has championed the rights of people with disabilities,” yet he “wants to let workers put some of their Social Security payroll taxes into personal investment accounts,” which “would reduce benefits for people with disabilities.”[463]

* Bush’s then-current plan did not propose any changes to the disability component of Social Security.[464] When Bush’s Social Security commission released a formal report later that year, it stated:

* Starting in 1946, Social Security cards had the following sentence imprinted on them:

* In 1961, the Social Security Administration issued new Social Security cards attached to a pamphlet that stated:

* Since 1961, various Congresses and presidential administrations have enacted more than 40 laws, regulations, and policies requiring the use of Social Security numbers for identity-related functions.[468]

* Starting in 1972, the sentence reading “For Social Security Purposes—Not For Identification” was removed from all newly issued Social Security cards.[469]

* In 1994, Democratic Congressman Dick Gephardt sponsored a law called the “Uruguay Round Agreements Act” that passed Congress with 67% of Democrats and 70% of Republicans voting for it. Democratic President Bill Clinton signed it into law. This legislation contains a section entitled:

* The law requires that parents submit Social Security numbers for their children with their tax return in order to obtain a tax exemption for their children.[471]

* Per the U.S. Social Security Administration:

[1] “2023 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, March 28, 2023. <www.ssa.gov>

[2] Textbook: Cost Accounting: Principles And Practice. By Manash Dutta. Pearson Education, 2004.

Page 23.2: “Inflation accounting presents a true and correct view of the financial state of affairs of a firm, leads to the maintenance of physical capital and enables the business entity to make rational financial decisions.”

[3] Book: Quantitative Investing for the Global Markets: Strategies, Tactics, and Advanced Analytical Techniques. Edited by Peter Carman. Fitzroy Dearborn Publishers, 1997.

Pages 25–26: “World stock and bond markets can be expected to continue to grow, although not at the explosive pace of the past few decades. Some of the past growth has been due to rises in nominal asset prices that merely compensate for inflation; such rises are likely to be at lower rates in the future. But we should be concerned not with nominal quantities but with real [inflation-adjusted] ones.”

[4] “2023 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, March 28, 2023. <www.ssa.gov>

Page 9:

The Trustees set key demographic, economic, and programmatic assumptions for three alternative scenarios. The intermediate assumptions reflect the Trustees’ best estimates of future experience. Therefore, most of the results presented in this overview indicate outcomes under the intermediate assumptions only. Any projection of the future is, of course, uncertain. For this reason, results are also presented under low-cost and high-cost alternatives to provide a range of possible future experience. The actual future costs are unlikely to be as extreme as those portrayed by the low-cost or high-cost projections.

Page 19: “Uncertainty of the Projections … Significant uncertainty surrounds the intermediate assumptions.”

[5] Webpage: “The Social Security Act of 1935.” United States Social Security Administration. Accessed September 16, 2021 at <www.ssa.gov>

The Social Security Act (Act of August 14, 1935) [House Resolution 7260]

An act to provide for the general welfare by establishing a system of Federal old-age benefits, and by enabling the several States to make more adequate provision for aged persons, blind persons, dependent and crippled children, maternal and child welfare, public health, and the administration of their unemployment compensation laws; to establish a Social Security Board; to raise revenue; and for other purposes.

[6] Report: “Major Decisions in the House and Senate on Social Security.” By Geoffrey Kollmann and Carmen Solomon-Fears. Domestic Social Policy Division, U.S. Social Security Administration, March 26, 2001. <www.ssa.gov>

H.R. [House Resolution] 7225, the Social Security Amendments of 1956, was signed by President Eisenhower on August 1, 1956. The amendments provided benefits, after a 6-month waiting period, for permanently and totally disabled workers aged 50 to 64 who were fully insured and had at least 5 years of coverage in the 10-year period before becoming disabled; to a dependent child 18 and older of a deceased or retired insured worker if the child became disabled before age 18; to women workers and wives at the age of 62, instead of 65, with actuarially reduced benefits; reduced from 65 to 62 the age at which benefits were payable to widows or parents, with no reduction; extended coverage to lawyers, dentists, veterinarians, optometrists, and all other self-employed professionals except doctors99 increased the tax rate by 0.25% on employer and employee each (0.375% for self-employed people) to finance disability benefits (thereby raising the aggregate tax rate ultimately to 4.25%); and created a separate disability insurance (DI) trust fund. The Social Security program now consisted of old-age, survivors, and disability insurance (OASDI).

[7] “2008 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, March 28, 2008. <www.ssa.gov>

Page 131:

The Federal Old-Age and Survivors Insurance (OASI) Trust Fund was established on January 1, 1940 as a separate account in the United States Treasury. The Federal Disability Insurance (DI) Trust Fund, another separate account in the United States Treasury, was established on August 1, 1956. All the financial operations of the OASI and DI programs are handled through these respective funds.

[8] Report: “Social Security Policy Options.” Congressional Budget Office, July 2010. <www.cbo.gov>

Page 3:

Revenues from payroll taxes and from taxes on benefits, along with intragovernmental interest payments, are credited to the two Social Security trust funds—one for OASI [Old-Age and Survivor’s Insurance] and one for DI [Disability Insurance]. The program’s benefits and administrative costs are paid from those funds. Legally, the two funds are separate, but they often are described collectively as the OASDI trust funds.

[9] Report: “Charting the Future of Social Security’s Disability Programs: The Need for Fundamental Change.” Social Security Advisory Board, January 2001. <www.ssab.gov>

Page 2 (of PDF): “[The] Social Security Advisory Board [is] an independent, bipartisan Board created by the Congress and appointed by the President and the Congress to advise the President, the Congress, and the Commissioner of Social Security on matters related to the Social Security and Supplemental Security Income programs.”

Page ii: “Supplemental Security Income (SSI) is a means-tested income assistance program for aged, blind, and disabled individuals (regardless of prior workforce participation) and is funded from general revenues of the Treasury.”

[10] Calculated with data from:

a) “2023 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, March 28, 2023. <www.ssa.gov>

Pages 63–64: “Table IV.B3.—Covered Workers and Beneficiaries, Calendar Years 1945–2100 … Historical data: … 2022 Beneficiariesb (in thousands) … OASDIc [=] 65,614 … b Beneficiaries with monthly benefits in current-payment status as of June 30. c This column is the sum of OASI [Old-Age & Survivors Insurance] and DI [Disability Insurance] beneficiaries. A small number of beneficiaries receive benefits from both funds.”

b) Dataset: “Monthly Population Estimates for the United States: April 1, 2020 to December 1, 2023.” U.S. Census Bureau, Population Division, December 2022. <www2.census.gov>

“Resident Population … June 1, 2022 [=] 333,133,413”

CALCULATION: 65,614,000 beneficiaries / 333,133,413 people = 20%

[11] Report: “Summary of Major Changes in the Social Security Cash Benefits Program: 1935–1996.” By Geoffrey Kollmann. Library of Congress, Congressional Research Service. Updated December 20, 1996. <www.ssa.gov>

Pages 1–2: “The Social Security Act of 1935 … Nearly all workers in commerce and industry under age 65, or about 60% of the work force, were required to participate in the Old-Age Insurance program. Principal groups excluded from the program were government workers, railroad employees, the self-employed, farm and domestic workers, and employees of nonprofit organizations.”

Page 4:

1950 Amendments

The 1950 amendments substantially expanded the scope of the Old-Age and Survivors Insurance (OASI) program by extending coverage to about 10 million additional workers. …

• Covered regularly employed farm and domestic workers, self-employed workers (except farmers and professionals), federal civilian employees not under a federal civil service retirement system ([for example] temporary employees), Americans employed outside the United States by American employers, and workers in Puerto Rico and the Virgin Islands. Not-for-profit organizations could elect coverage for their employees (except ministers). State and local governments could elect coverage for their employees not under public employee retirement systems.

Pages 16–17:

1983 Amendments …

• Coverage of federal civilian employees hired after December 31, 1983, and most current executive level political appointees and elected officials (including Members of Congress, the President, and the Vice President) and Federal judges, effective January 1984.

• Compulsory coverage of all employees of nonprofit organizations effective in January 1984 and a ban on the termination of coverage of nonprofit organization and state and local government employment after 1982.

[12] Report: “Annual Statistical Supplement to the Social Security Bulletin, 2013.” Social Security Administration, Office of Research, Evaluation, and Statistics, February 2014. <www.ssa.gov>

NOTE: Table 2.A1 in this report provides detailed information on “Covered Employment and Self-Employment Provisions, by Year Enacted.” This table is available at <www.ssa.gov>

[13] Report: “Reducing the Deficit: Spending and Revenue Options.” Congressional Budget Office, March 2011. <www.cbo.gov>

Page 171: “Unlike nearly all private-sector workers and federal employees, some workers employed by state and local governments—about 25 percent—are not covered by Social Security.”

[14] Article: “The Illusion of Pension Savings.” By Mary Williams Walsh. New York Times, September 17, 2010. <www.nytimes.com>

“Illinois’s pension funds are more fragile than most, but their survival is essential to thousands of people. The state’s teachers and certain other workers do not participate in Social Security, so for them, the pension fund is their only source of retirement income.”

[15] Webpage: “Social Security Coverage.” National Association of State Retirement Administrators. Accessed August 15, 2023 at <www.nasra.org>

Approximately one-fourth of employees of state and local government participate in a public retirement system in lieu of Social Security. This includes approximately 40 percent of public school teachers and over two-thirds of firefighters, police officers, and other first responders. Every state has groups of public employees that do not participate in Social Security. Most to substantially all of the public employees in Alaska, Colorado, Louisiana, Maine, Massachusetts, Nevada, and Ohio are not in Social Security.

[16] Webpage: “Are Members of Religious Groups Exempt From Paying Social Security Taxes?” United States Social Security Administration. Last modified October 7, 2022. <faq.ssa.gov>

Members of certain religious groups (including the Amish and Mennonites) may be exempt from paying Social Security taxes. To become exempt, they must:

• Waive their rights to all benefits under the Social Security Act, including hospital insurance benefits; and

• Meet the following requirements:

• Be a member of a recognized religious sect conscientiously opposed to accepting benefits under a private plan or system that makes payments in the event of death, disability or retirement, or which makes payments towards the costs of or provides for medical care (including the benefits of any insurance system established by social security);

• Be a member of a religious sect that makes a reasonable provision of food, shelter and medical care for its dependent members and has done so continuously since December 31, 1950; and

• Have never received or been entitled to any benefits payable under Social Security programs.

[17] Article: “The Great Depression and Wall Street Crash.” By Quentin R. Skrabec Jr. Economics: The Definitive Encyclopedia from Theory to Practice. Edited by David A. Dieterle. Greenwood, March 2017. Pages 192–195.

Page 194: “Today Social Security stands as the largest government program in the world and the single greatest expenditure in the U.S. federal budget.”

[18] Calculated with data from:

a) Dataset: “Table 3.16. Government Current Expenditures by Function [Billions of Dollars].” U.S. Department of Commerce, Bureau of Economic Analysis. Last revised November 17, 2023. <apps.bea.gov>

b) Report: “Fiscal Year 2024 Historical Tables: Budget Of The U.S. Government.” White House Office of Management and Budget, March 2023. <www.whitehouse.gov>

“Table 3.1—Outlays by Superfunction and Function: 1940–2028.” <www.whitehouse.gov>

NOTES:

[19] “2010 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, August 5, 2010. <www.ssa.gov>

Page 216: “Payroll Taxes. A tax levied on the gross wages of workers.”

[20] Article: “Payroll Tax, Federal.” By Edward W. Harris. Encyclopedia of Taxation & Tax Policy (2nd edition). Edited by Joseph J. Cordes and others. Urban Institute Press, 2005. Pages 293–295.

Page 293:

A group of taxes levied on the earnings of employees and self-employed persons.

Payroll taxes have grown substantially in past decades and are now the second largest source of federal revenues. As a share of total receipts, payroll taxes increased from 10 percent in 1937 to 40 percent in 2003. Over the same period, payroll taxes grew from 1 percent to almost 7 percent of gross domestic product.

Page 295:

Incidence of Federal Payroll Taxes

Unemployment taxes are statutorily levied on employers only, while Social Security and Medicare taxes are levied on both the employer and the employee. Economists generally believe that the burden of payroll taxes is borne by workers in the form of lower wages, regardless of whether the tax is levied on the employer or the employee.

Payroll taxes are less progressive than individual income taxes because payroll taxes tax only earned income, and most payroll taxes include a maximum taxable earnings base. Effective or average federal payroll taxes rates increase across the bottom of the income distribution, since the lowest-income people generally have little income from wages. Average rates are virtually flat across the broad middle of the income distribution and decline at the top of the income scale, where people often have earnings above the taxable level. (Including both payroll taxes and the benefits financed by those taxes would show a more progressive system.) In an effort to increase the progressivity of payroll taxes and to create incentive to entering the labor force, the earned income tax credit (EITC) was introduced in 1975 to lighten the burden on working people below certain incomes. Since then, the EITC has been expanded several times, including the Omnibus Budget Reconciliation Acts in 1990 and 1993.

[21] Calculated with data from:

a) Dataset: “Old-Age and Survivors Insurance Trust Fund, 1937–2022.” United States Social Security Administration, Office of the Chief Actuary. Accessed August 15, 2023 at <www.ssa.gov>

b) Dataset: “Disability Insurance Trust Fund, 1957–2022.” United States Social Security Administration, Office of the Chief Actuary. Accessed August 15, 2023 at <www.ssa.gov>

c) Dataset: “CPI—All Urban Consumers (Current Series).” U.S. Department of Labor, Bureau of Labor Statistics. Accessed January 27, 2023 at <www.bls.gov>

“Series Id: CUUR0000SA0; Series Title: All Items in U.S. City Average, All Urban Consumers, Not Seasonally Adjusted; Area: U.S. City Average; Item: All Items; Base Period: 1982–84=100”

NOTES:

[22] Report: “Overview of the Federal Tax System as in Effect for 2014.” U.S. Congress, Joint Committee on Taxation, March 28, 2014. <www.jct.gov>

Page 25:

Social Security benefits and certain Medicare benefits are financed primarily by payroll taxes on covered wages. The Federal Insurance Contributions Act (“FICA”) imposes tax on employers and employees based on the amount of wages paid to an employee during the year. The tax imposed is composed of two parts: (1) the old age, survivors, and disability insurance (“OASDI”) tax equal to 6.2 percent of covered wages up to the taxable wage base ($142,800 in 2021); and (2) the Medicare hospital insurance (“HI”) tax amount equal to 1.45 percent of covered wages with no wage cap.92 In addition to the tax on employers, each employee’s wages are subject to FICA taxes equal to the amount of tax imposed on the employer. The employee FICA taxes generally must be withheld and, along with employer FICA taxes, remitted to the Federal government by the employer.93 …

As a parallel to FICA taxes, the Self-Employment Contributions Act (“SECA”) imposes taxes on the net income from self-employment of self-employed individuals. The rate of the OASDI portion of SECA taxes is equal to the combined employee and employer OASDI tax rates and applies to self-employment income up to the FICA taxable wage base. Similarly, the rate of the HI portion is the sum of the combined employer and employee HI rates, and there is no cap on the amount of self-employment income to which the rate applies.94

92 FICA taxes also includes an additional hospital insurance tax. Sec. 3101(b)(2).

93 Instead of FICA taxes, railroad employers, employees, and employee representatives are subject, under the Railroad Retirement Tax Act (“RRTA”), to taxes equivalent to the OASDI and HI taxes under FICA. Under RRTA, employers and employees are also subject to an additional tax, referred to as the “tier 2” tax, on compensation up to a certain amount.

94 For purposes of computing net earnings from self-employment, taxpayers are permitted a deduction equal to the product of the taxpayer’s earnings (determined without regard to this deduction) and one-half of the sum of the rates for OASDI (12.4 percent) and HI (2.9 percent), [that is] 7.65 percent of net earnings. This deduction reflects the fact that the FICA rates apply to an employee’s wages, which do not include FICA taxes paid by the employer, whereas a self-employed individual’s net earnings are economically equivalent to an employee’s wages plus the employer share of FICA taxes.

[23] Calculated with data from the: “2023 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, March 28, 2023. <www.ssa.gov>

Page 213:

Table VI.G1.—Payroll Tax Contribution Rates for the OASDI [Social Security] and HI [Medicare Hospital Insurance] Programs [In percent] …

2013 and later … Self employedb … OASDI up to basec [=] 12.40% … HI all earningsd [=] 2.90% … HI over limite [=] 0.90% …

b Beginning in 1990, self-employed persons receive a deduction, for purposes of computing their net earnings, equal to half of the combined OASDI and HI contributions that would be payable without regard to the contribution and benefit base. The OASDI contribution rate then applies to net earnings after this deduction, but subject to the OASDI base.

c The payroll tax on earnings for the OASDI program applies to annual earnings up to a contribution and benefit base indexed to the average wage level. The base is $160,200 for 2023.

d Prior to 1994, the payroll tax on earnings for the HI program applied to annual earnings up to a contribution base. The HI contribution base was eliminated beginning in 1994.

e Starting with Federal personal income tax returns for tax year 2013, earned income exceeding $200,000 for individual filers and $250,000 for married couples filing jointly is subject to an additional HI tax of 0.9 percent. These income limits are not indexed after 2013.

Page 212: “This appendix does not include estimates for the Supplementary Medical Insurance (SMI) program because adequate financing is guaranteed in the law and because the SMI program is not financed through a payroll tax.”

Page 247: “Medicare consists of two separate but coordinated trust funds—Hospital Insurance (HI, Part A) and Supplementary Medical Insurance (SMI).”

CALCULATION: 12.4% + 2.9% = 15.3%

[24] Calculated with data from the: “2023 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, March 28, 2023. <www.ssa.gov>

Page 213:

Table VI.G1.—Payroll Tax Contribution Rates for the OASDI [Social Security] and HI [Medicare Hospital Insurance] Programs [In percent] …

2013 and later … Employees and employers, combineda … OASDI up to basec [=] 12.40% … HI all earningsd [=] 2.90% … HI over limite [=] 0.90% …

a Except as noted below, the combined employee/employer rate is divided equally between employees and employers.

c The payroll tax on earnings for the OASDI program applies to annual earnings up to a contribution and benefit base indexed to the average wage level. The base is $160,200 for 2023.

d Prior to 1994, the payroll tax on earnings for the HI program applied to annual earnings up to a contribution base. The HI contribution base was eliminated beginning in 1994.

e Starting with Federal personal income tax returns for tax year 2013, earned income exceeding $200,000 for individual filers and $250,000 for married couples filing jointly is subject to an additional HI tax of 0.9 percent. These income limits are not indexed after 2013.

Page 212: “This appendix does not include estimates for the Supplementary Medical Insurance (SMI) program because adequate financing is guaranteed in the law and because the SMI program is not financed through a payroll tax.”

Page 247: “Medicare consists of two separate but coordinated trust funds—Hospital Insurance (HI, Part A) and Supplementary Medical Insurance (SMI).”

CALCULATIONS:

[25] “2023 Annual Report of the Board of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.” United States Department of Health and Human Services, Centers for Medicare and Medicaid Services, April 6, 2023. <www.cms.gov>

Page 31: “In addition, starting in 2013, high-income workers pay an additional 0.9 percent of their earnings above $200,000 (for single workers) or $250,000 (for married couples filing joint income tax returns).”

[26] Report: “Overview of the Federal Tax System as in Effect for 2023.” U.S. Congress, Joint Committee on Taxation, May 11, 2023. <www.jct.gov>

Page 26:

Additional Hospital Insurance Tax on Certain High-Income Individuals

The employee portion of the HI [Medicare Hospital Insurance] tax is increased by an additional tax of 0.9 percent on wages received in excess of a specific threshold amount.140 Employers are required to withhold the additional 0.9 percent on wages of the employee in excess of $200,000. However, unlike the general 1.45 percent HI tax on wages, this additional tax is on the combined wages of the employee and the employee’s spouse, in the case of a joint return. The threshold amount is $250,000 in the case of married filing jointly, $125,000 in the case of married filing separately, and $200,000 in any other case (unmarried individual, head of household or surviving spouse).141 Any difference between the amount withheld on wages in excess of $200,000 and the applicable tax based on the thresholds is reconciled on the individual’s personal income tax return.

The same additional HI tax applies to the HI portion of SECA [Self-Employment Contributions Act] tax on self-employment income in excess of the threshold amount. Thus, an additional tax of 0.9 percent is imposed on every self-employed individual on self-employment income in excess of the applicable threshold amount.142

114 These threshold amounts are not indexed for inflation.

[27] Determined by examining varied paychecks.

[28] Report: “Historical Effective Federal Tax Rates: 1979 to 2005.” Congressional Budget Office, December 2007. <www.cbo.gov>

Page 3:

Who Pays Taxes?

CBO’s [Congressional Budget Office’s] analysis of effective tax rates … assumes—as do most economists—that employers’ share of payroll taxes is passed on to employees in the form of lower wages than would otherwise be paid. Therefore, the amount of those taxes is included in employees’ income, and the taxes are counted as part of employees’ tax burden.