Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

* “Energy,” as defined by the Oxford Dictionary of Biochemistry and Molecular Biology, is “the capacity of a system for doing work.”[1] [2] [3]

* Energy can take varying forms, such as thermal, electrical, mechanical, nuclear, chemical, gravitational, acoustic, and electromagnetic.[4]

* Two common measures of energy are British thermal units (Btu) and joules. All forms of energy can be expressed in these units. One Btu is the amount of energy needed to raise the temperature of one pound of water from 39 to 40 degrees Fahrenheit.[5] One joule is the amount of energy needed to lift one hundred grams (3.5 ounces) upward by one meter (3.3 feet) while on the surface of the earth.[6]

* As a consequence of the First Law of Thermodynamics, energy and matter cannot be created or destroyed; they can only be transformed from one form into another.[7] [8] [9] [10]

* As a consequence of the Second Law of Thermodynamics, when energy is transformed from one form to another, some of it disperses, thus making it less useful for performing work.[11] [12] [13] [14]

* Humans have learned to harness energy to accomplish tasks such as transporting people and products, heating and cooling homes, farming, cooking, manufacturing goods, communicating across vast distances, and generating light.[15]

* The average annual energy consumption in the U.S. is 293,000,000 Btu per person. To generate this amount of energy through physical human effort (like pedaling bicycles to drive generators) would require 197 people working nonstop for a year.[16]

* “Embodied energy” refers to the energy used in making materials. For example, to make a common clay brick weighing 5 pounds requires about 5,386 Btu of energy. The materials of a typical house embody about 850 million Btu, which is equivalent to the energy that would be generated by 573 people pedaling bicycles nonstop for a year.[17]

* In 2020, energy expenditures in the U.S. were $1.0 trillion ($1,007,433,000,000).[18] This amounts to:

* The costs of most products are affected by the costs of energy, even products with low embodied energies, because the costs of energy affect the costs of transporting products. Since energy costs influence the costs of products, higher energy costs tend to drive up unemployment, drive down wages, and cause other negative economic effects. Such consequences tend to be harsher in poorer nations.[23] [24] [25]

* Roughly one third of the world’s population does not have access to modern forms of energy.[26] [27] In these areas, people use biomass (primarily wood) for about 80% of their energy, and women and children spend an average of 9–12 hours a week collecting firewood. Per the Institute for Plasma Physics in the Netherlands:

* Higher energy costs drive up the costs of food.[31] This has greater impacts on poorer nations and individuals because they spend a larger portion of their income on food.[32] [33] In Haiti during 2007 and 2008, higher energy prices contributed to increased food prices, driving Haiti’s poorer people to obtain nourishment from cookies made of mud.[34]

* Per the Congressional Research Service, “The economic well-being and economic security of the nation depends on having stable energy sources.”[35]

* Per the U.S. Government Accountability Office, “Americans’ daily lives, as well as the economic productivity of the United States, depend on the availability of energy….”[36]

* Per the World Bank:

* Per the textbook Introduction to Air Pollution Science, “The availability of affordable electric power is essential for public health and economic prosperity.”[38]

* Per the U.S. Energy Information Administration:

* Per the textbook Microeconomics for Today, countries with slower economic growth “are less able to satisfy basic needs for food, shelter, clothing, education, and health.”[41]

* In order to perform useful work, energy usually must be converted from one form to another. Most energy on earth ultimately comes from the sun, and this energy typically undergoes multiple conversions before it is used to accomplish a particular task. For example, the energy that ultimately powers a light bulb may have the following history:

* With each conversion process, some amount of the energy is dispersed, thus making it less useful for performing work. Per the U.S. National Academy of Sciences:

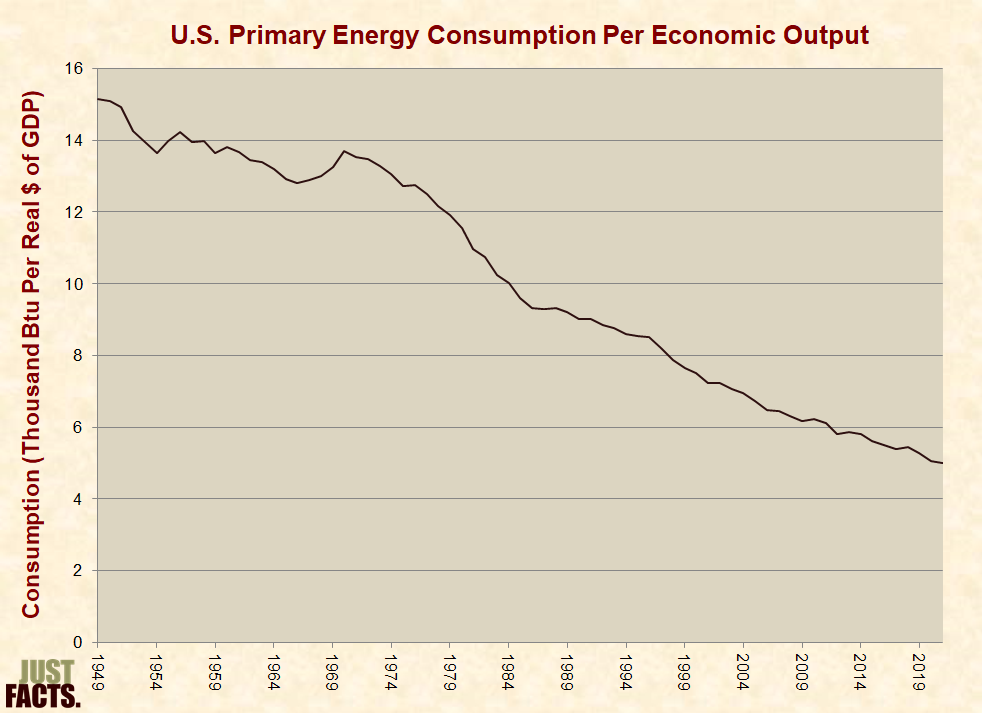

* In the U.S. from 1949 to 2021, energy consumption per inflation-adjusted dollar of economic output decreased by 67%:

* Homes built in the U.S. from 2000 to 2015 are about 25% larger than homes built prior to this period, but they use about 2% more total energy. This result is primarily due to better insulation and increased efficiencies of heating and air conditioning technologies.[49] [50]

* Homes built in the U.S. from 2000 to 2015 use about 23% more energy on appliances, electronics, and lighting than older homes. This is because newer homes are more likely to have “dishwashers, clothes washers, clothes dryers, and two or more refrigerators.” Also, because they have more square footage, newer homes tend to have more “computers, TVs, and TV peripherals such as digital video recorders (DVRs) and video game systems.”[51] [52]

* Increasing the efficiency of electronics, appliances, and lighting reduce the demand for energy and can save consumers money if the added cost of making these products more efficient does not exceed the cost of the energy saved.[53] [54]

* Energy Star is a joint program of the U.S. Environmental Protection Agency (EPA) and Department of Energy. Per the program’s website:

* In 2010, the U.S. Government Accountability Office (GAO) published an investigation of Energy Star in which GAO submitted 20 “bogus products” for approval. Fifteen of the products were approved, two were rejected, and three were unanswered at the time the report was published. Among the products certified as Energy Star compliant were:

* The U.S. Green Building Council, per its website, is a “nonprofit organization committed to a prosperous and sustainable future for our nation through cost-efficient and energy-saving green buildings.”[57] This organization provides various types of green building certifications that qualify the owners for government incentives, such as tax breaks and zoning allowances. This rating system is named LEED for “Leadership in Energy and Environmental Design.”[58]

* In 2012, USA Today conducted an investigation of schools with green building certifications (such as LEED) and found that:

* In 1989, Gus Speth, president of environmentalist organization World Resources Institute, stated:

* As of 2022, the Mitsubishi Mirage is the most fuel-efficient non-hybrid car. It travels 39 miles per gallon of gasoline, has a 78-horsepower engine, and weighs about 2,100 pounds.[61] [62]

* Per the U.S. National Academy of Sciences:

* During 2023:

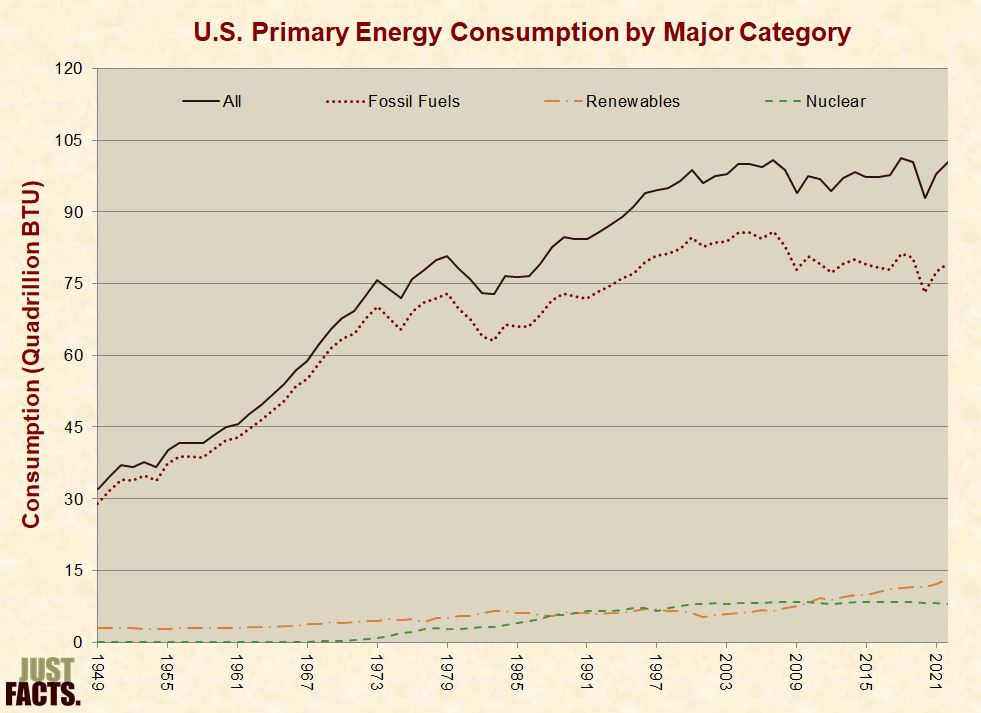

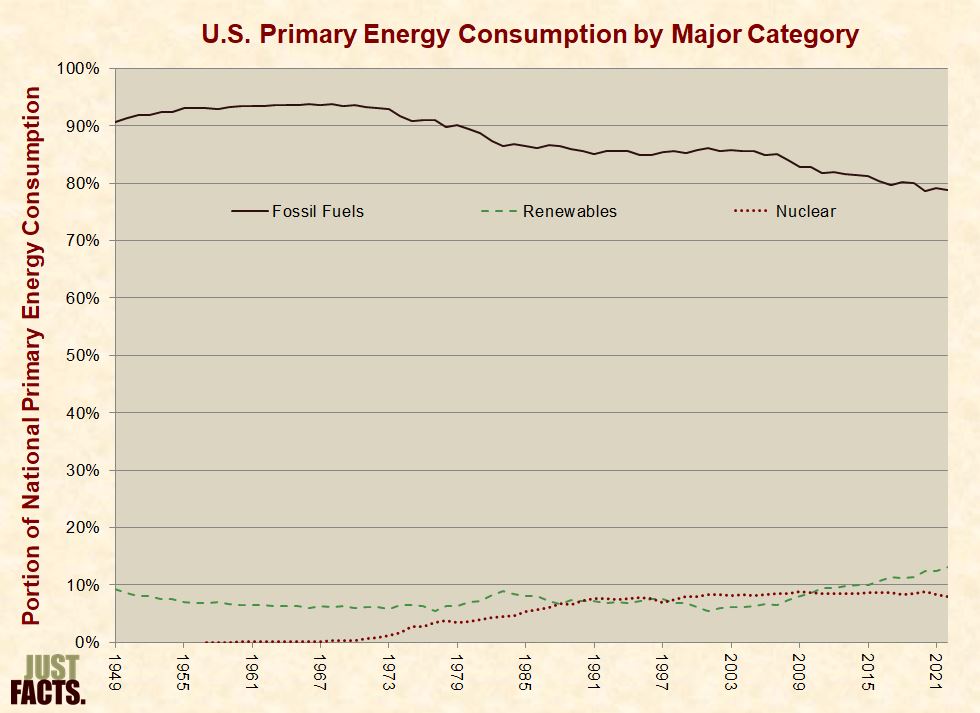

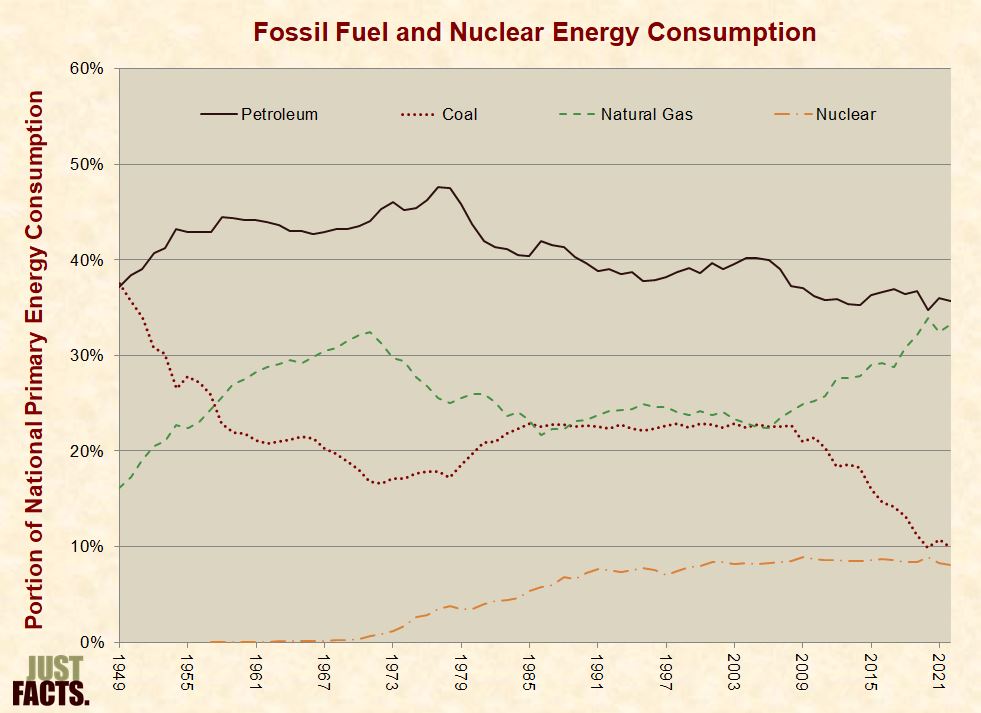

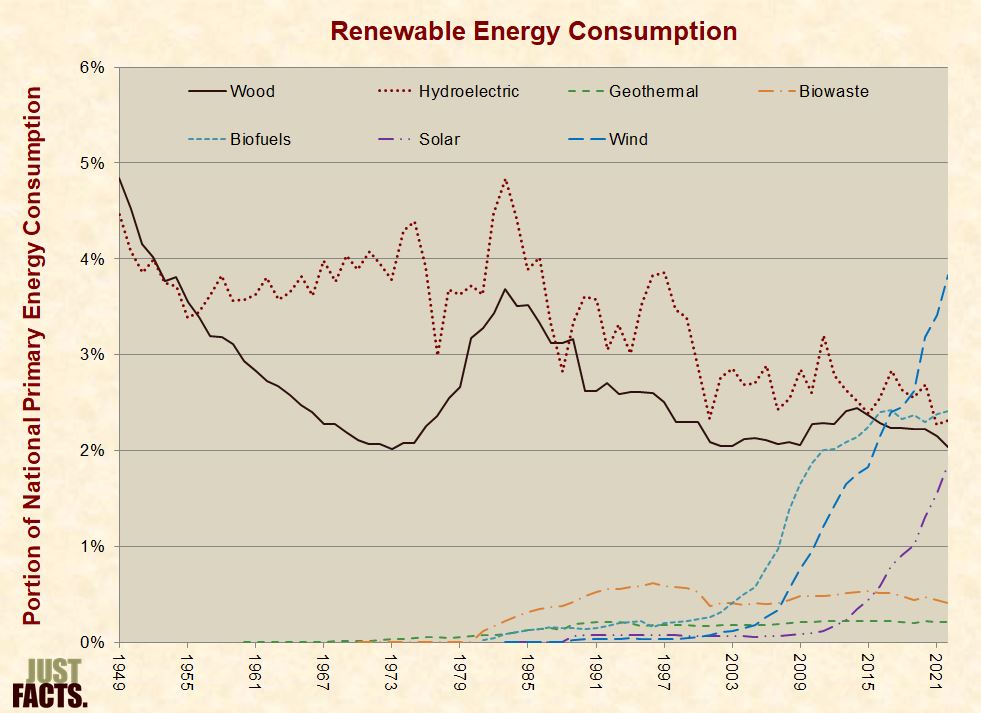

* The following charts show the components of U.S. energy consumption over time. The first shows consumption measured in Btus. The rest show consumption measured as a portion of total U.S. energy consumption. Each succeeding chart uses a smaller scale to provide increasing resolution.

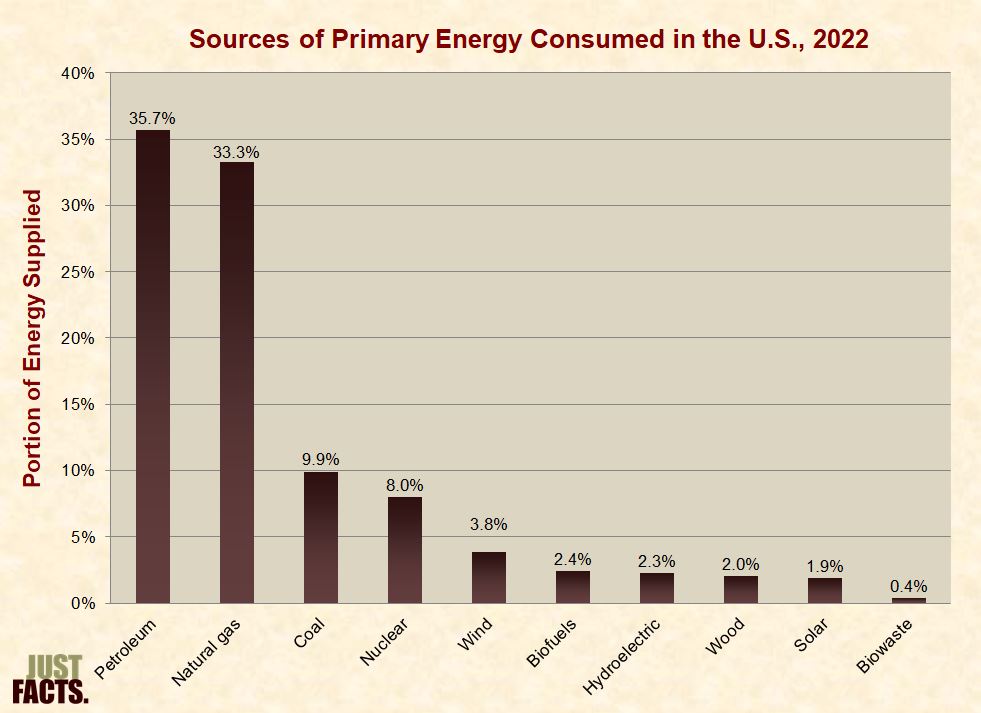

* Data from the charts above:

|

Components of U.S. Energy Consumption |

|||||||||

|

Source |

1950 |

1960 |

1970 |

1980 |

1990 |

2000 |

2010 |

2020 |

2023 |

|

Fossil Fuels |

91.4% |

93.5% |

93.6% |

89.4% |

85.6% |

85.7% |

82.8% |

78.7% |

78.3% |

|

Petroleum |

38.4% |

44.1% |

43.5% |

43.8% |

39.7% |

38.7% |

36.2% |

34.8% |

35.9% |

|

Natural Gas |

17.2% |

27.5% |

32.1% |

25.9% |

23.2% |

24.1% |

25.2% |

34.0% |

34.1% |

|

Coal |

35.7% |

21.8% |

18.1% |

19.8% |

22.7% |

22.9% |

21.4% |

9.9% |

8.3% |

|

Renewables |

8.6% |

6.5% |

6.0% |

7.0% |

7.2% |

6.2% |

8.5% |

12.3% |

13.4% |

|

Wind |

N/A |

N/A |

N/A |

N/A |

0.0% |

0.1% |

0.9% |

3.2% |

3.8% |

|

Biofuels |

N/A |

N/A |

N/A |

N/A |

0.1% |

0.2% |

1.9% |

2.3% |

2.7% |

|

Solar |

N/A |

N/A |

N/A |

N/A |

0.1% |

0.1% |

0.1% |

1.3% |

2.2% |

|

Hydroelectric |

4.1% |

3.6% |

3.9% |

3.7% |

3.6% |

2.8% |

2.6% |

2.7% |

2.1% |

|

Wood |

4.5% |

2.9% |

2.1% |

3.2% |

2.6% |

2.3% |

2.3% |

2.1% |

1.9% |

|

Biowaste |

N/A |

N/A |

0.0% |

0.0% |

0.5% |

0.5% |

0.5% |

0.5% |

0.4% |

|

Geothermal |

N/A |

0.0% |

0.0% |

0.1% |

0.2% |

0.2% |

0.2% |

0.2% |

0.2% |

|

Nuclear |

0.0% |

0.0% |

0.4% |

3.5% |

7.2% |

8.0% |

8.6% |

8.9% |

8.2% |

* The U.S. Energy Information Administration (EIA) divides the energy market into four major sectors: residential,[78] commercial,[79] transportation,[80] and industrial.[81] [82]

* In 2021, the residential sector consumed 21% of all U.S. energy, the commercial sector consumed 18%, the transportation sector consumed 28%, and the industrial sector consumed 33%.[83]

* EIA sometimes classifies “electric power” as a separate sector,[84] although the electricity produced by this sector is consumed by the four major sectors.[85]

* In 2021, the electric power sector consumed 38% of all U.S. energy.[86]

* Per the Institute for Plasma Physics in the Netherlands:

* During 2021—amid the Covid-19 pandemic and related restrictions on business and personal activities:[88] [89] [90]

* Economic growth is a key factor in the growth of electricity generation.[93]

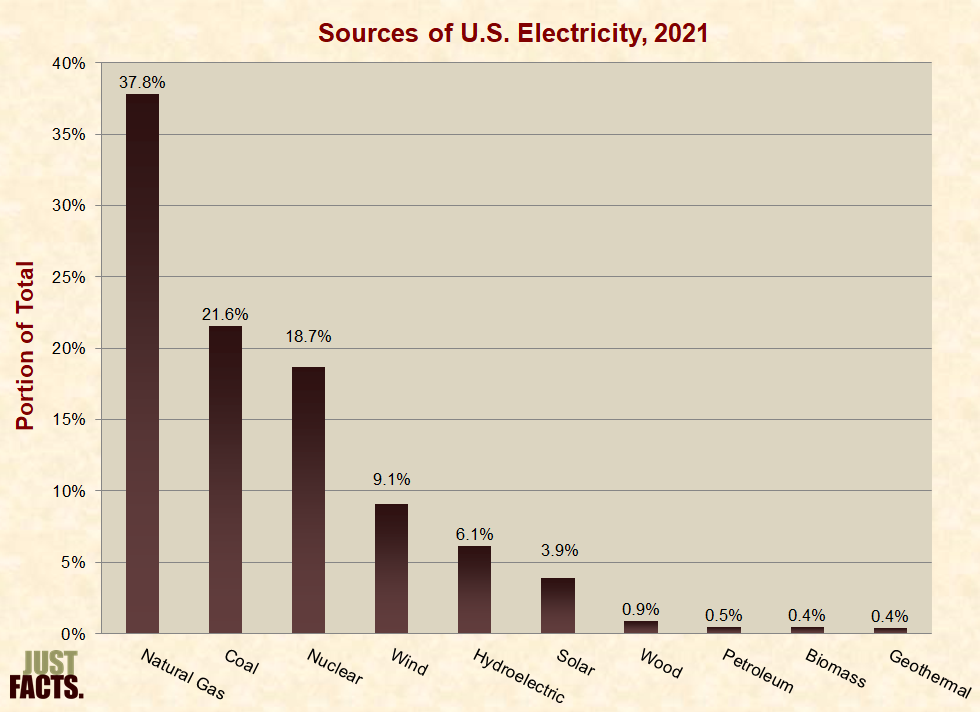

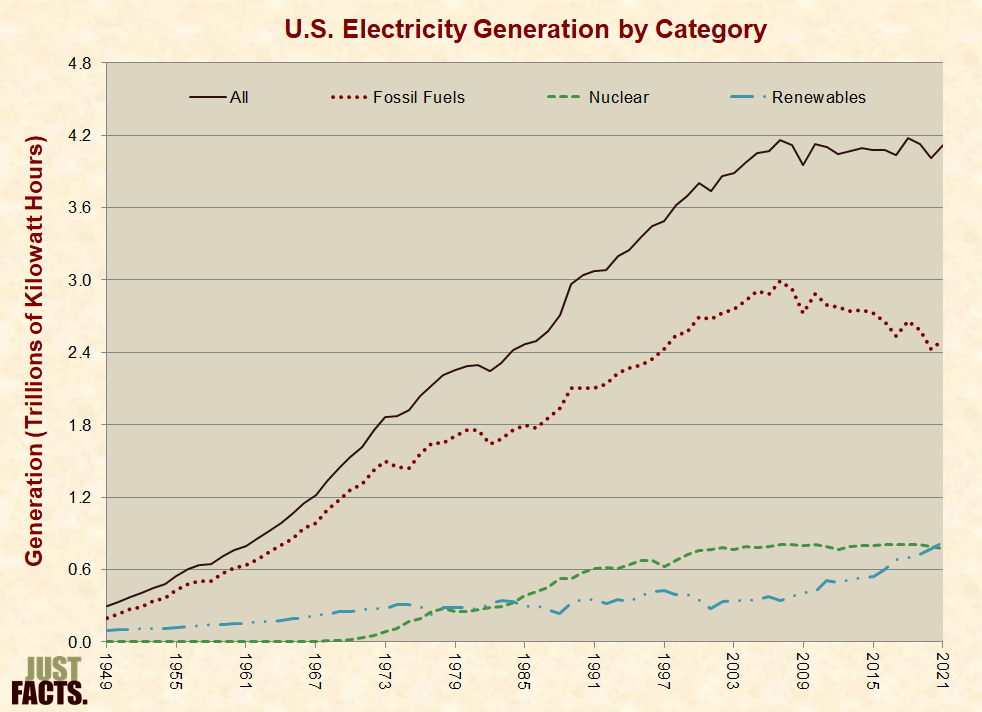

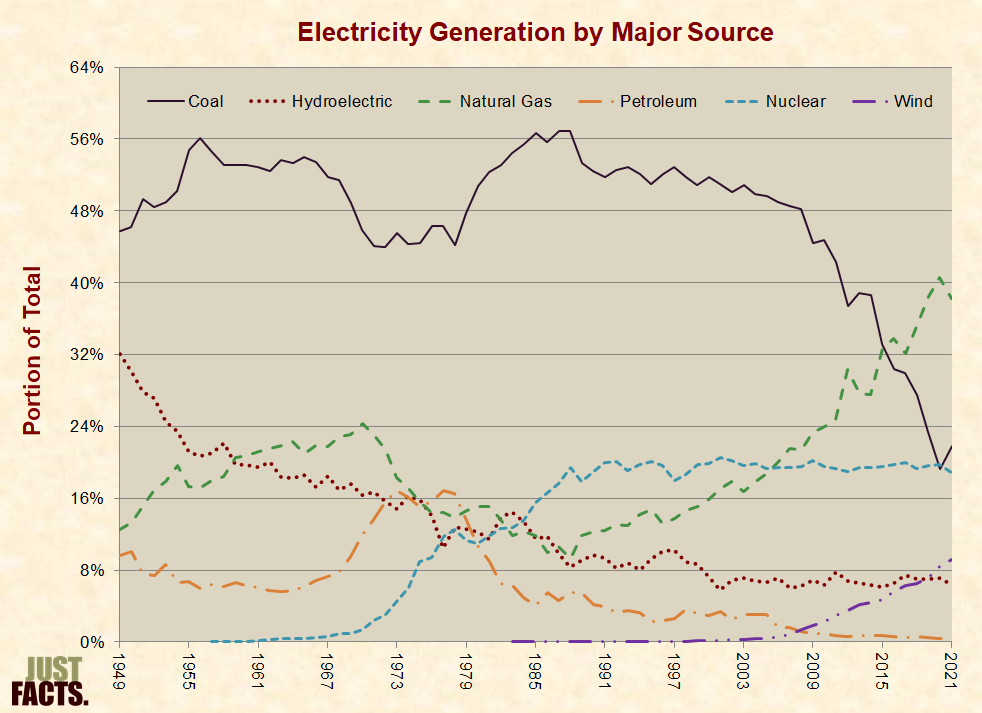

* The following graphs show the components of U.S. electricity generation over time. The first graph shows generation measured in kilowatt hours. The rest show generation measured as a portion of total U.S. electricity generation. Each succeeding graph uses a smaller scale to provide increasing resolution.

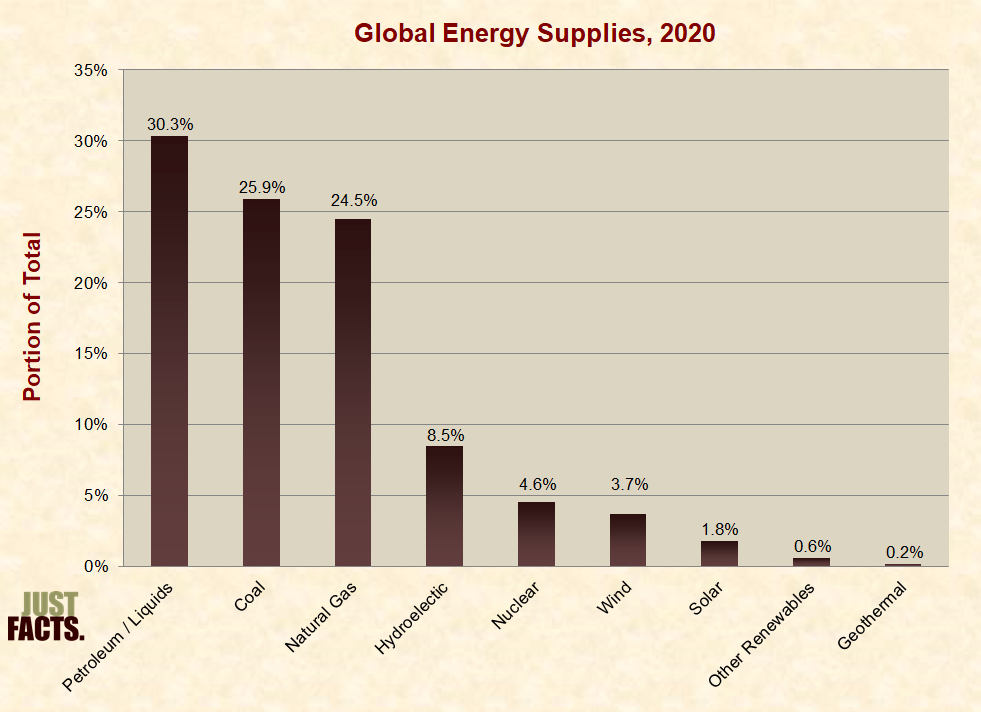

* Excluding energy sources that are not commercially sold (like self-procured firewood), during 2020:

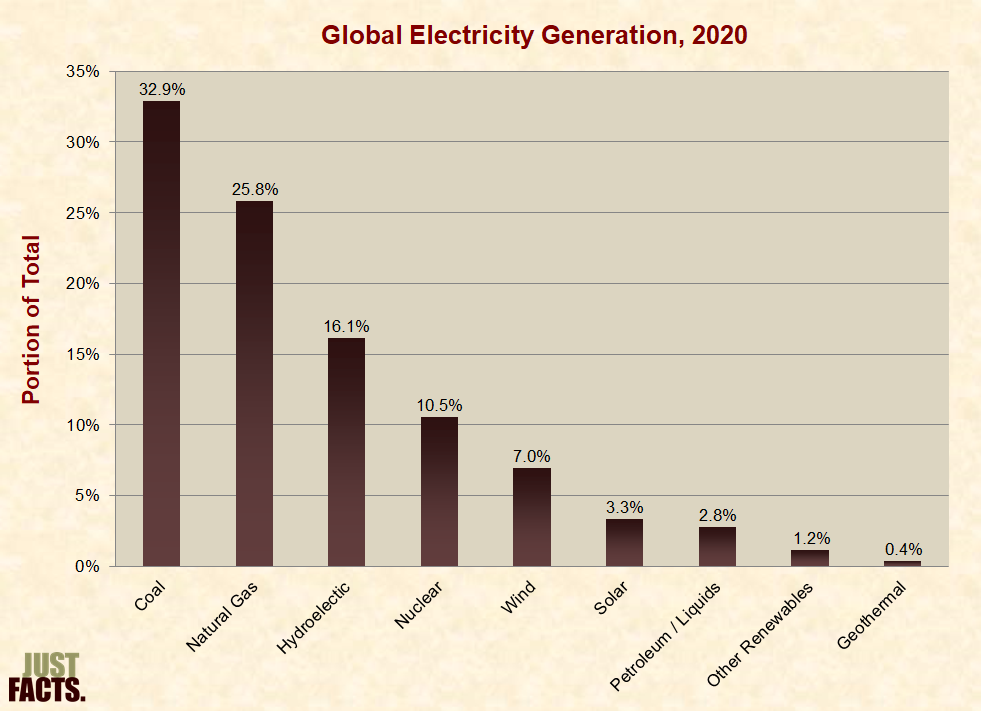

* During 2020:

* In both developing and developed countries, when modern energy is unavailable or expensive, people tend to burn more wood, crop waste, manure, and coal in open fires and simple home stoves. Open fires and home stoves do not burn fuel as efficiently as commercial energy technologies, and hence they produce elevated levels of outdoor and indoor pollutants. The added consumption of wood also causes deforestation.[105] [106] [107] [108]

* Assessing the full environmental impacts of different energy technologies requires looking beyond the effects at a single point of production, use, or disposal. To do this, researchers perform “life cycle assessments” or LCAs. Per the U.S. Environmental Protection Agency (EPA), LCAs allow for:

* Per the journal Environmental Science & Technology:

* The air pollutants generated by energy sources vary with factors such as combustion methods, manufacturing techniques, and pollution control technologies.[113] [114] For example, bituminous coal combusted in a fluidized bed boiler without pollution controls produces one tenth the sulfur dioxide of the same fuel burned in a cyclone boiler without pollution controls.[115] [116] [117]

* Environmental lifecycle analyses are subject to multiple levels of uncertainty.[118] [119] [120] [121]

* In general:

* Per the U.S. Department of Energy (2010):

* In the U.S. from 1990 through 2021, sulfur dioxide (SO2) emissions per Btu of coal-generated energy decreased by 94%, and nitrogen oxides (NOX) emissions decreased by 88%.[141]

* Since the late 1970s, new automobiles have been equipped with catalytic converters, an “anti-pollution device” that converts “exhaust pollutants … to normal atmospheric gases such as nitrogen, carbon dioxide, and water.”[142] [143] [144]

* The federal government and various states financially subsidize electric cars.[145] [146] Some states have also begun to mandate electric cars while claiming that they are “zero-emission vehicles.”[147] [148]

* Electric cars have no tailpipe emissions, but this does not mean they have no emissions. A study published by the Journal of Cleaner Production in 2021 found that electric cars emit more toxic emissions over their life cycles than gas cars. From “cradle-to-grave,” the study estimates that relative to gas cars, the manufacturing, usage, and disposal of electric cars will increase:

* Facts about air pollution levels and their effects are detailed in Just Facts’ research on pollution.

* Carbon dioxide (CO2) contributes more to the greenhouse effect than any other gas released by human activity.[150] [151] [152]

* In general:

|

Pounds of CO2 Per Million Btu |

|

|

Natural gas |

117 |

|

Propane |

139 |

|

Gasoline |

156 |

|

Diesel fuel & heating oil |

163 |

|

Coal |

205–229 |

* The federal government and various states financially subsidize electric cars.[166] [167] Some states have also begun to mandate electric cars while claiming that they are “zero-emission vehicles.”[168] [169]

* Electric cars have no tailpipe emissions, but this does not mean they have no emissions during their manufacturing, usage, and disposal. A study published by the Journal of Cleaner Production in 2021 found that from “cradle-to-grave,” electric cars emit 52% of the CO2 of gas cars.[170]

* Biofuels such as ethanol generate CO2 when burned, but the crops used to make these fuels absorb an equal amount of CO2 as they grow. However, planting, fertilizing, harvesting, processing, and distributing ethanol emits more CO2 than extracting, refining, and distributing gasoline.[171] [172] [173] [174] [175]

* Per the U.S. Congressional Budget Office, lifecycle analyses comparing CO2 emissions of corn-based ethanol and gasoline have produced varying results. The most authoritative study in the eyes of the federal government (conducted by Argonne National Laboratory) estimates that, on average, corn-based ethanol produces about 20% less CO2 than gasoline.[176]

* Another type of biofuel called cellulosic ethanol has the potential to produce 60–95% less CO2 emissions than gasoline. This fuel is more difficult to manufacture than regular ethanol, and as of 2022, producers have been unable to make enough of it to meet the mandated amounts specified in federal law.[177] [178] [179] [180] [181] [182] [183]

* Converting undeveloped land to cultivate crops for biofuels creates CO2 emissions because existing plant life is removed and the soil is disrupted. If this land is repeatedly used to produce biofuels, the net CO2 emissions will be less than using fossil fuels. The timeframe until this breakeven point occurs depends upon factors such as the type of land converted and type of biofuel produced. Per a 2008 paper in the journal Science, the CO2 breakeven time of converting:

* Per the U.S. Energy Information Administration:

* Facts about greenhouse gases and climate change are detailed in Just Facts’ research on global warming.

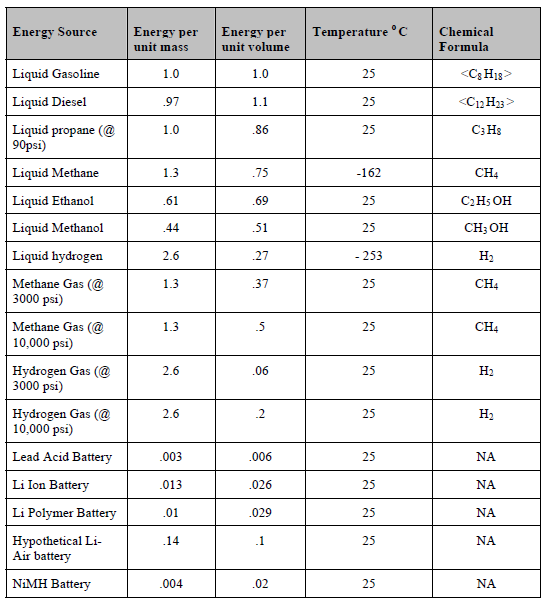

* Transportation fuels have different energy densities, and thus, the price per volume of each fuel does not accurately reflect the energy supplied to consumers. For example, the energy content of a gallon of ethanol is 31% less than a gallon of gasoline. Hence, a car fueled with E85 (a mixture of 70–85% ethanol and 15–30% gasoline) will get 25–30% fewer miles per gallon than the same car when it is fueled with pure gasoline.[186] [187] [188] [189] [190]

* Like ethanol, the volume of biodiesel blended with regular diesel is shown by a number that follows the first letter of the named fuel. Thus, B20 contains 20% biodiesel and 80% regular diesel.[191]

* On an energy-equivalent basis, the average subsidized retail prices (including taxes) for transportation fuels during 2021 were as follows:

|

Fuel |

Nationwide Average Price in Gasoline-Gallon Equivalents |

Price Relative to Gasoline |

|

Compressed Natural Gas |

$2.23 |

-29% |

|

Biodiesel (B20) |

$2.60 |

-17% |

|

Diesel |

$2.78 |

-11% |

|

Gasoline |

$3.13 |

0% |

|

Ethanol (E85) |

$3.18 |

2% |

|

Biodiesel (B100) |

$3.47 |

11% |

|

Propane |

$4.08 |

30% |

* A federal law known as the “Renewable Fuel Standard” requires U.S. consumers to use certain amounts of ethanol and other biofuels. This mandate uses a compliance mechanism that transfers some of the costs of producing these fuels from biofuel companies to petroleum companies. These added costs are then passed on to consumers in the form of higher gas prices.[193] [194] [195] [196] [197]

* During 2021, a federal tax credit subsidized biodiesel at a rate of $1.00 per gallon.[198]

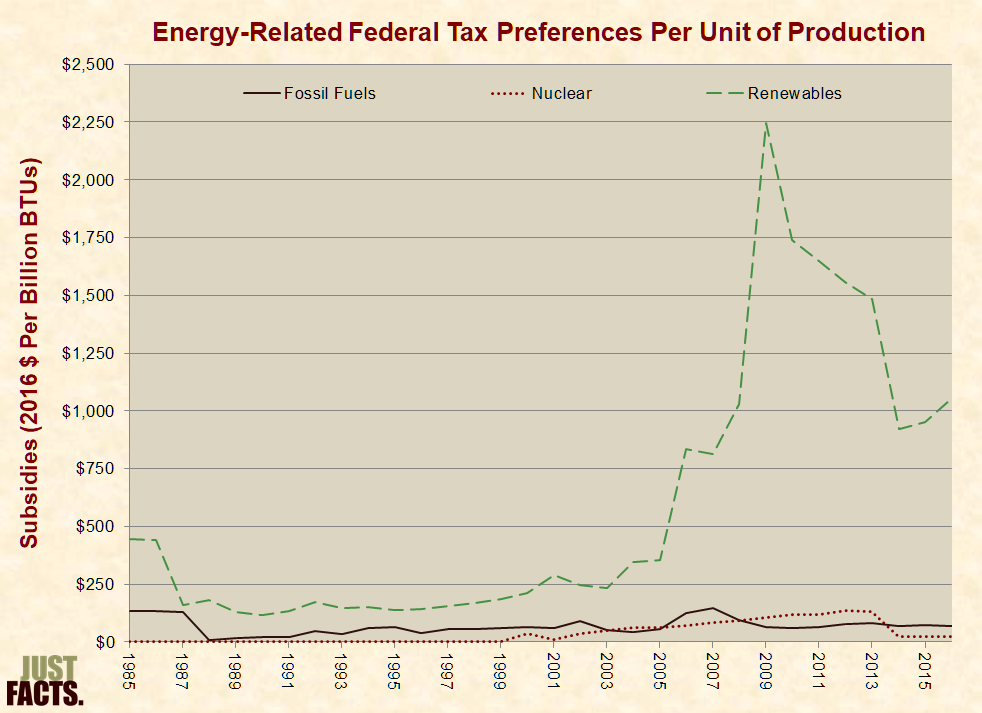

* During 2016, federal energy “subsidies” penalized petroleum and natural gas production at an average rate of $0.002 per gasoline-gallon equivalent.[199]

* Combining the data above yields the following average prices for transportation fuels during 2021 without federal subsidies:

|

Fuel |

Unsubsidized Price in Gasoline-Gallon Equivalents |

Unsubsidized Price Relative to Gasoline |

|

Compressed Natural Gas |

$2.23 |

-29% |

|

Diesel |

$2.78 |

-11% |

|

Biodiesel (B20) |

$2.92 |

-7% |

|

Gasoline |

$3.13 |

0% |

|

Propane |

$4.08 |

30% |

|

Ethanol (E85) |

$4.22 |

35% |

|

Biodiesel (B99–B100) |

$6.21 |

98% |

* A scientific, nationally representative survey commissioned in 2019 by Just Facts found that 40% of voters believed that the unsubsidized cost of ethanol or biodiesel was lower than gasoline.[202] [203] [204] In 2019, the unsubsidized cost of:

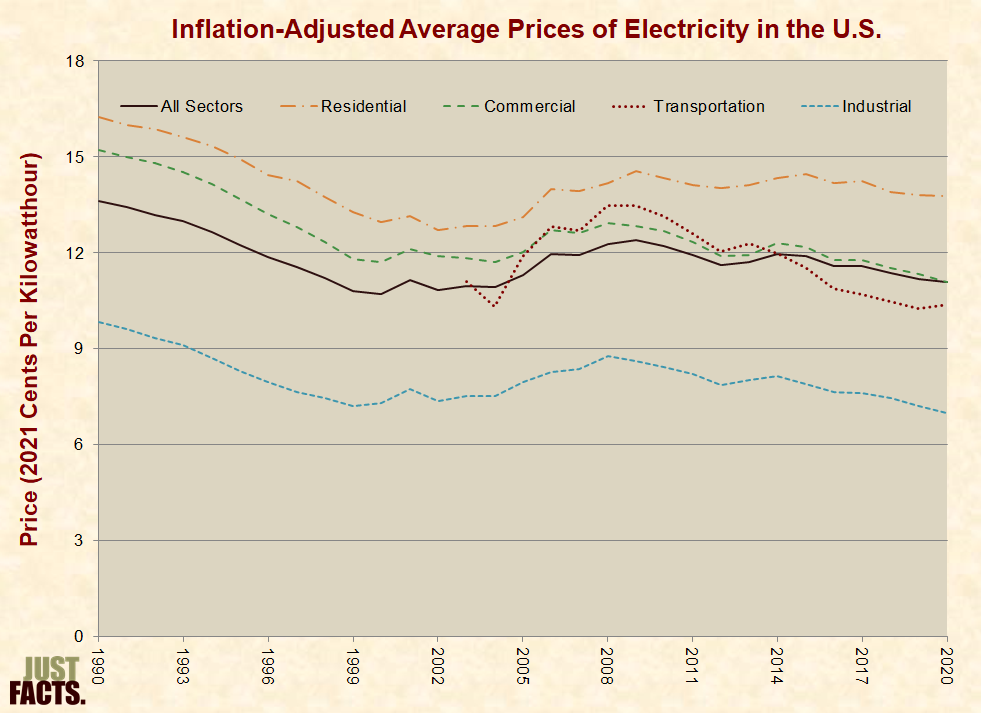

* From 1929 to 1967, the inflation-adjusted average price of electricity for U.S. residential customers declined from about 60 cents per kilowatt hour to 10 cents, and it stayed roughly around this level through 2015.[206] [207]

* Since 1990, the inflation-adjusted average prices of electricity for all U.S. consumers and the four major energy sectors have varied as follows:

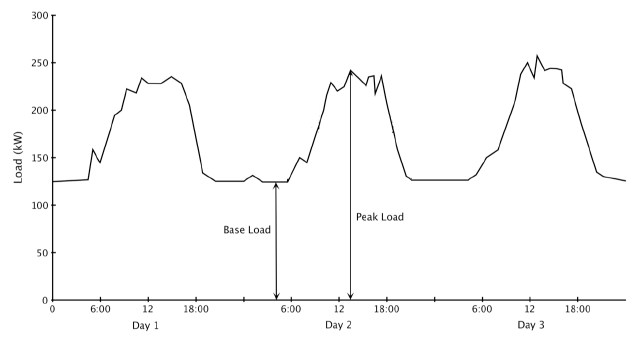

* Demand for electricity varies on an hourly, daily, and seasonal basis due to factors such as:

* As shown in the following graph, the terms “baseload” and “peak load” are used to describe the minimum and maximum demands for electricity over a given time period. The term “intermediate load” is used to describe the range between them.[212] [213]

* Coal is the dominant energy source for generating baseload capacity, because low fuel costs make coal plants inexpensive to run continuously, which is ideal for generating baseload capacity. For the same reason, nuclear power is a primary source of baseload capacity. Natural gas, hydropower, geothermal, and waste-to-energy plants are also sources of baseload capacity.[215] [216] [217] [218]

* Natural gas is the dominant energy source for generating intermediate and peak load capacity because natural gas power plants can ramp up and down quickly, which is ideal for intermediate and peak load capacity.[219] [220] [221] [222]

* In 2009, natural gas became competitive with coal for generating baseload capacity in some areas of the U.S. This was primarily due to increased domestic natural gas production, which reduced prices. Other factors included increased coal prices, stricter environmental regulations, and expansion of natural gas pipelines.[223] [224] [225] [226]

* Both coal and natural gas are competitive for generating baseload capacity under differing circumstances in different regions of the U.S.[227] [228] [229] [230] [231]

* For existing power plants, natural gas plants that employ a high efficiency technology called “combined cycle” can generate baseload power less expensively than coal plants when natural gas is about equal to or less than 1.5 times the price of coal.[232] [233] [234] In 2021, the average price paid by electric power plants for natural gas was about 2.5 times the price of coal.[235]

* Determining which electricity-generating technologies will provide the lowest cost while maintaining reliability is complicated by the following factors:

* A commonly cited measure of the costs of building and operating new power plants is the “levelized cost” data published by EIA. Levelized costs reflect “both the capital and operating costs of deploying and running new utility-scale generation capacity of any given type.”[255] [256] Per EIA:

* The following features, caveats, and limitations are inherent in EIA’s levelized costs:

* Based on the features, caveats, and limitations above, EIA’s 2022 levelized cost projections for plants beginning operation in 2027 are:

|

Plant Type (Lowest Cost Option From Each Major Category) |

Cost Per Megawatthour |

Cost Relative to Natural Gas |

|

Dispatchable Technologies |

||

|

Natural Gas Combined Cycle |

$40 |

0% |

|

Geothermal |

$40 |

0% |

|

Advanced Nuclear |

$88 |

121% |

|

Ultra-Supercritical Coal |

$83 |

107% |

|

Non-Dispatchable Technologies |

||

|

Onshore Wind |

$40 |

1% |

|

Offshore Wind |

$137 |

242% |

|

Hydropower |

$64 |

61% |

|

Photovoltaic Solar |

$36 |

–9% |

* Per EIA, “a better assessment of economic competitiveness can be gained through consideration of avoided cost, a measure of what it would cost the grid to generate the electricity that is otherwise displaced by a new generation project, as well as its levelized cost.” Calculating these costs involves a greater degree of complexity than levelized costs.[294] [295]

* In July 2013, EIA published a preliminary discussion paper using avoided costs and levelized costs to compare the projected 2018 and 2035 economic values of advanced combined cycle natural gas, onshore wind, and PV solar.[296] Because there is significant variability in factors that affect electricity costs and values in different regions of the country, the paper assessed 22 regions of the United States. It found that without subsidies for wind and with a 10% tax credit for solar:

* The following features, caveats, and limitations are inherent in this analysis:

* In 2022, EIA used levelized costs and avoided costs to estimate which type of electricity plants would be economically competitive to build and begin producing electricity in 2027. Positive values indicate an economic incentive to build, and negative values indicate a disincentive:[309]

|

Levelized Avoided Costs Minus Levelized Costs ($ Per Megawatthour) |

||

|

Plant Type (Best Value From Each Major Category) |

Incentive |

Incentive Relative to Natural Gas |

|

Dispatchable Technologies |

||

|

Natural Gas Combined Cycle |

0 |

0 |

|

Geothermal |

5 |

6 |

|

Ultra-Supercritical Coal |

–44 |

–44 |

|

Advanced Nuclear |

–50 |

–49 |

|

Non-Dispatchable Technologies |

||

|

Onshore Wind |

–6 |

–5 |

|

Offshore Wind |

–101 |

–100 |

|

Hydropower |

–26 |

–26 |

|

Photovoltaic Solar |

–4 |

–3 |

* Forest product companies often use byproducts from their operations to generate their own electricity.[311] During 2021, wood generated 0.9% of all electricity in the U.S., as compared to 4.0% for solar and 0.4% for geothermal.[312]

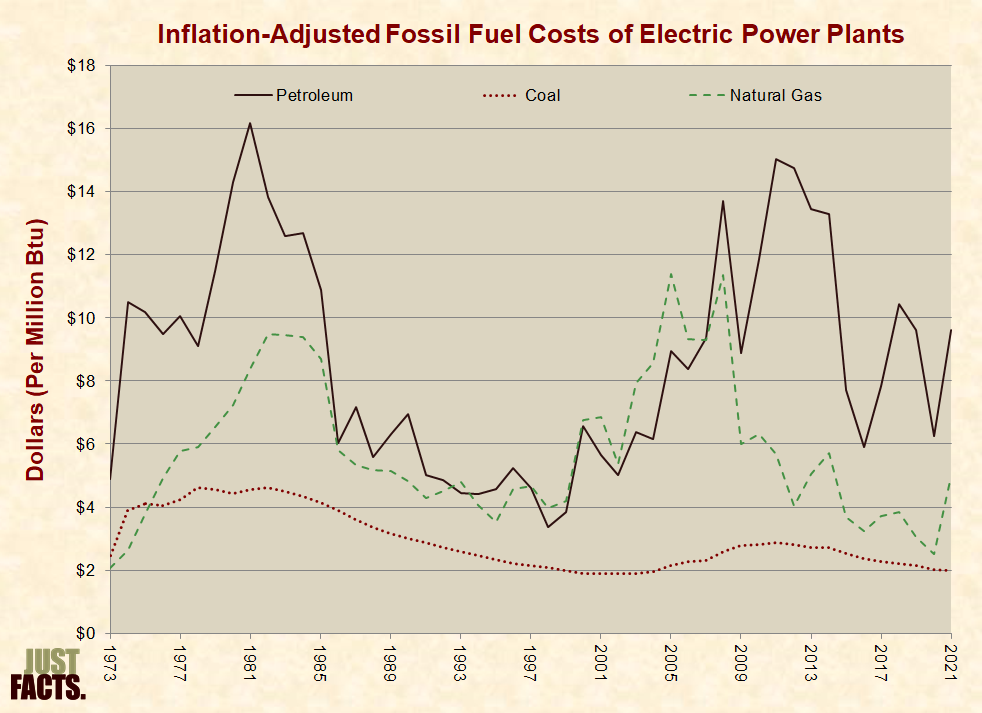

* Oil and biofuels are rarely used to create electricity because they are significantly more costly than the major sources of electricity.[313] [314] In 2021, the average energy-equivalent price paid by electric power plants for petroleum was about 4.8 times the price of coal.[315]

* Petroleum is a class of fossil fuels that are generally liquid at atmospheric pressure, although broader definitions of the term also include some gases and solids. The terms “petroleum” and “crude oil” are sometimes used synonymously, although petroleum is typically defined to include several other types of fossil fuels.[316] [317]

* Petroleum is primarily comprised of organic compounds called hydrocarbons, which consist of carbon and hydrogen. Other common elements of petroleum are nitrogen, oxygen, and sulfur.[318] [319] [320]

* Petroleum is mainly thought to be formed of diverse marine organisms that were buried by sediments and transformed by heat, pressure, and time.[321] [322] [323]

* The first oil well was drilled in 1857, the first intercontinental oil shipment occurred in 1861, and the first modern oil refinery commenced operations in 1862. By the 1870s, “refineries, tank cars, and pipelines had become characteristic features of the industry,” and by 1874, U.S. crude oil production had grown to 10 million barrels per year.[324]

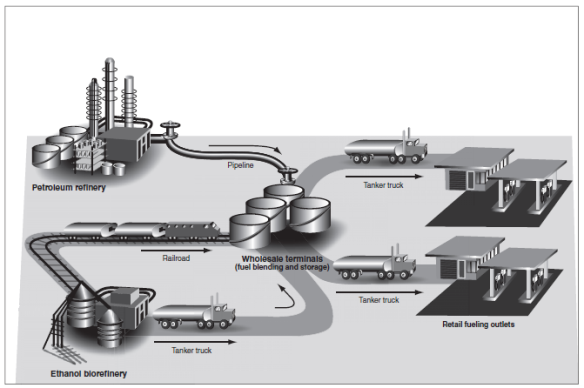

* Today, the vast majority of crude oil is transported via pipelines and ships, and most refined petroleum fuels are transported from refineries to wholesale terminals through pipelines. Pipelines are the safest and most economical means of transporting petroleum in the U.S.[325] [326] [327] [328] [329]

* Petroleum is used to manufacture wide-ranging products, such as gasoline, diesel fuel, jet fuel, heating oil, lubricants, asphalt, propane, synthetic fabrics, plastics, paints, fertilizers, and soaps.[330] [331]

* In 2021, petroleum supplied:

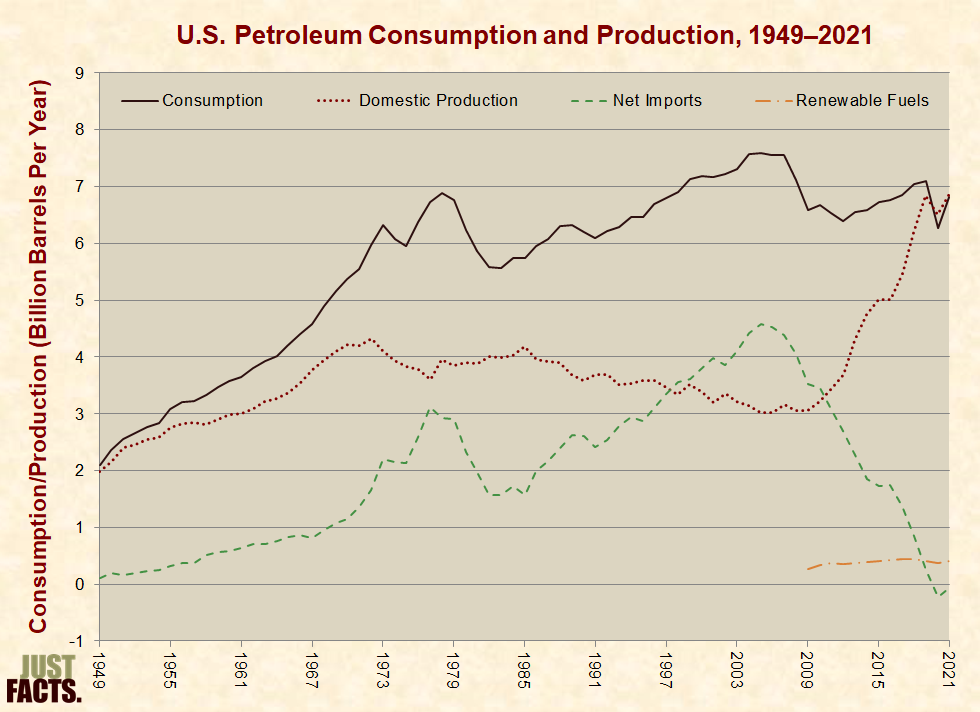

* In 2021, the U.S. produced about 6.9 billion barrels of petroleum, consumed about 6.8 billion barrels, and had net exports of about 60 million barrels.[334]

* U.S. petroleum consumption and net imports both peaked in 2005 and fell until 2012. From then until 2019, consumption rose, while net imports fell. These trends were primarily due to rising U.S. petroleum production from fracking, the Great Recession, efficiency improvements, and renewable fuel usage.[335] [336] [337] In 2020, U.S. consumption fell—primarily due to the Covid-19 pandemic—and the U.S. was a net exporter of petroleum.[338] [339] [340]

* Since 2005, U.S. petroleum production has risen by 128%, and net imports have fallen by 101%:

* In 2021, net petroleum imports from countries where the U.S. had a petroleum trading deficit were distributed as follows:

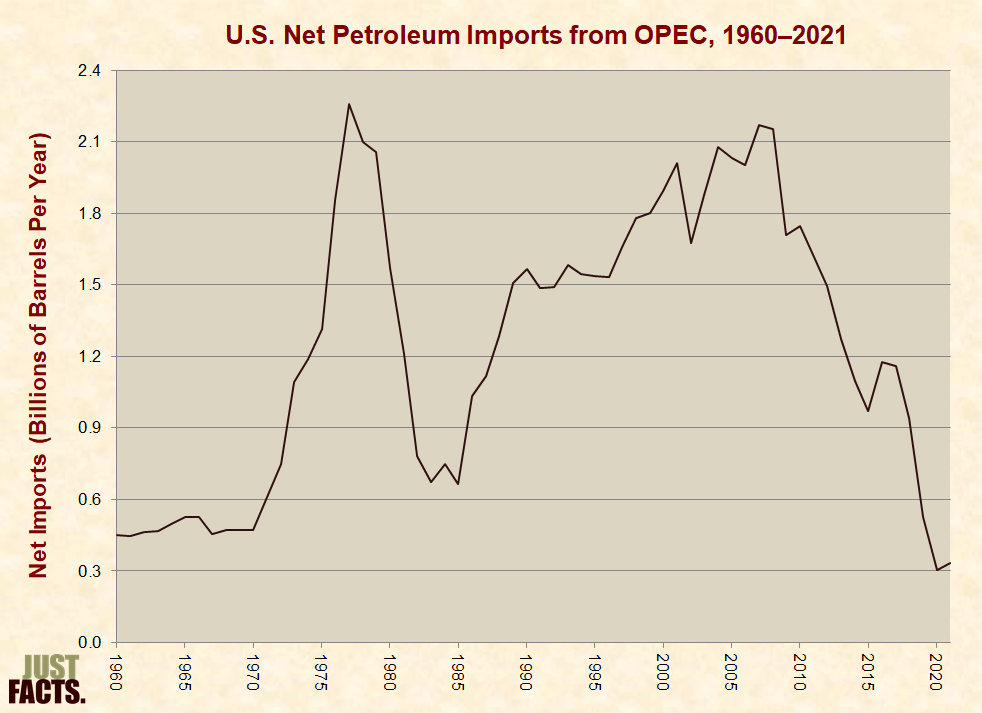

* Since OPEC’s founding in 1960, its member nations have adopted various strategies to exert control over the petroleum market. One of their more common strategies has been to limit their petroleum production in order to boost prices and increase their profits.[347] [348] [349]

* OPEC nations have also adopted the opposite strategy of maximizing their petroleum production in order to drive down prices, force their competitors out of business, and grow their market share. Some OPEC nations have recently done this in response to increased production from non-OPEC countries.[350] [351] [352] [353] [354] [355] [356] [357]

* From 1960 to 2021, the U.S. imported an average of 1.2 billion barrels of petroleum per year from OPEC nations, ranging from a low of 0.3 billion in 2020 to a high of 2.3 billion in 1977:

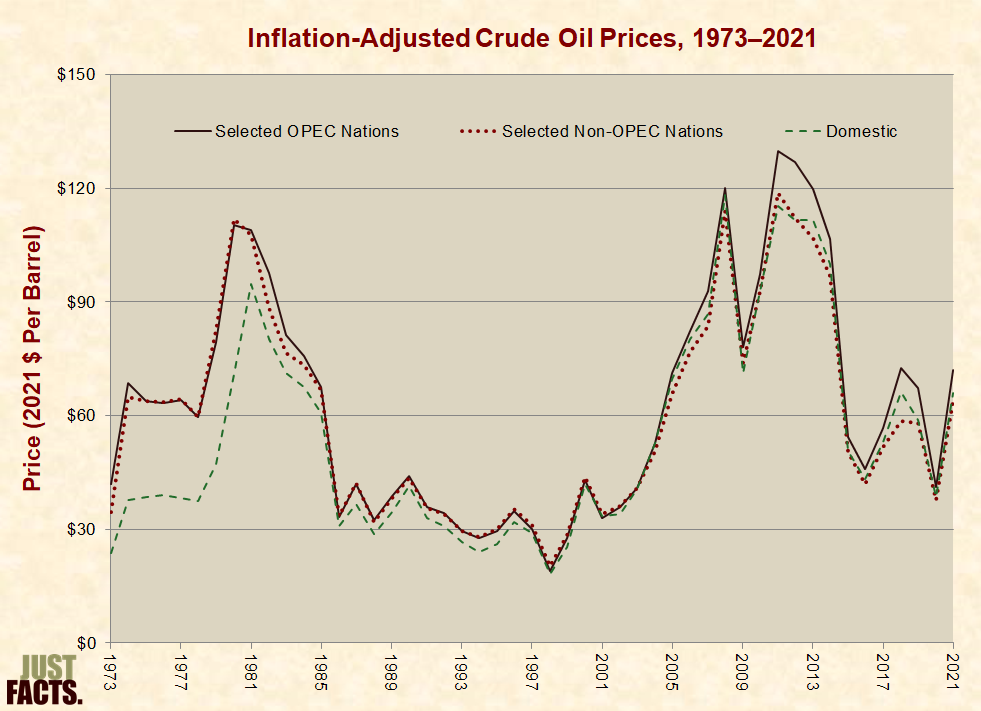

* Crude oil prices are affected by global and local factors that impact the supply of petroleum and the demand for petroleum products, such as:

* In the U.S. during 2021, the average landed (i.e., delivered) price of crude oil from selected OPEC nations was 9% more than the average price of domestic crude, and the average landed price of crude from selected non-OPEC nations was 3% less than the average price of domestic crude.[366]

* In 2021, the average retail price of a gallon of regular-grade gasoline in the U.S. was $3.01. Broken down by its components:

* Crude oil resources can be grouped into four major categories based upon their accessibility:[368]

* Horizontal drilling involves penetrating the ground vertically (like traditional drilling) and then turning horizontally in order to drill along the layer that contains the fossil fuel resources. This method of drilling exposes more of the fossil fuel resources to the bore of each well, thus increasing yields, decreasing the surface footprint of drilling operations, and decreasing unwanted output from the wells, such as water.[383] [384]

* Horizontal drilling was first successfully employed in 1929 and has been used commercially since the late 1980s. By 1990, more than 1,000 horizontal wells were drilled worldwide, roughly 85% of which were in Texas.[386]

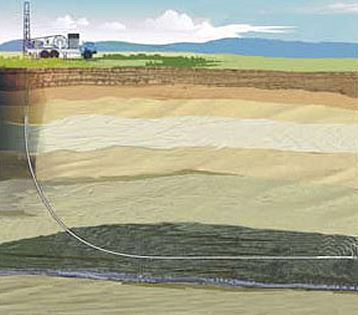

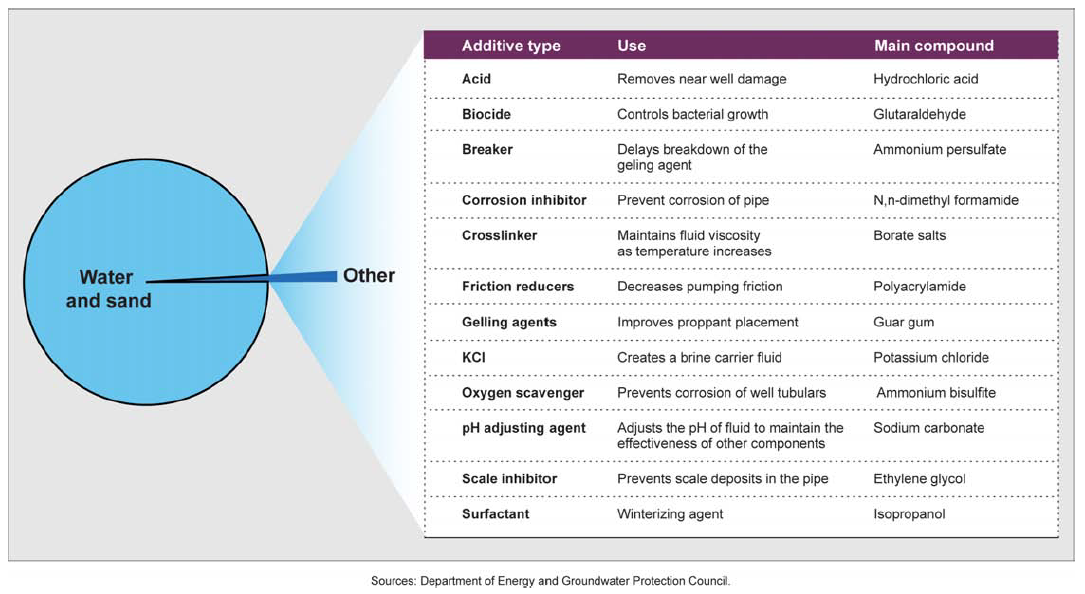

* Hydraulic fracturing or fracking involves injecting fluids at high pressures from the bore of the well into the layer that contains the fossil fuel resources. This process creates fractures in the rock, which allows oil to flow to the bore of the well. The fluids used for fracking typically contain sand or ceramic beads that serve to hold open the fractures after they have been created. This fluid also contains varying chemicals that are used for purposes such as reducing friction and preventing pipe corrosion.[387] [388] [389] (A detailed description of the process is shown in the video below.)

* Hydraulic fracturing was first successfully employed in 1947 and has been used commercially since the 1950s. By 1955, more than 100,000 fracking treatments were performed.[390]

* Since the mid-2000s, technological advancements and market conditions have made it economically worthwhile to extract tight oil by using a combination of horizontal drilling and hydraulic fracturing.[391] [392] [393] [394] [395] [396] The process is shown in this video:

* From 2005 to 2021, U.S. crude oil production increased by 128%, primarily due to the use of horizontal drilling coupled with hydraulic fracturing in tight oil formations.[397] [398] [399] [400] [401] [402] [403]

* In 2021, horizontal drilling coupled with hydraulic fracturing provided about 62% of total crude oil production in the U.S.[404] [405]

* As of 2021, horizontal drilling coupled with hydraulic fracturing has not been widely used to extract tight oil outside the U.S.[406] [407] [408] [409] [410] [411] [412] [413] [414] In 2013, the U.S. Energy Information Administration (EIA) estimated that 10% of worldwide technically recoverable oil resources are located in tight formations.[415]

* For facts about the environmental impacts of horizontal drilling and hydraulic fracturing, visit the fracking section of this research.

* Estimates of crude oil resources are uncertain and subject to change, particularly for tight oil formations.[416] [417] [418]

* Definitions used for estimates of fossil fuel resources include:

* Per the U.S. Energy Information Administration (EIA), it is “misleading” to make assessments about total fossil fuel resources on the basis of proved reserves. This is because:

* In 1955, America’s proved reserves of oil were equal to 11–12 years of U.S. oil consumption at that time.[429]

* In 1977, the U.S. had 31.8 billion barrels of proved crude oil reserves. If this represented all U.S. crude oil resources, the U.S. would have run out of oil in 1988.[430]

* In 1974, Stanford University professor and bestselling author Paul Ehrlich predicted that:

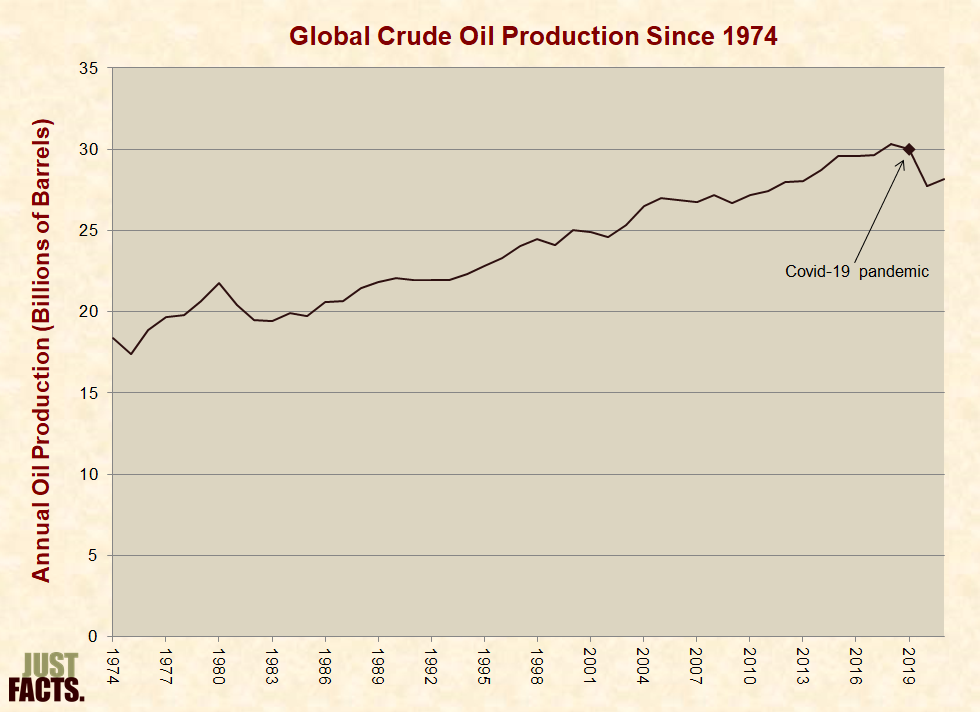

* From 1974 to 2021, annual global production of crude oil rose by 53%:

* As of 2020, EIA estimates that the U.S. has 373 billion barrels of technically recoverable crude oil. This figure does not include:

* 373 billion barrels of technically recoverable crude oil is roughly equivalent to:

* As of 2013, EIA estimates that the world has 3,357 billion barrels of technically recoverable crude oil. This figure does not include several crude oil resources, such as offshore shale oil, shale oil formations in the Middle East and Caspian region, tight sandstone formations, and other formations that have not yet been quantified by EIA.[439]

* 3,357 billion barrels of technically recoverable crude oil is equivalent to 121 years of worldwide petroleum production at the 2013 production rate.[440]

* According to a 2009 estimate by the U.S. Department of Energy, worldwide oil shale reserves, which are not included in the above estimates of technically recoverable crude oil, are equivalent to about 3.7 trillion barrels of crude oil. In 2009, this was roughly 40% more than all other global reserves of petroleum. About two thirds of these oil shale reserves are located in the U.S.[441]

* In 2010, the U.S. Department of the Interior reported that roughly 45% to 80% of oil shale reserves may be technically recoverable.[442]

* The largest known oil shale reserves are located in the Green River Formation, which is situated in southwestern Wyoming, northeastern Utah, and northwestern Colorado.[443] [444]

* In 2013, the U.S. Department of the Interior reported that the Green River Formation contains about 4.3 trillion barrels of oil shale and that roughly 8% to 27% of this has “a high potential for development.”[445] This amounts to:

* Per the U.S. Department of the Interior:

* Compiling the above estimates of technically recoverable crude oil and Green River oil shale with high potential for development:

* Natural gas is a mixture of fossil fuels (mostly methane) that are gaseous at atmospheric pressure and room temperature. Natural gas is sometimes defined differently because certain fossil fuels that are gases inside the earth become liquids when brought to the surface, and because certain natural gases (like propane) are commonly processed into liquids called natural gas liquids.[452] [453] [454]

* The U.S. Energy Information Administration (EIA) typically classifies natural gas liquids as petroleum. Therefore, the above data on petroleum production, consumption, etc. generally includes these natural gas liquids, and the corresponding data below on natural gas generally does not.[455]

* Natural gas is primarily comprised of organic compounds called hydrocarbons, which consist of carbon and hydrogen.[456]

* Natural gas is mainly thought to be formed of diverse marine organisms that were buried by sediments and transformed by heat, pressure, and time.[457] [458] [459]

* Natural gas and crude oil are often found in the same geological formations. In 2021, roughly 11% of all natural gas extracted from the ground in the U.S. came from crude oil wells.[460] [461]

* The first known natural gas well was drilled in China in 211 BC, and the gas was used for drying salt. The first North American natural gas well was drilled in Fredonia, N.Y. in 1821, and the gas was used for lighting and cooking.[462]

* The vast majority of natural gas is currently transported through pipelines. Prior to the early-to-mid 1900s, natural gas was not widely used because it was difficult to transport large amounts of it over long distances. Since then, advances in pipeline technology and infrastructure have made it economical to transport large volumes of natural gas under many conditions.[463] [464] [465]

* In circumstances where pipelines are not practical or cost-effective (like when shipping overseas), it is more expensive to ship natural gas than crude oil, because the density of natural gas is 942 times less than crude oil. When shipping overseas, natural gas is often liquefied by cooling it to –258ºF (–161ºC), which reduces its volume by a factor of 610. During this process, about 8–10% of the gas is consumed to generate the energy to cool the gas to these subzero temperatures.[466] [467] [468] [469]

* Before the widespread construction of pipelines, natural gas produced from oil wells was often discarded through burning it (called flaring) or releasing it into the air (called venting).[470] [471] [472]

* In 1949, 11.3% of natural gas extracted from the ground in the U.S. was vented or flared. By 1971, this figure declined to 1.2%, and since then, it has averaged 0.7%.[473]

* In 2020, 1.5% of U.S. natural gas production was vented or flared.[474] Worldwide in 2020, roughly 3.5% of natural gas production was flared (data on venting is unavailable).[475]

* Natural gas and natural gas liquids are combusted for purposes such as space heating, cooking, and electricity generation. Natural gas liquids are also used as ingredients in wide-ranging products such as plastics, fertilizers, and detergents.[476] [477] [478] [479] [480]

* In 2021, natural gas supplied:

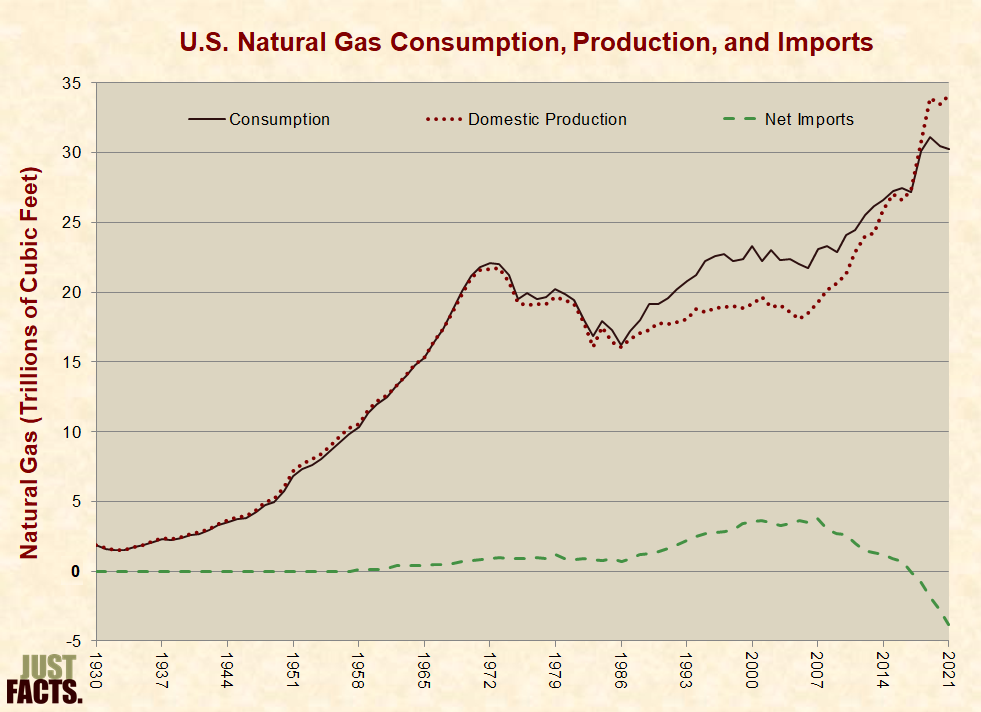

* In 2021, the U.S. produced 34.1 trillion cubic feet of natural gas, consumed 30.3 trillion cubic feet, and had net exports of 3.8 trillion cubic feet:

* In the U.S. from 2007 to 2021, net imports of natural gas declined from 16% of the nation’s consumption to net exports equaling 13% of consumption. This is primarily due to increased domestic production through technologies known as horizontal drilling and hydraulic fracturing (described below):

* Natural gas prices are affected by factors that impact supply and demand, such as economic growth and recessions, weather, and technological advancements.[488] [489] [490] [491] Because natural gas is more difficult to transport than petroleum, natural gas prices are more affected by local and regional factors than petroleum prices, which are primarily driven by global factors.[492] [493] [494] [495] [496]

* In 2021, the average production price for natural gas was roughly $3.78 per thousand cubic feet, and the average price for residential consumers was $12.24 per thousand cubic feet.[497]

* In 2021, natural gas supplied 32% of the primary energy consumed in the U.S. electric power sector.[500] Because certain natural gas power plants are more efficient than coal power plants,[501] [502] and because some electricity is generated outside of the electric power sector, during 2021 natural gas supplied:

* Demand for electricity varies on an hourly, daily, and seasonal basis due to factors such as:

* As shown in the following graph, the terms “baseload” and “peak load” are used to describe the minimum and maximum demands for electricity over a given time period. The term “intermediate load” is used to describe the range between them.[508] [509]

* Natural gas is the dominant energy source for generating intermediate and peak load capacity because natural gas power plants:

* Coal is the dominant energy source for generating baseload capacity because once built, low fuel costs make coal plants inexpensive to run continuously, which is ideal for generating baseload capacity.[515] [516] [517]

* In 2009, natural gas became competitive with coal for generating baseload capacity in some areas of the U.S. This was primarily due to increased domestic natural gas production, which reduced prices. Other factors included increased coal prices, stricter environmental regulations, and expansion of natural gas pipelines.[518] [519] [520] [521]

* Both coal and natural gas are competitive for generating baseload capacity under differing circumstances in different regions of the U.S.[522] [523] [524] [525] [526] [527]

* Due to their higher efficiency, natural gas power plants that employ a technology called “combined cycle” can generate baseload power less expensively than coal plants when natural gas is about equal to or less than 1.5 times the price of coal.[528] [529] [530] In 2021, the average energy-equivalent price paid by electric power plants for natural gas was about 2.5 times the price of coal.[531]

* In 2021, natural gas supplied 4% of the energy used in the U.S. transportation sector.[532]

* Between 2007 and 2013, the combination of increased oil prices, decreased natural gas prices, increased domestic natural gas production, and stricter environmental regulations created incentives to use natural gas more widely for transportation.[533] [534] [535] [536] Steep declines in oil prices since 2014 have made natural gas less competitive as a transportation fuel.[537] [538] [539]

* Other disincentives to the wider use of natural gas in transportation include:

* Per the U.S. Energy Information Administration (EIA):

* In 2012, the only factory-built compressed natural gas car available to non-fleet customers in the U.S. was the Honda Civic Natural Gas.[546] It was the “cleanest internal-combustion vehicle ever tested by the U.S. Environmental Protection Agency.”[547] Compared to a similarly equipped Honda Civic EX, the natural gas model:

* Based on the average nationwide prices of gasoline and compressed natural gas in:

* In 2015, Honda announced it was cancelling the Civic Natural Gas after 2015 due to low gasoline prices and a lack of consumer demand.[555]

* Per Vivek Chandra, a natural gas industry consultant and the author of Fundamentals of Natural Gas:[556]

* Home fueling is possible with natural gas vehicles, but Honda does not recommend this for the Civic Natural Gas because “of moisture and other contaminants inherent in some natural gas supplies, and the inability of some home refueling systems to adequately dry the gas and remove contaminants….”[558]

* Natural gas resources can be grouped into two major categories based upon their accessibility:

* Horizontal drilling involves penetrating the ground vertically (like traditional drilling) and then turning horizontally in order to drill along the layer that contains the fossil fuel resources. This method of drilling exposes more of the fossil fuel resources to the bore of each well, thus increasing yields and decreasing the surface footprint of drilling operations.[565] [566]

* Horizontal drilling was first successfully employed in 1929 and has been used commercially since the late 1980s. By 1990, more than 1,000 horizontal wells were drilled worldwide, almost all for the purpose of extracting crude oil.[568]

* Hydraulic fracturing or fracking involves injecting fluids at high pressures from the bore of the well into the layer that contains the fossil fuel resources. This process creates fractures in the rock, which allows natural gas to flow to the bore of the well. The fluids used for fracking typically contain sand or ceramic beads that serve to hold open the fractures after they have been created. This fluid also contains varying chemicals that are used for purposes such as preventing pipe corrosion.[569] [570] (A detailed description of the process is shown in the video below.)

* Hydraulic fracturing was first successfully employed to drill for oil in 1947 and has been used commercially since the 1950s. By 1955, more than 100,000 fracking treatments were performed. In the 1980s and early 1990s, Texas oilman George Mitchell refined the process of fracking to extract natural gas from shale in a cost-effective manner.[571] [572]

* In the early 2000s, horizontal drilling coupled with hydraulic fracturing became widely used to extract natural gas from shale. In the mid-2000s, the combination of these technologies also became widely used to extract oil from shale.[573] [574] [575] The process is shown in this video:

* From 2005 to 2021, U.S. natural gas production increased by 89%, primarily due to the use of horizontal drilling coupled with hydraulic fracturing in shale formations.[576] [577] [578]

* In 2021, horizontal drilling coupled with hydraulic fracturing provided about 77% of total dry natural gas production in the U.S.[579] [580]

* As of 2021, horizontal drilling coupled with hydraulic fracturing has not been widely used to extract natural gas outside the U.S.[581] [582] [583] [584] [585] [586] [587] In 2013, the U.S. Energy Information Administration (EIA) estimated that 32% of worldwide technically recoverable natural gas resources are located in shale formations.[588]

* For facts about the environmental impacts of horizontal drilling and hydraulic fracturing, visit the fracking section of this research.

* Estimates of natural gas resources are uncertain and subject to change, particularly for shale formations.[589] [590] [591]

* Definitions used for estimates of fossil fuel resources include:

* Per the U.S. Energy Information Administration (EIA), it is “misleading” to make assessments about total fossil fuel resources on the basis of proved reserves because “proved reserves are an accounting concept that is based on known projects, and it is not an appropriate measure for judging total resource availability in the long term.”[598] [599] [600] [601]

* In 1977, the U.S. had 207 trillion cubic feet of proved natural gas reserves. If this represented all U.S. natural gas resources, the U.S. would have run out of natural gas in 1989.[602]

* As of 2020, EIA estimates that the U.S. has 2,926 trillion cubic feet of technically recoverable natural gas. This figure does not include resources located in “areas where drilling is officially prohibited,” and it does not include about 33 trillion cubic feet of offshore natural gas located in areas that are not expected to be drilled.[603]

* 2,926 trillion cubic feet of technically recoverable natural gas is equivalent to:

* As of 2013, EIA estimates that the world has 22,882 trillion cubic feet of technically recoverable natural gas. This figure does not include several natural gas resources, such as offshore shale gas, shale gas formations in the Middle East and Caspian region, and other formations that have not yet been quantified by EIA.[606]

* 22,882 trillion cubic feet of technically recoverable natural gas is equivalent to 159 years of worldwide natural gas production at the 2021 production rate.[607]

* The figures above do not account for methane hydrates, which are “cage-like lattices of water molecules containing methane, the chief constituent of natural gas.” Globally as of 2012, these resources were estimated to be equivalent to 10,000–100,000 trillion cubic feet of natural gas, or 84–837 years of worldwide natural gas production at the 2012 production rate.[608] [609]

* Per EIA, methane hydrates:

* Coal is a class of combustible rocks that are at least 50% carbon by weight.[611] [612]

* Coal is categorized into different “ranks,” primarily depending upon how much of it is comprised of carbon. Coals with higher carbon content generally contain more energy and have a higher rank. The main ranks of coal (from lowest to highest) are lignite, subbituminous coal, bituminous coal, and anthracite.[613] [614] [615] [616]

* Coal is formed of plant materials that have been buried and transformed by pressure, heat, and time.[617]

* Coal may have been used as early as 3,000 years ago to smelt copper in China, and it was used in England for cooking during the era of the Roman Empire. The burning of coal to generate heat became widespread in Europe during the mid-1600s to early 1700s. Coal usage continued to expand and diversify through the 1800s, particularly as fuel for powering steam engines.[618] [619]

* Today, coal is the world’s leading fuel for generating electricity, due to attributes such as low cost and widespread availability.[620] [621]

* More than 90% of the coal produced in the U.S. is used to generate electricity.[622]

* Coal is also:

* Many nations have enacted polices to limit the use of coal in order to reduce greenhouse gases. Based upon these policies and other variables,[627] the U.S. Energy Information Administration projected in 2019 that:

* Coal accounted for 36% of global electricity production in 2021.[629] [630]

* In 2021, coal supplied:

* In 2020, the U.S. had 599 coal-fired electricity generating units located at 284 electric power plants.[633]

* Because coal power plants are less efficient than certain natural gas power plants,[634] [635] and because some electricity is generated outside of the electric power sector, during 2021 coal supplied:

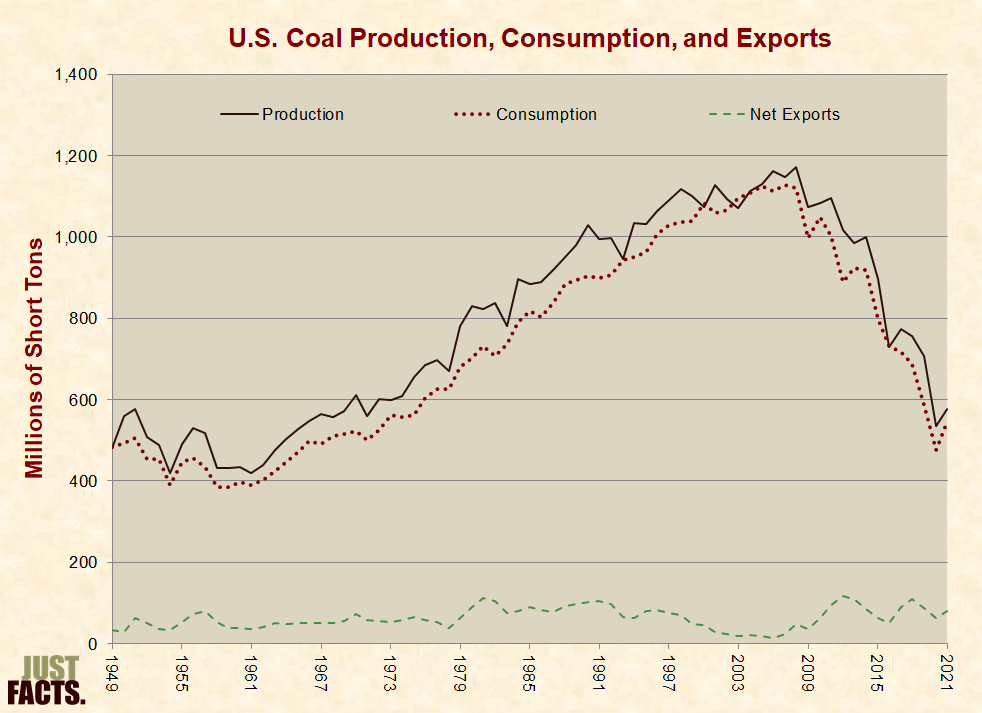

* In 2021, the U.S. produced 577 million short tons of coal, consumed 546 million short tons, and had net exports of 80 million short tons.[639] [640]

* From 2008 to 2021, U.S. coal consumption declined by 52%, primarily as a result of lower natural gas prices and stricter environmental regulations:[641] [642] [643] [644]

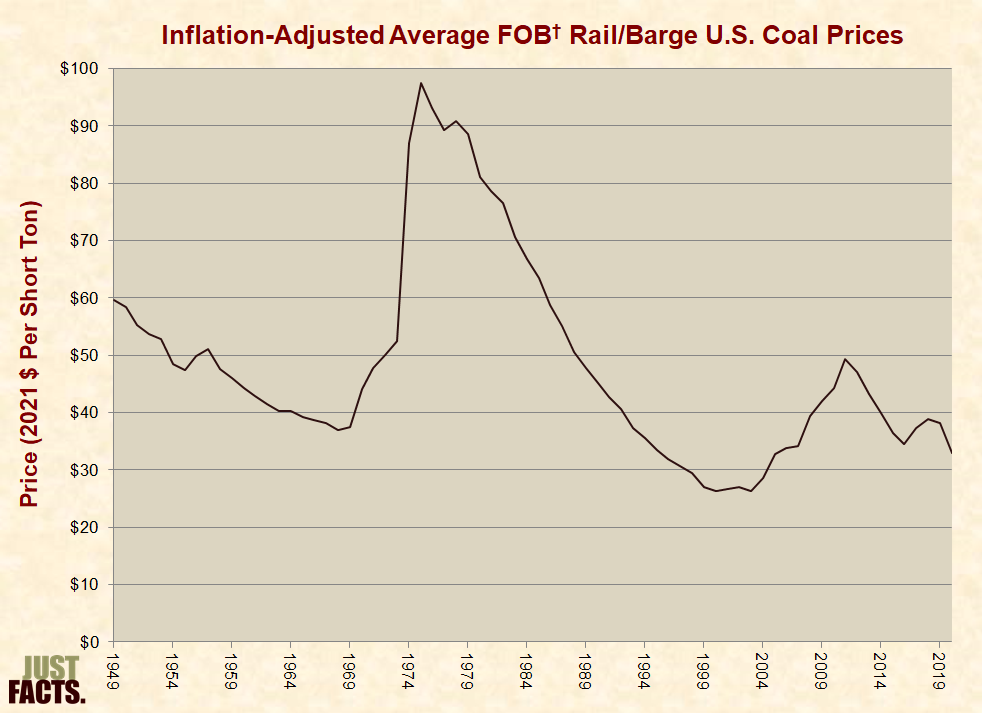

* In 2020, the average domestic price of coal was $31.41 per ton.[646]

|

* Demand for electricity varies on an hourly, daily, and seasonal basis due to factors such as:

* As shown in the following graph, the terms “baseload” and “peak load” are used to describe the minimum and maximum demands for electricity over a given time period. The term “intermediate load” is used to describe the range between them.[652] [653]

* Coal is the dominant energy source for generating baseload capacity because once built, low fuel costs make coal plants inexpensive to run continuously, which is ideal for generating baseload capacity.[655] [656] [657]

* Natural gas is the dominant energy source for generating intermediate and peak load capacity because:

* In 2009, natural gas became competitive with coal for generating baseload capacity in some areas of the U.S. This was primarily due to increased domestic natural gas production, which reduced prices. Other factors included increased coal prices, stricter environmental regulations, and expansion of natural gas pipelines.[662] [663] [664] [665]

* Both coal and natural gas are competitive for generating baseload capacity under differing circumstances in different regions of the U.S.[666] [667] [668] [669] [670] [671]

* Due to their higher efficiency, natural gas power plants that employ a technology called “combined cycle” can generate baseload power less expensively than coal plants when natural gas is about equal to or less than 1.5 times the price of coal.[672] [673] [674] In 2021, the average energy-equivalent price paid by electric power plants for natural gas was about 2.5 times the price of coal.[675]

* In the U.S., coal is mined in two primary ways: surface mining and underground mining. Per the U.S. Department of Energy:

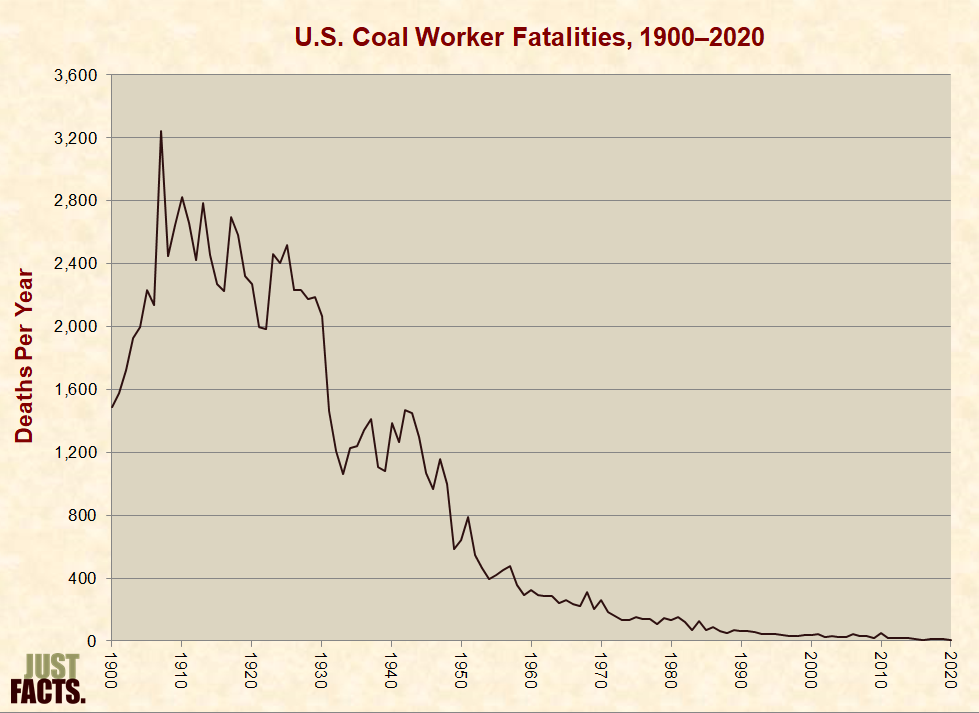

* In 2020, five U.S. coal workers were killed while working.[677] [678] In conjunction with technological advances, improved safety measures, and stricter regulations,[679] [680] coal worker fatalities have declined from a high of 3,242 people in 1907 to a low of 5 people in 2020:

* Per the Encyclopædia Britannica:

* Five countries have about 75% of the world’s coal resources, including:

* In 2020, the U.S. Energy Information Administration estimated that the U.S. has 252 billion short tons of recoverable coal reserves. These resources amount to:

* Based on U.S. Energy Information Administration estimates from 2011, the U.S. had roughly 262 billion short tons of recoverable coal reserves, comprised of 23 billion tons of lignite, 96 billion tons of subbituminous coal, 139 billion tons of bituminous coal, and 4 billion tons of anthracite. These resources amount to:

* Based on U.S. Energy Information Administration estimates from 2021, there were roughly 1.2 trillion short tons of worldwide recoverable coal reserves. These resources amount to 123 years of coal production at the 2022 production rate.[690] [691]

* Nuclear energy is so-named because it is stored in the nuclei of atoms. Through the process of fission, this energy is transformed into heat, which can be used to power steam boilers that drive electricity-generating turbines.[692] [693]

* Uranium is the primary fuel used in nuclear power plants because the process of fission is most easily achieved with elements with heavy nuclei, and uranium is the “heaviest naturally-occurring element available in large quantities.”[694] [695]

* The world’s first controlled nuclear fission reactor was built in the U.S. by Italian physicist Enrico Fermi, and it became operational in 1942.[696] The world’s first nuclear-powered electricity plant was built in the Soviet Union, and it became operational in 1954.[697]

* Through fission, a single pound of uranium can generate as much energy as burning three million pounds of coal.[698]

* In 2021, nuclear energy supplied 8.4% of all primary energy consumed in the United States:

* In 2021, nuclear energy generated 19% of all electricity produced in the U.S.[700]

* Demand for electricity varies on an hourly, daily, and seasonal basis due to factors such as:

* As shown in the following graph, the terms “baseload” and “peak load” are used to describe the minimum and maximum demands for electricity over a given time period. The term “intermediate load” is used to describe the range between them.[704] [705]

* Nuclear power is a major source of baseload capacity because once built, low fuel costs make nuclear plants inexpensive to run continuously, which is ideal for generating baseload capacity.[707] [708] [709]

* Because the products of nuclear fission emit hazardous levels of radiation, generate heat, and could be used in weapons called “dirty bombs,” they must be reprocessed and/or stored in secure locations and cooled.[710] [711] [712] [713] [714] [715]

* Waste and fuel from commercial nuclear power plants cannot accidentally or intentionally be used to produce a nuclear blast. Such explosions require different grades of materials than those used and produced by commercial power plants.[716] [717]

* Nuclear power plant operators must pay up-front fees to the federal government for the future costs of decommissioning of their plants, thus making it impossible for operators to avoid these costs through bankruptcy after the plant closes.[718] [719] [720]

* The Nuclear Waste Policy Act of 1982 required the federal government to:

* A 1987 law directed the federal government to evaluate storing the waste in the Yucca Mountain, which is located on a 230-square mile plot of federal land in the Mojave Desert of southern Nevada:[726] [727]

* Current law limits the amount of fuel that could be stored at Yucca Mountain to 70,000 metric tons, which is equal to about 79% of the nation’s current commercial nuclear waste. Per evaluations performed by the Department of Energy, at least 3–4 times this limit can be safely stored at Yucca.[729] [730] [731] [732]

* At a cost of hundreds of millions of dollars during the 1990s, the U.S. Department of Energy drilled a 5-mile long, 25-feet diameter tunnel into the Yucca Mountain, along with a 2-mile long tunnel that branches off of it.[733] [734] [735]

* A 2002 federal law approved the Yucca site for permanent nuclear waste storage.[736] [737]

* By 2006, Minnesota had banned the construction of new nuclear power plants, and 11 other states had restricted the construction of new plants until certain provisions for long-term disposal of nuclear waste are met.[738] [739] [740]

* In June 2008, the Bush administration Department of Energy (DOE) submitted an application to the Nuclear Regulatory Commission (NRC) for approval to construct a waste repository at Yucca Mountain.[741]

* In March 2009, the Obama administration DOE announced that it was going to terminate the Yucca Mountain repository. Inquiries to DOE by the U.S. Government Accountability Office and Nuclear Regulatory Commission found that the decision “was made for policy reasons, not technical or safety reasons.” Per the Obama administration DOE:

* After this announcement, the Obama administration moved to shut down the Yucca Mountain program by September 2010 by terminating leases and contracts, archiving documents, eliminating the jobs of all federal employees working on the project, and disposing or transferring federal assets used for the project.[744]

* From 1983 to 2011, the federal government spent roughly $15 billion “to evaluate potential nuclear waste repository sites, evaluate the Yucca Mountain site in more depth, and develop and submit the license application for it.”[745]

* From 1983 to 2011, nuclear power plant operators paid more than $30 billion in fees (including earned interest) to the federal government to dispose of nuclear waste. The government used $9.5 billion of these fees “to evaluate potential nuclear waste repository sites, evaluate the Yucca Mountain site in more depth, and develop and submit the license application for it.”[746] [747]

* As of 2021, the U.S. had 88,248 metric tons of commercial nuclear waste, most of which was stored at nuclear power plants.[748] [749] [750] [751] [752]

* Due to a breach of its responsibility to start taking waste from power plants starting in 1998, the federal government has paid $9.0 billion in court-ordered damages and settlements to power plant operators as of September 2021.[753] [754]

* In 2021, the Inspector General of the Department of Energy estimated that the federal government’s total liabilities for breaching this responsibility will amount to $40 billion. The nuclear power industry estimates that it will be at least $50 billion.[755]

* In 2013, a three-judge panel of the District of Columbia Court of Appeals ruled (2–1) that the NRC “was violating federal law by declining to further process the license application” for the Yucca facility. The court ordered the NRC to continue this process.[756] [757]

* After this ruling, the NRC published reports in 2014 and 2016 finding that the Yucca facility could safely store nuclear waste for a million years.[758] [759] [760]

* President Trump’s 2018–2020 budget blueprints called for funding to restart the Yucca Mountain program and provide for interim storage of nuclear waste.[761] [762] [763] [764] [765] [766] [767] [768] These provisions were not included in the budgets passed by Congress and signed by the president.[769] [770] [771]

* After Congress rejected President Trump’s calls for funding the Yucca Mountain program in the previous three years, his 2021 budget blueprint did not request funding for it.[772] [773]

* In 2021, the Biden administration announced that it is “beginning that process” to find a site for long-term nuclear waste storage and that Yucca Mountain is “off the table” as a potential site.[774]

* A commonly utilized measure of radiation dosage is millisieverts (mSv). On average, each person receives 2.4 mSv per year of natural background radiation per year, typically varying from 1 to 13 mSv. Per the United Nations Scientific Committee on the Effects of Atomic Radiation, “sizable population groups receive 10–20 mSv annually” of natural radiation. This does not include any radiation from human activities.[775] [776]

* Over the course of a lifetime, most people receive about 70–700 mSv of radiation from natural sources.[777]

* After tobacco smoke, the second leading cause of lung cancer in the U.S. is radon, a gas that arises from the decay of natural uranium, which is common in rocks and soils. The EPA estimates that 14% of lung cancer deaths in the U.S. are related to radon.[778]

* Due to hot springs that leach a radioactive element from underground, 2,000 residents in the city of Ramsar, Iran, receive up to 260 mSv of natural background radiation per year. Per a 2002 paper in journal Health Physics, preliminary studies indicate an “apparent lack of ill effects among observed populations of these high dose rate areas….”[779]

* Regarding manmade sources of radiation, on average:

* Concentrated (i.e., high-level, high-rate) radiation doses generally cause more harm than the same doses spread out over longer periods of time.[782] Concentrated radiation doses of:

* Two major studies of survivors of the 1945 atomic bombings in Hiroshima and Nagasaki have found increased rates of certain cancers among populations who received concentrated radiation doses below 100 mSv, but none of the results were statistically significant below this level.[784]

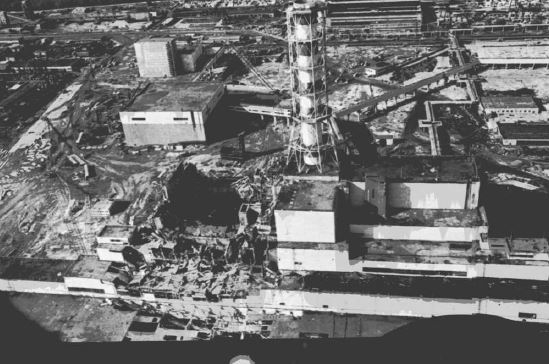

* The largest nuclear power accident in the world occurred in the city of Chernobyl in the Soviet Union in 1986.[785] A picture of the reactor after the accident is shown here:

* Per the official summary of a 2006 three-volume report by the International Atomic Energy Agency, World Health Organization, U.N. Development Programme, Food and Agriculture Organization, U.N. Environment Programme, U.N. Office for the Coordination of Humanitarian Affairs, U.N. Scientific Committee on the Effects of Atomic Radiation, World Bank, and the governments of Belarus, the Russian Federation, and Ukraine:[787]

* Per the “environment” volume of the above-cited 2006 report:

* The second-largest nuclear power accident occurred in March of 2011 at the Fukushima Daiichi nuclear power facility in Japan. A 9.0-magnitude earthquake and resulting tsunami killed roughly 18,500 people, caused $220 billion in damage, and caused explosions and radiation leaks in multiple reactors at the nuclear power facility.[799] [800]

* A 2014 report about the Fukushima nuclear accident by the United Nations Scientific Committee on the Effects of Atomic Radiation found that:

* The largest nuclear power plant accident in the U.S. occurred near Middletown, Pennsylvania at the Three Mile Island nuclear facility in March of 1979.[803]

* As a result of the Three Mile Island accident, the maximum radiation dosage to local residents was less than 1 mSv.[804] [805] [806] Per the U.S. Nuclear Regulatory Commission:

* As of 2014, the U.S. nuclear power industry had accumulated 3,500 reactor-years of operation without any known deaths or injuries to the public.[809]

* The term “biomass” refers to non-fossil organic materials that can be used as energy sources.[810]

* There are three main types of biomass:

* Biomass, particularly wood, was the first inanimate energy source that mankind learned to harness. Up through the Middle Ages, wood remained the primary fuel of civilization.[820]

* The world’s first internal combustion engine ran on a mixture of ethanol and turpentine refined from pine trees. The world’s first diesel engine ran on peanut oil.[821]

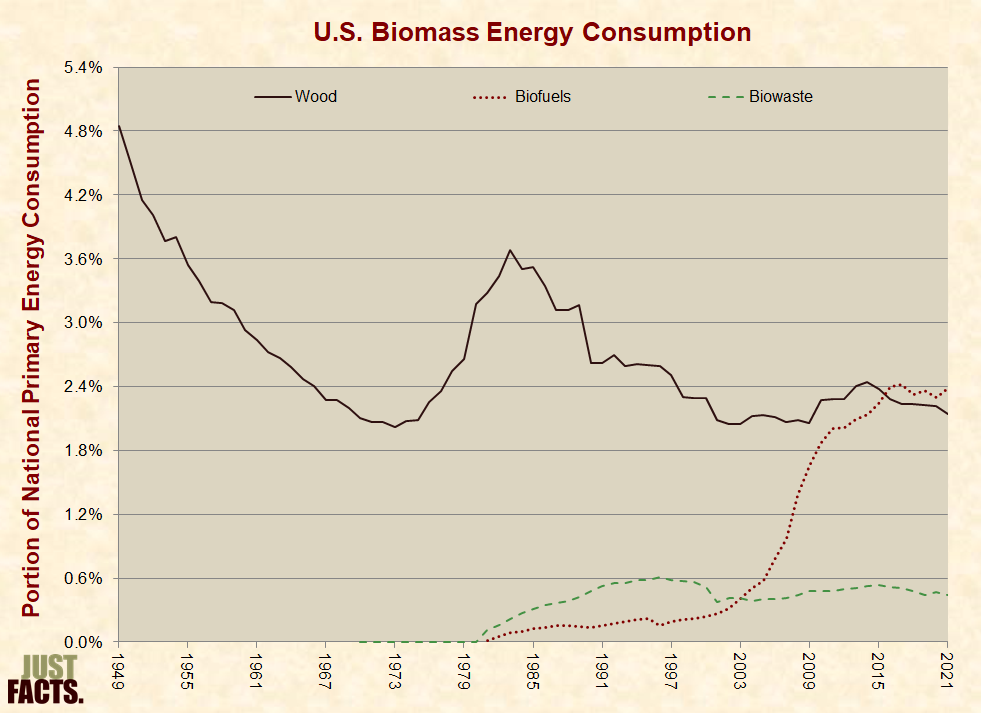

* In 2021, biomass supplied 5.0% of all primary energy consumed in the United States. Biofuels comprised 2.4 percentage points of this total, wood 2.1 percentage points, and biowaste 0.4 percentage point:

* In 2021, biomass supplied:

* Ethanol is the dominant biofuel in the U.S. and globally.[828] [829] [830] [831] [832] [833]

* In late 1970s, the federal government began promoting domestic biofuels by subsidizing the production of domestic ethanol and placing tariffs on ethanol imports.[834]

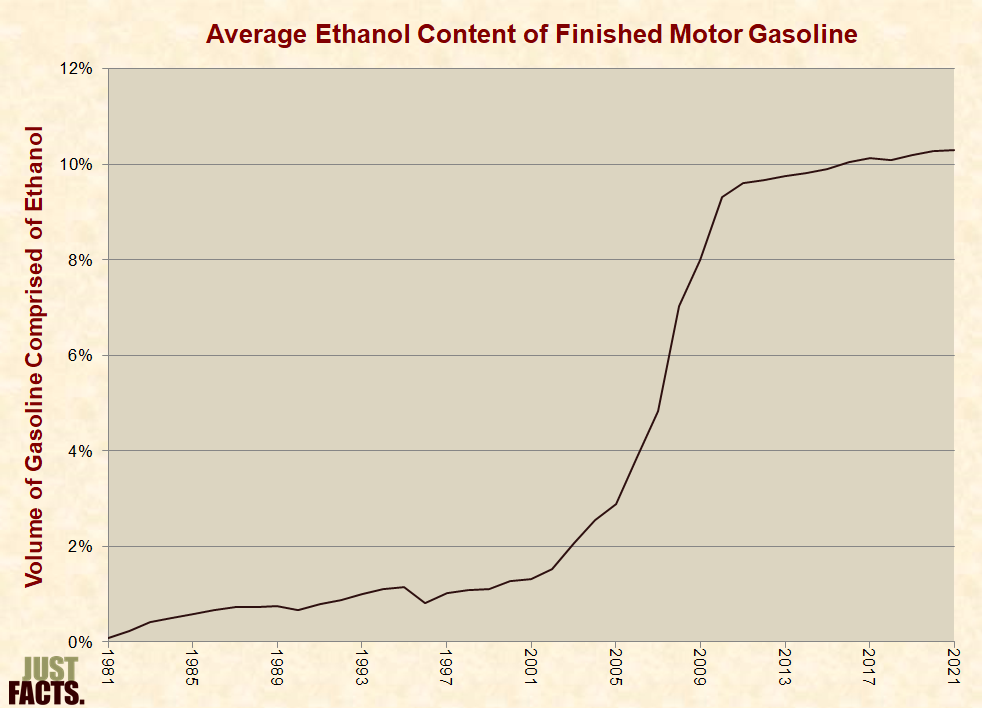

* Federal laws passed in 2005 and 2007 mandate that increasing volumes of biofuels be used in the U.S. transportation sector through 2022.[835] [836] [837] Due primarily to these laws,[838] [839] the portion of automotive fuel that is comprised of ethanol has risen from 2.9% in 2005 to 10.3% in 2021:

* Ethanol is another name for ethyl alcohol or grain alcohol, and it is chemically identical to the intoxicating ingredient in alcoholic beverages.[842] Before shipping ethanol, producers make it unfit for human consumption by adding inedible substances to it.[843]

* Ethanol has higher octane than gasoline, which increases engine power.[844] [845]

* The energy content per unit volume of ethanol is 31% below that of gasoline, which reduces fuel economy and hence vehicle range.[846] [847] [848]

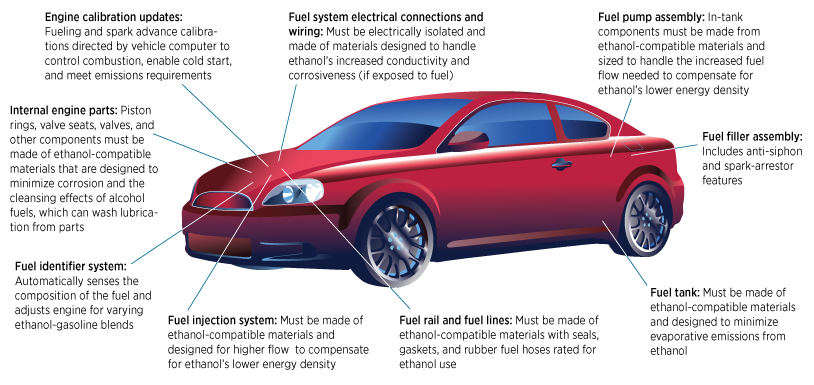

* The elemental differences between ethanol and gasoline restrict the amount of ethanol that can be used in many engines and fuel systems. As compared to gasoline, ethanol:

* Whether or not the above effects occur depends upon the designs of engines and fuel systems, the concentrations of ethanol, exposure timeframes, and other variables such as pressure and temperature.[850]

* Federal law prohibits material changes to automotive fuels and additives without approval from the Environmental Protection Agency (EPA). In 1979, EPA approved the use of automotive fuel comprised of up to 10% ethanol by volume.[851] [852]

* In the late 2000s, a combination of the following factors created a situation in which almost all general-purpose gasoline sold in the U.S. contained 10% ethanol by volume:[853]

* In 2016 nearly all ethanol consumed in the U.S. was used in a fuel called E10, which is a blend of 10% ethanol and 90% gasoline.[858] [859] Per the U.S. Energy Information Administration (EIA):

* In response to the looming blend wall, in 2009 a coalition of ethanol producers petitioned the EPA to allow for general usage of E15, which is a blend of 15% ethanol and 85% gasoline.[862] [863]

* In 2010, EPA approved the use of E15 for model year 2007 and later general-purpose autos, and in 2011 EPA extended this approval to cars with models years of 2001 and later. However, EPA did not approve the use of E15 in older cars, heavy-duty vehicles, motorcycles, boats, lawnmowers, chainsaws, and other nonroad equipment.[864] [865] [866] Per EPA:

* In the wake of EPA’s rulings, the following factors have limited the usage of E15:[868]

* In 2019 the Trump administration issued regulations that allow the year-round sale of E15.[877] [878] Prior to this, E15 could not be sold during summer months due to its potential to increase smog.[879]

* Certain autos called “flex-fuel vehicles” are designed to run on wide-ranging fuel mixtures up to 85% ethanol (E85). In 2012, 4.9% of light duty automobiles could run on E85, and 1.6% of gas stations dispensed E85.[880] [881] [882]

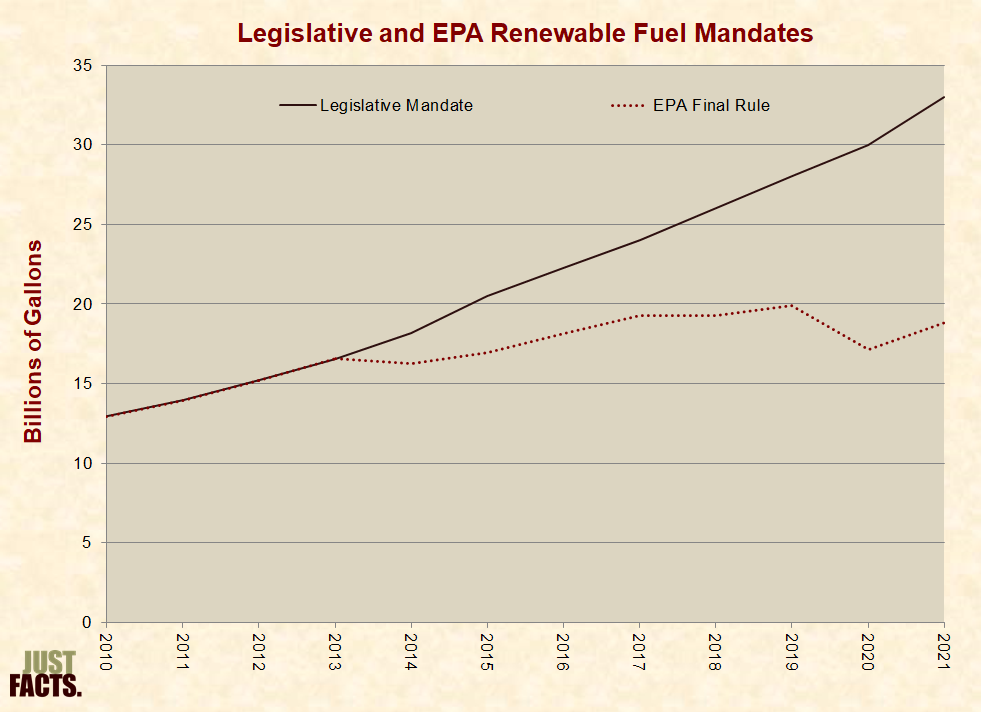

* Due to the blend wall and other practical limitations on the usage of biofuels, the EPA has used its regulatory authority to reduce the amount of biofuels required by federal law from 2014 to 2021:

[883] [884] [885] [886] [887] [888] [889]

* As opposed to petroleum and refined petroleum fuels—which are primarily transported to wholesale terminals via pipelines—ethanol is mainly transported to wholesale terminals by rail, trucks, and barges.[890] Generally, the most economical and safest way to transport liquid fuels is through pipelines,[891] but wide-ranging technical and logistical issues currently prevent most ethanol from being transported in this manner.[892] [893]

* In 2016, EIA reported that biofuel production “often depends heavily on policies or mandates to support growth.”[894]

* In 2020, biofuels accounted for 6% of U.S. liquid fuels production (by volume) and 3% of global liquid fuels production.[895]

* In 2021, EIA projected that by 2050, biofuels will account for 3% of global liquid fuels production.[896] [897] [898]

* Federal law also mandates the usage of biofuels that produce less greenhouse gases than corn-based ethanol. One of these fuels is cellulosic biofuel, which is made from grasses, crop waste, and trees.[899] [900] [901] [902]

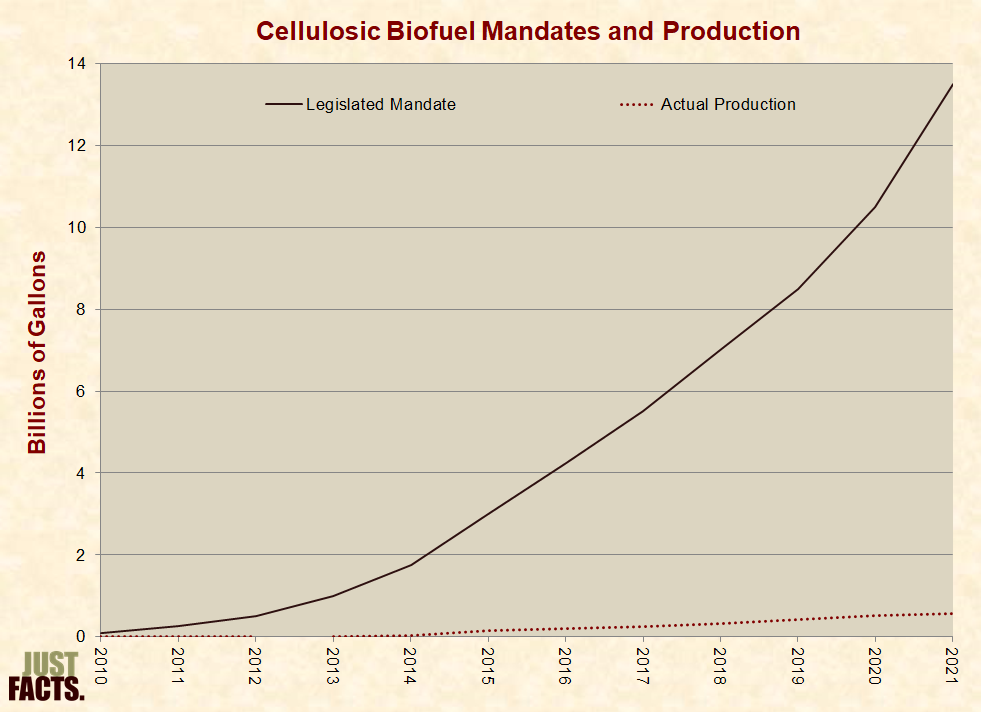

* In 2007, when the mandate for cellulosic biofuels became law, such fuels were not being produced in commercial quantities. The law specifies how much of these fuels are to be used starting in 2010, but before the outset of each year, EPA is required to project how much this fuel will actually be produced and to relax the mandate accordingly.[903] [904] [905]

* For 2010, EPA reduced the law’s cellulosic biofuel mandate by 94%, but none of the fuel was actually produced.[906] [907]

* For 2011, EPA reduced the mandate by 98% and leveled fines of $6.8 million on motor fuel suppliers for failing to use the nonexistent fuel.[908] [909] [910] [911]

* For 2012, EPA reduced the mandate, but a federal appeals court struck it down because EPA had not used a “neutral methodology” to set the mandate.[912]

* In 2007, when the mandate for cellulosic biofuels became law, such fuels were not being produced in commercial quantities. The law specifies how much of these fuels are to be used starting in 2010, but before the outset of each year, EPA is required to project how much this fuel will actually be produced and to relax the mandate accordingly.[913] [914] [915] In the year:

* From 2010 to 2021, the gaps between cellulosic biofuel production and the legislated mandate were as follows:

* In 2013, the EPA qualified a new fuel product (renewable gasoline blendstock) in the cellulosic biofuel class. This product accounted for all cellulosic biofuel production in 2013. The EPA has not published production data for renewable gasoline blendstock since 2014.[924] [925]

* In 2014, the EPA amended its cellulosic biofuel regulations to classify corn kernel fiber as a crop waste.[926]

* In 2014, the EPA amended its cellulosic biofuel regulations to include compressed and liquefied natural gas from renewable sources like landfills and wastewater treatment facilities.[927] [928] From 2014 to 2021, compressed and liquefied natural gas from renewable sources accounted for 96–99% of annual cellulosic biofuel production.[929]

* In 2015, the U.S. Department of Energy reported the results of a government-industry collaboration that produced a “cellulosic ethanol solution that meets the demands of renewable fuel and chemical producers for a cost effective, sustainable, scalable technology.”[930] [931] This technology prompted three companies (DowDuPont, POET, and Abengoa) to open commercial production facilities.[932] [933] [934] The Department of Energy called this “a huge step toward meeting the Department’s goals of”:

* As of September 2022:

* Hydropower is generated by harnessing the energy of moving water. Hydroelectric power plants typically channel water through turbines, thus causing them to spin and produce electricity.[946] [947] [948]

* More than 2,000 years ago, the ancient Greeks used hydropower to grind corn, pump water, and power other types of machinery. The world’s first hydroelectric power plant was built in Appleton, Wisconsin (U.S.A.) and became operational in 1882.[950] [951] [952] [953]

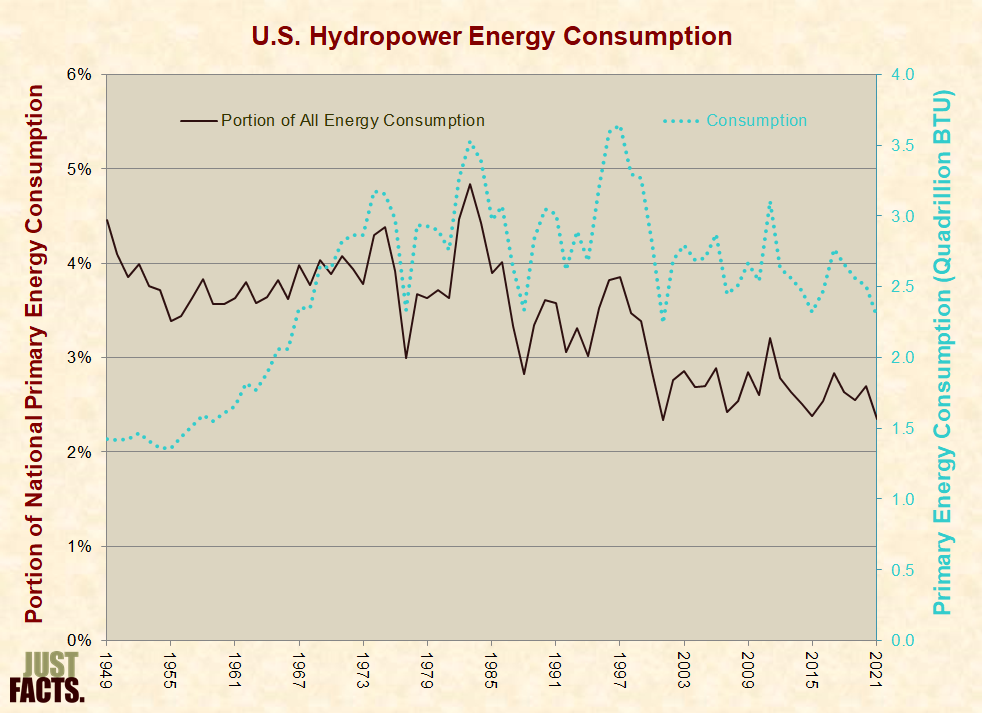

* Hydropower output typically varies from year to year because it is dependent upon rainfall and other elements of climate and weather.[954] In 2021, hydropower supplied 2.3% of all primary energy consumed in the United States:

* In 2021, hydropower generated 6.3% of all electricity produced in the U.S.[956]

* Most large-scale hydroelectric power plants are built on rivers and use a dam to accumulate and release water. This allows the plant to generate varying amounts of electricity as the demand for electricity fluctuates.[957] [958] [959] [960]

* Large-scale hydroelectric power plants that use dams can displace surrounding residents, impede the migration of fish, modify water temperatures, and cause other changes to river ecosystems.[961] [962] [963] [964]

* Per the U.S. Energy Information Administration’s Office of Energy Efficiency & Renewable Energy:

* Roughly 3% of the dams in the U.S. are used to generate hydropower. The rest are primarily used for recreation (38%), flood control (18%), water storage (17%), irrigation (11%), and other purposes (13%).[966] [967] [968]

* A 2012 analysis by Oak Ridge National Laboratory estimated that the U.S. could increase its hydropower generation by 15% through adding hydroelectric generators to existing non-powered dams (NPDs). The analysis “did not consider the economic feasibility of developing each unpowered facility” but noted that:

* Hydroelectric power can also be produced without dams by “run-of-the-river” generators, which temporarily divert a portion of the river through canals or pipes that flow through turbines.[970]

* A 2006 analysis by Idaho National Laboratory estimated that U.S. rivers and streams have an average hydropower potential of 297,436 megawatts. The analysis also estimated that:

* Wind power is harnessed by converting the energy of natural air movements into mechanical energy used to drive electric power generators, pumps, and mills.[973]

* More than 2,000 years ago, the Chinese used windmills to pump water. Around 600 A.D., Persians used windmills to grind grain.[975]

* From 1998 through 2021, the portion of U.S. primary energy supplied by wind grew from 0.03% to 3.4%:

* In 2021, wind generated 9.2% of all electricity produced in the U.S.[977]

* Ideally, commercial wind turbines should be located:

* Wind speeds fluctuate on an hourly, daily, monthly, and seasonal basis. In wind-rich areas, winds are sometimes not strong enough to drive turbines for days at a time.[983] [984] [985] Per the U.S. Energy Information Administration (EIA):

* Power capacity (a commonly cited statistic for wind energy installations[988]) is the amount of electricity that wind turbines produce when operating at full capacity, which occurs when wind conditions are optimal. It is not a measure of actual production.[989] [990] In the U.S. during 2010–2020, actual production from wind turbines was 32% of their power capacity.[991]

* With the exception of pumped hydropower, current technology cannot economically store large quantities of electricity. Thus, utilities must produce enough electricity to meet their customers’ demands on a second-by-second basis.[992] [993] [994] [995] [996] [997] [998]

* Because wind power is intermittent, and utility-scale electricity cannot be easily stored, most wind power capacity must be backed up by other energy sources that can generate electricity on demand, such as natural gas power plants.[999] [1000] [1001] [1002] [1003] [1004] Per EIA:

* As the amount of wind capacity rises in a given region, so do the challenges and costs of backing up its intermittent energy output.[1007] [1008] [1009] [1010] [1011] [1012] Reliance on wind as a major energy source can contribute to electricity blackouts during dangerous weather conditions.[1013] [1014] [1015] [1016] [1017]

* Solar power is harnessed by converting electromagnetic energy from the sun into heat or electricity. The current primary solar energy technologies include:

* In the third century B.C., Greeks and Romans used mirrors to concentrate solar energy for the purpose of lighting torches. In the late 1800s, a French mathematician built the world’s first solar-powered steam engine.[1022]

* In 1953, three U.S. scientists built the world’s first silicon photovoltaic cell. This was the first photovoltaic cell that generated enough energy to power common electrical devices. One year later, Western Electric began selling commercial licenses for silicon photovoltaic technologies.[1023]

* With the exception of nuclear and geothermal power, all major current energy sources ultimately derive from solar energy. Wind energy arises from sunlight heating the atmosphere, biofuels and fossil fuels are made of organic materials that were nourished by sunlight, and hydropower is driven by the hydrological cycle, which is powered by the sun.[1024] [1025] [1026] [1027]

* From 1984 through 2021, the portion of U.S. primary energy supplied by solar power grew from 0.0001% to 1.5%:

* In 2021, solar energy produced 3.9% of all electricity generated in the U.S.[1029]

* From 1998 to 2014, the average reported installed price for residential and commercial PV systems declined by about 6–12% per year.[1030]

* From 2000 to 2020, the median installed price for residential PV systems declined yearly on average by 6%.[1031]

* From 2007 to 2020, the median installed price for utility-scale PV systems declined yearly on average by 13%.[1032]

* Over the past two decades, residential and commercial PV system price declines were due primarily to technological advancements, economies of scale, and government subsidies.[1033] [1034] [1035] [1036] [1037] [1038] [1039]

* In 2009, Jeffrey Punton of Rochester, N.Y. installed 20 solar panels at his home for a cost of $42,480. The federal government and state of New York paid for $29,504 or 69% of these costs.[1040] Per a 2012 report by Lawrence Berkeley National Laboratory:

* Power capacity (a commonly cited statistic for solar energy installations[1042]) is the amount of electricity that solar systems produce when operating at full capacity, which occurs when the sun is directly overhead, the solar panels are perpendicular to the sunlight, the sky is clear, and temperatures are low. It is not a measure of actual production.[1043] [1044] [1045] In the U.S. during 2010–2020, actual production from utility-scale solar systems was 20% of their power capacity.[1046]

* With the exception of pumped hydropower, current technology cannot economically store large quantities of electricity. Thus, utilities must produce enough electricity to meet their customers’ demands on a second-by-second basis.[1047] [1048] [1049] [1050] [1051] [1052] [1053]

* Because solar panels only generate electricity when the sun is shining, and utility-scale electricity cannot be easily stored, most solar power capacity must be backed-up by other energy sources that can generate electricity on demand, such as natural gas power plants.[1054] [1055] [1056] [1057] [1058]

* As the amount of solar capacity rises in a given region, so do the costs of backing up its intermittent energy output.[1059] [1060] [1061] Reliance on solar as a major energy source can contribute to electricity blackouts during dangerous weather conditions.[1062] [1063] [1064] [1065] [1066]

* Geothermal energy is harnessed by transferring heat from or to the earth. The current main geothermal technologies include:

* Since ancient times, people have used hot springs for bathing, cooking, and heating.[1072]

* The world’s first electricity-generating geothermal plant was built in 1904 in Tuscany, Italy.[1073]

* From 1960 through 2021, the portion of U.S. primary energy supplied by geothermal power grew from 0.001% to 0.2%:

* In 2021, geothermal generated 0.4% of all electricity produced in the U.S.[1075]

* Electricity-generating geothermal plants are typically built at sites where geothermal reservoirs are not buried too deeply. In the U.S., such resources are mostly in the western states and Hawaii.[1076] [1077]