Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

* Income is “a flow of purchasing power” that comes from work, investments, and other sources, like government benefits.[1] [2]

* Per the Organization for Economic Cooperation and Development:

* Some common measures of income in the U.S. are reported by federal agencies, including the Census Bureau, the Congressional Budget Office, the Bureau of Labor Statistics, the Bureau of Economic Analysis, the Internal Revenue Service, and the Federal Reserve.[4] [5] [6] [7] [8] [9]

* Different methods of income measurement can lead to conflicting conclusions about people’s economic conditions.[10] [11] [12] [13]

* The Census Bureau has 17 definitions of income, and other agencies use differing measures.[14] [15] [16] [17] Each has strengths and weaknesses, such as the following:

* To gain a broader understanding of people’s economic status, it is sometimes helpful to examine multiple measures, such as income, wealth, and consumption.[37]

* Analysts often group people into brackets according to their income, such as the lowest 20%, the middle 20%, and the highest 20%. The middle group is considered to be “middle class.” Median income—“the amount which divides the income distribution into two equal groups, one having incomes above the median, and the other having incomes below the median”—is another common way to define the middle class.[38] [39] [40]

* Comparisons of income groups over time often do not represent the experiences of specific people. This is because people typically move through life stages in which their income varies significantly, causing them to move in and out of different income groups.[41] [42]

* Unless otherwise stated, all international comparisons of income in this research are provided in “purchasing power parities,” or PPPs. Purchasing power parities allow for accurate measures of economic data across countries because they account for the prices of goods and services in different nations. Thus, an apple in one nation is counted the same as an apple in another.[43] [44] [45]

* In keeping with Just Facts’ Standards of Credibility, all charts in this research show the full range of available data, and all facts are cited based upon availability and relevance, not to slant results by singling out specific years that are different from others.

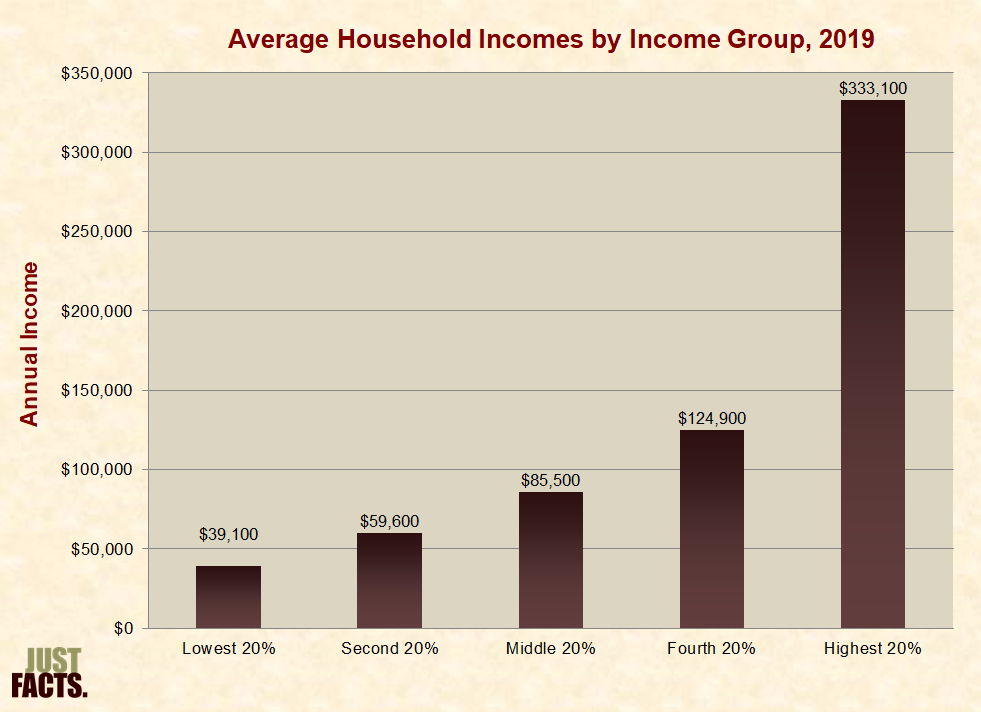

* According to data from the Congressional Budget Office, U.S. households had an average income of $125,500 in 2019 prior to the Covid-19 pandemic.[46] This includes income sources like wages, salaries, capital gains, rental income, and untaxed government and employer-provided benefits like food stamps and health insurance. This varied by income group as follows:

* According to data from the Congressional Budget Office, U.S. households had an average income of $133,000 in 2020 amid Covid-19 government lockdowns and intensified social spending:[49] [50] [51]

* From 1979 to 2019 (prior to the Covid-19 pandemic,[54]) the inflation-adjusted average income of U.S. households increased by $54,300 or 76%. This varied by income group as follows:

|

Inflation-Adjusted Household Income |

||||

|

Income Group |

1979 |

2019 |

Increase From 1979 to 2019 |

|

|

Dollars |

Percent |

|||

|

Lowest 20% |

$21,500 |

$39,100 |

$17,600 |

82% |

|

Second 20% |

$40,200 |

$59,600 |

$19,400 |

48% |

|

Middle 20% |

$60,600 |

$85,500 |

$24,900 |

41% |

|

Fourth 20% |

$82,000 |

$124,900 |

$42,900 |

52% |

|

Highest 20% |

$155,100 |

$333,100 |

$178,000 |

115% |

|

Top 1% |

$595,300 |

$1,998,700 |

$1,403,400 |

236% |

|

All Groups |

$71,200 |

$125,500 |

$54,300 |

76% |

* From 1979 to 2020 (amid Covid-19 government lockdowns and intensified social spending,[57] [58] [59]) the inflation-adjusted average income of U.S. households increased by $61,000 or 85%. This varied by income group as follows:

|

Inflation-Adjusted Household Income |

||||

|

Income Group |

1979 |

2020 |

Increase From 1979 to 2020 |

|

|

Dollars |

Percent |

|||

|

Lowest 20% |

$21,800 |

$42,200 |

$20,400 |

94% |

|

Second 20% |

$40,700 |

$63,600 |

$22,900 |

56% |

|

Middle 20% |

$61,300 |

$90,500 |

$29,200 |

48% |

|

Fourth 20% |

$82,900 |

$131,800 |

$48,900 |

59% |

|

Highest 20% |

$156,800 |

$360,900 |

$204,100 |

130% |

|

Top 1% |

$602,000 |

$2,291,800 |

$1,689,800 |

281% |

|

All Groups |

$72,000 |

$133,000 |

$61,000 |

85% |

* After federal taxes, the inflation-adjusted average income of U.S. middle-income households rose from $49,700 in 1979 to $84,300 in 2020, or by $34,600 or 70%:

[62] [63] [64] [65] [66] [67] [68]

* After federal taxes, the inflation-adjusted average income of U.S. households rose by $46,800 or 84% during 1979 to 2019 (prior to the Covid-19 pandemic.[69]) This varied by income group as follows:

|

Inflation-Adjusted Household Income After Federal Taxes |

||||

|

Income Group |

1979 |

2019 |

Increase From 1979 to 2019 |

|

|

Dollars |

Percent |

|||

|

Lowest 20% |

$20,100 |

$38,900 |

$18,800 |

94% |

|

Second 20% |

$34,300 |

$54,900 |

$20,600 |

60% |

|

Middle 20% |

$49,100 |

$74,800 |

$25,700 |

52% |

|

Fourth 20% |

$64,300 |

$104,400 |

$40,100 |

62% |

|

Highest 20% |

$113,100 |

$252,100 |

$139,000 |

123% |

|

Top 1% |

$386,700 |

$1,398,500 |

$1,011,800 |

262% |

|

All Groups |

$55,600 |

$102,400 |

$46,800 |

84% |

* After federal taxes, the inflation-adjusted average income of U.S. households rose by $56,500 or 101% during 1979 to 2020 (amid Covid-19 government lockdowns and intensified social spending.[73] [74] [75]) This varied by income group as follows:

|

Inflation-Adjusted Household Income After Federal Taxes |

||||

|

Income Group |

1979 |

2020 |

Increase From 1979–2020 |

|

|

Dollars |

Percent |

|||

|

Lowest 20% |

$20,300 |

$45,800 |

$25,500 |

126% |

|

Second 20% |

$34,700 |

$63,200 |

$28,500 |

82% |

|

Middle 20% |

$49,700 |

$84,300 |

$34,600 |

70% |

|

Fourth 20% |

$65,000 |

$115,100 |

$50,100 |

77% |

|

Highest 20% |

$114,300 |

$275,700 |

$161,400 |

141% |

|

Top 1% |

$391,000 |

$1,605,400 |

$1,214,400 |

311% |

|

All Groups |

$56,200 |

$112,700 |

$56,500 |

101% |

* The two main categories of income are:

* Private charities provide other sources of non-cash income to low-income people. These include but are not limited to food, clothing, housing, and healthcare.[81] [82] [83] [84]

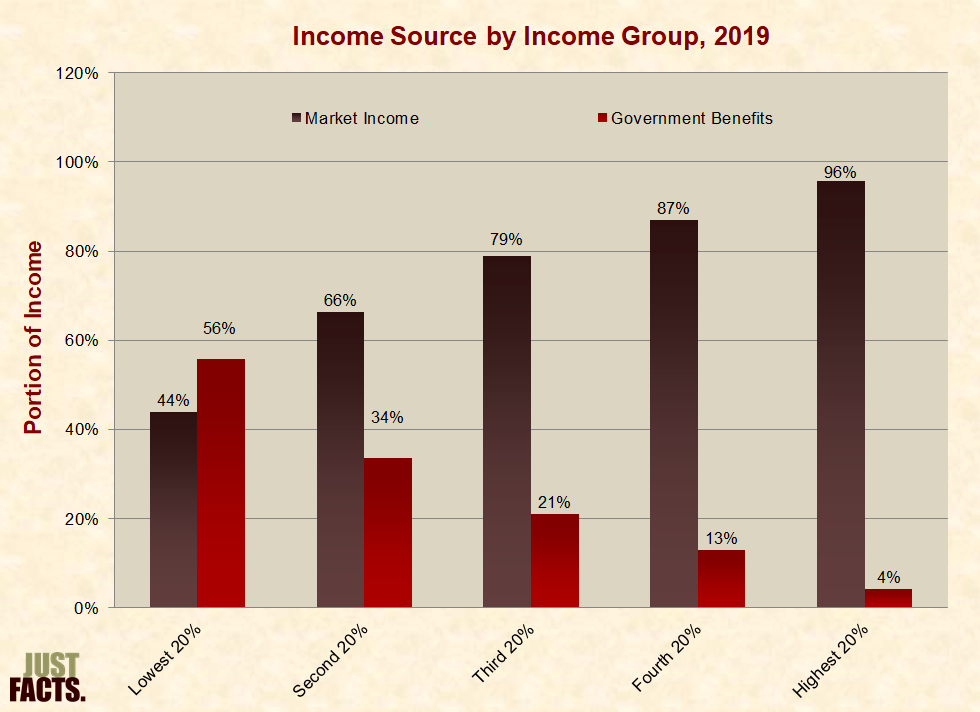

* According to data from the Congressional Budget Office, U.S. households obtained about 86% of their income from the market and 14% from the government in 2019 prior to the Covid-19 pandemic.[85] This varied by income group on average as follows:

* According to data from the Congressional Budget Office, U.S. households obtained about 82% of their income from the market and 18% from the government in 2020 amid Covid-19 government lockdowns and intensified social spending.[88] [89] [90] This varied by income group on average as follows:

* From 1979 to 2019 (prior to the Covid-19 pandemic,[93]) government benefits rose from 9% of total household income to 14%, or by 60%. This varied by income group as follows:

|

Average Portion of Household Income From Government Benefits |

||||

|

Income Group |

1979 |

2019 |

Change |

|

|

Percentage Points |

Percent |

|||

|

Lowest 20% |

51% |

56% |

5 |

9% |

|

Second 20% |

19% |

34% |

15 |

77% |

|

Middle 20% |

8% |

21% |

13 |

155% |

|

Fourth 20% |

5% |

13% |

8 |

168% |

|

Highest 20% |

2% |

4% |

2 |

74% |

|

All Groups |

9% |

14% |

5 |

60% |

* From 1979 to 2020 (amid Covid-19 government lockdowns and intensified social spending,[96] [97] [98]) government benefits rose from 9% of total household income to 18%, or by 100%. This varied by income group as follows:

|

Average Portion of Household Income From Government Benefits |

||||

|

Income Group |

1979 |

2020 |

Change |

|

|

Percentage Points |

Percent |

|||

|

Lowest 20% |

51% |

64% |

13 |

25% |

|

Second 20% |

19% |

42% |

23 |

120% |

|

Middle 20% |

8% |

27% |

19 |

227% |

|

Fourth 20% |

5% |

16% |

12 |

241% |

|

Highest 20% |

2% |

5% |

2 |

99% |

|

All Groups |

9% |

18% |

9 |

100% |

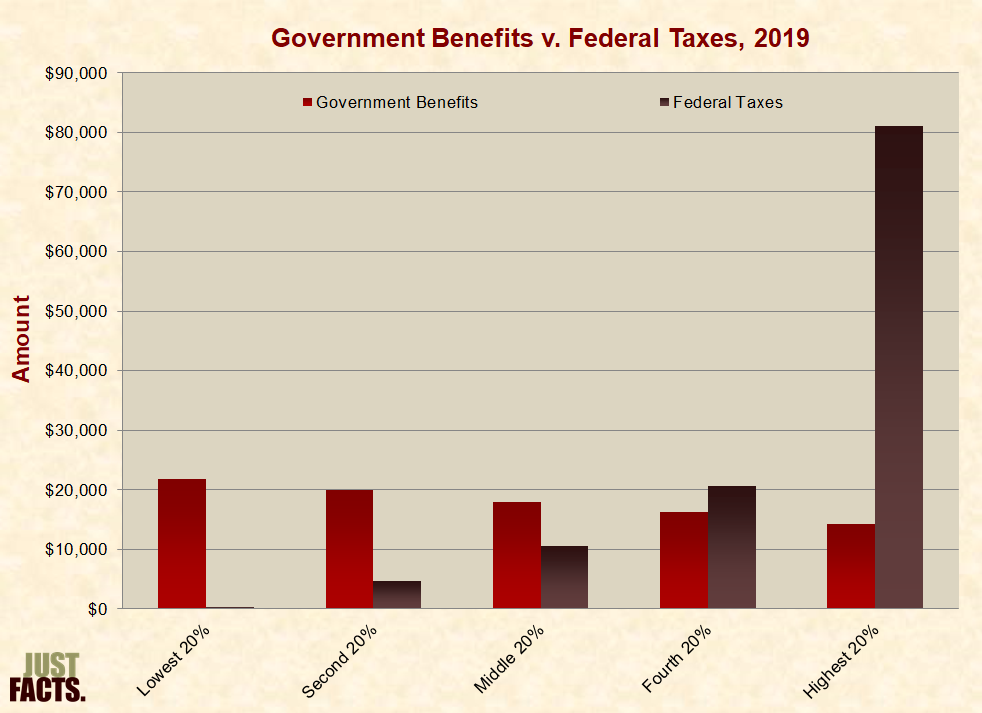

* In 2019, prior to the Covid-19 pandemic,[101] roughly 60% of U.S. households received more in federal, state, and local government benefits than they paid in federal taxes:

* In 2020, amid Covid-19 government lockdowns and intensified social spending,[105] [106] [107] roughly 80% of U.S. households received more in federal, state, and local government benefits than they paid in federal taxes:

* In 1979, only the lowest-income 20% of U.S. households and the second lowest 20% received more in federal, state, and local government benefits than they paid in federal taxes. Since then, the following households have also moved into this territory:

* Government benefits can suppress market income by:

* According to data from the Congressional Budget Office, cash wages and salaries accounted for 62% of market income to U.S. households in 2020. Capital and business income provided 29%, and employer-paid benefits made up the remaining 8%. This varied by income group as follows:

* According to data from the Congressional Budget Office, benefits paid by employers accounted for 11% of middle-income worker compensation in 1979. By 2020, this figure had risen to 15%. This varied by income group as follows:

|

Portion of Worker Compensation in Benefits |

||

|

Income Group |

1979 |

2020 |

|

Lowest 20% |

11% |

14% |

|

Second 20% |

12% |

15% |

|

Middle 20% |

11% |

15% |

|

Fourth 20% |

10% |

14% |

|

Highest 20% |

9% |

10% |

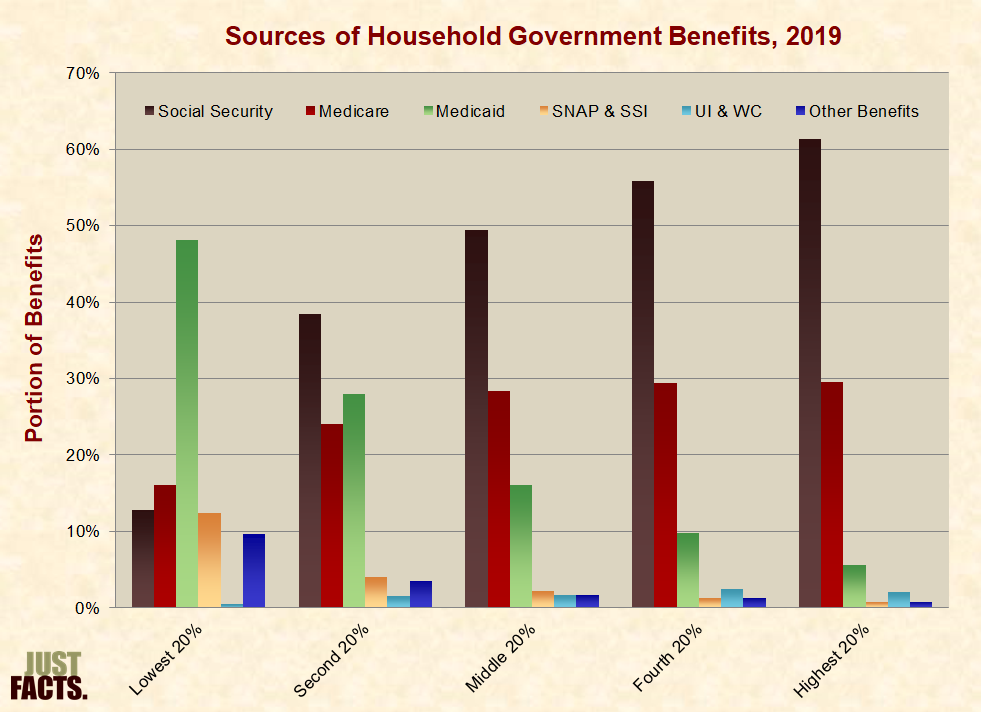

* The two largest sources of household government income are Social Security and Medicare, both of which benefit elderly and disabled people.[132] [133] [134]

* In June of 2021, 65.0 million people—20% of the U.S. population—received Social Security benefits.[135]

* In 2021, 63.8 million people—19% of the U.S. population—received Medicare benefits.[136]

* According to data from the Congressional Budget Office, in 2019 prior to the Covid-19 pandemic:[137]

* According to data from the Congressional Budget Office, in 2020 amid Covid-19 government lockdowns and intensified social spending:[142] [143] [144]

* “Personal consumption” is a comprehensive measure of the goods and services consumed by households. In the United States, consumption is recorded by the federal government’s Bureau of Economic Analysis and includes all material resources:

* Per the World Bank:[152]

* Per a 2003 paper in the Journal of Human Resources:

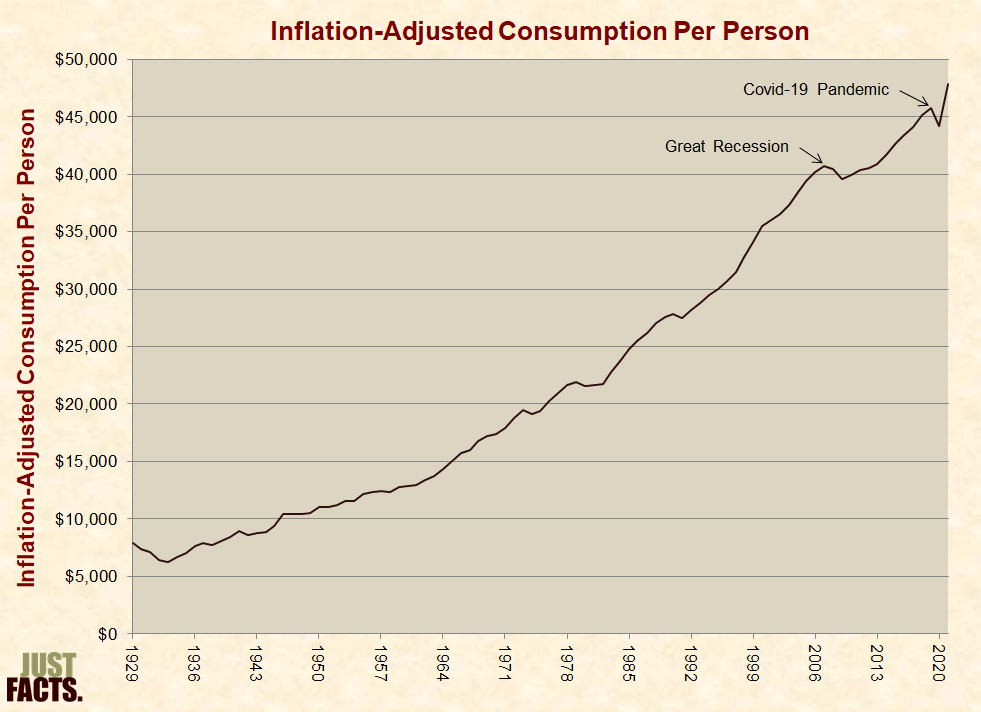

* In the United States from 1929 to 2021, the average inflation-adjusted consumption per person rose by 5.1 times:

* Most U.S. households—especially lower-income ones—consume more goods and services than revealed by common measures of income.[160] [161] [162] This is because widely used income measures, like the Census Bureau’s “money income”:

* With regard to the exclusion of noncash benefits from common income measures:

* With regard to the underreporting of income on government household surveys:

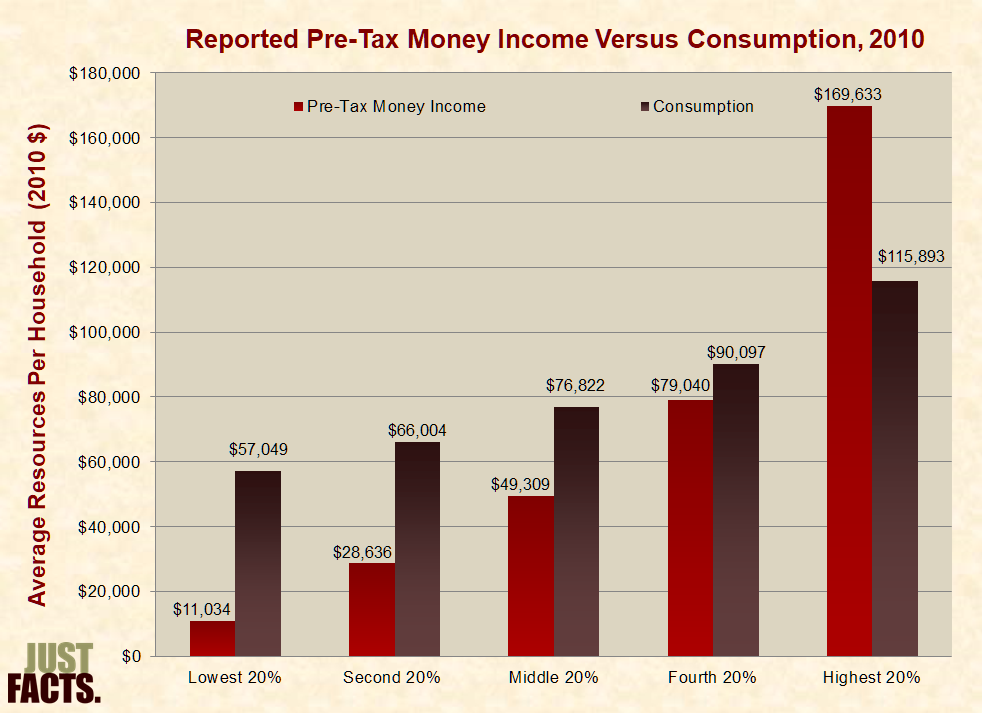

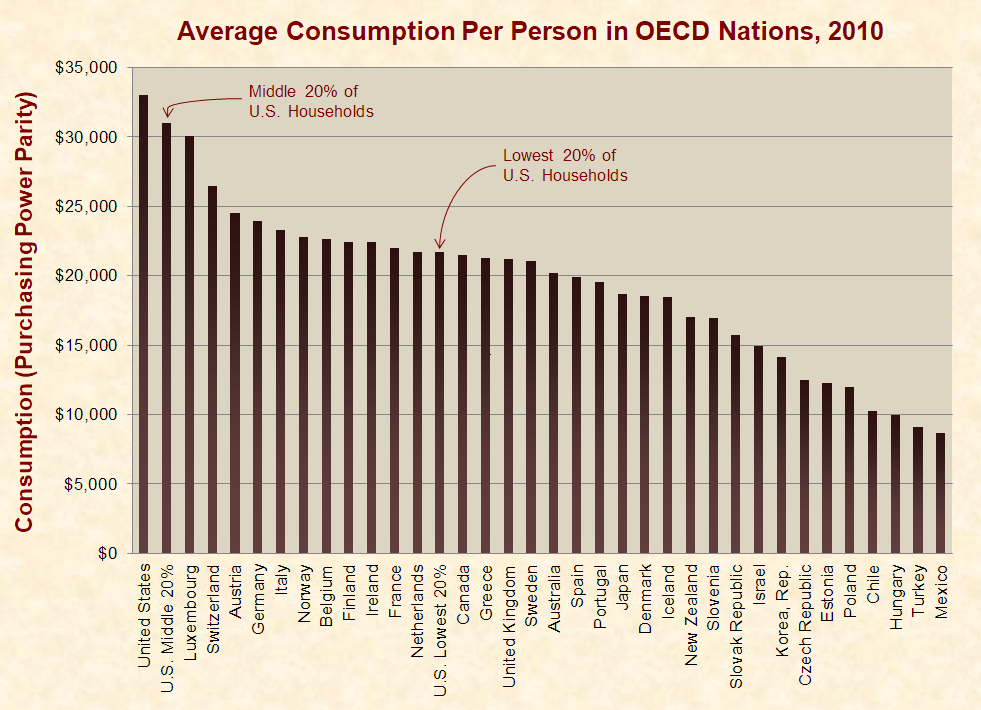

* The U.S. Bureau of Economic Analysis normally reports consumption for the entire nation and doesn’t break down the data to show how people at different levels fare. However, it published a report in 2012 that does that for 2010.[204]

* In 2010, the poorest 20% of U.S. households consumed on average of $57,049 of goods and services per household, while they reported an average of $11,034 in pre-tax money income. For other households, the amounts varied as follows:

* The U.S. Bureau of Labor Statistics collects data on a subset of consumption called “consumer expenditures.” This includes all direct purchases by households, including those made with the proceeds of government benefits like cash welfare and food stamps. However, it excludes goods and services received but not directly purchased by households, such as Medicaid, Medicare, housing subsidies, school lunches, and employer-provided health insurance.[207] [208] [209] [210] [211] [212]

* The Department of Labor collects data on consumer expenditures via household surveys.[213] Per the U.S. Bureau of Economic Analysis, such surveys “have issues with recalling income and expenditures and are subject to deliberate underreporting of certain items.”[214] [215]

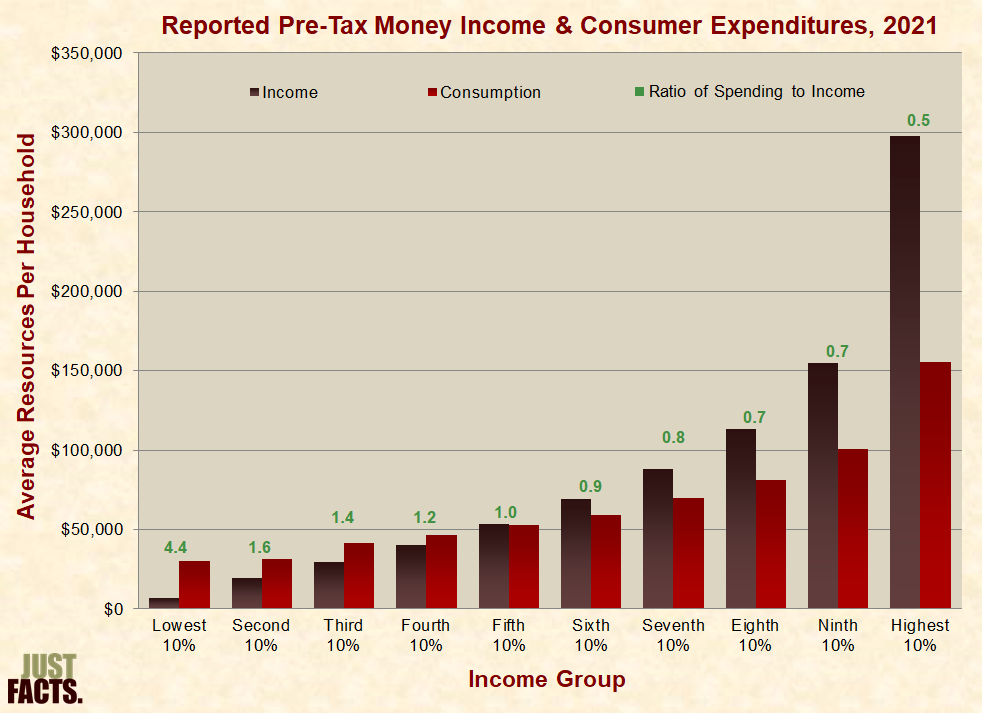

* The average consumer expenditures of the poorest 10% of U.S. households are 4.4 times their reported, before-tax, money income. The ratios of spending to income for other groups varied as follows:

* The Department of Labor explains that consumers can temporarily spend more than their income by borrowing or “drawing down savings and investments.”[218] Thus, some people in the lowest income group “have expenditures that are more typical of upper-income consumers.”[219]

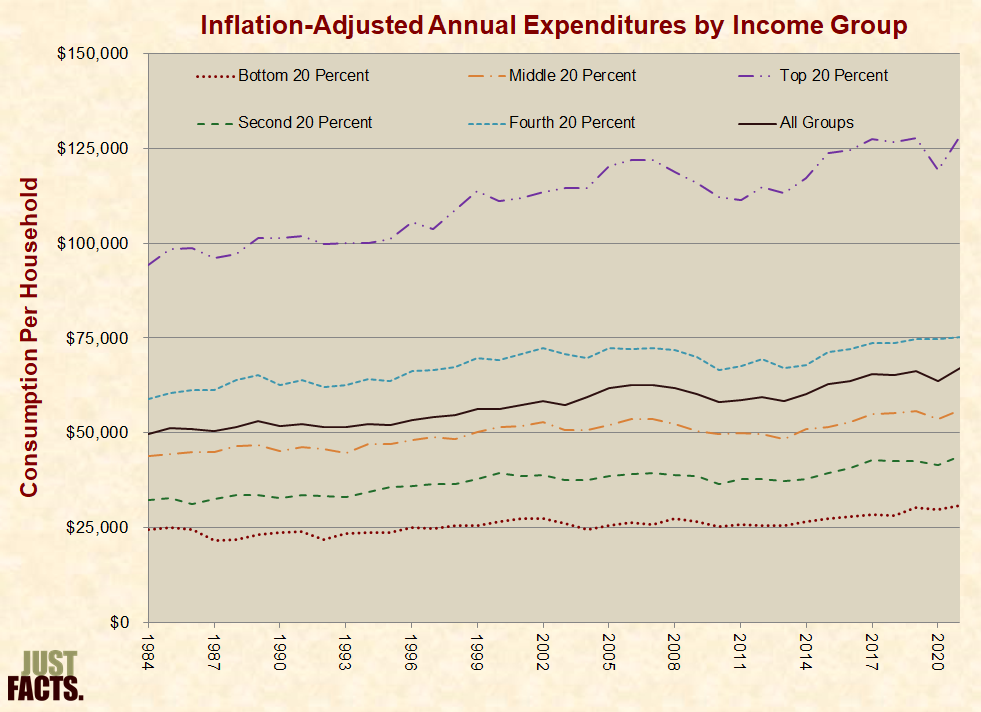

* From 1984 to 2021, the average inflation-adjusted consumer expenditures per household varied as follows:

* From 1984 to 2021, the average inflation-adjusted consumer expenditures of the bottom 20% of households increased by $6,306. This gain closed the 1984 gap between the bottom 20% and the next income group by 81%. The gap closures between the other groups varied as follows:

|

Inflation-Adjusted Consumer Expenditures |

|||

|

Income Group |

Year |

Portion of 1989 Gap Closed |

|

|

1984 |

2021 |

||

|

Bottom 20 Percent |

$24,563 |

$30,869 |

81% |

|

Second 20 Percent |

$32,326 |

$43,918 |

100% |

|

Middle 20 Percent |

$43,897 |

$55,914 |

80% |

|

Fourth 20 Percent |

$58,934 |

$75,284 |

46% |

|

Top 20 Percent |

$94,304 |

$128,213 |

– |

* Per the U.S. Bureau of Labor Statistics, “consumption patterns indicate the priorities that families place on the satisfaction of the following needs”:

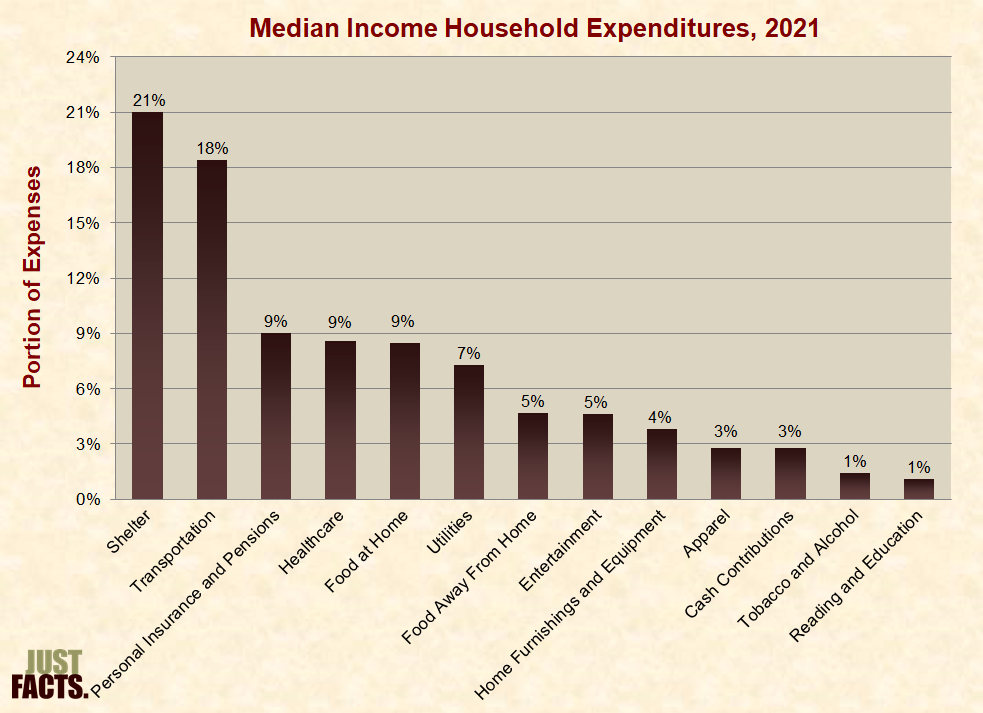

* In 2021, households spent 21% of their consumer expenditures on shelter:

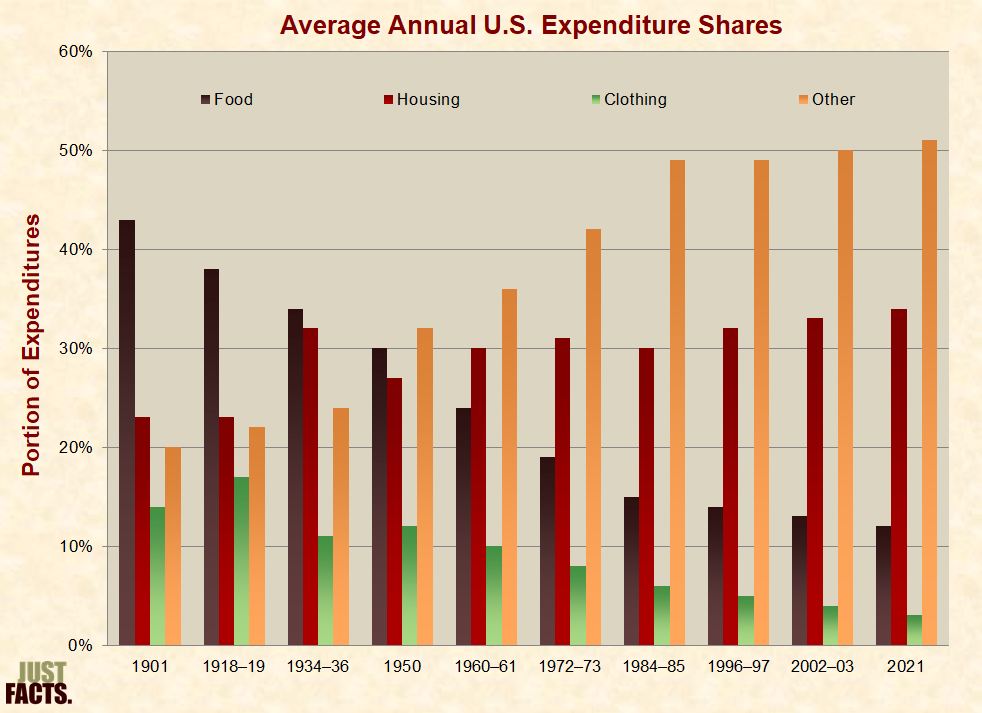

* In 1901, U.S. households spent 43% of their income on food. By 2021, spending on food had decreased to 12% of income. The spending levels for other expenses varied as follows:

* Per a 2006 report by the Bureau of Labor Statistics:

* In 2020, 88% of U.S. homes had air conditioning. The average usage or possession rates for air conditioning and other appliances varied by income group as follows:

|

Average Usage or Possession Rates by Income Group |

||||

|

Income Group |

Appliance |

|||

|

Air Conditioning |

Dishwasher |

Clothes Washer |

Clothes Dryer |

|

|

Less than $20,000 |

80% |

38% |

61% |

58% |

|

$20,000 to $40,000 |

87% |

61% |

80% |

78% |

|

$40,000 to $60,000 |

88% |

72% |

85% |

84% |

|

$60,000 to $100,000 |

90% |

83% |

90% |

90% |

|

$100,000 to $150,000 |

93% |

90% |

93% |

93% |

|

$150,000 or More |

93% |

95% |

95% |

94% |

|

All Homes |

88% |

73% |

84% |

83% |

* As of 2020, 93% of U.S. homes had internet access. The average usage and possession rates for different types of electronic devices and services varied by income as follows:

|

Average Usage or Possession Rates by Income Group |

||||

|

Income Group |

Electronic Device or Service |

|||

|

Primary TV 40” or Larger |

Cable & Digital Video Recorder |

Internet Access |

Smartphone |

|

|

Less than $20,000 |

53% |

20% |

76% |

72% |

|

$20,000 to $40,000 |

65% |

29% |

89% |

80% |

|

$40,000 to $60,000 |

71% |

33% |

95% |

89% |

|

$60,000 to $100,000 |

77% |

37% |

98% |

94% |

|

$100,000 to $150,000 |

80% |

40% |

99% |

96% |

|

$150,000 or More |

85% |

47% |

100% |

98% |

|

All Homes |

72% |

34% |

93% |

88% |

* Gross domestic product (GDP) is the standard measure of nations’ economic output. It is equal to the value of all goods and services that a country produces in a year minus the resources used to produce them. GDP is defined by the equation: Hours worked × Labor productivity.[233] [234]

* GDP divided by the population is often used to measure a country’s standard of living. Per the textbook Macroeconomics for Today:

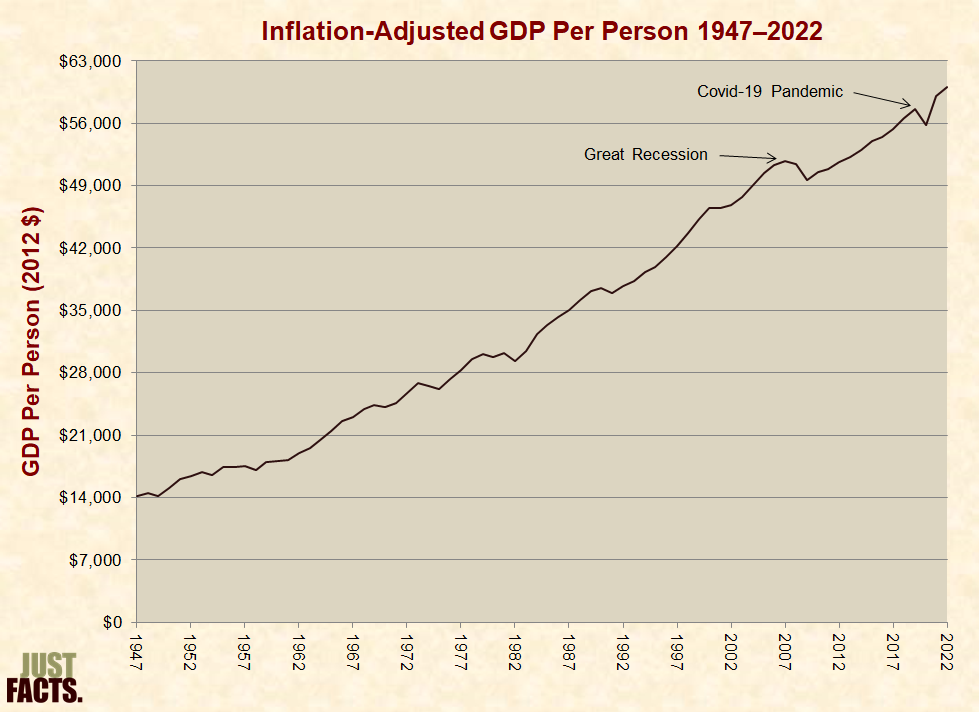

* In the U.S. from 1947 to 2022, the average inflation-adjusted GDP per person rose by 4.2 times:[236]

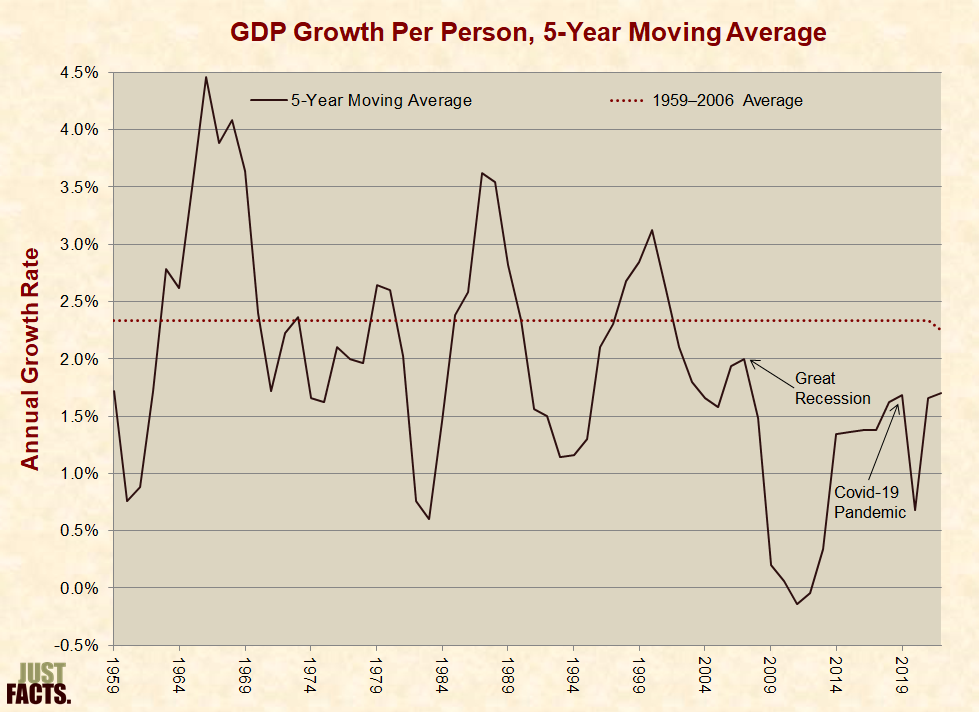

* Inflation-adjusted GDP growth per person in the U.S. has varied as follows since 1959:

* In 2012, the Journal of Economic Perspectives published a paper about the economic consequences of government debt. Using 2,000+ data points on national debt and economic growth in 20 advanced economies (such as the United States, France, and Japan) from 1800 to 2009, the authors found that countries with national debts above 90% of GDP averaged 34% less real annual economic growth than when their debts were below 90% of GDP.[245]

* At the close of 2022, the debt/GDP level in the U.S. was 123%.[246]

* In 2013, the Political Economy Research Institute at the University of Massachusetts, Amherst, published a paper about the economic consequences of government debt. Using data on national debt and economic growth in 20 advanced economies from 1946 to 2009, the authors found that countries with national debts over 90% of GDP averaged:

* The authors of the above-cited papers have engaged in a heated dispute about the results of their respective papers and the effects of government debt on economic growth. Facts about these issues can be found in Just Facts’ article, “Do Large National Debts Harm Economies?“

* “Personal consumption” is a comprehensive measure of the goods and services consumed by households. It includes all material resources:

* Per the World Bank:[250]

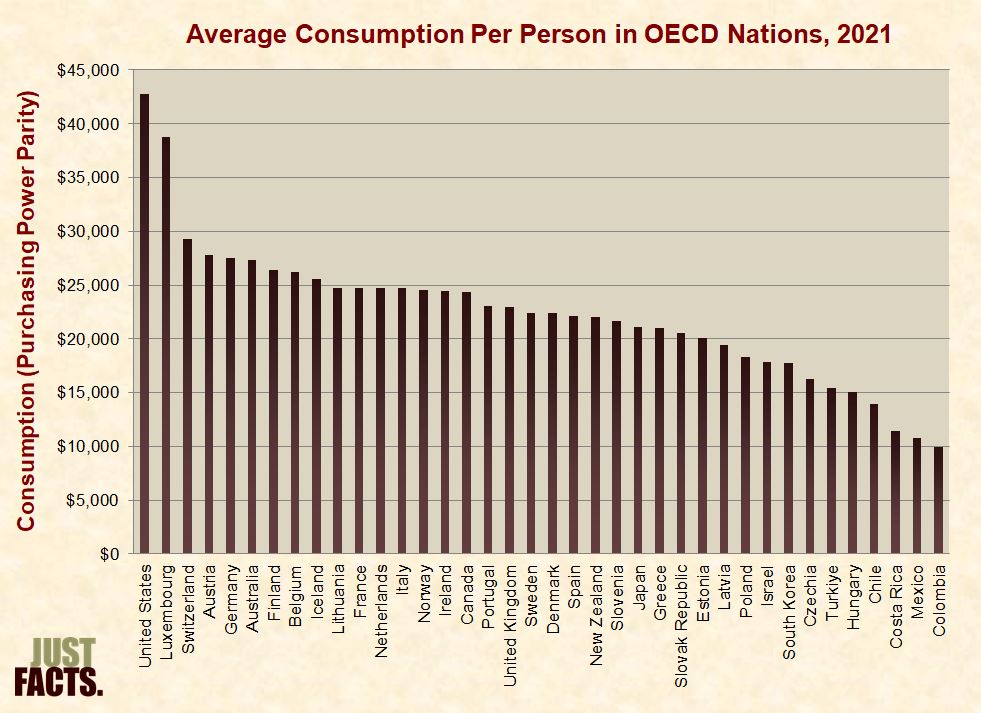

* The Organization for Economic Cooperation and Development (OECD) is an international association that is mainly comprised of wealthy, developed nations.[253] [254] In 2021, the United States had the highest average consumption per person of all 38 nations in the OECD:

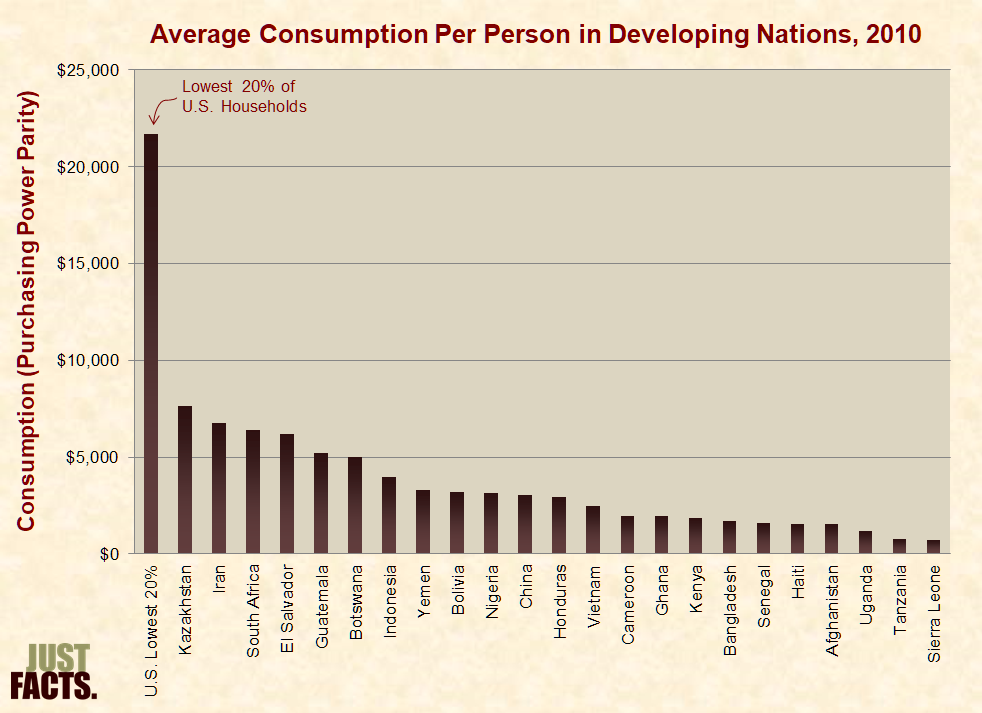

* The federal government’s Bureau of Economic Analysis—which is the source of consumption data for the United States—normally reports consumption for the entire nation and doesn’t break down the data to show how people at different levels fare. However, it published a report that does that for 2010.[258] Combined with World Bank data for the same year, these datasets show that:

* In 2010, the poorest 20% of Americans consumed three to 30 times more goods and services on average than the national averages for all people in an array of developing nations:

* For an article and video by Just Facts about how the New York Times misled the public about poverty in the U.S. compared to other nations, click here.

* Gross domestic product (GDP) is the standard measure of nations’ economic output. It is equal to the value of all goods and services that a country produces in a year minus the resources used to produce them.[264] [265]

* Per the U.S. Bureau of Labor Statistics:

* Per the textbook Macroeconomics for Today:

* In 2021, the worldwide average GDP per person was $16,997. This varied from a high of $62,403 in North America to a low of $3,717 in Sub-Saharan Africa:

* In 2021, the U.S. ranked 5th among 41 developed nations in average GDP per person. Other developed nations ranked as follows:

* Per the Organization for Economic Cooperation and Development:

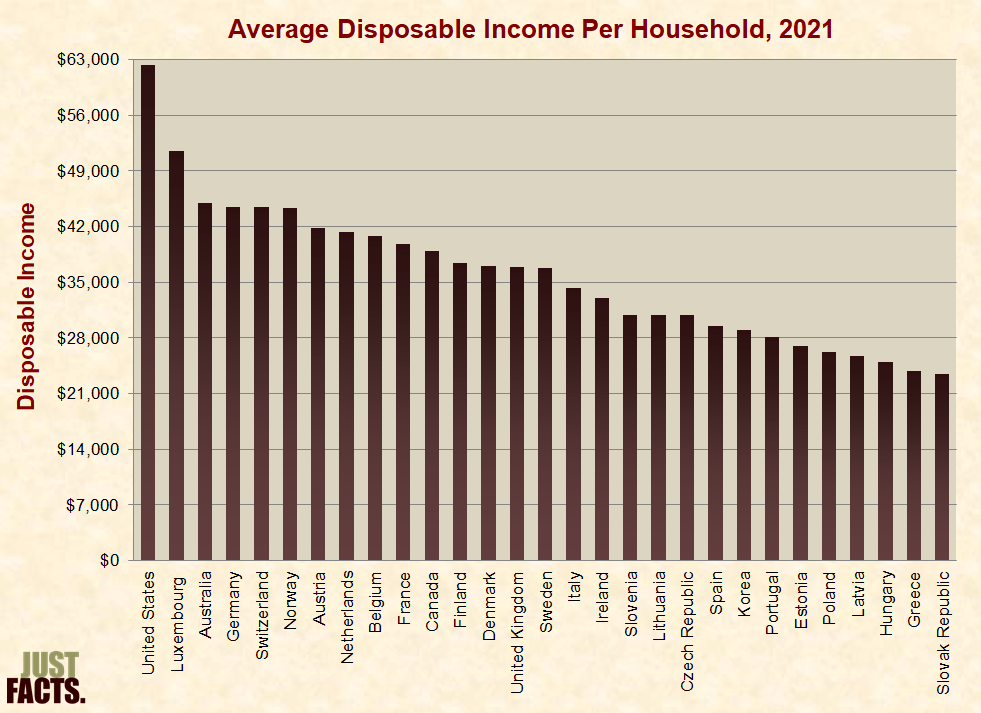

* Household disposable income equals:

* In 2021, the United States ranked first among 29 developed nations in average disposable income per household:

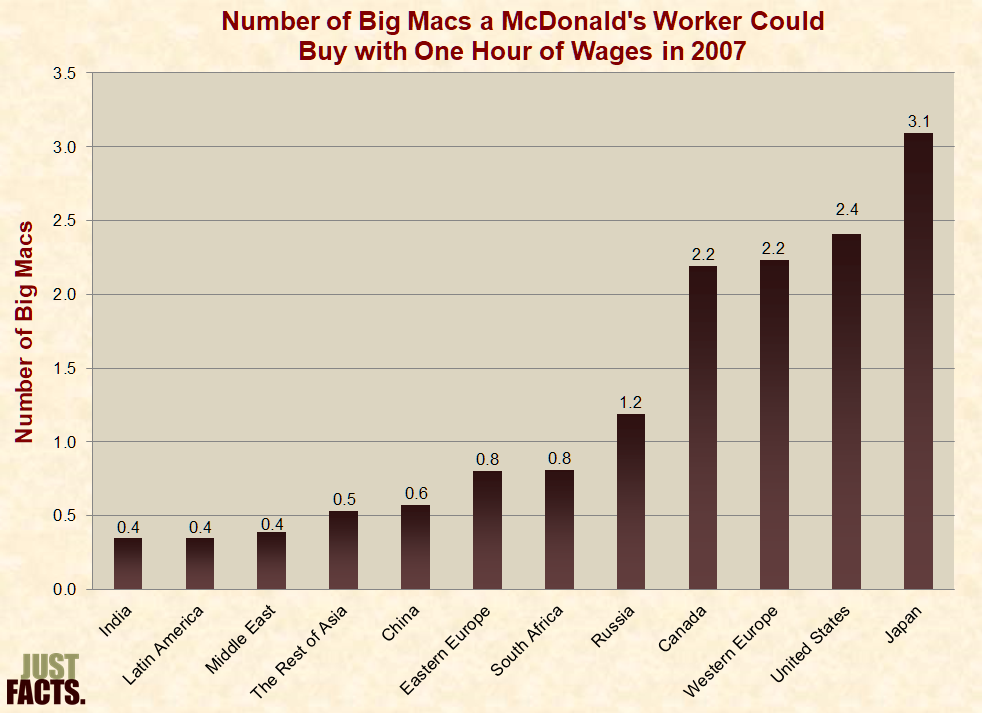

* Real wages are a measure of the goods that workers can buy with the money they earn from one hour of work.[276]

* In 2012, the American Economic Review published a paper by Princeton University economist Orley Ashenfelter that compared the real wages of McDonald’s workers in over 60 countries. He did this by determining how many Big Macs they could buy with their income from an hour of work. The advantage of using this measure is that:

* The study found that McDonald’s workers in the United States had the second-highest real wages of McDonald’s workers in all economic regions:

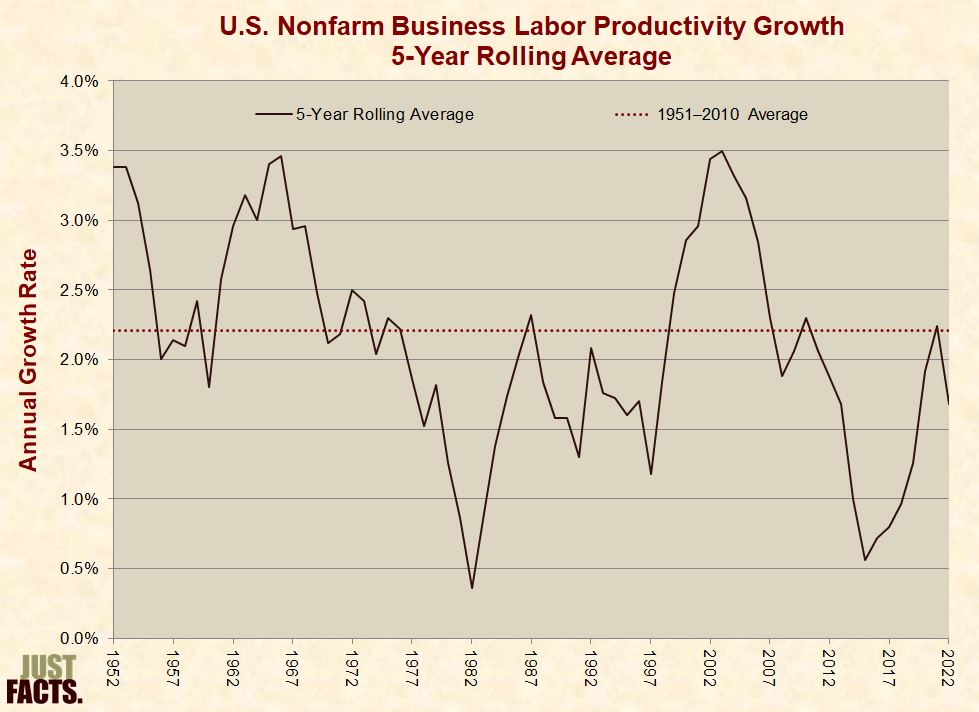

* Labor productivity is the amount of goods and services that workers produce in an hour.[279] [280] [281] [282]

* Per Federal Reserve Chair Janet Yellen (and various other economists with wide-ranging political views):

* Per the Congressional Budget Office, “a small change in the growth of productivity” over an extended period can do more harm than recessions, because low labor productivity reduces economic “output by an ever-increasing amount.”[290]

* As an example of labor productivity growth, U.S. businesses increased their inflation-adjusted output by 42% from 1998 to 2013 without any increase in work hours.[291]

* Labor productivity growth is driven by three primary factors:

* Because productivity growth often fluctuates over the short term, it is sometimes measured in five-year moving averages.[295] [296]

* The U.S. Bureau of Labor Statistics considers the nonfarm business sector to be the best single indicator of labor productivity for the U.S. economy. This is because it excludes sectors that are volatile or don’t produce concretely measurable output.[297] [298] [299]

* Nonfarm labor productivity growth in the U.S. has varied as follows since 1952:

* If the labor productivity slowdown that took place from 2005 to 2015 had not occurred, the U.S. economy in 2015 would have been about $3 trillion larger. This amounts to an average of $24,100 for every household in the United States.[301]

* Productivity growth can be suppressed by a variety of factors, such as:

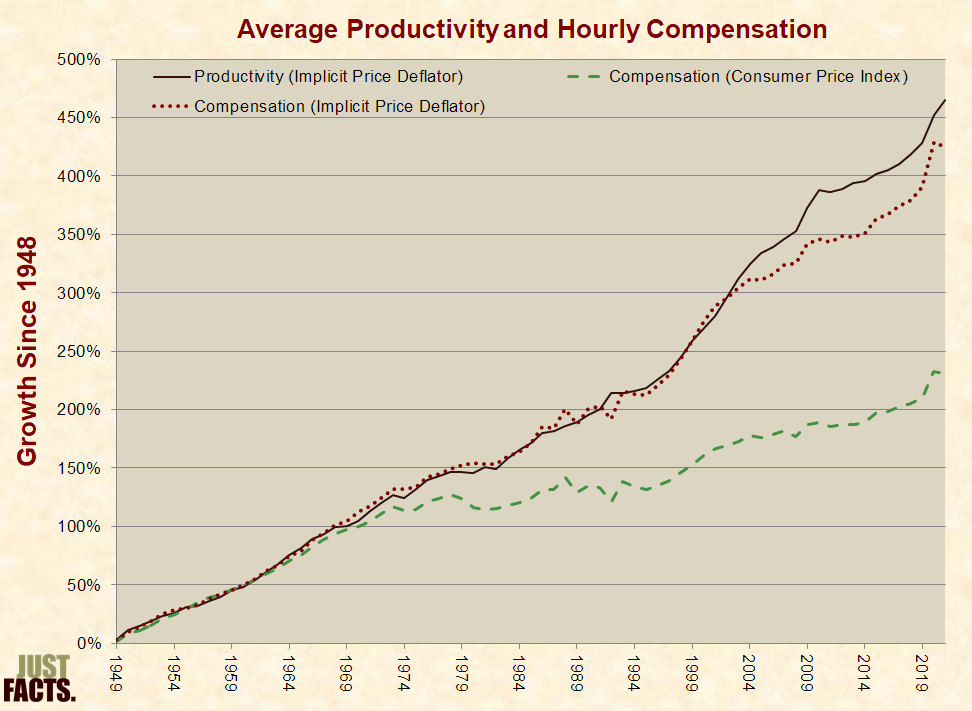

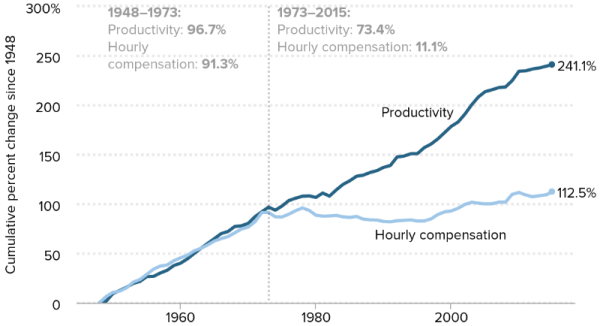

* Some politicians, commentators, and policy analysts have claimed that worker compensation has risen more slowly than worker productivity for decades, such as:

* Per Ph.D. economist Martin Feldstein, professor of economics at Harvard University and President Emeritus of the National Bureau of Economic Research:[321]

* Another reason behind claims that worker compensation has not kept pace with productivity growth is that some studies compare the compensation of one group of workers to the productivity of another group of workers.[323] [324]

* An objective comparison of labor productivity and compensation requires that:

* The U.S. government typically adjusts:

* When adjusted for inflation using:

* Beyond economic trends in earnings, profits, and government benefits—household incomes are affected by social factors like divorce, cohabitation, single parenting, and dual-income families.[341]

* According to data from the Congressional Budget Office, the inflation-adjusted average income of U.S. households rose by 76% between 1979 and 2019 (prior to the Covid-19 pandemic.)[342] For various income groups, it grew as follows:

* According to data from the Congressional Budget Office, the inflation-adjusted average income of U.S. households rose by 85% between 1979 and 2020 (amid Covid-19 government lockdowns and intensified social spending.)[345] [346] [347] For various income groups, it grew as follows:

* From 1979 to 2019 (prior to the Covid-19 pandemic),[350] the inflation-adjusted average income of U.S. households after federal taxes rose by about $46,800 or 84%. For various income groups, it grew as follows:

|

Inflation-Adjusted Household Income After Federal Taxes |

||||

|

Income Group |

1979 |

2019 |

Increase From 1979 to 2019 |

|

|

Dollars |

Percent |

|||

|

Lowest 20% |

$20,100 |

$38,900 |

$18,800 |

94% |

|

Second 20% |

$34,300 |

$54,900 |

$20,600 |

60% |

|

Middle 20% |

$49,100 |

$74,800 |

$25,700 |

52% |

|

Fourth 20% |

$64,300 |

$104,400 |

$40,100 |

62% |

|

Highest 20% |

$113,100 |

$252,100 |

$139,000 |

123% |

|

Top 1% |

$386,700 |

$1,398,500 |

$1,011,800 |

262% |

|

All Groups |

$55,600 |

$102,400 |

$46,800 |

84% |

* From 1979 to 2020 (amid Covid-19 government lockdowns and intensified social spending),[354] [355] [356] the inflation-adjusted average income of U.S. households after federal taxes rose by about $56,500 or 101%. For various income groups, it grew as follows:

|

Inflation-Adjusted Household Income After Federal Taxes |

||||

|

Income Group |

1979 |

2020 |

Increase From 1979 to 2020 |

|

|

Dollars |

Percent |

|||

|

Lowest 20% |

$20,300 |

$45,800 |

$25,500 |

126% |

|

Second 20% |

$34,700 |

$63,200 |

$28,500 |

82% |

|

Middle 20% |

$49,700 |

$84,300 |

$34,600 |

70% |

|

Fourth 20% |

$65,000 |

$115,100 |

$50,100 |

77% |

|

Highest 20% |

$114,300 |

$275,700 |

$161,400 |

141% |

|

Top 1% |

$391,000 |

$1,605,400 |

$1,214,400 |

311% |

|

All Groups |

$56,200 |

$112,700 |

$56,500 |

101% |

* From 1979 to 2019 (prior to the Covid-19 pandemic),[360] U.S. middle-income households’ share of total income after federal taxes decreased by about 1.9 percentage points, or by 12%. The share of income for other groups changed as follows:

|

Share of Total Income After Federal Taxes |

||||

|

Income Group |

1979 |

2019 |

Change |

|

|

Percentage Points |

Percent |

|||

|

Lowest 20% |

7.8% |

7.7% |

–0.1 |

–1% |

|

Second 20% |

12.3% |

10.7% |

–1.6 |

–13% |

|

Middle 20% |

16.4% |

14.5% |

–1.9 |

–12% |

|

Fourth 20% |

22.1% |

20.2% |

–1.9 |

–9% |

|

Highest 20% |

41.8% |

48.5% |

6.7 |

16% |

|

Top 1% |

7.4% |

13.0% |

5.6 |

76% |

* From 1979 to 2020 (amid Covid-19 government lockdowns and intensified social spending),[364] [365] [366] U.S. middle-income households’ share of total income after federal taxes decreased by about 1.4 percentage points, or by 9%. The share of income for other groups changed as follows:

|

Share of Total Income After Federal Taxes |

||||

|

Income Group |

1979 |

2020 |

Change |

|

|

Percentage Points |

Percent |

|||

|

Lowest 20% |

7.8% |

8.2% |

0.4 |

5% |

|

Second 20% |

12.3% |

11.4% |

–0.9 |

–7% |

|

Middle 20% |

16.4% |

15.0% |

–1.4 |

–9% |

|

Fourth 20% |

22.1% |

20.0% |

–2.1 |

–10% |

|

Highest 20% |

41.8% |

46.8% |

5.0 |

12% |

|

Top 1% |

7.4% |

13.2% |

5.8 |

78% |

* The Gini index is the most common measure of income inequality.[370] [371] [372]

* Various reporters at major media outlets have cited the Gini index for household income to claim that:

* A 2014 study published by the Social Science Research Network found that:

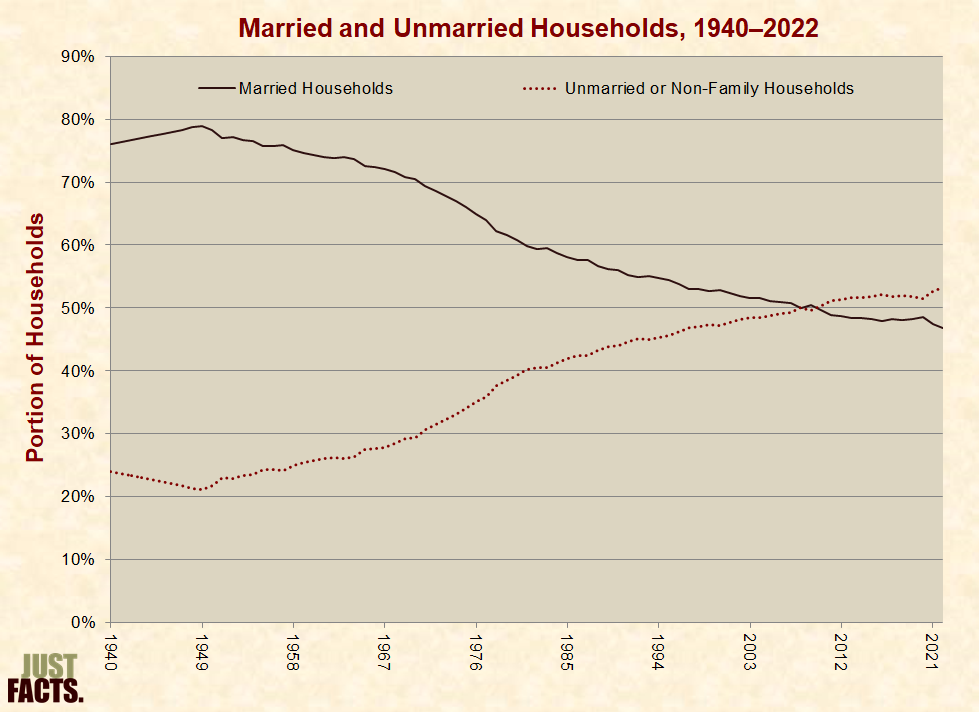

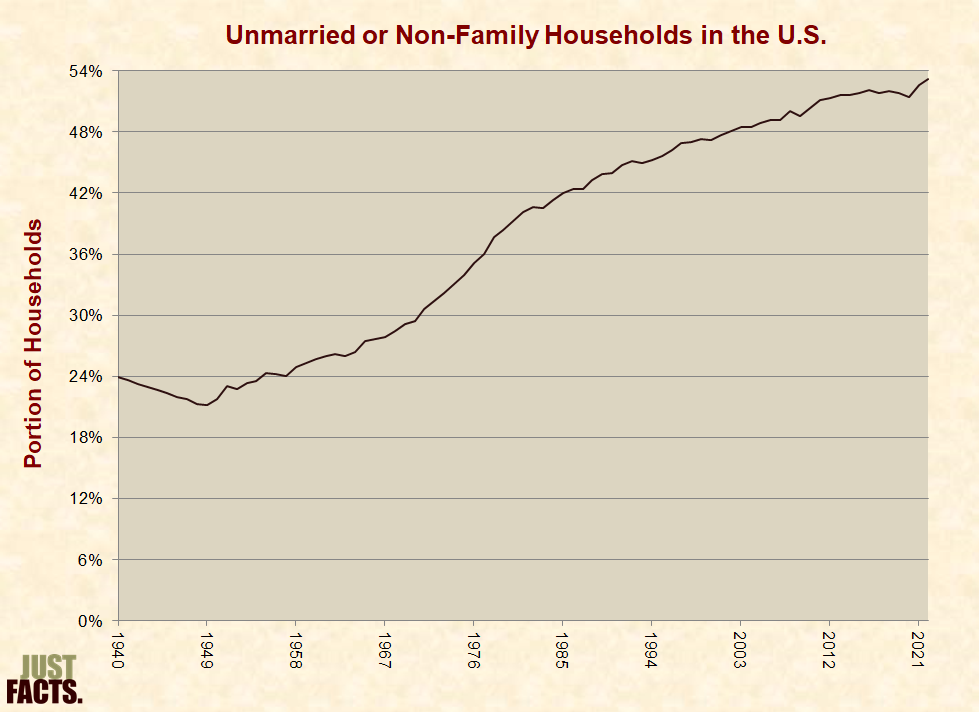

* From 1940 to 2022, the number of households in the U.S. increased by 275%, while the U.S. population increased by 152%.[377] [378] During this same period, the portion of unmarried or non-family households rose from 24% to 53%:

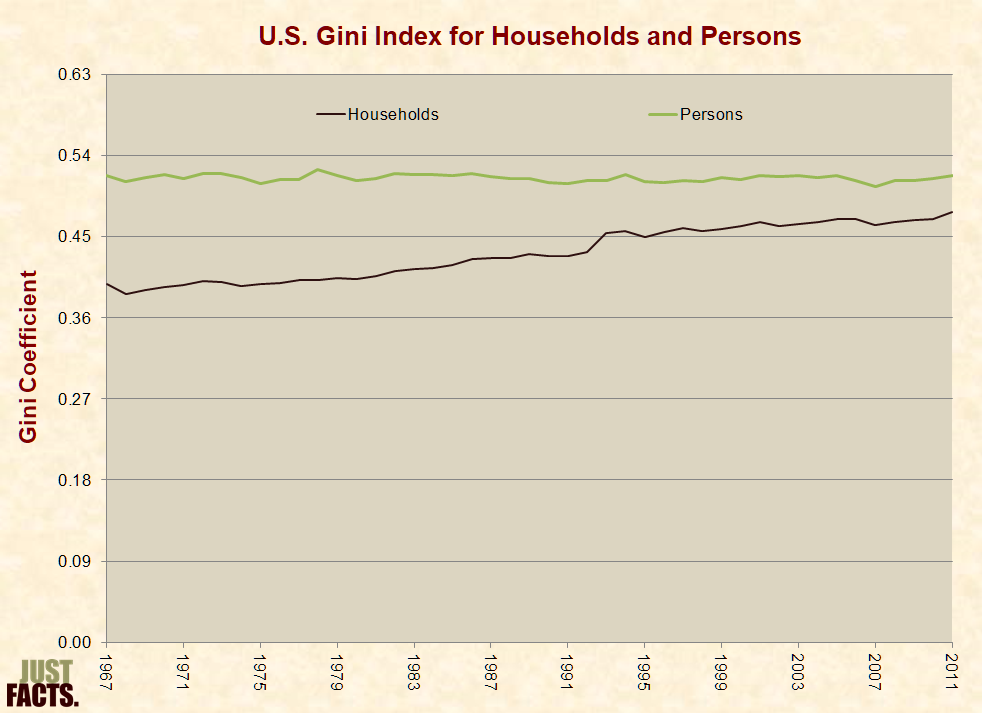

* From 1967 to 2011:

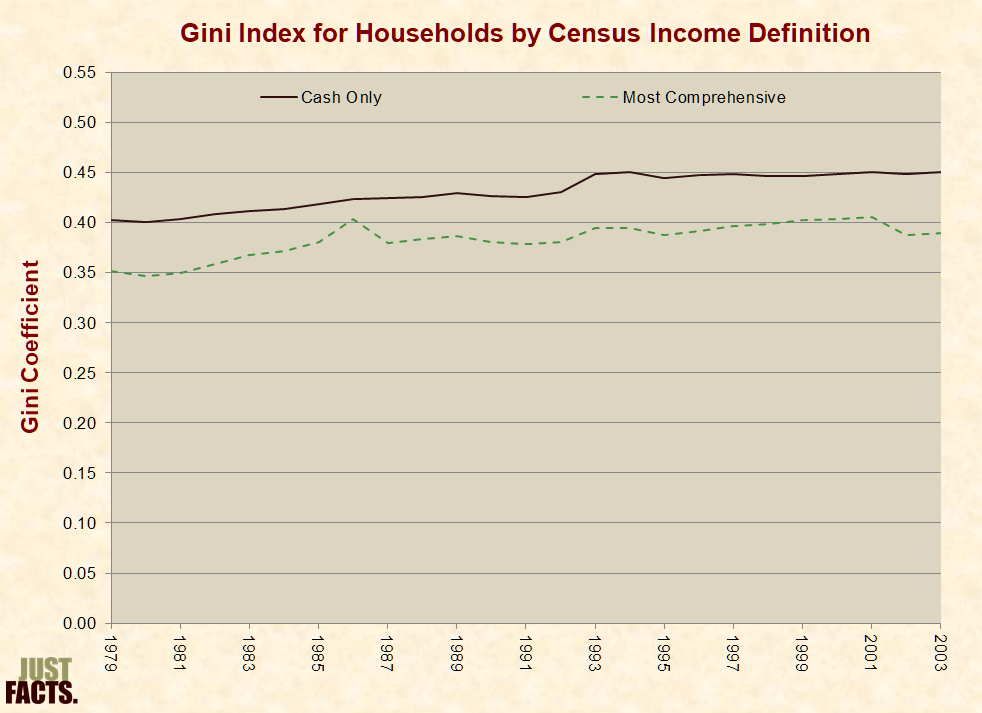

* The standard Gini index published by the Census Bureau does not include all income and taxes.[381] From 1979 to 2003, the Census Bureau published Gini index data based on more comprehensive measures of income.[382] [383] Over this period, the standard Gini index averaged 12% higher than the Gini index based on the most comprehensive Census income measure:

* All Gini indexes based on Census Bureau data are derived from surveys, and households often underreport their cash and noncash income on such surveys.[385] [386]

* Per a 2015 paper in the Journal of Economic Perspectives entitled “Household Surveys in Crisis”:

* An analysis of Federal Reserve data published by Rice University’s Baker Institute for Public Policy found that income inequality fell between 2016 and 2019. The decline was the largest since 1992.[390]

* During his acceptance speech at the 2016 Republican National Convention, Donald Trump made the following claim, and New York Times and NPR reported that it was “true”:

* This claim is based on data from the U.S. Census Bureau,[394] which:

* More comprehensive data from the Congressional Budget Office shows that the inflation-adjusted average household income of the middle 20% of U.S. households rose from $72,100 in 2000 to $81,500 in 2016, or by $9,2400 or 13%. After federal taxes, their income climbed by $10,600 or 18%.[401] [402] [403]

* To adjust income data for inflation, the Congressional Budget Office uses the Personal Consumption Expenditure price index.[404] [405] If it were adjusted for inflation using the Consumer Price Index, this same data would show that from 2000 to 2016, average middle-class household income rose by $6,361 or 8%, and average middle-class household income after federal taxes rose by $8,161 or 13%.[406] [407] [408]

* In 2015, U.S. Senator Elizabeth Warren of Massachusetts made the following claim based on data from tax returns, and PolitiFact said it was “mostly true”:

* More comprehensive data from the Congressional Budget Office shows that the inflation-adjusted average income of households in the bottom 90% rose from $55,527 in 1980 to $83,591 in 2015, or by 51%. After federal taxes, their income climbed from $44,922 in 1980 to $71,527 in 2015, or by $26,606 or 59%.[411] [412] [413]

* In 2013, the Pew Research Center claimed that:

* More comprehensive data from the Congressional Budget Office shows that in 2012, the top 1% received 18% of all pretax income, and the bottom 90% received 62%. The distribution of pretax income since 1979 has varied as follows:

* After federal taxes, the top 1% received 15% of all household income in 2012, and the bottom 90% received 66%. The distribution of income after federal taxes since 1979 has varied as follows:

* The claims above from PolitiFact (2015), and Pew Research (2013), are based on the work of Ph.D. economists Thomas Piketty and Emmanuel Saez.[420] [421] Paul Krugman of the New York Times has called their work on income inequality a “landmark piece of research that has had a major impact.”[422]

* Piketty and Saez have published articles and academic papers that overstate income inequality by:

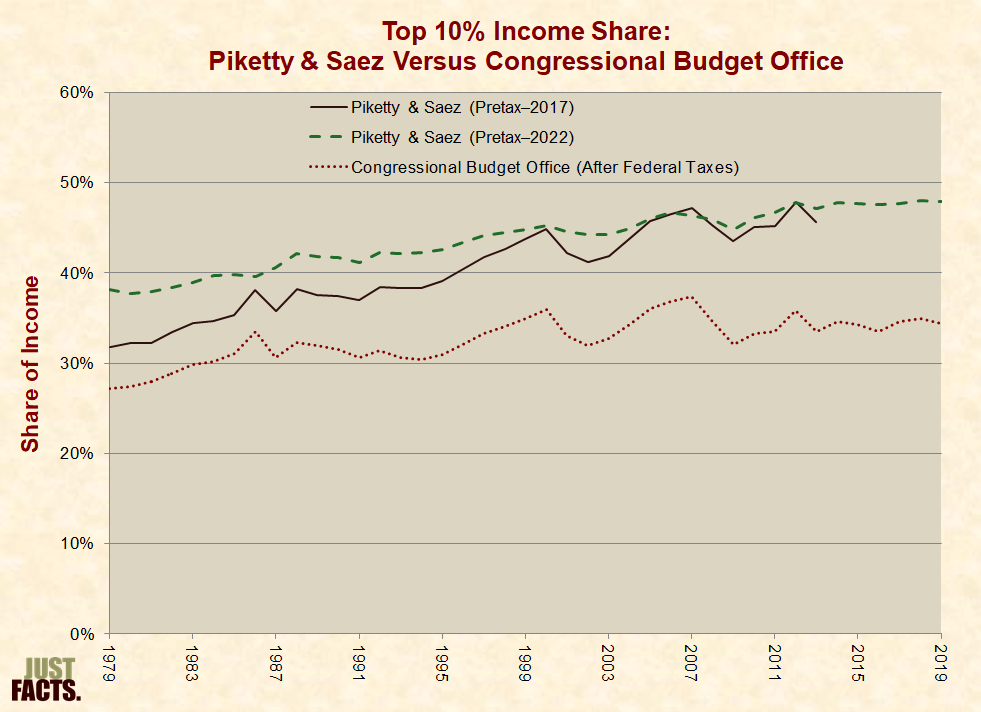

* The income share of the top 10%—as estimated by Piketty and Saez in 2017, Piketty and Saez in 2022, and the Congressional Budget Office in 2022—have varied as follows:

|

NOTE: This chart does not account for the rise in number of households, which would reduce the income share growth of the top 10% over time.[443] |

* According to Piketty and Saez, “the average federal tax burden on top 1% families has decreased from 44.4% in 1980 to 30.4% in 2004,” or by 14 percentage points.[444]

* More comprehensive tax and income data from the Congressional Budget Office shows that the average federal tax burden on the top 1% of households decreased from about 33% in 1980 to 30% in 2004, or by 3 percentage points.[445] [446] [447]

* According to Piketty and Saez, from 1980 to 2004, the total decrease in federal taxes paid by the top 1% was greater than the total increase in government benefits received by the bottom 99%.[448]

* More comprehensive inflation-adjusted data from the Congressional Budget Office shows that from 1980 to 2004:

* In 1997, the Journal of Economic Behavior & Organization published a survey of 247 faculty, students, and staff at the Harvard School of Public Health. This survey:

* In 2015, U.S. residents of varying income, race, education, and marital status described their overall economic well-being as follows:

|

Self-Perception of Overall Economic Well-Being |

||||

|

Characteristic |

Finding It Difficult to Get By |

Just Getting By |

Doing Okay |

Living Comfortably |

|

Family Income |

||||

|

Less than $40,000 |

18% |

32% |

39% |

12% |

|

$40,000–$100,000 |

4% |

19% |

47% |

29% |

|

Greater than $100,000 |

2% |

8% |

37% |

54% |

|

Race/Ethnicity |

||||

|

White, non-Hispanic |

9% |

20% |

41% |

30% |

|

Black, non-Hispanic |

10% |

28% |

41% |

20% |

|

Hispanic |

12% |

25% |

43% |

21% |

|

Education |

||||

|

High school degree or less |

13% |

26% |

41% |

20% |

|

Some college or associate degree |

9% |

25% |

42% |

24% |

|

Bachelor’s degree or more |

6% |

14% |

40% |

41% |

|

Marital and Parental Status |

||||

|

Unmarried, no children under 18 |

12% |

25% |

42% |

21% |

|

Married, no children under 18 |

6% |

15% |

43% |

37% |

|

Unmarried, children under 18 |

19% |

34% |

34% |

13% |

|

Married, children under 18 |

7% |

22% |

40% |

31% |

|

Overall |

9% |

22% |

41% |

28% |

NOTE: When interpreting the facts in this section, it is important to realize that correlation does not prove causation. This is because numerous factors can affect economic outcomes such as income, and there is frequently no objective way to identify, measure, and determine the interplay between all of them.

* Per an academic textbook about analyzing data:

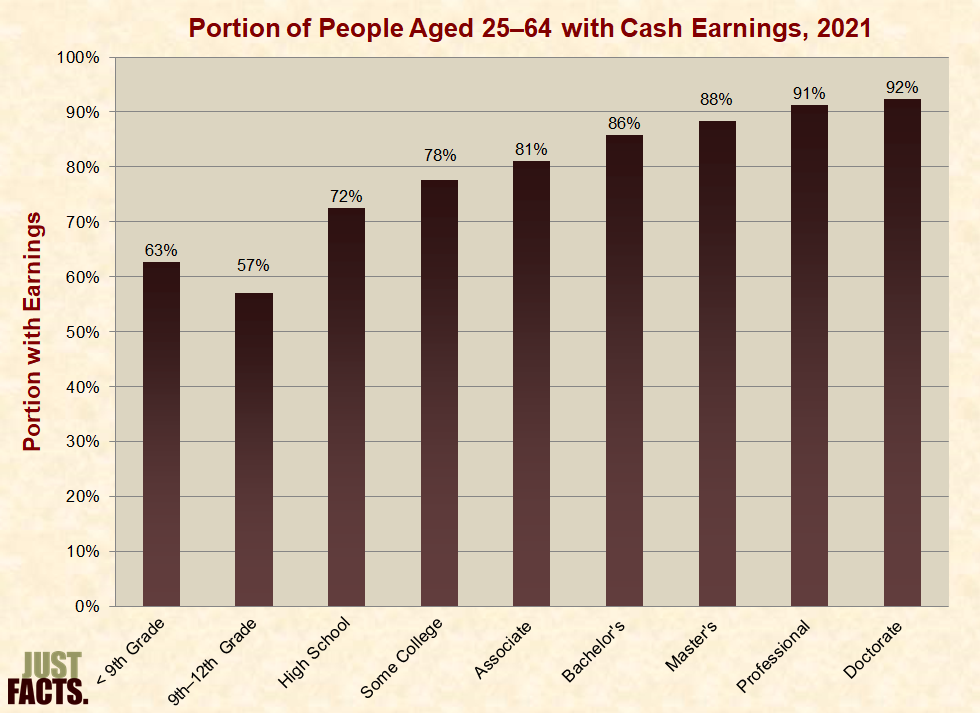

* In 2021, the average reported cash earnings of U.S. residents aged 25–64 with different levels of formal education varied as follows:

* In 2021, 79% of U.S. residents aged 25–64 reported having at least some cash earnings, and 21% did not report any cash earnings. For varying levels of education, the rates varied as follows:

* In 2021, the top-10 highest-paying occupations were all in the medical or dental fields.[460]

* For more facts about education and income, visit Just Facts’ research on education.

* In 2011, the EPPI-Centre at the University of London published a systematic review of 115 corruption studies which found that “corruption has negative and statistically significant effects on [economic] growth—directly and indirectly.”[461] [462]

* Gross Domestic Product (GDP) is the most common measure of a nation’s economic output.[463] It measures the value of all “goods and services produced within a country’s geographic borders.”[464]

* Per the textbook Microeconomics for Today (and other academic sources):

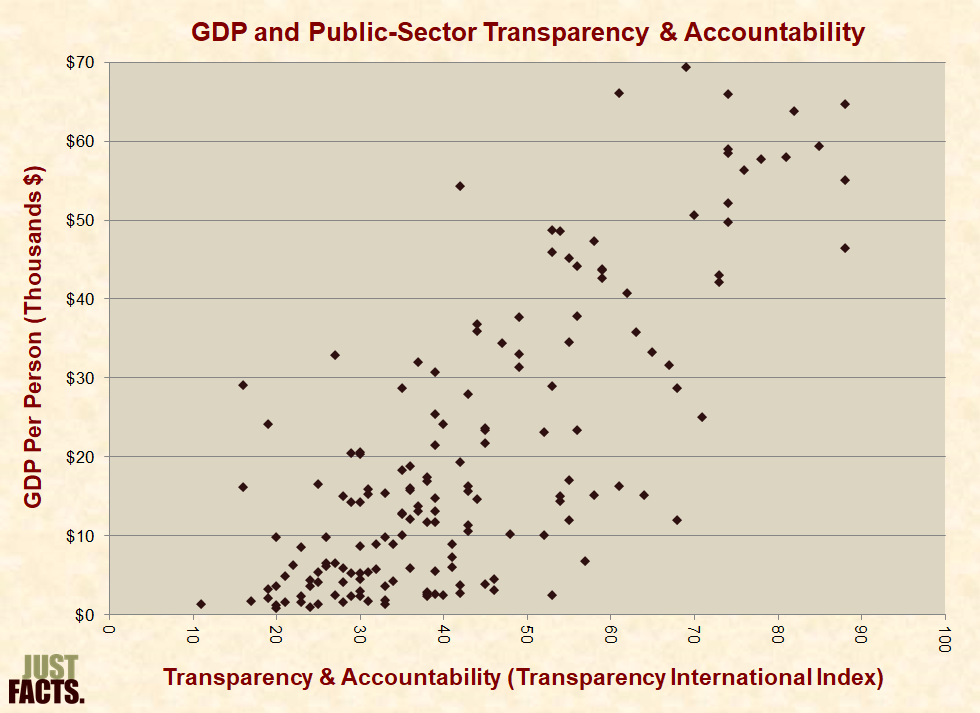

* Based on data from 170 countries, GDP per person is generally higher in countries with greater public-sector transparency and accountability:

* Nations have three primary types of resources or wealth:

* In 2006, the World Bank analyzed the capital resources of 118 nations and found that the wealth of most nations is mainly comprised of intangible capital. In about 85% of these countries, intangible capital accounted for more than half of their wealth.[475] Per the study:

* In 2005, the capital resources of nations with the highest and lowest wealth per person varied as follows:

|

Total Wealth Top and Bottom 10 Countries, 2005 |

|||||

|

Rank |

Country |

Wealth Per Person (PPP) |

Capital |

||

|

Natural |

Produced |

Intangible |

|||

|

Top 10 Countries |

|||||

|

1 |

Luxembourg |

$779,601 |

$5,805 |

$203,387 |

$570,409 |

|

2 |

Kuwait |

$765,219 |

$618,083 |

$168,548 |

–$21,412 |

|

3 |

United States |

$734,195 |

$13,692 |

$99,137 |

$621,367 |

|

4 |

United Arab Emirates |

$728,889 |

$291,256 |

$175,427 |

$262,207 |

|

5 |

Brunei Darussalam |

$657,376 |

$1,087,550 |

$438,724 |

–$868,898 |

|

6 |

Norway |

$616,547 |

$82,291 |

$136,760 |

$397,496 |

|

7 |

Iceland |

$593,380 |

$7,730 |

$85,959 |

$499,690 |

|

8 |

Singapore |

$555,934 |

$4 |

$183,775 |

$372,155 |

|

9 |

Switzerland |

$543,986 |

$7,511 |

$132,137 |

$404,337 |

|

10 |

Canada |

$537,878 |

$36,665 |

$89,182 |

$412,031 |

|

Bottom 10 Countries |

|||||

|

142 |

Ethiopia |

$13,876 |

$4,406 |

$1,272 |

$8,198 |

|

143 |

Sierra Leone |

$13,061 |

$4,110 |

$758 |

$8,194 |

|

144 |

Niger |

$12,312 |

$3,767 |

$1,017 |

$7,529 |

|

145 |

Chad |

$12,078 |

$10,205 |

$2,878 |

–$1,005 |

|

146 |

Liberia |

$10,631 |

$6,702 |

$454 |

$3,475 |

|

147 |

Guinea-Bissau |

$10,464 |

$5,010 |

$1,456 |

$3,998 |

|

148 |

Mozambique |

$9,807 |

$2,115 |

$1,199 |

$6,492 |

|

149 |

Burundi |

$9,388 |

$10,840 |

$666 |

–$2,118 |

|

150 |

Malawi |

$9,261 |

$2,916 |

$1,315 |

$5,030 |

|

151 |

Congo, Dem. Rep. |

$5,127 |

$3,309 |

$414 |

$1,403 |

* From 1940 to 2022, the portion of unmarried or nonfamily households in the U.S. rose from 24% to 53%:

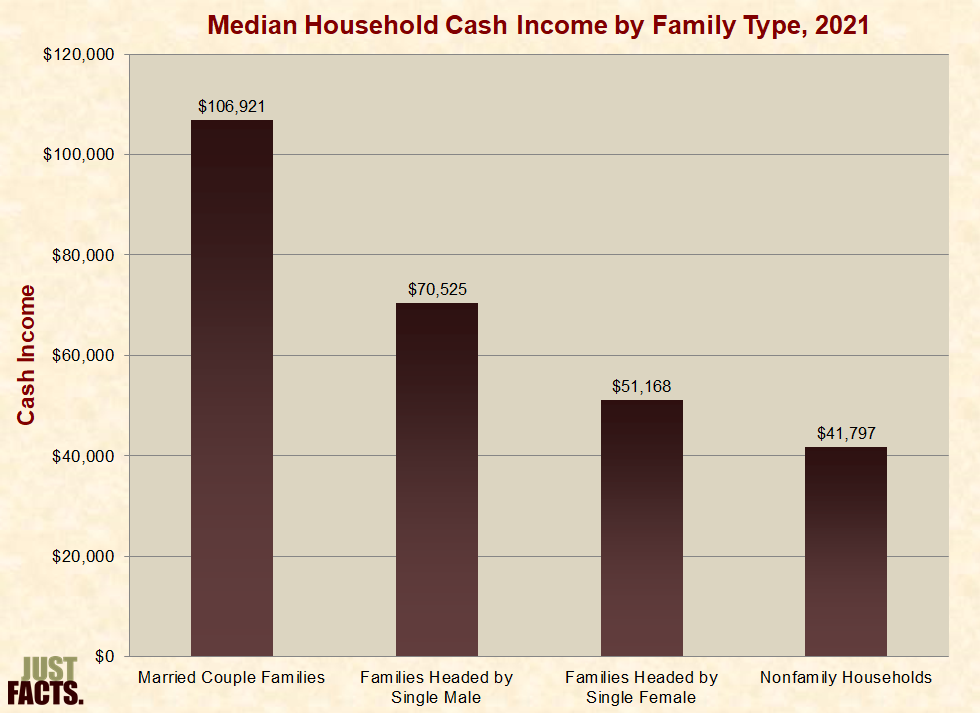

* In 2021, the reported median household cash income for U.S. households with different marital statuses varied as follows:

* In 2011, the reported median cash income of U.S. households with children:

* From 1960 to 2011, the share of single mothers who have never married rose from 4% to 44%.[484]

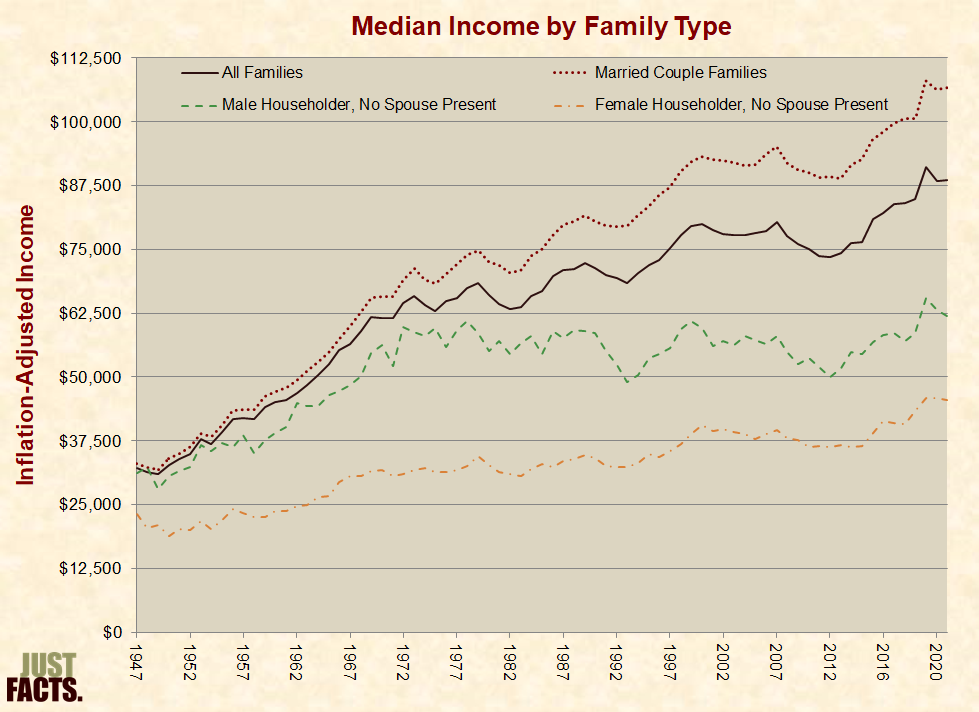

* From 1949 to 2021 the reported median inflation-adjusted cash income of married-couple families in the U.S. rose by 3.2 times. The change in income for other types of families varied as follows:

* In 2021, full-time, year-round female workers reportedly earned median cash wages of $49,263. This was 23% less than the $60,428 earned by males.[487]

* During his 2014 State of the Union address, President Barack Obama stated:

* Obama’s statement does not account for the following factors that pertain to “equal pay” and “equal work”:

* Various studies that have attempted to account for some (but not all) of the factors above have found:

* Per a 2009 analysis of gender wage studies conducted for the U.S. Department of Labor by CONSAD Research Corporation:

* In 2021, the median reported household cash incomes of different races and ethnicities in the U.S. varied as follows:

|

Median Household Cash Income |

|

|

Race / Ethnicity |

Median Income |

|

Asian |

$101,418 |

|

White |

$74,262 |

|

Hispanic |

$57,981 |

|

Black |

$48,297 |

|

All Groups |

$70,784 |

* In 2021, the formal education levels of U.S. residents over age 25 with different races and ethnicities varied as follows:

|

Race / Ethnicity |

Formal Education |

|||

|

No High School Diploma |

High School |

Some College |

Bachelor’s or Higher |

|

|

Asian |

12% |

14% |

17% |

56% |

|

White |

7% |

26% |

29% |

38% |

|

Black |

12% |

31% |

32% |

25% |

|

Hispanic |

28% |

28% |

25% |

20% |

* In 2021, the median reported cash earnings of full-time workers in the U.S. aged 25 and older with different levels of formal education, races, and ethnicities varied as follows:

|

Race / Ethnicity |

Median Earnings (Thousands $) |

|

|

High School[511] |

Bachelor’s or Higher[512] |

|

|

Asian |

$41 |

$95 |

|

White |

$46 |

$81 |

|

Black |

$39 |

$66 |

|

Hispanic |

$41 |

$70 |

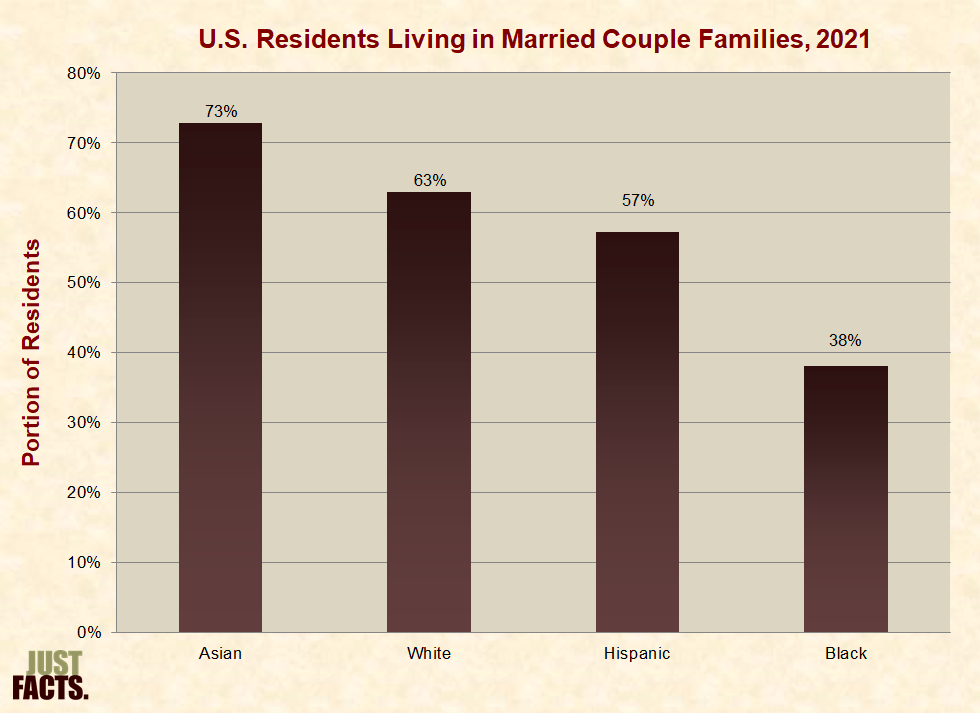

* In 2021, the portion of U.S. residents living in married couple families ranged from 73% for Asians to 38% for blacks:

* In 2021, the median reported household cash incomes for U.S. households of different races, ethnicities, and marital or family statuses were as follows:

|

Race / Ethnicity |

Median Household Cash Income (Thousands $) |

|||

|

Type of Family Household |

||||

|

Married Couple |

Single Male |

Single Female |

Nonfamily |

|

|

Asian |

$131 |

$92 |

$72 |

$59 |

|

White |

$107 |

$72 |

$55 |

$43 |

|

Black |

$90 |

$58 |

$41 |

$34 |

|

Hispanic |

$77 |

$66 |

$45 |

$40 |

|

All Groups |

$107 |

$71 |

$51 |

$42 |

* For more facts about race and income, visit Just Facts’ research on racial issues.

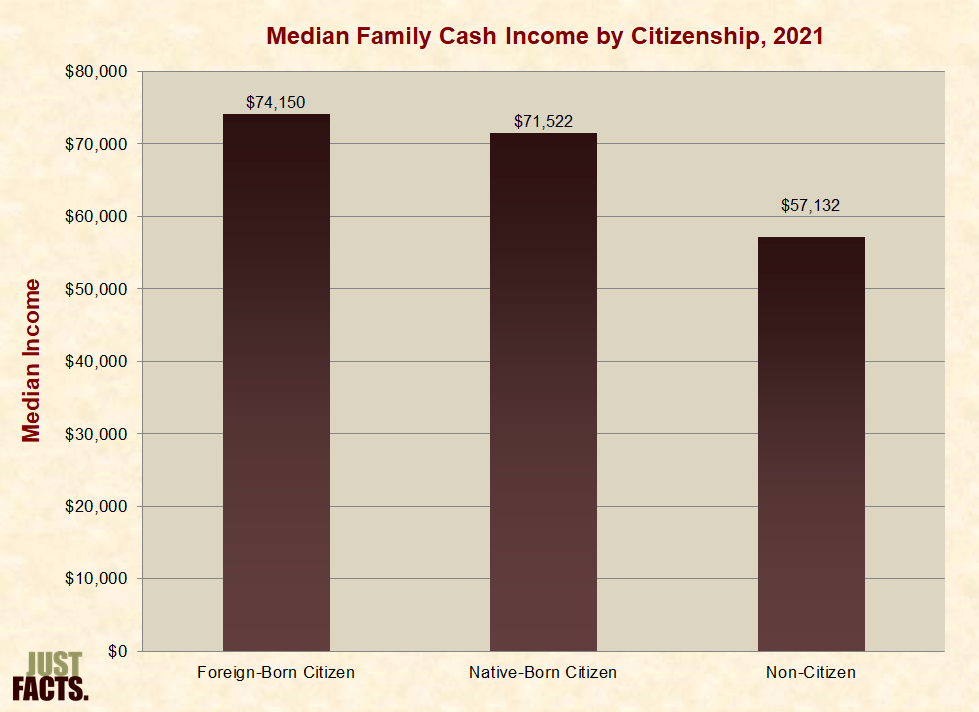

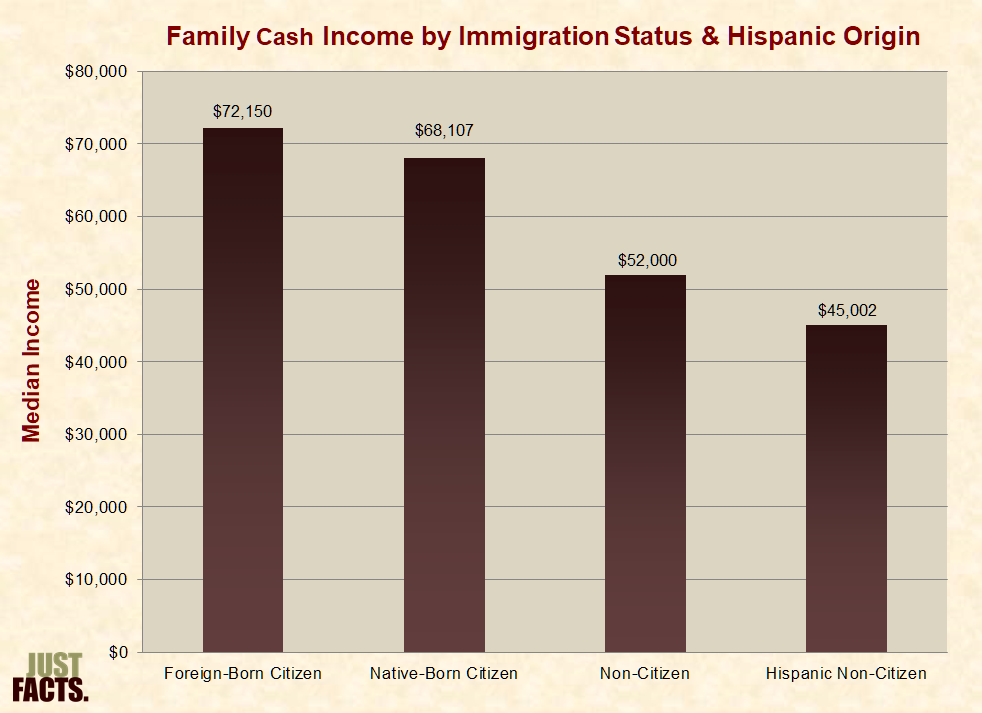

* In 2021, the reported median cash income of families living in the U.S. was $91,162. This varied by immigration status and Hispanic origin as follows:

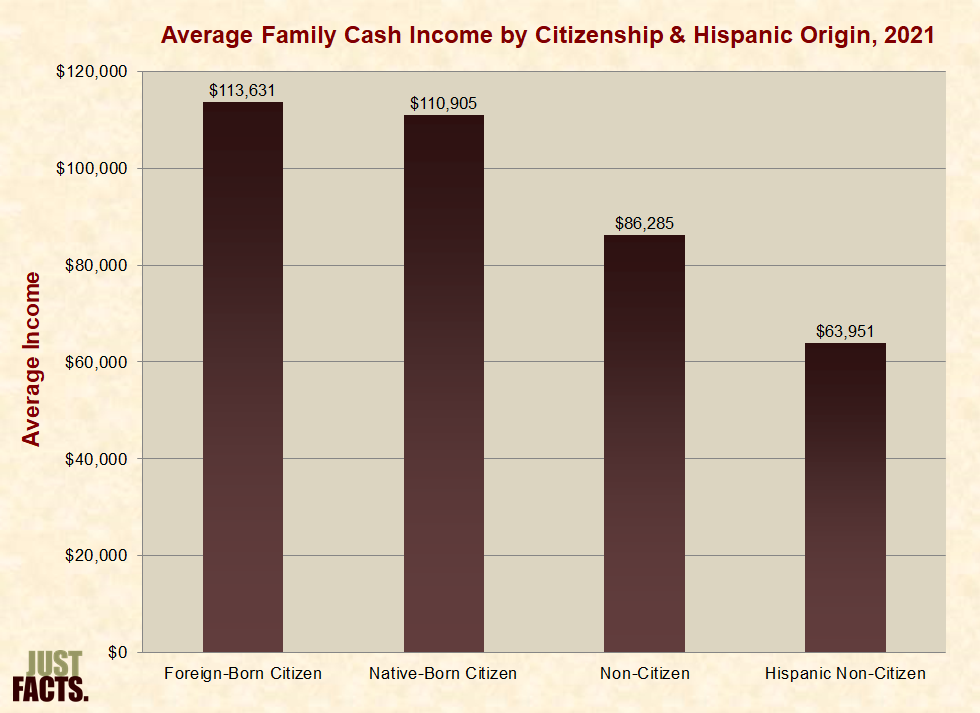

* In 2021, the reported average cash income of families living in the U.S. was $109,299.[525] [526] [527] This varied by immigration status and Hispanic origin as follows:

* In 2017, the reported median cash income of families living in the U.S. was $67,123. This varied by immigration status and Hispanic origin as follows:

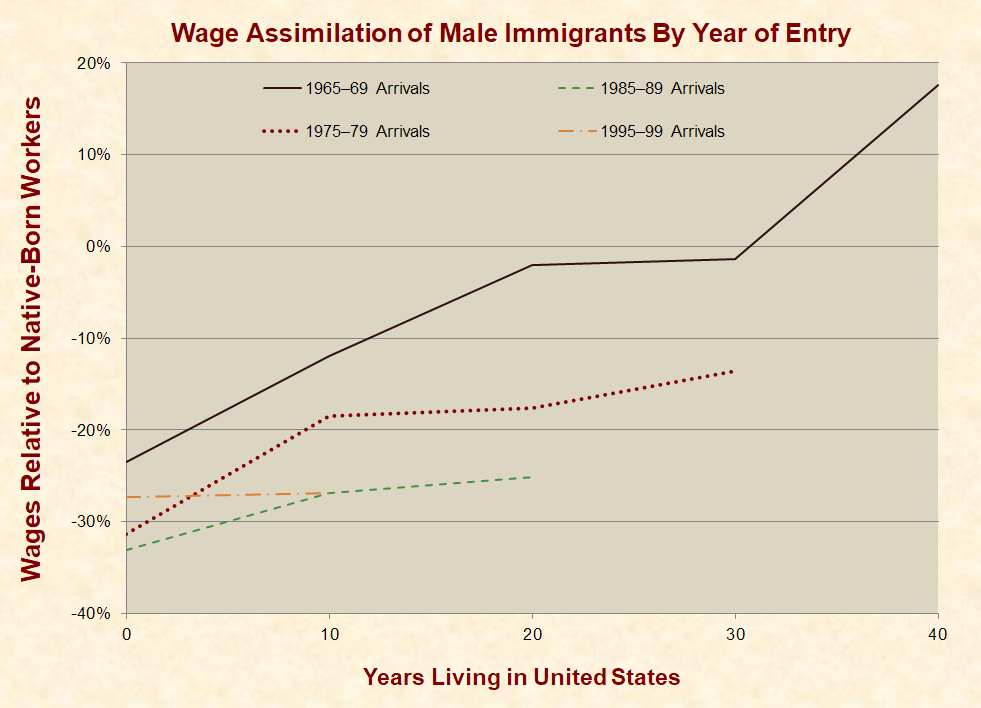

* Male immigrants who arrived in the U.S. during:

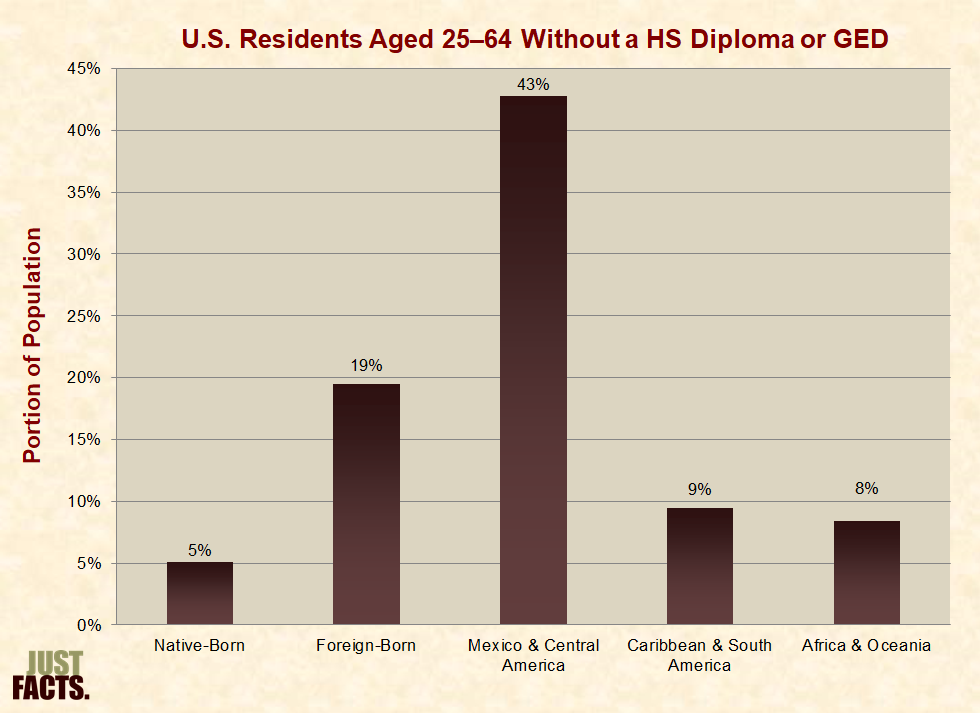

* In 2022, 43% of Mexican and Central American immigrants aged 25–64 did not have a high school diploma or GED, as compared to 5% of people born in the U.S. in the same age group. The rates for other groups were as follows:

* A 2014 study by the Brookings Institution found that:

* For more facts about immigration and income, visit Just Facts’ research on immigration.

* One of the key factors that impact nations’ standards of living is their average hours of work per person.[539]

* Unpaid work—such as caring for children, cooking, and cleaning—increases standards of living, but it is often not recorded in standard economic measures.[540] [541] Per an academic book published by Stanford University Press:

* In 2022, the employment status of the total U.S. civilian, non-institutionalized population was as follows:

* In 2022, the employment status of the U.S. civilian, non-institutionalized population aged 16 years and over was as follows:

* In 2022, the employment status of the U.S. civilian, non-institutionalized population aged 25–54 was as follows:

* In 2021, 16% of adults earned income from occasional informal work.[546]

* Per the Congressional Budget Office:

* The labor force, as defined by the Bureau of Labor Statistics, includes all people who are “either working or actively seeking work.” The potential labor force used by the Bureau to determine the labor force participation rate includes:

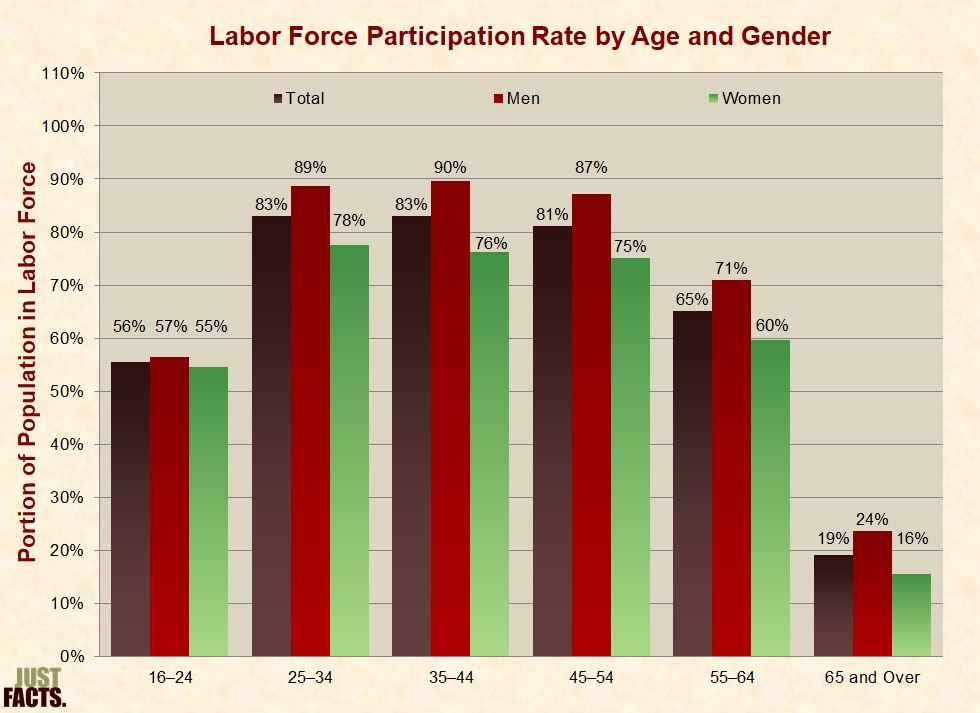

* In 2022, men aged 35–44 had a labor force participation rate of 90%. This was the highest rate of all age and gender groups, which varied as follows:

* From 1976 to 2022, the portion of men in their prime working years (25–54) who were not in the labor force increased by 96%.[551] [552]

* Current labor force participation rates for men of all age groups are lower than they were in 1948, while the opposite is true for women:

* As defined by the U.S. Bureau of Labor Statistics, “employed” people are those who, over the course of a week:

* “Unemployed” people are those who are not working but are “available for work” and:

* The federal unemployment rate is determined by dividing the number of unemployed people by the number of people in the labor force.[556] The labor force does not include:

* From 1947 to 2022, the annual unemployment rate averaged 5.7%, varying from a low of 2.9% in 1953 to a high of 9.7% in 1982. In 2022, it was 3.6%:

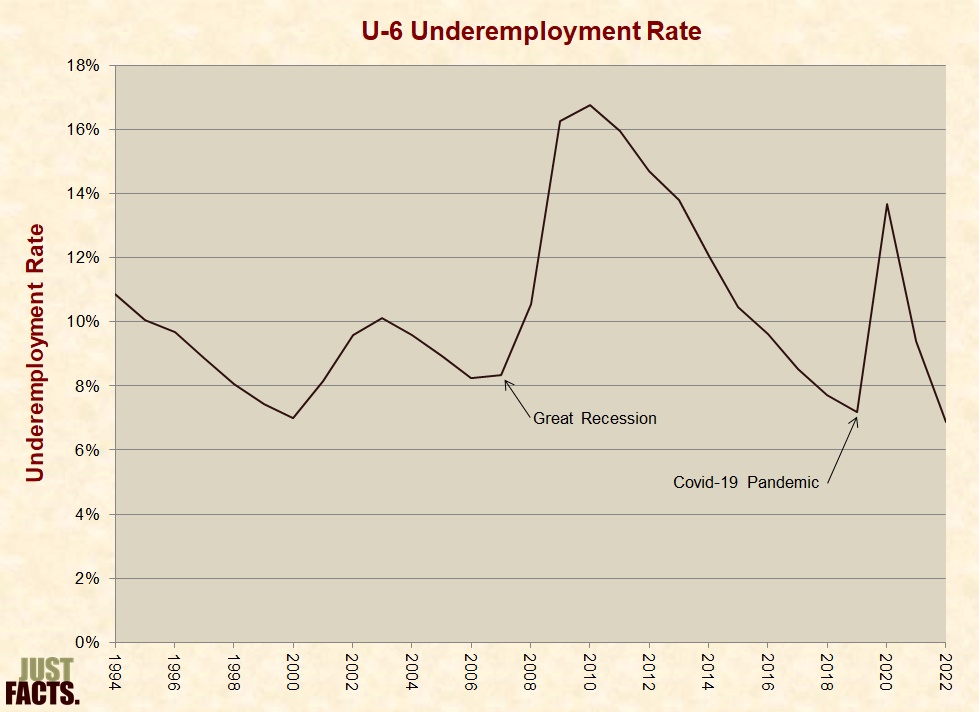

* “Underemployment” is a wider measure of idle potential labor than unemployment. The broadest measure of underemployment published by the U.S. Bureau of Labor Statistics is called “U-6,” which includes:

* From 1994 to 2022, the annual underemployment rate averaged 10.3%, varying from a low of 6.9% in 2022 to a high of 16.7% in 2010. In 2022, it was 6.9%:

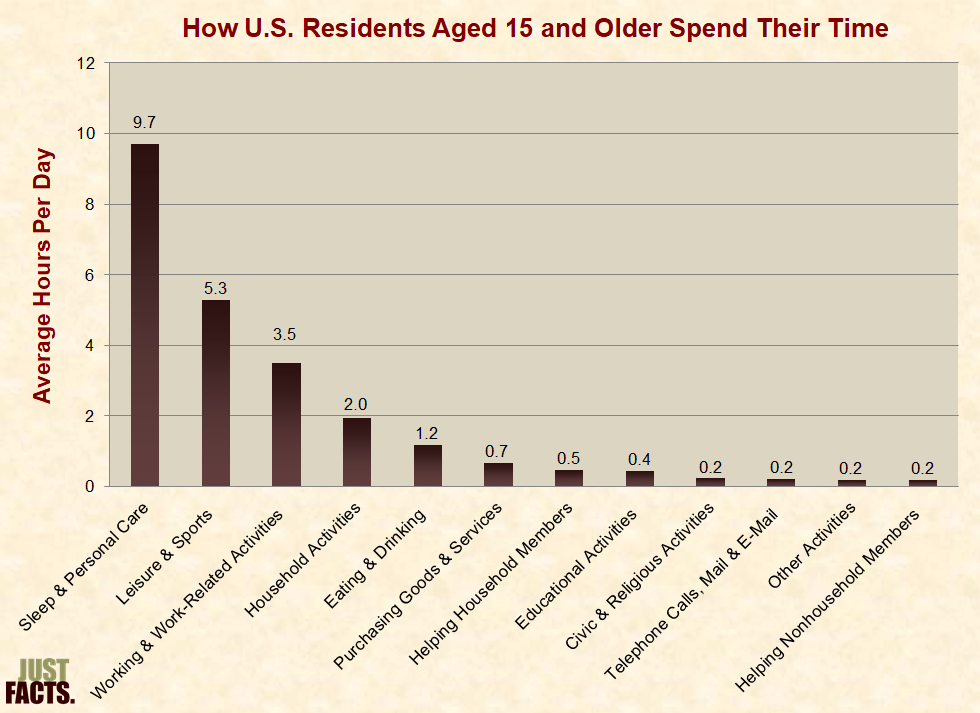

* During 2021, U.S. civilian residents aged 15 and over spent an average of 51% more time on leisure and sports than on paid work and work-related activities:

* During 2021, the U.S. residents of different age groups spent the following hours per day on various activities:

|

Average Hours Per Day Spent on Activities by Age Range |

||||||||

|

Activity |

15–19 |

20–24 |

25–34 |

35–44 |

45–54 |

55–64 |

65–74 |

75+ |

|

Sleep & Personal care |

10.8 |

9.9 |

9.7 |

9.4 |

9.4 |

9.5 |

9.7 |

9.9 |

|

Eating & drinking |

1.1 |

1.2 |

1.1 |

1.1 |

1.2 |

1.3 |

1.3 |

1.4 |

|

Household activities |

0.7 |

1.2 |

1.8 |

1.9 |

2.0 |

2.2 |

2.7 |

2.6 |

|

Purchasing goods & services |

0.5 |

0.7 |

0.6 |

0.6 |

0.7 |

0.7 |

0.8 |

0.7 |

|

Caring for & helping household members |

0.1 |

0.2 |

0.9 |

1.2 |

0.4 |

0.1 |

0.1 |

0.1 |

|

Caring for & helping non-household members |

0.1 |

0.1 |

0.1 |

0.1 |

0.2 |

0.4 |

0.3 |

0.2 |

|

Working & work-related activities |

1.3 |

3.9 |

4.5 |

5.1 |

5.0 |

3.8 |

1.3 |

0.3 |

|

Educational |

3.0 |

1.5 |

0.3 |

0.1 |

0.0 |

0.1 |

–2 |

0.0 |

|

Organizational, civic, & religious activities |

0.2 |

0.1 |

0.1 |

0.2 |

0.2 |

0.3 |

0.4 |

0.4 |

|

Leisure & sports |

5.7 |

4.9 |

4.5 |

3.9 |

4.5 |

5.4 |

6.9 |

7.7 |

|

Telephone calls, mail, & e-mail |

0.4 |

0.2 |

0.2 |

0.1 |

0.2 |

0.2 |

0.3 |

0.3 |

|

Other activities not elsewhere classified |

0.2 |

0.2 |

0.2 |

0.2 |

0.2 |

0.2 |

0.2 |

0.3 |

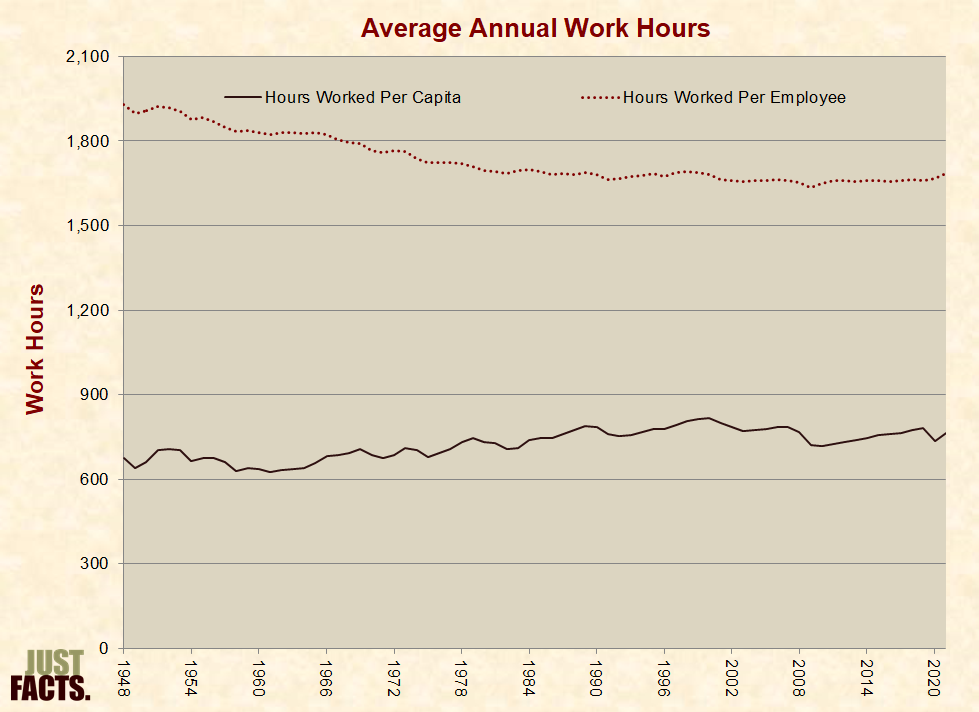

* In 1890, U.S. manufacturing laborers worked an average of 60 hours per week,[571] as compared to 40 hours in 2022.[572]

* In the U.S. from 1948 to 2021, the average annual work hours per employee declined by 13%.[573] Over this period, work hours per employee and per person varied as follows:

* In 2021, full-time workers averaged 8.2 hours of work per day on the days that they worked. This figure was higher on weekdays (8.5 hours) than on weekends or holidays (5.9 hours).[575]

* A 2011 study published by U.S. Bureau of Labor Statistics found that:

* Some of the primary factors that determine employee compensation are:[579]

* Per the U.S. Department of Labor, “In the final four decades of the 20th century, employee compensation, as measured by employer costs, has undergone dramatic shifts” from cash to benefits. Many of these benefits are “legally required” by government, such as Social Security and Medicare.[590]

* Government mandates that force employers to pay for programs like Social Security, Medicare, and the Affordable Care Act (ACA) suppress the wages and salaries of employees. Per the:

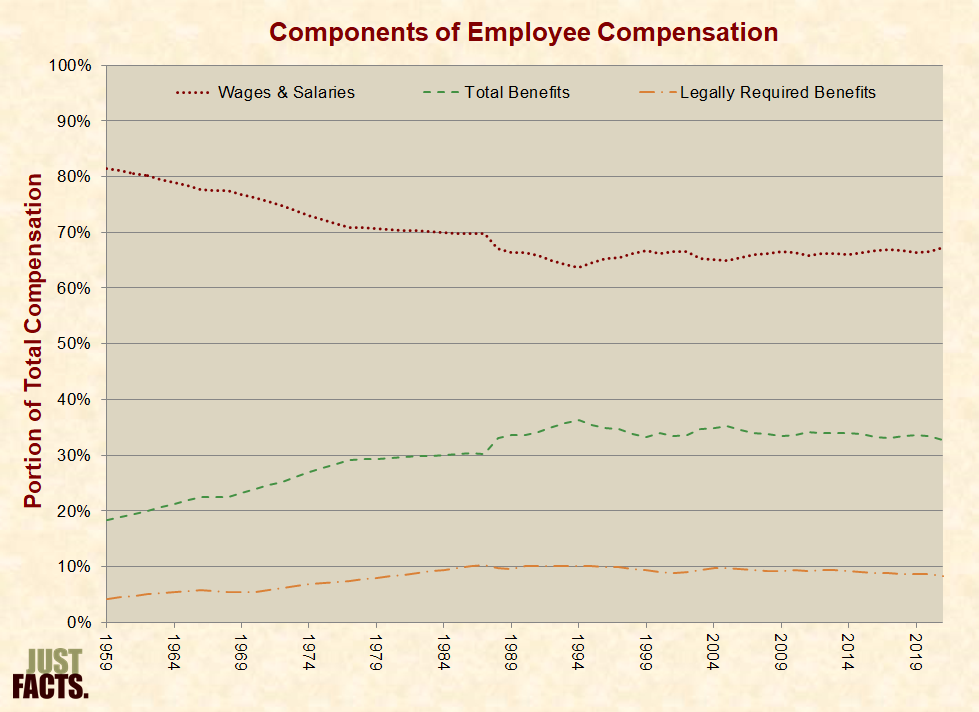

* From 1959 to 2021, the portion of blue collar worker compensation consisting of:

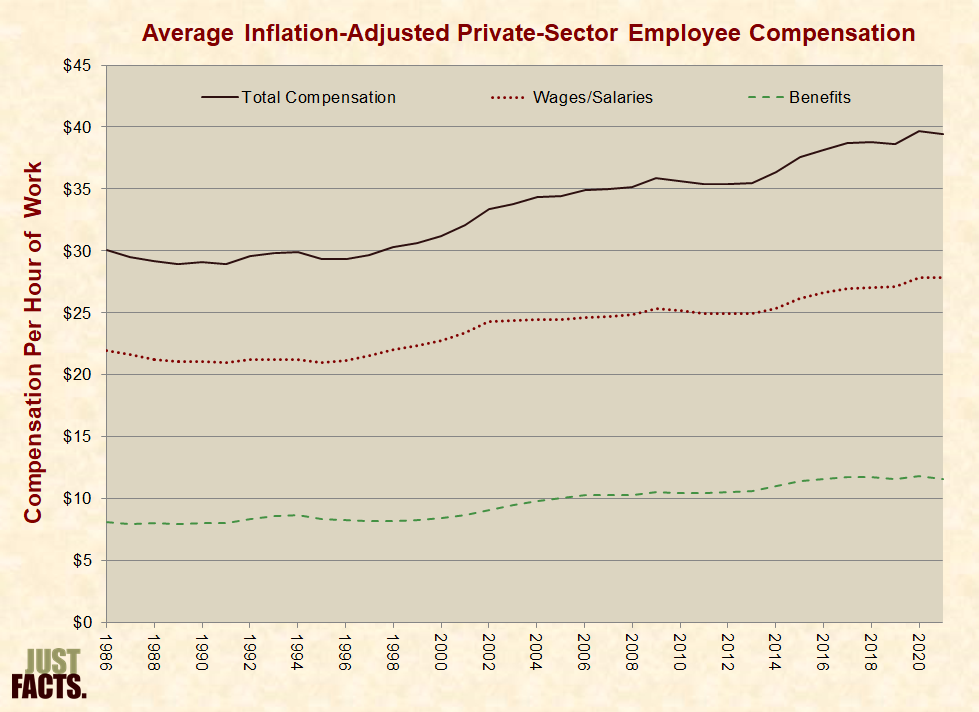

* Adjusted for inflation, the average hourly compensation of private-sector employees (including wages, salaries, and benefits) rose by 31% between 1986 and 2021:

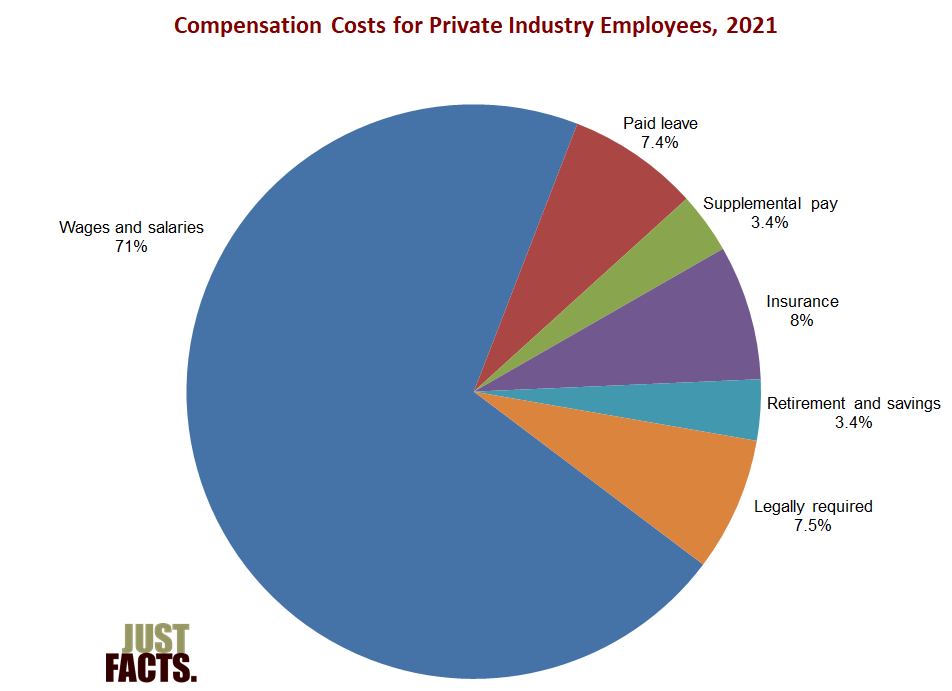

* In 2021, the components of compensation for private industry employees were as follows:

* Adjusted for inflation, average hourly employee compensation rose at the following rates over the time periods below:

|

Inflation-Adjusted Hourly Cost Growth of Employee Compensation |

||

|

Category |

Private Sector |

State and Local |

|

Wages & Salaries |

27% |

22% |

|

Benefits |

43% |

72% |

|

Total |

31% |

37% |

* In 2022, federal, state, and local governments spent $2.21 trillion on employee compensation. This amounts to an average of $17,016 from every household in the United States.[604] [605] [606] [607] [608] [609]

* In 2022, government workers accounted for 15% of all employees in the United States.[610]

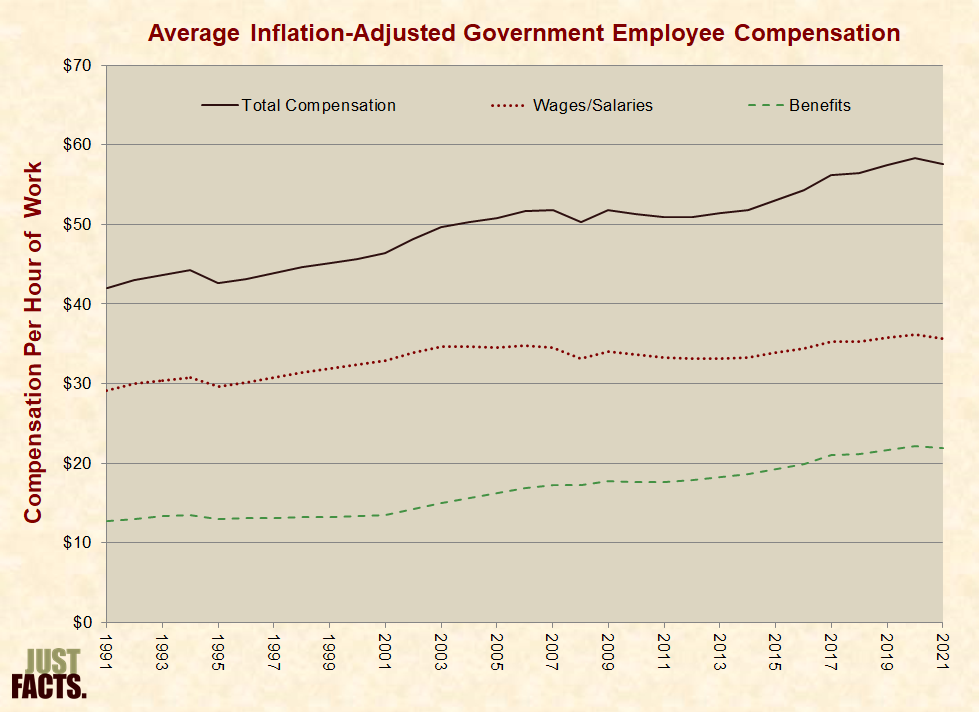

* Adjusted for inflation, the average hourly compensation of government employees (including wages, salaries, and benefits) rose by 31% between 1991 and 2021:

* In 2017, the Congressional Budget Office published a study comparing the compensation of full-time, year-round private sector workers to non-postal, civilian, federal workers in 2011 to 2015. The study accounted for education, occupation, work experience, geographic location, employer size, and various demographic characteristics. The study found that:

|

Federal Employee Compensation Premiums Relative to Private Sector |

|||

|

Formal Education |

Wages |

Benefits |

Total |

|

High School Diploma or Less |

34% |

93% |

53% |

|

Some College |

22% |

80% |

39% |

|

Bachelor’s Degree |

5% |

52% |

21% |

|

Master’s Degree |

–7% |

30% |

5% |

|

Professional Degree or Doctorate |

–24% |

–3% |

–18% |

|

All Levels of Education |

3% |

47% |

17% |

* Click here for an article from Just Facts about the compensation of federal civilian employees and a broad range of studies about this issue.

* Adjusted for inflation, average hourly employee compensation rose at the following rates over the time periods below:

|

Inflation-Adjusted Hourly Cost Growth of Employee Compensation |

||

|

Category |

Private Sector |

State and Local |

|

Wages & Salaries |

27% |

22% |

|

Benefits |

43% |

72% |

|

Total |

31% |

37% |

* In 2013, the journal Public Administration Research published a study comparing the compensation of full-time workers over 50 years of age in government and private sectors during 2006. The study accounted for wages and pensions but not “employment security, paid vacation, health insurance benefits,” and other types of compensation. It found that:

* In 2010, full-time private industry workers worked an average of 12% more hours per year than full-time state and local government workers. This includes time spent working beyond assigned schedules at the workplace and at home.[615]

* For more facts about government employee compensation, visit Just Facts’ research on unions.

* Minimum wage laws force employers to pay certain employees more than the market rate for their services.[616] [617]

* In 1931, the 71st U.S. Congress and Republican President Herbert Hoover enacted the first federal minimum wage law. It required contractors engaged in federal construction projects in excess of $5,000 dollars to pay workers “not less than the prevailing rate of wages for work of a similar nature in” the area.[618]

* In 1938, the 75th U.S. Congress and Democratic President Franklin D. Roosevelt enacted a law that required all employers to pay a minimum wage to most employees “engaged in commerce or in the production of goods for commerce.”[619]

* The 1938 law set the federal minimum wage at $0.25 per hour. Adjusted for inflation, this is equivalent to $5.30 in 2023 dollars.[620] [621]

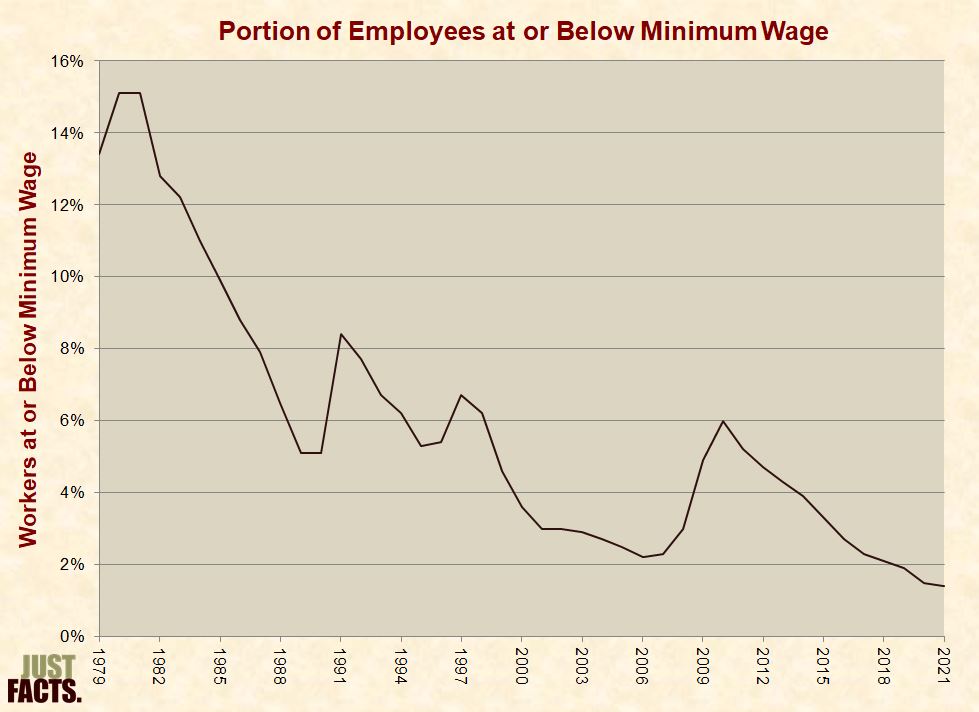

* Since 1938, various federal laws have increased the minimum wage more than 20 times. The latest increase, in July of 2009, brought the minimum wage to $7.25 per hour.[622]

* Adjusted for inflation, the federal minimum wage is currently 37% higher than when it was enacted in 1938.[623]

* Federal minimum wage law has exceptions that “apply under specific circumstances to workers with disabilities, full-time students, youth under age 20 in their first 90 consecutive calendar days of employment, tipped employees and student-learners.”[624]

* Excluding tips, commissions, and overtime pay, 1% of all employees in the U.S. were paid at or below the federal minimum wage in 2021. The rates for different age groups varied as follows:

|

U.S. Employees Paid at or Below Minimum Wage |

||

|

Age Group |

Total |

Portion |

|

16 to 19 Years |

4,776,000 |

4% |

|

20 to 24 Years |

10,377,000 |

3% |

|

25 Years and Older |

60,973,000 |

1% |

* Per the U.S. Bureau of Labor Statistics:

* In 2021, part-time hourly employees—those who worked 34 hours or less—accounted for 48% of employees at or below the federal minimum wage.[627]

* The portion of employees at or below federal minimum wage peaked at 15% in 1980 and 1981. It has since varied as follows:

* As of January 1, 2023:

* While noting there is “considerable uncertainty” about the effects of the minimum wage, a 2019 study by the Congressional Budget Office found that increasing the minimum wage by 65%, or from $7.25 per hour to $12, “would boost wages, but it would also increase joblessness, reduce business income, raise prices, and lower total output in the economy.”[631] With regard to families at different income levels, the study estimated that such a law would:

* The same 2019 Congressional Budget Office study estimated that increasing the minimum wage by more than 100%, or from $7.25 per hour to $15 would:

* A 5.2% increase in reported cash income (or $589) would raise the average total income of families below the poverty line by about 1%. This is because reported cash income accounts for about 19% of their total income, while the other 81% is comprised of unreported cash and non-cash government benefits like Food Stamps, Medicaid, housing, and a wide array of other programs.[636] [637] [638] [639]

* Per a 2014 paper by Ph.D. labor economists David Neumark, J.M. Ian Salas, and William Wascher:[640] [641] [642]

* In 2007, the journal Foundations and Trends in Microeconomics published a review of the “new minimum wage research” that examined 102 studies. This review found that:

* In 2015, the Los Angeles Federation of Labor union helped lead an effort to increase the minimum wage in Los Angeles to $15/hour by 2020. After the city council passed the bill, the same labor union lobbied to change it so that companies with union workers would be exempt from the law.[648]

* For more facts about the effects of governments forcing employers to pay wages that are above market rates, visit Just Facts’ research on unions.

* The U.S. Department of Labor regulates overtime pay, which is 1.5 times an employee’s hourly rate for hours worked over forty hours.[649]

* Executive, administrative and professional workers are among those employees who are exempt from overtime pay regulations.[650]

* In the 2000s, three employees brought a class action lawsuit against IBM for withholding overtime pay from workers that IBM considered to be exempt from the regulations. The company settled the lawsuit for $65 million.[651] [652]

* To prevent future lawsuits, IBM converted 7,000 salaried employees into hourly employees and decreased their base pay by 15% to offset the anticipated overtime costs.[653]

* In 2016, the U.S. Department of Labor, then under the leadership of Barack Obama, enacted a regulation to make overtime pay mandatory for workers earning less than $47,476/year. This was double the previous threshold of $23,660.[654] [655] [656]

* Obama’s regulation was scheduled to take effect on December 1, 2016,[657] but a federal judge granted an injunction before it was implemented.[658]

* In 2017, a federal judge appointed by Obama struck down this regulation,[659] and the Trump administration decided to not appeal this ruling.[660]

* Wealth, or net worth, is the value of assets minus debts at a given point in time, while income is “a flow of purchasing power.” [661] [662] [663] [664] [665]

* Assets include items such as:

* Per the Organization for Economic Cooperation and Development and the U.S. Census Bureau:

* Researchers generally consult two primary sources of information for the wealth of U.S. residents: the Federal Reserve’s Survey of Consumer Finances and Internal Revenue Service tax returns. The Congressional Budget Office and the Census Bureau also publish wealth data.[670] [671] [672] [673] [674] These sources have varying strengths and weaknesses:

* Per the Federal Reserve’s Survey of Consumer Finances:

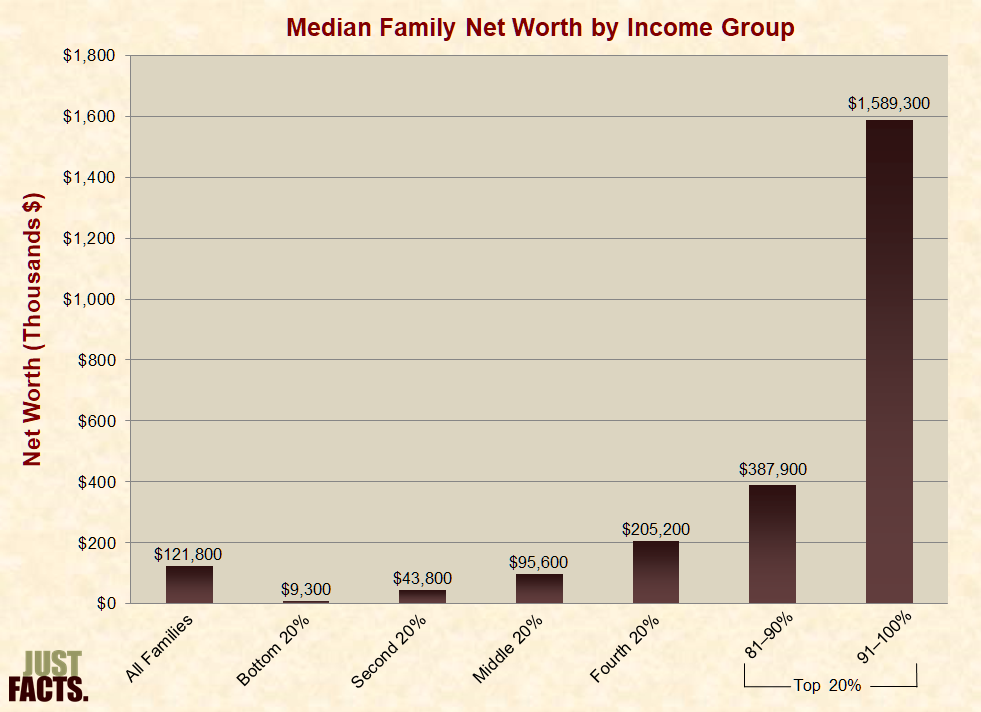

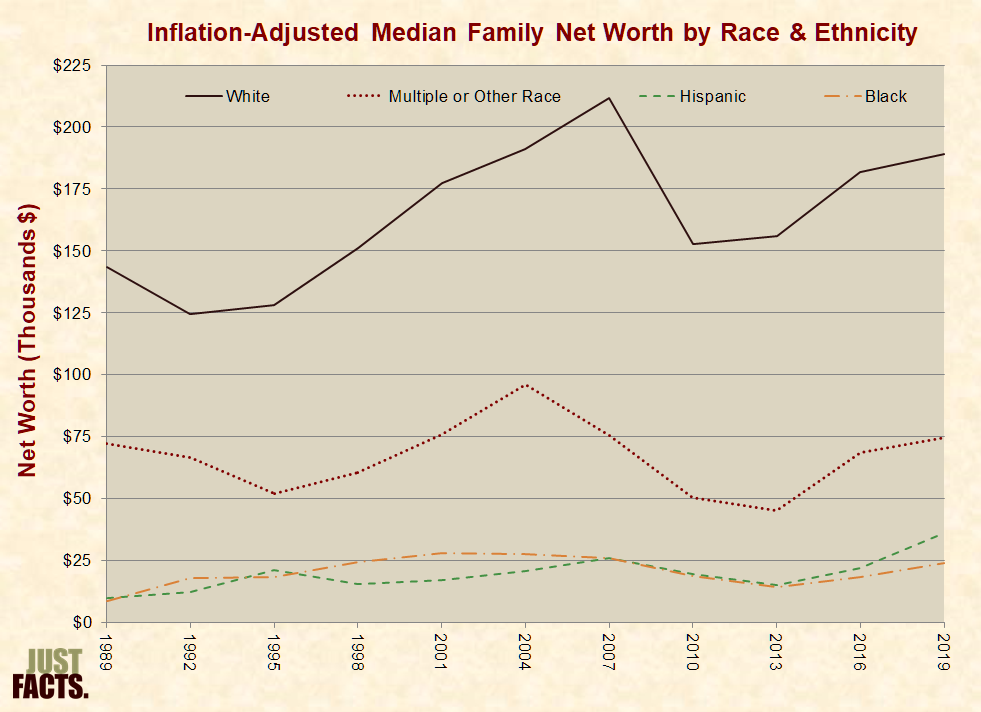

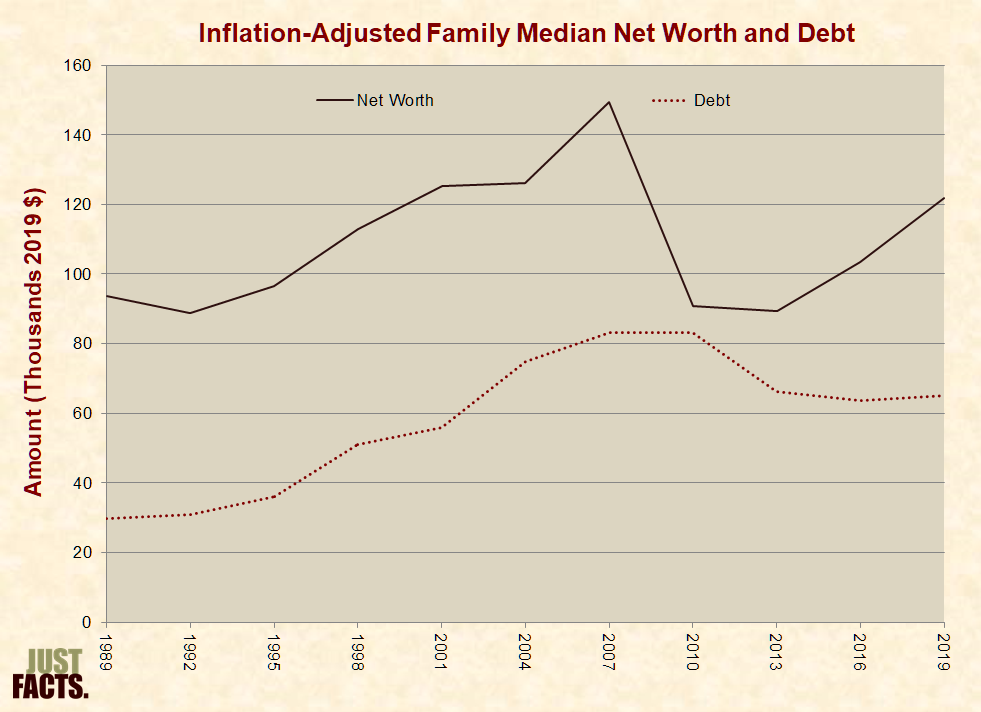

* According to the Federal Reserve’s Survey of Consumer Finances, the median net worth of U.S. families was $121,800 in 2019. The net worth for different income groups varied as follows:

* The inflation-adjusted median net worth of U.S. families increased by 30% from 1989 to 2019. The change in net worth for different wealth groups varied as follows:

* Per a 2017 report by the Federal Reserve:

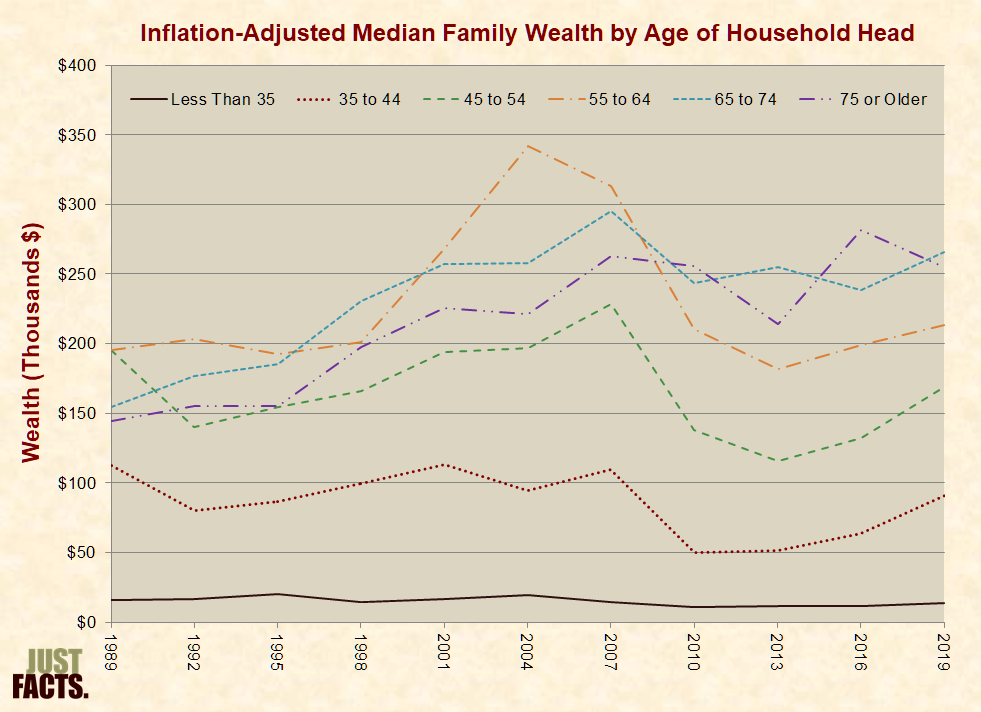

Age

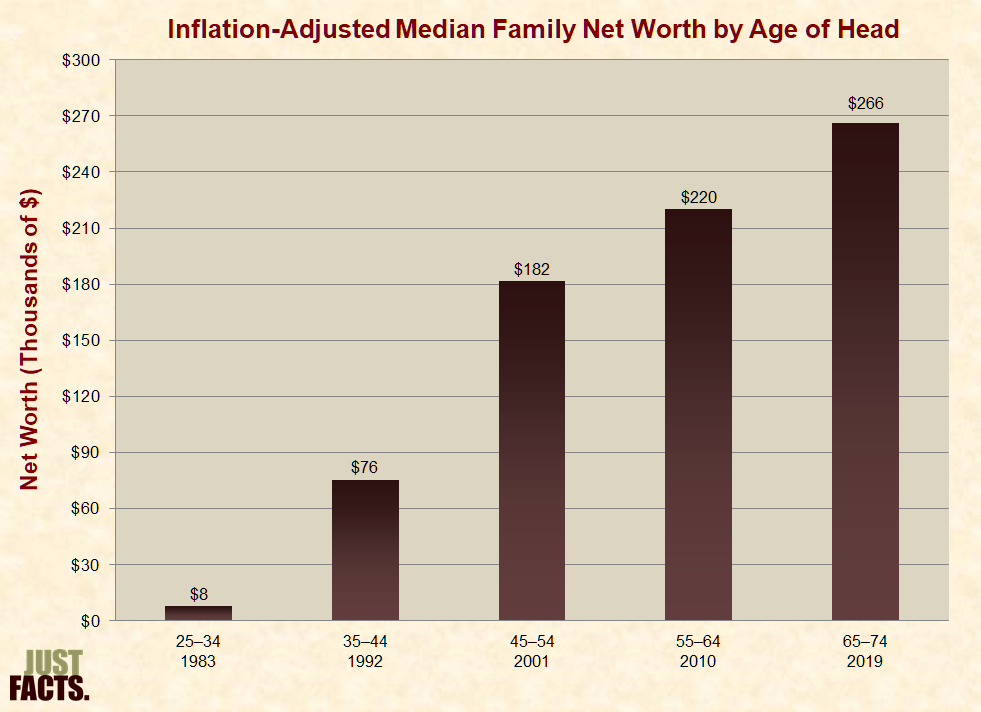

* In 2019, the median wealth of families where the head of household is aged 65 to 74 was 18.2 times that of families under the age of 35:

Education

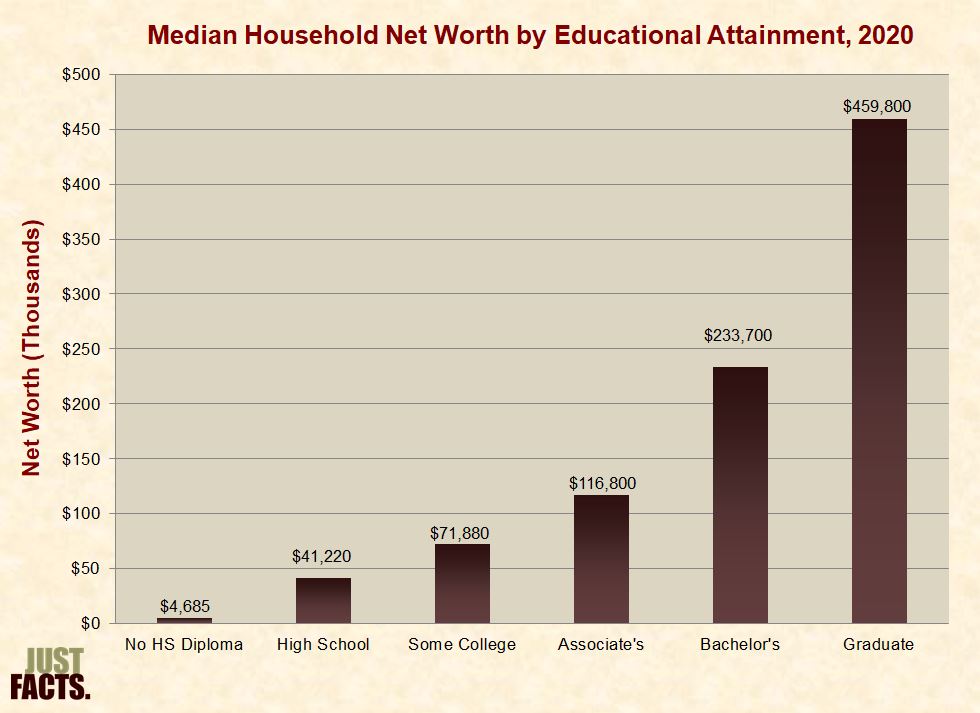

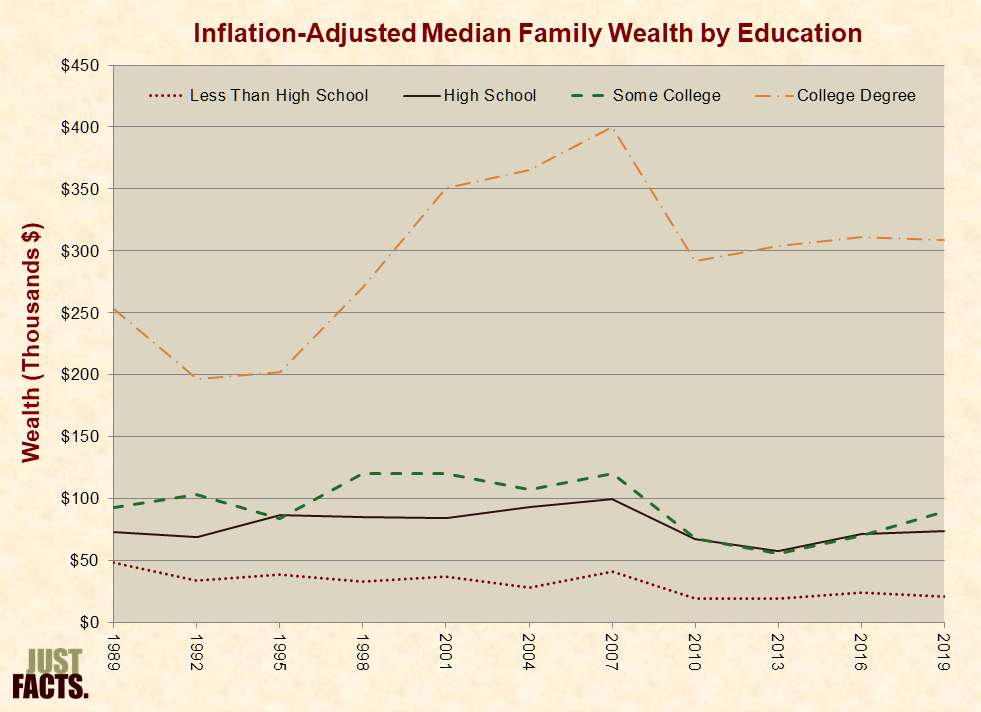

* According to U.S. Census Bureau data, the median net worth of households in which someone had a bachelor’s degree (and no further education) was $233,700 in 2020. The net worth of those with other levels of educational attainment varied as follows:

* Federal Reserve data shows that from 1989 to 2019, inflation-adjusted median family wealth:

Race

* The median net worth of U.S. families was $121,800 in 2019. Family net worth by race and ethnicity varied as follows:

* Data from a 2020 study by the Federal Reserve show that inheritances account for 11% of the median wealth gap between blacks and whites.[698]

Family Structure

* The median net worth of U.S. families was $121,800 in 2019. Net worth by family structure varied as follows:

* In 2021, 75% of working adults reported having “at least some retirement savings,” while about 25% said they had none.[701]

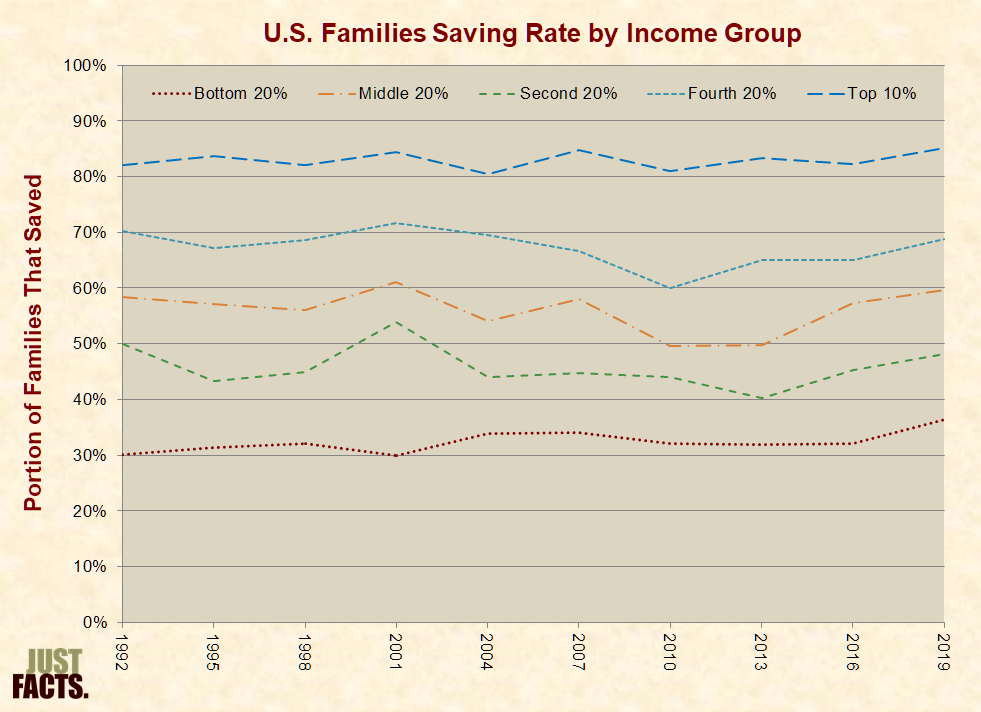

* In 2019, 36% of low-income families were saving some of their income, as compared to 60% of middle-income families. From 1992 to 2019, the portion of families who saved varied as follows:

* Per the Congressional Budget Office:

* The Congressional Budget Office and the Survey of Consumer Finances provide “a series of snapshots of family wealth” rather than “information about changes in the wealth of particular families over time.”[704]

* It is possible to approximate changes in the net worth of particular families over time. For example, many of the 25–34 year-olds interviewed for the 1983 Survey of Consumer Finances were aged 35–44 in the 1992 survey (notwithstanding the deceased and migrants). From 1983 to 2019, this group of families increased their median inflation-adjusted net worth by 33 times:

* In 2018, the Journal of Human Development and Capabilities published a paper that found:

* Per Ph.D. economist Martin Feldstein, professor of economics at Harvard University and President Emeritus of the National Bureau of Economic Research:[708]

* Middle-income U.S. workers are hindered from saving because they are forced to contribute 15.3% of their paychecks to social insurance taxes.[710] If these workers saved and invested one-fifth of these taxes during their careers, each retired worker would have an additional $199,000 to $764,000 in savings today.[711]

* A study published by the University of Chicago Press in 2002 found that Social Security:

* Per the U.S. Federal Deposit Insurance Corporation (FDIC):

* In 2019, 18% of U.S. families’ access to credit was constrained due to denial (11%) and the fear of denial (13%).[715]

* In 1999, Freddie Mac—a government-sponsored enterprise that is tasked to “promote affordable housing”—published a study that measured the rates of “bad credit” among Americans of different races. As defined by the study, people with “bad credit” were those over the past two years who were more than 30 days late paying two bills, more than 90 days late paying one bill, or had a bankruptcy, lien, or judgment. The study, which was based on a scientific sample of 80,000 people, showed that upper-middle income blacks had a higher rate of bad credit than lower-income Asians and whites. For example:

* Per a 2017 study in the Journal of Behavioral and Experimental Finance, the “ability to control impulses is undoubtedly a key factor for long-term success in many areas of life.”[718]

* A 2015 paper by scholars from the International Monetary Fund and the European Central bank found that households who:

* A 2020 study by the Federal Reserve found that 30% of white families in the U.S. have received an inheritance. Adjusted for inflation into 2019 dollars, the median value of these inheritances was $88,500. For various races and ethnicities, inheritances are as follows:

|

Inheritances |

White |

Black |

Hispanic |

Other |

|

Portion Who Received |

30% |

10% |

7% |

18% |

|

Median Value (2019 dollars) |

$88,500 |

85,800 |

$52,200 |

$59,400 |

* Data from the same study show that inheritances account for 11% of the median wealth gap between blacks and whites.[721]

* Per the Department of Housing and Urban Development:

* Some of the downsides of owning a home can include:

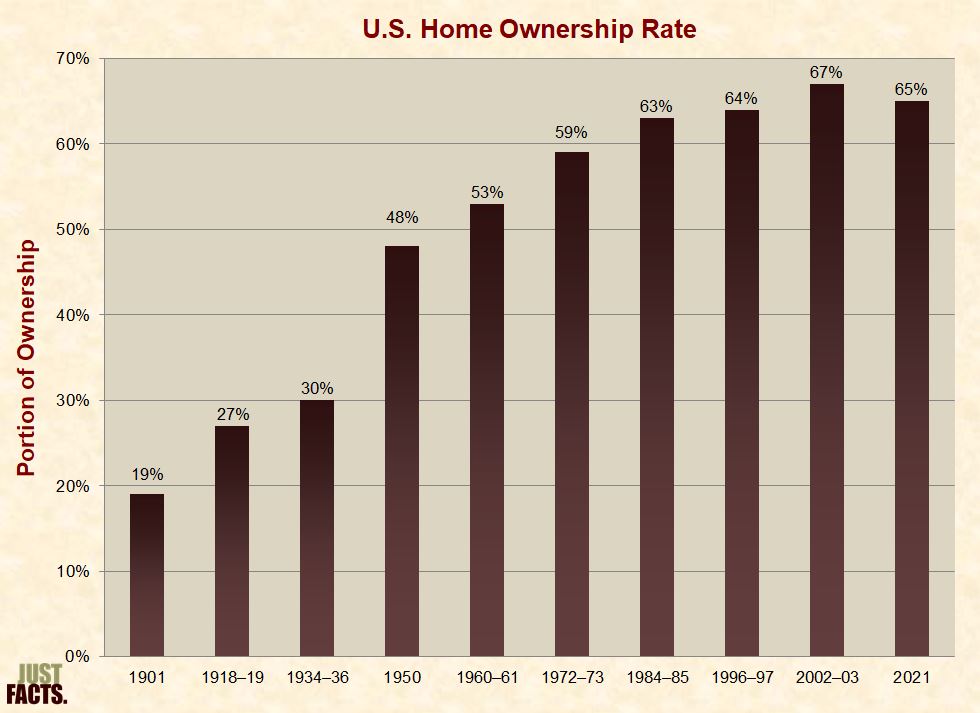

* In 2021, 65% of U.S. households owned their home. Since 1901, home ownership rates have varied as follows:

* Poverty can be measured in absolute or relative terms. Relative poverty is based on comparisons to people living in certain nations or areas, while absolute poverty is based on stable benchmarks.[730] For example:

* Governments originally measured poverty based on people’s consumption of goods and services. They now measure poverty based on people’s “money income” because it is easier for people to report this.[734] [735] [736] [737] Money income:

* The official U.S. poverty rate:

* With regard to the exclusion of noncash benefits from money income:

* With regard to the underreporting of cash income on government household surveys:

* In 2010 (latest data), the poorest 20% of households reported an average of $11,034 in pre-tax money income per household, while they consumed an average of $57,049 of goods and services per household—or 5.2 times their reported money income:

* The official poverty thresholds were developed in 1963–1964 by an economist at the Social Security Administration named Mollie Orshansky. In 1969, the White House Office of Management & Budget made them the formal standard. Per Orshansky:

* The U.S. government uses two “slightly different” poverty benchmarks:

* The Census Bureau poverty thresholds “do not vary geographically, but they are updated for inflation using the Consumer Price Index.”[781]

* Per the Department of Health and Human Services, its:

* In 2022, the Census Bureau poverty thresholds and Health and Human Services poverty guidelines for families or households of different sizes varied as follows:

|

2022 Poverty Measures |

||

|

Family/Household |

Census Thresholds* |

HHS Guidelines† |

|

1 Adult, No Children |

$15,225 |

$13,590 |

|

1 Adult, 1 Child |

$20,172 |

$18,310 |

|

1 Adult, 2 Children |

$23,578 |

$23,030 |

|

1 Adult, 3 Children |

$29,782 |

$27,750 |

|

2 Adults, No Children |

$19,597 |

$18,310 |

|

2 Adults, 1 Child |

$23,556 |

$23,030 |

|

2 Adults, 2 Children |

$29,678 |

$27,750 |

|

2 Adults, 3 Children |

$34,926 |

$32,470 |

|

* Householder under age 65 |

||

|

† 48 Contiguous States and the District of Columbia |

||

* In 2021, the official U.S. poverty rate was 11.6%, representing 38 million people in poverty.[785]

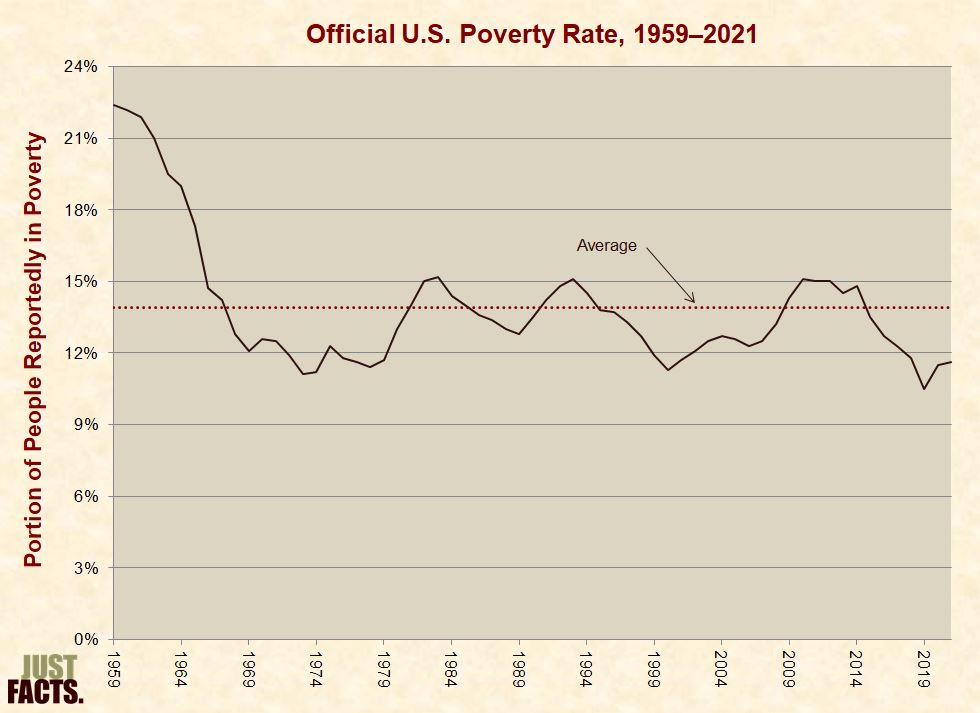

* From 1959 to 2021, the portion of the U.S. population with reported cash income at or below the official federal poverty line ranged from 22.4% to 10.5%, with an average of 13.9%:

* In 2021, the portion of the U.S. population with reported cash income at or below:

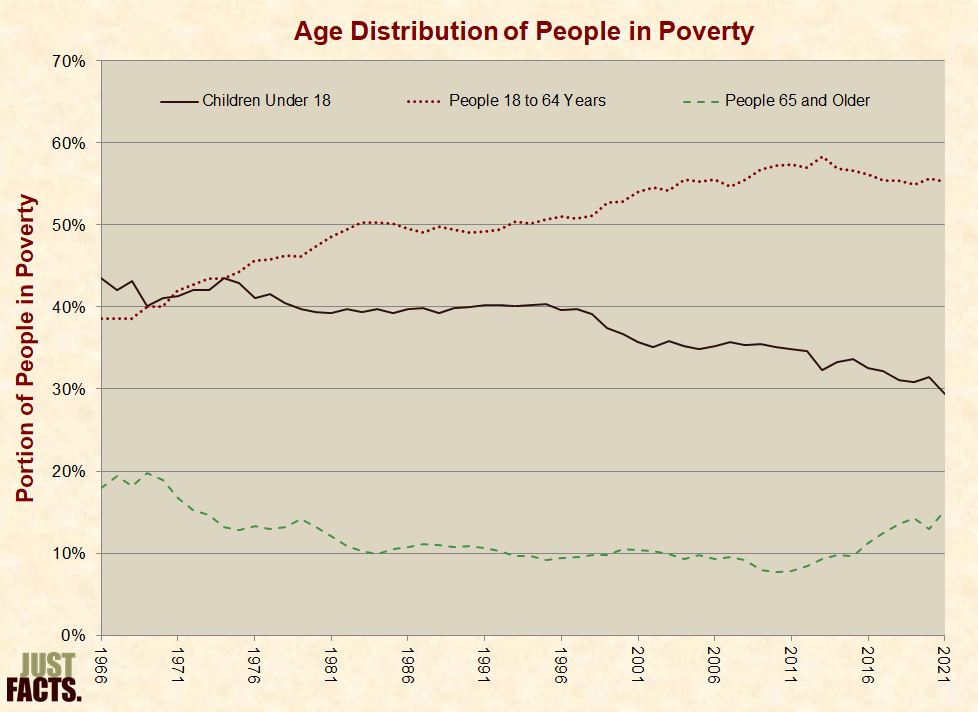

* In 2021, adults aged 18–64 accounted for 55% of people reportedly in poverty. Children under the age of 18 and people above 65 years comprised 29% and 15%, respectively. From 1966 to 2021, the portion of the U.S. population reportedly in poverty varied by age as follows:

* “Means-tested welfare” programs—commonly called “welfare”—provide cash and other benefits to people with incomes and/or assets below certain thresholds. Examples of such include:

* In 2015, the U.S. Government Accountability Office identified 82 federal means-tested welfare programs.[795]

* Seven of the 10 largest federal means-tested welfare programs are “mandatory.”[796] [797] This means they are permanently funded and can spend money without Congress and the president passing new laws. In contrast, Congress and the president typically fund “discretionary” programs for one year at a time.[798] [799]

* In 2020, the federal government spent $869 billion on mandatory means-tested welfare programs, amounting to 81% of all spending “on benefits and services for people with low income.”[800]

* Per the U.S. Government Accountability Office:

* Various government agencies use the Department of Health and Human Services poverty guidelines—or multiples of them—to determine eligibility for at least 31 means-tested programs.[804] Eligibility for the programs below is based on the applicant’s reported income being at or under the following percentages of the HHS poverty guidelines:

* The following programs use other criteria instead of the Health and Human Services guidelines:

* In 2021—amid the Covid-19 pandemic,[811] [812] the federal government spent $1.6 trillion on means-tested welfare.[813] [814] This amounts to:

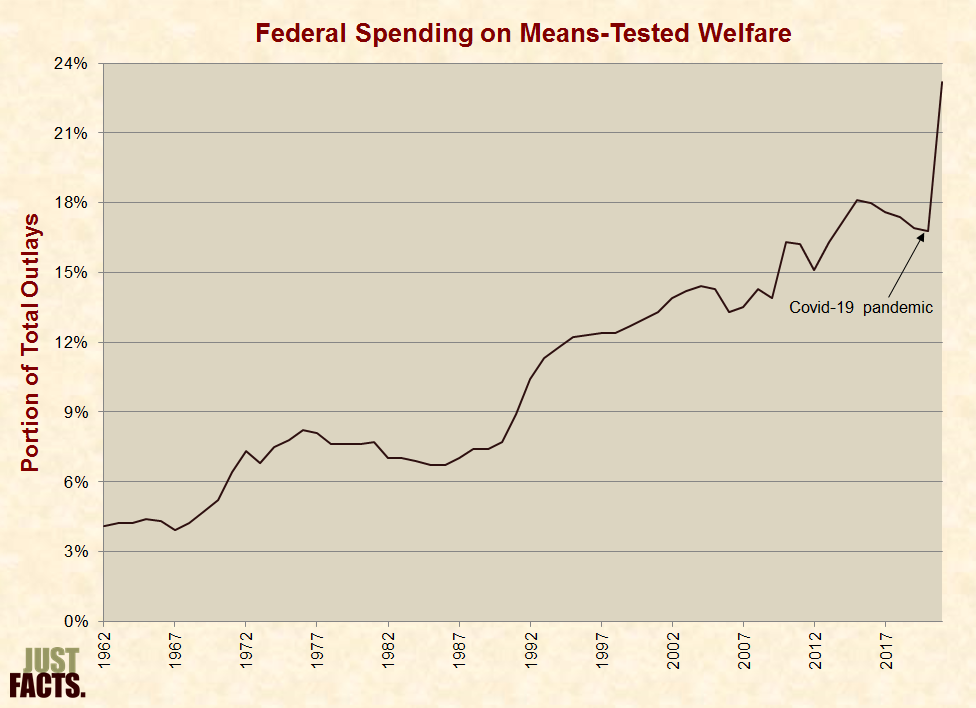

* From 1962 to 2021, spending on means-tested welfare increased from 4% of all federal outlays to 23%:

NOTE: When interpreting the facts in this section, it is important to realize that correlation does not prove causation. This is because numerous factors can affect societal outcomes like poverty, and there is frequently no objective way to identify, measure, and determine the interplay between all of them.

* In 2021, the portion of the U.S. population aged 18–64 with incomes reportedly below Census Bureau poverty thresholds varied by work time as follows:

|

People Aged 18–64 in Poverty by Work Time, 2021 |

|

|

Type of Worker |

Portion |

|

Less Than 1 Week of Work |

30% |

|

Less Than Full-Time Year-Round Workers |

12% |

|

All Workers |

5% |

|

Full-Time Year-Round Workers |

2% |

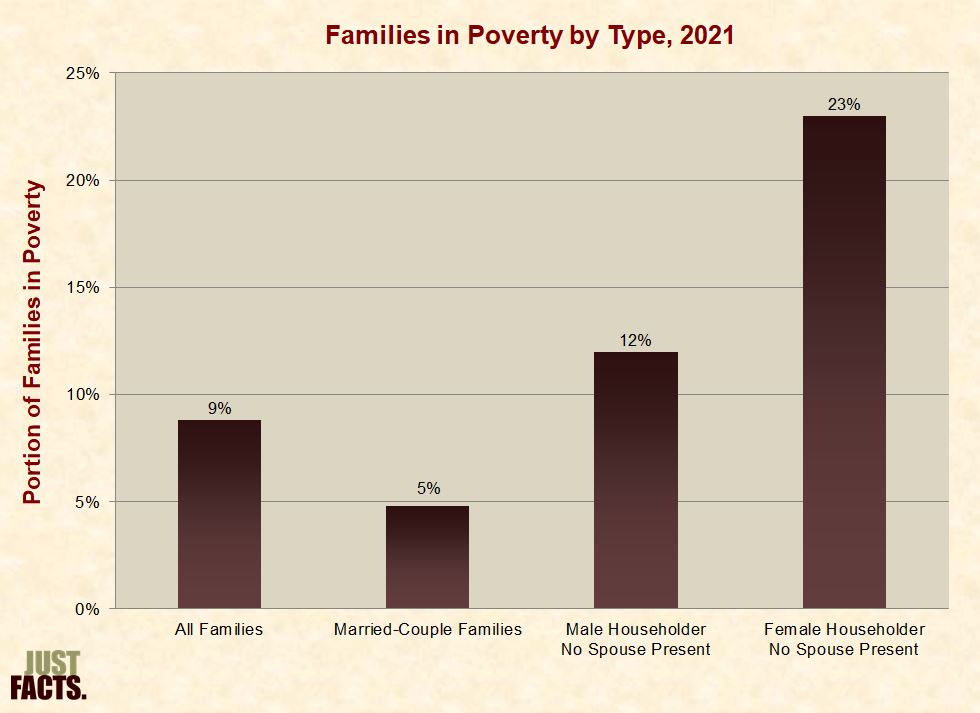

* In 2021, 5% of married-couple families reported incomes below Census Bureau poverty thresholds. The rates for other types of families varied as follows:

* In 2021, the portion of children in families with incomes reportedly below Census Bureau poverty thresholds varied by their family structure as follows:

|

Children in Poverty by Family Structure, 2021 |

|

|

Kind of Family |

Portion |

|

Female Householder |

36% |

|

Male Householder |

18% |

|

Husband–Wife Family |

7% |

* In 2021, the portion of the U.S. population with incomes reportedly below Census Bureau poverty thresholds varied by race as follows:

|

People in Poverty by Race, 2021 |

|

|

Race |

Portion |

|

Black |

20% |

|

Hispanic |

17% |

|

White |

10% |

|

Asian |

9% |

* In 2019—prior to the Covid-19 pandemic—the reported poverty rates for U.S. residents of different races, ethnicities, and marital statuses varied as follows:

|

Race / Ethnicity |

Poverty Rate by Race, Ethnicity, and Marital Status, 2019 |

|||

|

Married, Spouse Present |

Divorced |

Separated |

Never Married |

|

|

White |

6% |

14% |

24% |

13% |

|

Asian |

9% |

13% |

26% |

14% |

|

Black |

9% |

19% |

28% |

21% |

|

Hispanic |

14% |

19% |

34% |

20% |

* In 2021—amid increased government spending on Covid-19 “relief” programs—the reported poverty rates for U.S. residents of different races, ethnicities, and marital statuses varied as follows:

|

Race / Ethnicity |

Poverty Rate by Race, Ethnicity, and Marital Status, 2021 |

|||

|

Married, Spouse Present |

Divorced |

Separated |

Never Married |

|

|

White |

4% |

11% |

12% |

7% |

|

Asian |

7% |

12% |

17% |

11% |

|

Black |

7% |

15% |

16% |

12% |

|

Hispanic |

9% |

13% |

18% |

11% |

* For more facts about poverty and race, visit Just Facts’ research on racial issues.

* In 2021, the portion of the U.S. population aged 18–64 with incomes reportedly below Census Bureau poverty thresholds varied by immigration status as follows:

|

People Aged 18–64 in Poverty by Immigration Status, 2021 |

|

|

Nativity Status |

Portion |

|

Non-Citizen |

17% |

|

Native Born |

10% |

|

Naturalized Citizen |

9% |

* For more facts about poverty and immigration, visit Just Facts’ research on immigration.

* In 2021, the portion of the U.S. population aged 25 and older with incomes reportedly below Census Bureau poverty thresholds varied by educational attainment as follows:

|

People Aged 25 and Older in Poverty by Education, 2021 |

|

|

Educational Attainment |

Portion |

|

No High School Diploma |

27% |

|

High School, No College |

13% |

|

Some College, No Degree |

9% |

|

Bachelor’s Degree or Higher |

4% |

* For more facts about poverty and education, visit Just Facts’ research on education.

* In 2021, the portion of the U.S. population aged 18–64 with incomes reportedly below Census Bureau poverty thresholds varied by disability status as follows:

|

People Aged 18–64 in Poverty by Disability Status, 2021 |

|

|

Disability Status |

Portion |

|

With a Disability |

25% |

|

With No Disability |

9% |

* Per the U.S. Census Bureau:

* Per a 2007 Federal Reserve Board working paper published near the outset of the Great Recession:

* The same Federal Reserve paper states that the increases “in debt–income ratios” make “some households more vulnerable to shocks to” incomes, interest rates, and asset prices.[846]

* Debt can be secured or unsecured.[847] Per the District of Oregon U.S. Bankruptcy Court:

* Some of the consequences of failure to repay unsecured debt are:

* In the fourth quarter of 2022, the average U.S. household owed $144,475 in consumer debt, such as mortgages and credit cards.[850]

* In 2019, 77% of U.S. families had some kind of debt. Among these families, the median debt was $65,000, and:

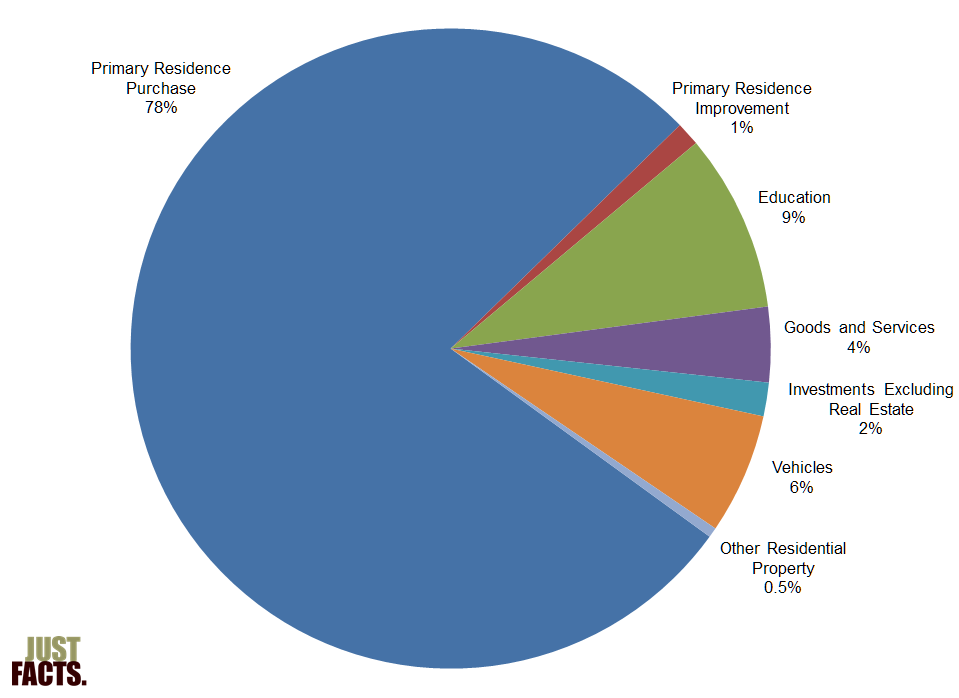

* The most common category of family debt in 2019 was for a primary residence. Other categories varied as follows:

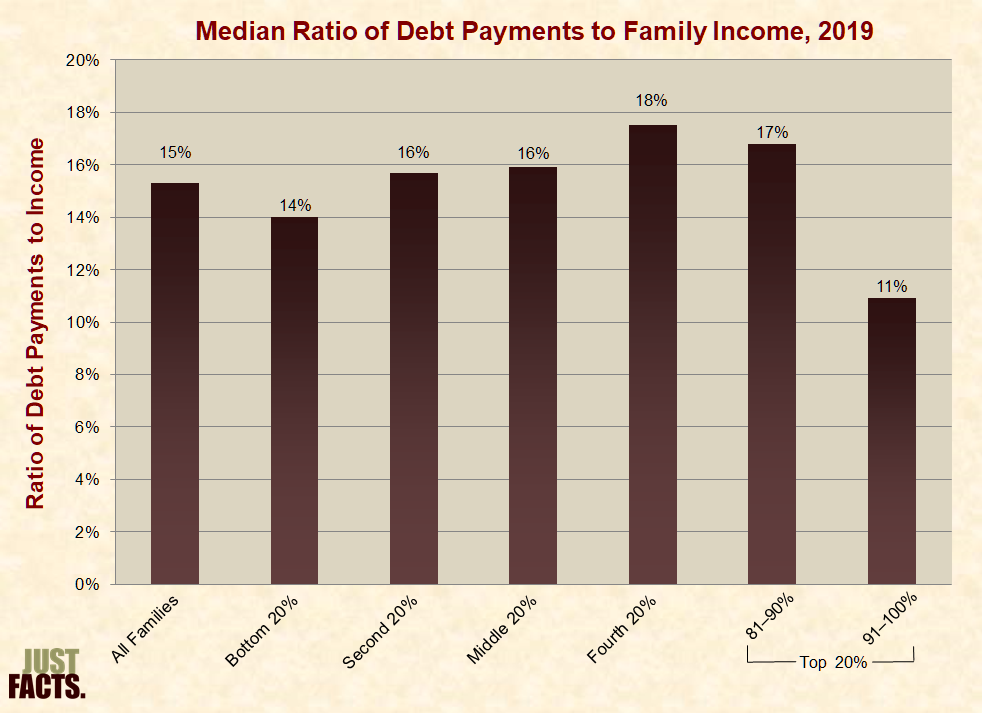

* In 2019, the median ratio of debt payments to family income for families who carried debt was 15%. This varied by family income as follows:

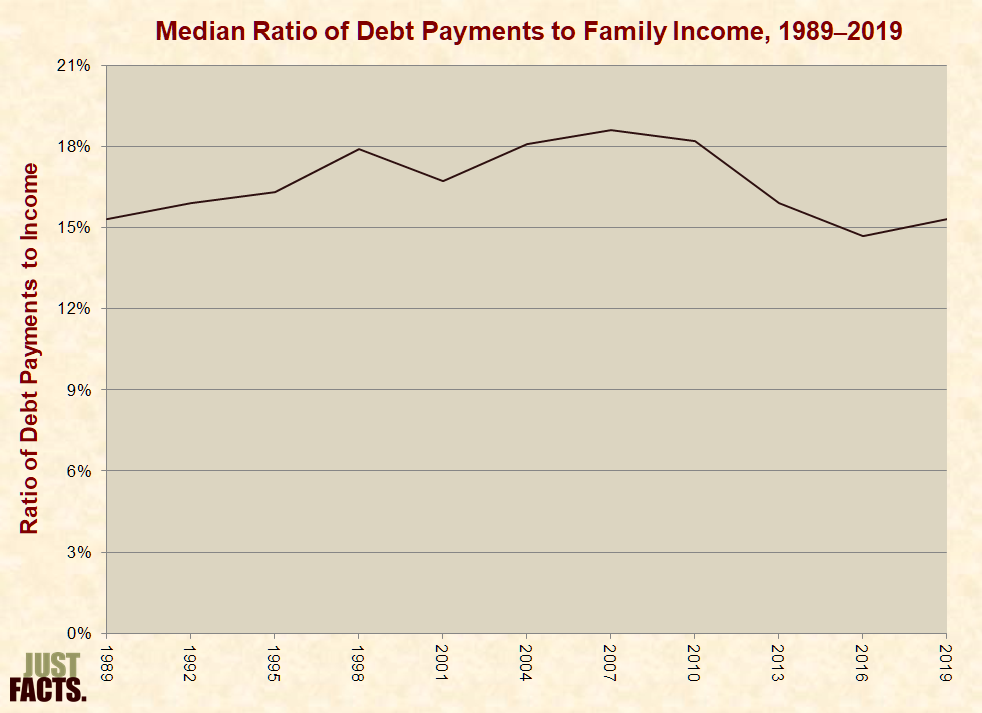

* In 2019, the median ratio of family debt payments was roughly 15%. Since 1989, the ratio has varied as follows:

* In 2016, the Congressional Budget Office reported that during and after the Great Recession:

* Adjusted for inflation, median family debt peaked at $83,200 in 2010. Since 1989, inflation-adjusted median family net worth and debt have varied as follows:

* From 1989 to 2013, the inflation-adjusted average indebtedness of families in debt increased by 256%.[858]

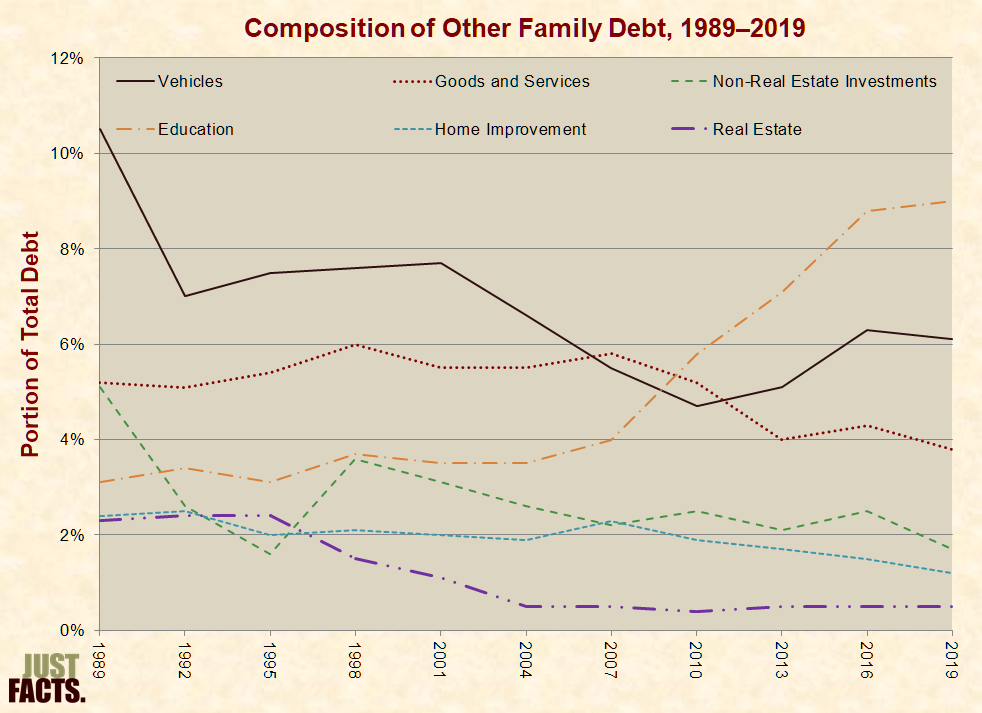

* From 1989 to 2019, the portion of debt payments for the purchase of a primary residence rose from 71% to 78%. The portion of debt payments for other purchases varied as follows:

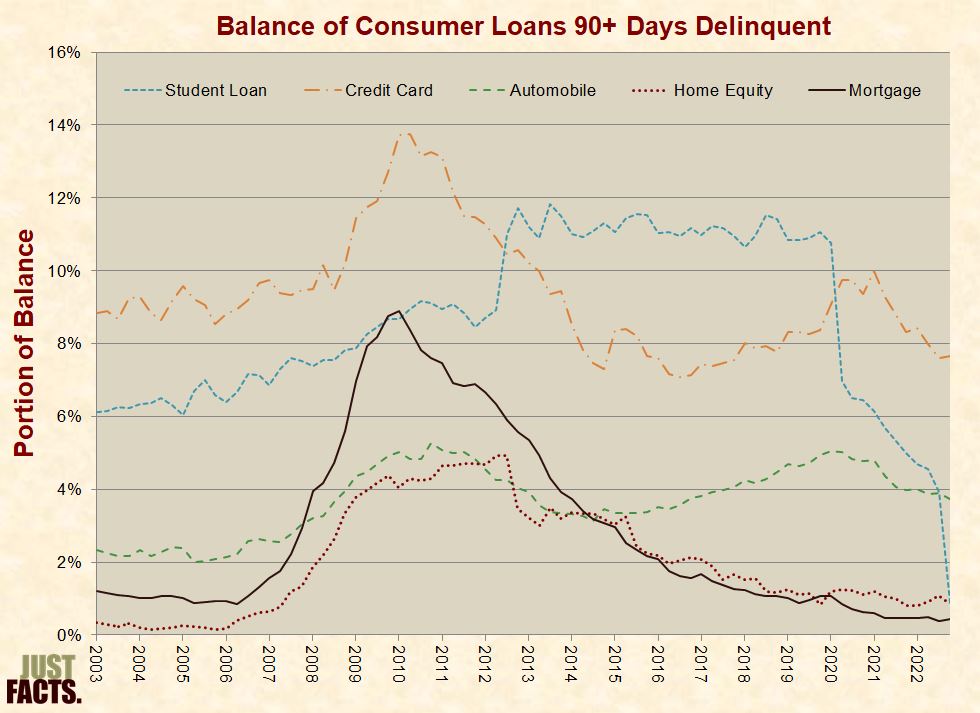

* In 2012, the 90+ day delinquency rate for student loans exceeded that of credit cards for the first time since reliable data on this measure became available in 2003.[861] It remained the most common type of delinquent debt until early 2020 when the federal government passed a law that suspended student loan payments in the wake of the Covid-19 pandemic through September 2020.[862] After this, President Trump and President Biden unilaterally extended this policy:[863]

* For more facts about student loans, visit Just Facts’ research on education.

* Per the Administrative Office of the U.S. Courts:

* Per the Federal Trade Commission:

* In 2005, Congress passed and President Bush signed the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005.[869] The purpose of the bill was to:

* Congress passed this law in response “to many of the factors contributing to the increase in consumer bankruptcy filings,” such as the:

* The law mandated “the implementation and monitoring of”:

* During the Covid-19 pandemic the federal government and banks took actions to prevent bankruptcies.[873] [874]

* Since 2001 personal bankruptcy filings have varied as follows:

* At the close of 2022, the official debt of the United States government was $31.4 trillion ($31,419,689,421,558).[880] This amounted to:

* For comprehensive facts about the national debt, visit Just Facts’ research on this issue.

[1] Article: “Income Tax, Personal.” By David N. Hyman. Encyclopedia of Contemporary American Social Issues, Volume 1: Business and Economy. Edited by Michael Shally-Jensen. ABC-CLIO, 2011. Pages 170–178.

Pages 170–172:

What Is Income?